Cash Payments Vs Digital Payments Statistics and Facts by Payment Methods, Country, Adoption, Recent Developments Insights And Trends (2026)

Updated · Jan 04, 2026

Table of Contents

Introduction

Cash Payments Vs Digital Payments Statistics: Imagine entering a store and making a payment in a cashless manner by just a tap, scan, or click. By 2025, this is no longer a futuristic setting. It has become the norm in many parts of the world. The digital payment era has been developing at an astonishingly fast rate. It has not only changed the whole commercial landscape but also the behaviours and economies of consumers. Despite this rapid shift to digital payment methods, a surprising contrast remains. It lies between the steady decline of cash and the sudden rise of digital alternatives.

This article examines shifts in Cash Payments Vs Digital Payments Statistics through research-based insights and a global perspective. It will not only identify the growing and declining payment methods but also the reasons for the shifts. Furthermore, it will show how it will impact different stakeholders: merchants, customers, and regulators.

Editor’s Choice

- Credit is the leading payment method based on preference, with 82% of credit cardholders liking it, while cash is mainly utilized through necessity rather than the opposite.

- Although alternative digital payment methods have advanced, cash remains prevalent in several regions, particularly in Asia, Africa, and Europe, including Germany, Japan, Italy, and Spain, among others.

- The share of cash in Europe’s point-of-sale transactions has gradually declined, accounting for only 52% of the total in 2024, while cards and online and mobile payments have grown.

- The Asia-Pacific region is a leader in global digital payment adoption, accounting for nearly 66% of total digital wallet spending and experiencing a substantial increase in mobile wallet usage.

- China, India, Indonesia, and Nigeria are among the major countries gradually moving toward a primarily mobile payments ecosystem, as in some markets, smartphones already outnumber cards.

- Digital payments account for 54% of all global transactions, with mobile payments reaching US$8.1 trillion in 2024.

- The global digital payments market is experiencing rapid growth and is projected to increase from US$125.94 billion in 2024 to over US$700 billion by 2034.

- Digital wallets are expected to dominate by 2030, accounting for 65% of global ecommerce payments and 45% of POS transactions worldwide.

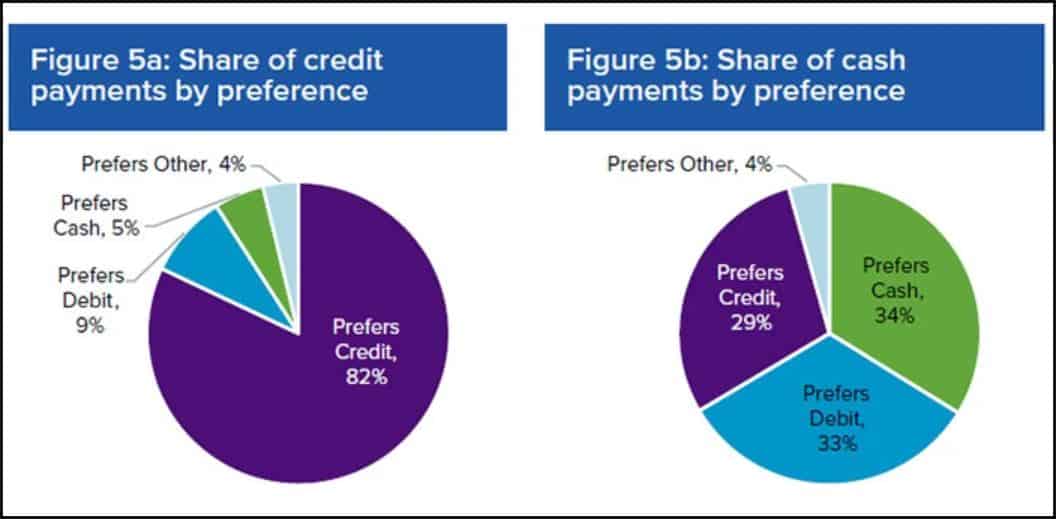

Payment Methods Preferences

(Source: coinlaw.io)

- The data indicate significant congruence between the payment methods consumers adopt and their corresponding preferences, particularly among credit card users.

- The vast majority of credit card users at the point of sale prefer it; 82% report that credit is their favourite mode of payment.

- Only a small percentage of users would like to change to debit (9%) or cash (5%), and merely a few would choose other means.

- This indicates a very high level of satisfaction and loyalty associated with credit, likely attributable to convenience, rewards, and short-term liquidity benefits.

- On the other hand, cash utilisation appears to be much less driven by consumer preferences.

- Approximately one-third (34%) of consumers who use cash prefer it as their preferred payment method.

- Nearly the same proportion (33%) would prefer a debit card, while a large proportion (29%) would favour a credit card.

- This indicates that many consumers use cash because of temporary difficulties—such as lack of access to banking or digital payments—rather than simply preferring it.

- As a result of the comparison, it has become evident that credit is a payment method of choice, whereas cash is often used only because of the lack of other options.

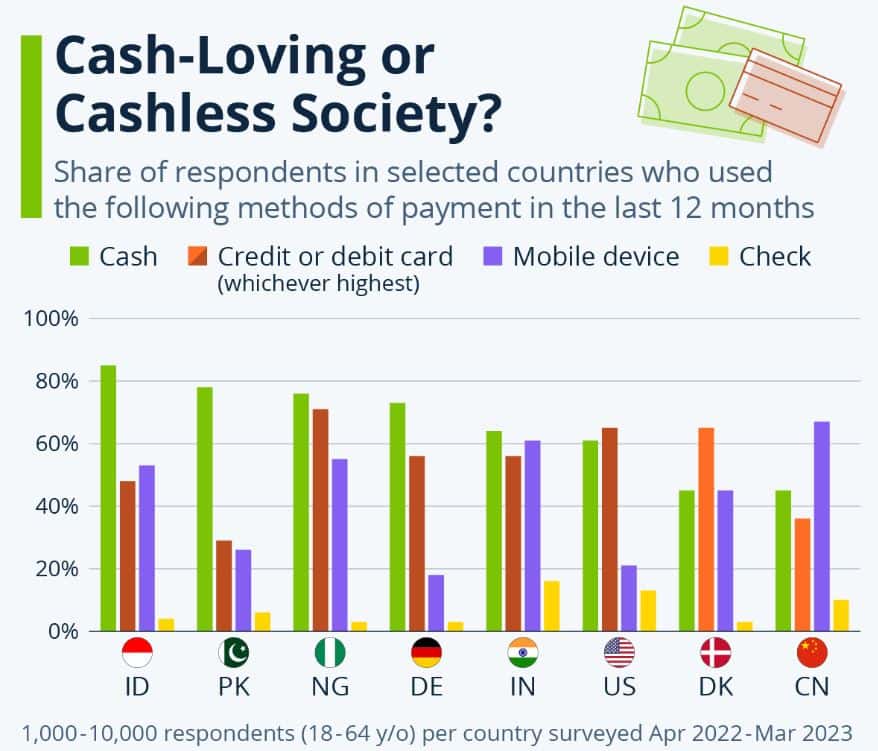

Mode of Payment People Use By Country

(Source: statista.com)

- In many regions globally, cash is still and for a long time will be the most popularly accepted payment method, notwithstanding the increasing variety of payment options available not only in physical stores, restaurants, but also on the internet.

- Western and Northern European countries, along with some nations in the Americas and Oceania, have come close to relying exclusively on card-based transactions, while cash still predominates in most of Asia and Africa.

- Some advanced economies show a clear exception to the general trend of moving to cards.

- In Germany, for instance, 73% of the population said to had used cash in the last year, whereas 56% used debit cards and only 18% opted for mobile payments.

- Comparable trends could be found in Austria, Poland, Italy, Spain, and Japan – all these countries remain strong cash-oriented markets.

- Statista’s Consumer Insights reveal that card payment is still mainly considered the best method in English-speaking countries, Nordic and Benelux countries, and in Brazil, Chile, South Korea, Russia, and France.

- The use of debit cards, contrary to common assumptions about credit cards, is higher than that of credit cards not only in America but also in most other countries included in the survey.

- The countries of Denmark, France, and South Korea were noted as the best markets for credit cards, with these being the only countries in which credit cards were the most frequently used payment method.

- The U.S. did not rank highest for check usage either, as only 13% of Americans utilized checks in the past year, while 14% of Swiss, 16% of Indians, and 20% of French residents reported doing so.

- The most prominent use of mobile payments was seen in China, the sole country in the survey where this method of payment surpassed all other methods, with 67% of the participants having used mobile payments in the last year.

- In the ranking of mobile payment usage, India, Indonesia, and Nigeria followed with high figures, where India and Indonesia even outstripped debit card usage, thus emphasizing the rapid development of m-commerce-based payment environments in these regions.

Denial of Cash In Europe

- Cash’s gradual decline is evident in the euro area, even though it is still very much in use.

- In 2024, cash represented 52% of all point-of-sale transactions, which is a decrease from 59% in 2022.

- During the same time period, card payments increased their proportion to 39%, which is an increase from 34%, showing a consistent transition to electronic payments.

- The trend of online transactions has been even more remarkable, with 21% of all payments in 2024 compared to only 7% in 2019, while mobile payments via apps and digital wallets have increased their share to 6%.

- Nonetheless, cash continues to be the most preferred payment method in most of the eurozone countries.

- It is still the most popular payment method in 14 out of the 20 member states, holding 45- 55% of the market share, on average. Usage is very much country-specific.

- The Netherlands has one of the lowest cash usage rates of approximately 20% of POS payments, while Malta heavily relies on cash, where it still has about 67% of the transaction market.

- The key factors driving the cashless transition are the improvements in card infrastructure and the spread of contactless technology.

Asia-Pacific Adoption

- The Asia-Pacific region is at the forefront of the world in the switch to digital payments, as it is the main market for digital wallets, with 66% of the global use, which is around US$9.8 trillion.

- Digital wallets account for 66% of POS payments in the area, which is a dramatic increase when compared to 50% in 2023.

- Southeast Asia is predicted to experience phenomenal growth, with the mobile wallet user base increasing by 311% and ultimately reaching almost 440 million.

- Among the countries, Indonesia has topped the list with e-wallet usage of 92% followed by the Philippines with 87%.

- The mobile wallet market in the region has been valued at US$4.37 billion, and the growth rate is 26.47% CAGR.

- It is expected that cashless transactions will be 1.5 trillion by the year 202,8, with China, Indonesia, and South Korea taking the lead in influencing the number the most.

- The Asia-Pacific region is also home to 60% of the global digital wallet users, and e-commerce being done through digital payments has grown from 42% in 2014 to 81% now in the region.

- The mobile payments sector is the biggest revenue earner with more than US$31.3 billion and a 38.9% CAGR growth rate, while Hong Kong is the city with the highest digital wallet penetration, nearly 88%.

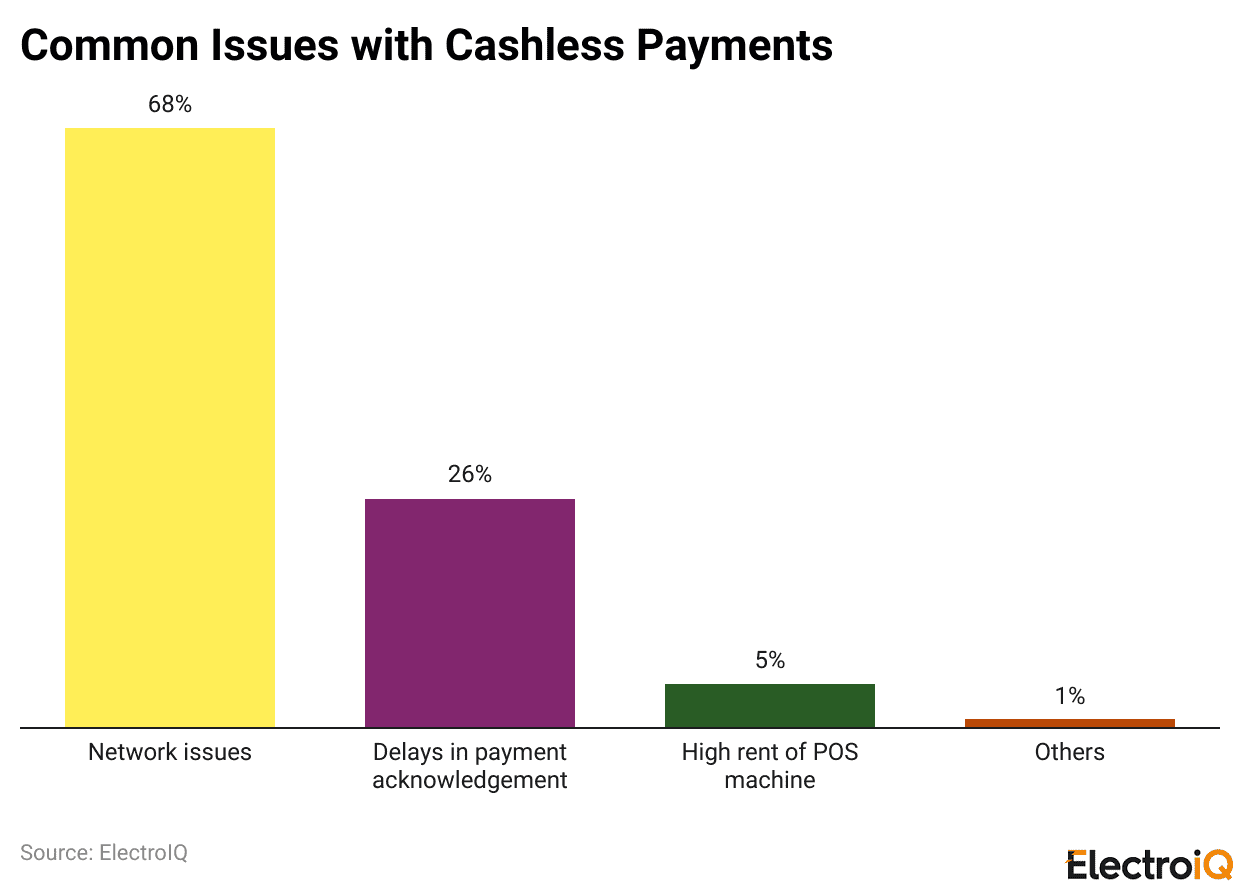

Common Issues With Cashless Payments

- The users of cashless transaction systems are still facing problems despite the fast acceptance of these systems.

- The most common problem is the lack of good network connectivity, which affects 68% of users.

- Another problem that is experienced by 26% of the users is the delay in payment confirmation.

- A small percentage (5%) of users complain about the high rents of POS machines being a factor that slows down the adoption of cashless payments.

- 1% of the total cashless transaction users report other minor issues that interrupt the smooth working of cashless payments.

Transaction Volume Data

- Digital payments have now taken the lion’s share of global transactions, accounting for 54% of all payments globally by 2025.

- Mobile payments reached a whopping US$8.1 trillion in 2024, which shows that they are becoming more and more important in the global payments ecosystem.

- In the euro area, the first half of 2024 saw card usage continuing its upward spiral with 10.3% yearly growth in transaction volume to 40.1 billion payments.

- The total value of those transactions also increased by 7% to some €1.5 trillion.

- The contactless card payments category experienced the fastest growth, as the volume of transactions increased by 13.2% and the value of transactions rose by 13.1% compared to the same period last year (2023).

- By the middle of 2024, 86% of the approximately 20.8 million POS terminals in the euro area were equipped for contactless payments.

- The use of other electronic payment methods has also developed. Credit transfers rose by 7.7% to 15.7 billion transactions, which in total were worth €105.2 trillion in the first half of 2024.

- The number of e-money transactions decreased modestly by 2.7% to 4.2 billion, but their total value increased by 6.6% to around €0.3 trillion.

Value Of Payments

- The digital payments market reached the figure of US$125.94 billion in 2024, and it is still growing very fast due to the expanding acceptance globally.

- From 2025 to 2034, the market will witness a CAGR of about 17.1% and it will be worth US$701.5 billion in 2034.

- The global market for mobile payments only is going to be US$116.14 billion by the year 2025.

- There was a 7% average annual increase in global payment revenues during the period 2019-2024. However, this growth rate has started to decrease due to the changing mix of payment methods.

- With the increasing acceptance of low-fee digital and mobile payments, there is a corresponding decline in the revenue of traditional, high-fee payment methods that are slowly transforming the dynamics of the global payments industry.

Digital Wallets Set To Dominate Global Payments By 2030

(Source: thefinancialbrand.com)

- By the year 2030, it is anticipated that digital wallets will be the major payment method for consumers worldwide.

- Digital wallets will capture 65% of global ecommerce transactions, while in the USA their uptake will be 52%.

- Digital wallets are also extending the adoption at offline points of sale, where it is projected that soon 45% of all transactions globally and 30% in the US will be done through wallet-based payments.

- With the change in acceleration, traditional payment cards are gradually turning into digital, being kept inside digital wallets.

- In the US, credit cards stand out as the most common funding source for digital wallet transactions at 40%, followed by debit cards at 25% and direct bank account links (22%).

- The findings have been derived from the tenth edition of Worldpay’s Global Payments Report, which studies payment behaviour in 40 countries and gives a wide-reaching view of the world.

- The report places digital payments on a wide range, covering digital wallets, account-to-account, buy now, pay later, and even cryptocurrency transactions.

- Digital wallets alone, however, are classified as those payments that are made from both card-based as well as non-card sources.

- The main trigger of such a drastic change was the widespread adoption of smartphones that started with the debut of the iPhone in 2007 and Android devices in 2008, as well as the rapid increase of buy now, pay later, and account-to-account methods and consumer spending in general.

- The research relied on responses from 66,000 consumers globally and was further supported by secondary data and verified by local payment experts.

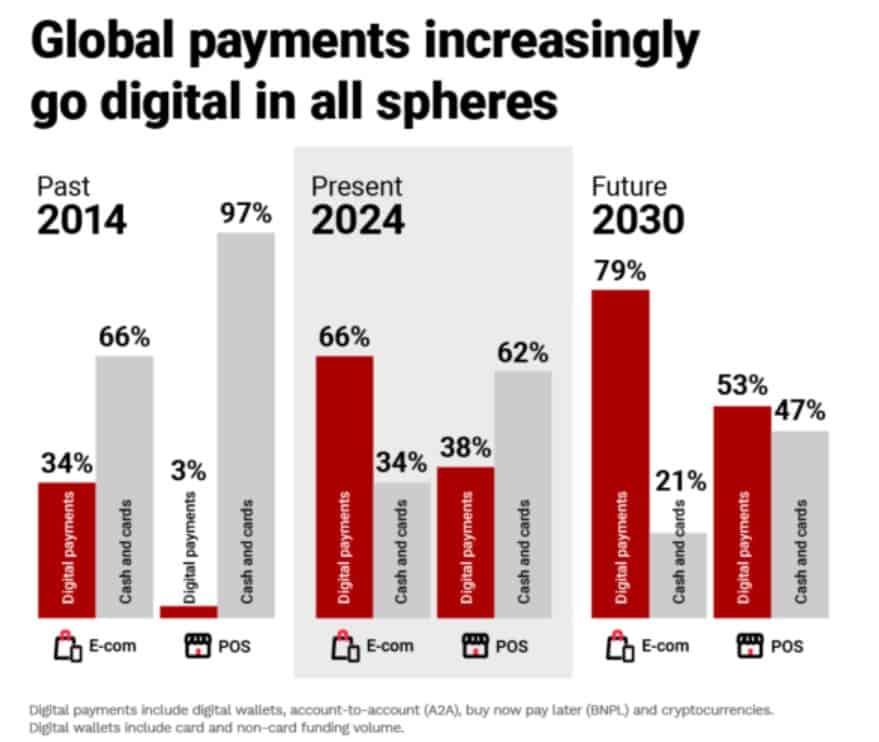

- The report depicts one of the most remarkable developments that has taken place in the past decade – the online payment methods’ preference turning around.

- Ten years back, online transactions were primarily made using cash and cards, which represented 66% of all transactions, while digital was only at 34%.

- Now, the situation is completely reversed, with 66% of the transactions being made through digital channels and only 34% through cash and cards.

- Worldpay’s forecast for 2030 suggests that digital payments will account for 79% of all online sales, which means cash and cards will comprise just 21%.

- It is worth mentioning that the latter category comprises cash-on-delivery payments, prepaid vouchers purchased with cash, and post-pay arrangements where consumers pay in cash upon pickup.

Age Group Preferences

- Mobile and digital payment usage is mainly propelled by the younger generation.

- In the year 2024, people aged 18-24 were responsible for 45% of mobile phone payments made monthly, which is almost twice the national average of 23% for all U.S. consumers combined.

- Gen Z has the highest rate of digital wallet usage, 91% of this age group are active users, and 41% perform more than five transactions every month.

- As for the Millennials and Gen Z, they together contribute the most to mobile and wallet-based payments, and many of them have completely given up on carrying a physical wallet.

- On the other hand, the older demographics (55+) still prefer cash, but they are slowly adopting digital payments.

Income Level Variations

- Payment pattern is another thing that varies significantly by income. Households in the U.S. with an annual income below US$25,000 use cash to pay for approximately 24% of their purchases, whereas this figure is only 9% for households with an income above US$150,000.

- The younger generation, as well as the higher adoption groups, are showing the widespread use of digital wallets, with 91% of adults in the age range of 18 to 26 using them, whereas only about 30% of the elderly Americans are doing the same.

- The usage of digital wallets in the developing regions is increasing very fast, more than 300% in Southeast Asia, and over 90% of the adult population in some Indian cities are already paying through digital wallets.

- However, there is still a sector of the older American population, about 20%, that is not aware of wallet technology yet.

- On the other hand, mobile payment in Africa is increasing at 35% per year, while in Latin America, the adoption of wallets is growing at a rate of 50% per year across all income levels.

Recent Developments

- A global survey in 2025 indicates that cash is steadily being replaced by other payment methods, with cash use in transactions at around 80% of the level recorded in 2019, implying a decline of approximately 4% per annum on average.

- Payment systems that enable instantaneous transactions, which were previously used very little, have become commonplace across major markets and are displacing checks and cash for day-to-day purchases and bill payments.

- Additionally, the global digital payment market is projected to reach approximately US$114.41 billion by 2024, and strong growth is expected to continue for the remainder of the decade.

- The trend of digital payment acceptance among consumers is also broadening: approximately 42% of the global adult population made at least one payment to a digital merchant in 2024, up from 35% in 2021.

- As a result, banks and retailers are not only retaining customers but also upgrading their infrastructure to support them, adding more POS terminals, powering card networks, and accommodating mobile wallet acceptance.

- This is leading to changes in transaction processes, accounting practices, and overall consumer behaviour.

Conclusion

Cash Payments vs Digital Payments Statistics: Cash and digital payments have become contemporary partners in a rapidly changing global payments ecosystem. However, the scale is unquestionably tilted in favour of the latter. Alongside the gradually waning cash-in-hand situation, the necessity of its use in more and more places is diminishing. Though, the necessity eventually vanishes in the case of cashless transactions. Digital payments, such as mobile wallets, are becoming the preferred option in almost all settings. This is due to their spread, speed, and convenience.

The transition is depicted as not complete but only partial, with regional differences, age, and income as determinants. With improved connectivity and the advent of real-time environments, digital channels will be the primary ones in commerce. Retailers and regulators will have to work hard to avoid exclusion, ensure that the use of digital currency is secure and trustworthy, and provide support in an increasingly cashless world.

FAQ.

Digital payments are growing fast due to their convenience and the fact that they are getting widely adopted due to the availability of smartphones. Also, better POS infrastructure, contactless technology, and mobile wallets in the Asia-Pacific especially have all contributed to the faster adoption manifold.

Cash is still the most widely relied upon mode of payment in a good number of areas, irrespective of the surging digital payments. Some of the locations are mainly in the continents of Europe, Asia, and Africa. For example, in the euro area, cash is still more than half of POS transactions, and there are countries like Germany, Japan, and Italy that are very much cash-friendly.

Asia-Pacific remains the number one region globally, contributing almost two-thirds of the spending done by digital wallets. The countries in the region, China, India, Indonesia, and the Philippines, especially, are very much into mobile payment; now digital wallets are not only winning e-commerce transactions but also POS in the region.

Even though the adoption of cashless payments has been quite fast, there are still several challenges that come with it. The majority of users face heavy network connectivity problems, such as payment confirmation delays and POS equipment costs, which also serve to create friction.

The youngest consumers, mainly Gen Z and Millennials, are nearly unanimous in their preference for mobile and digital payments, with many hardly ever using physical cash. Besides, high-income families are more dependent on cards than cash compared to low-income families.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.