Table of Contents

- Introduction

- Editor’ Choice

- Parental Financial Support For Gen Alpha Teens

- Gen Alpha’s Regular Income

- Strong Purchasing Patterns

- Gen Alpha Population And Economic Impact

- Earnings From Chores, Side Hustles, And Part-Time Work

- Spending Power And Annual Expenditure

- Access To Financial Services Among Gen Alpha Teens

- Everyday Spending Categories (Online And Offline)

- Digital Shopping And In-App Purchases

- Influence Of Peers, Influencers, And Social Media On Spending

- Gen Alpha Teens And Early Savings Readiness

- Gen Alpha’s All-Digital Lifestyle

- Recent Changes In Financial Power And Habits Of Gen Alpha

- Conclusion

Introduction

Gen Alpha Financial Behavior Statistics: Generation Alpha (2010-2024) is still young, having no bank accounts or full-time jobs, but their economic influence is already huge. The billions in revenues that they create just through their spending, digital skills, and impact on family purchasing decisions. By 2025, the oldest members of Gen Alpha will be approximately 15 years old, yet they already influence nearly every industry, particularly fintech, gaming, e-commerce, and entertainment.

Reports indicate that Gen Alpha has a global impact on household spending of more than US$500 billion annually. This article provides an exhaustive account of the Gen Alpha financial behavior statistics in 2025, covering their spending areas, financial perception, and entry to the economy as a tech-savvy, investment-oriented generation.

Editor’ Choice

- The majority of parents, about 85%, admit that their Gen Alpha kids have a say in family decisions regarding purchases, and this is often the case when they are as young as 3-4 years old and are already exposed to the digital world.

- Parents remain a significant source of financial support, with 73% intending to finance college education and more than half assisting with car purchases, driving lessons, and early independence costs.

- More than half of Gen Alpha teenagers receive more than US$100 per month in allowance, through paid chores, or through part-time jobs, thereby providing them with early financial independence.

- Income sources for Gen Alpha teens include parental allowances, paid chores, babysitting, tutoring, online reselling, and small side hustles, with 21% already engaging in entrepreneurial activities.

- Gen Alpha represents the largest global generation to date, with approximately 2 billion individuals, accounting for nearly 25% of the world’s population.

- The population of Gen Alpha in the U.S. is approximately 45.6 million, and its total annual spending power is estimated to range from US$28 billion to US$101 billion.

- An average of US$1,300-US$2,100 is spent by families on their kids yearly, thus indicating the financial significance of Gen Alpha.

- Nearly 9 out of 10 Gen Alpha children have been shown to earn personal income, indicating that they are part of the economy at a very young age.

- Most allowances are set at approximately US$45 to US$67 per week, but can reach US$100 or more in affluent families.

- Furthermore, Gen Alpha’s contributions to household purchasing decisions are approximately 42%, with food, entertainment, and daily necessities as the areas where their influence is greatest.

- In terms of savings, Gen Alpha teens are no exception, as 48% of them have more than US$1,000 in savings—beating the Gen Z cohort at the same age.

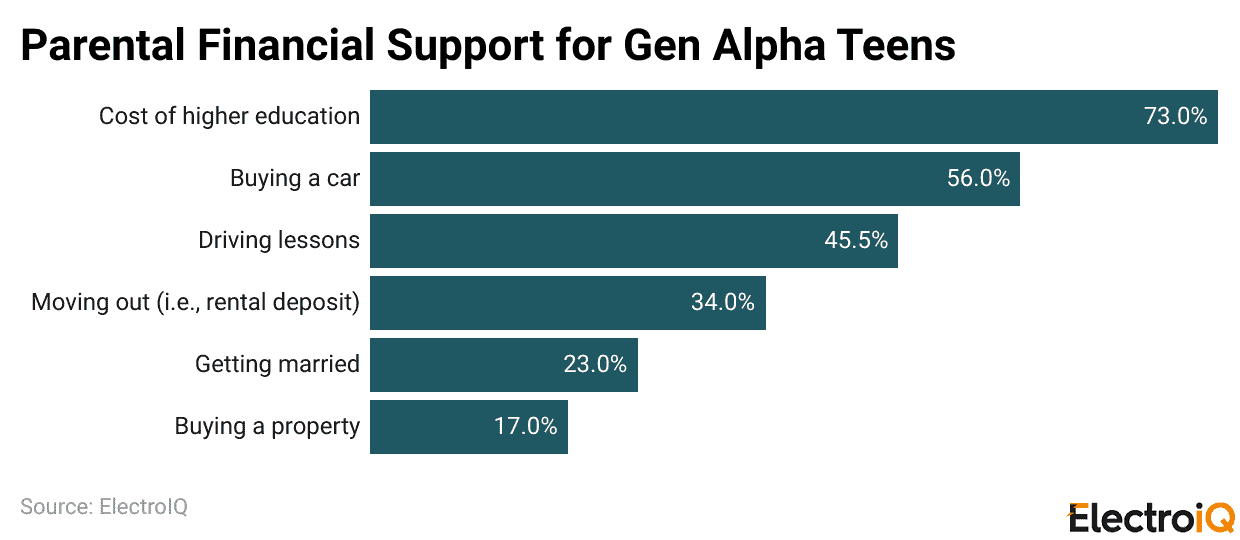

Parental Financial Support For Gen Alpha Teens

(Reference: coinlaw.io)

- During the transition from adolescence to adulthood, parents assume significant financial responsibility.

- The highest financial priority is educational expenses, as almost three-quarters of parents (73%) will cover the costs of higher education, indicating that education is their by far highest priority.

- Additionally, over half of parents (56%) will help with the car purchase, while 45.5% are willing to pay for driving lessons, thereby enabling teenagers to become more independent and travel.

- Only about 34% plan to support moving-out expenses, such as rental deposits, to ease the transition to independent living.

- Smaller but still noteworthy percentages of parents plan for major life events, such as marriage (23%) and buying a house (17%), indicating that parents will remain highly involved in long-term financial decision-making.

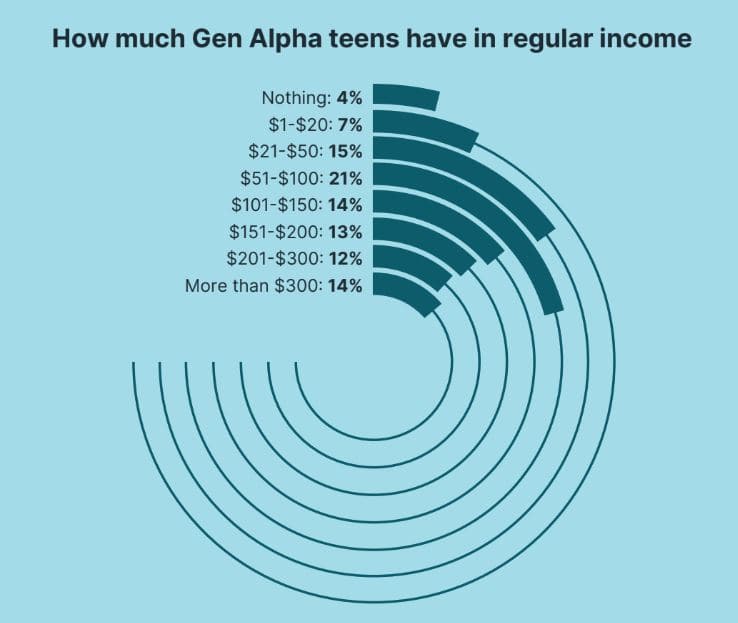

Gen Alpha’s Regular Income

(Source: askattest.com)

- Gen Alpha adolescents are gaining spending power much earlier than any previous generation, and they are also often managing their money.

- More than half receive monthly amounts exceeding US$100, either as allowances, for performing chores, or as part-time jobs, which gives them a strong sense of independence.

- This early money has a great impact on their decision-making, identity expression, and brand interaction.

- Although the most commonly reported monthly income is between US$51 and US$100, there is a huge variation in teen incomes.

- Some receive very little, while another group of teenagers earns a few hundred dollars per month, indicating that financial experiences vary within this cohort.

- Income sources are diverse, ranging from parents’ financial support and paid chores to babysitting and part-time jobs.

- Teens from affluent families are more likely to earn income from tutoring, which is indicative of socioeconomic disparities.

- For many adolescents, early income is empowering for spending and may lead to a generation of youngsters who are less challenging in terms of entrepreneurial skills.

Strong Purchasing Patterns

- Gen Alpha can be considered an active and influential consumer group, primarily due to their increasing financial independence.

- These teens usually possess their own disposable income that gives them comfort in spending money on both online and physical stores, thus sometimes even not necessitating their parents’ help for everyday purchases.

- The majority of 15- to 16-year-olds eat fast food or get takeout at least once a week, and some do that several times a week.

- These expenses demonstrate the teens’ independence, as when they go out for a meal, often, they often pay the bills and are not at home.

- Another area in which they are spending is on digital products. Teens in Gen Alpha often buy in-game items, apps, or digital content.

- They consider digital purchases as valuable as physical goods, indicating that their interaction with the online world is smooth and fast.

- Then there are personal care and cosmetics, which consume a substantial portion of their money.

- The regular buy-ups in this section not only benefit teenagers but also give them the freedom of choice regarding the brands they want to associate with.

- They purchase apparel less frequently than others, yet the frequency remains high enough to indicate concern with fashion and self-expression.

Gen Alpha Population And Economic Impact

- Gen Alpha is the largest and fastest-growing generation globally, estimated to be approximately 2 billion.

- The number of Gen Alpha births per week is approximately 2.5 million, and they constitute almost a quarter of the global population (24.4%).

- In the U.S., the number of Gen Alphas is about 45.6 million.

- In the U.S., their direct spending power is projected to range from US$28 billion to US$101 billion annually, depending on the method used to measure spending.

- On an individual level, Gen Alpha children typically receive a weekly allowance between US$45 and US$67, influenced by age and household income.

- Families also spend heavily on them, averaging US$1,300-US$2,100 per child per year.

- Notably, 91% of Gen Alpha children earn some income, indicating early financial participation.

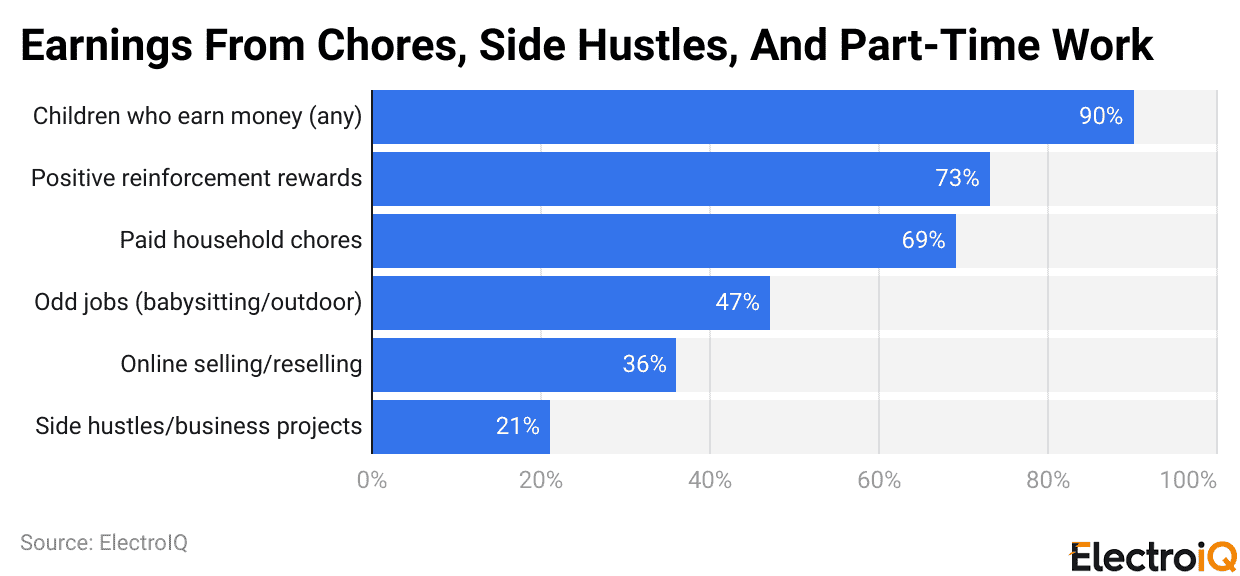

Earnings From Chores, Side Hustles, And Part-Time Work

(Reference: coinlaw.io)

- Gen Alpha children typically receive an allowance of US$45 to US$67 per week, which varies by age and family income.

- Not to mention, families also make substantial expenditures on their children’s behalf, with annual expenditures ranging from US$1,300 to US$2,100.

- Moreover, 91% of Gen Alpha children appear to be financially involved, even if only a small portion of their income.

- To put it differently, when it comes to income generation, the vast majority (90%) of Gen Alpha children report having some source of personal income.

- Some are facilitated by positive rewards, such as 73% earning money for their good behaviour or achievements.

- Another common (and perhaps the most traditional) way of earning is through household chores, which account for 69% of cases.

- Nearly half of the children surveyed have been paid for performing odd jobs such as babysitting or yard work. Digital activity is another area where some children earn income, with 36% earning money by selling or reselling items online.

- Moreover, 21% are upfront about their side hustles, which are small-business projects, showcasing Gen Alpha’s entrepreneurial nature and mindfulness of earning independent income.

Early Access To Money And Allowances

- Especially for older teens, Gen Alpha is now accessing money at an earlier age.

- A little over half of 15–16-year-olds receive more than US$100 per month, and a considerable number receive more than US$300; thus, they have substantial funds to spend.

- The average Gen Alpha child spends approximately US$45 per week, whereas high-income families spend more than US$100.

- Parents typically administer allowances contingent on children completing chores or demonstrating good behaviour, thereby gradually fostering basic money-management skills.

- These habits, in turn, affect household spending, as parents are influenced by their children’s brand and product preferences.

- The regular payment of allowances is associated with greater interest in future side ventures and entrepreneurial activities.

Spending Power And Annual Expenditure

- The weekly allowance for Gen Alpha typically ranges from US$45 to US$67, depending on the child’s age and family income.

- The children, however, apart from their own purchases, remain a factor in approximately 42% of household purchasing decisions.

- The majority of the allowance is spent on daily necessities such as candy and toys, while a smaller but still considerable amount is devoted to dining out and drinking.

- The family’s investment in a child remains substantial, with annual expenses ranging from US$1,300 to US$2,100 per child, reflecting the increasing economic strength of Gen Alpha.

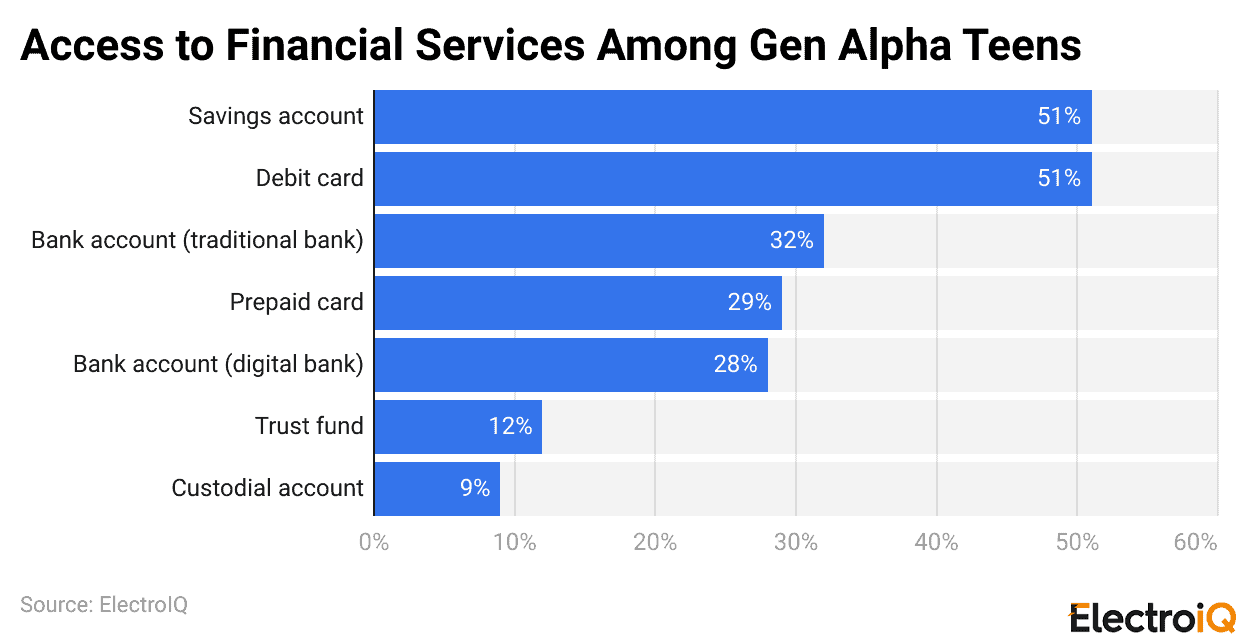

Access To Financial Services Among Gen Alpha Teens

(Reference: coinlaw.io)

- Not-to-Say-That Gen Alpha teens, in some cases, are already formally using financial tools.

- Savings accounts and debit cards constitute half of them, thereby enabling them to manage money online.

- In addition to traditional banking, an increasing number of users are turning to digital banks and prepaid cards for greater flexibility and convenience.

- Some teenagers get long-term financial educational benefits from trust funds or custodial accounts managed by parents.

- All these trends indicate that Gen Alpha is becoming financially literate and digitally comfortable at an earlier stage than their predecessors.

Everyday Spending Categories (Online And Offline)

- A clear differentiation in the spending behaviour among different ages of Gen Alpha is one.

- Children aged 1-5 years, among the youngest group, allocate their entire budget to toys and snacks; this is indicative of both their needs and their parents’ purchasing strategy.

- The same pattern holds for 6-10 years, where toys and snacks still predominate in spending.

- As children enter adolescence (11-14 years), spending shifts toward clothing and electronics, indicating a growing concern with self-expression and the acceptance of new technologies.

- Across all age groups, purchases of snacks and toys remain the most common with allowances, and electronics account for almost one-third of total expenditure.

- Although the younger generation (Gen Alpha) has been extensively exposed to digital media, they still prefer shopping in physical stores.

- However, the trend among older children to notice and purchase beauty products, skincare, and other trend-related items, driven by online discovery, is becoming stronger.

Digital Shopping And In-App Purchases

- Gen Alpha’s consumption patterns are significantly influenced by digital spending.

- In fact, in-game items, apps, and digital downloads are regularly purchased by many teens, and the vast majority of young gamers spend money on virtual goods such as currency and gear.

- The convenience of online shopping becomes increasingly attractive as children grow older, although in-store shopping remains the preferred method overall.

- Product discovery is primarily conducted online, where children watch YouTube videos and influencer clips.

- Early on, Gen Alpha is becoming accustomed to digital transactions, facilitated by universal smartphone access and the increasing adoption of digital wallets.

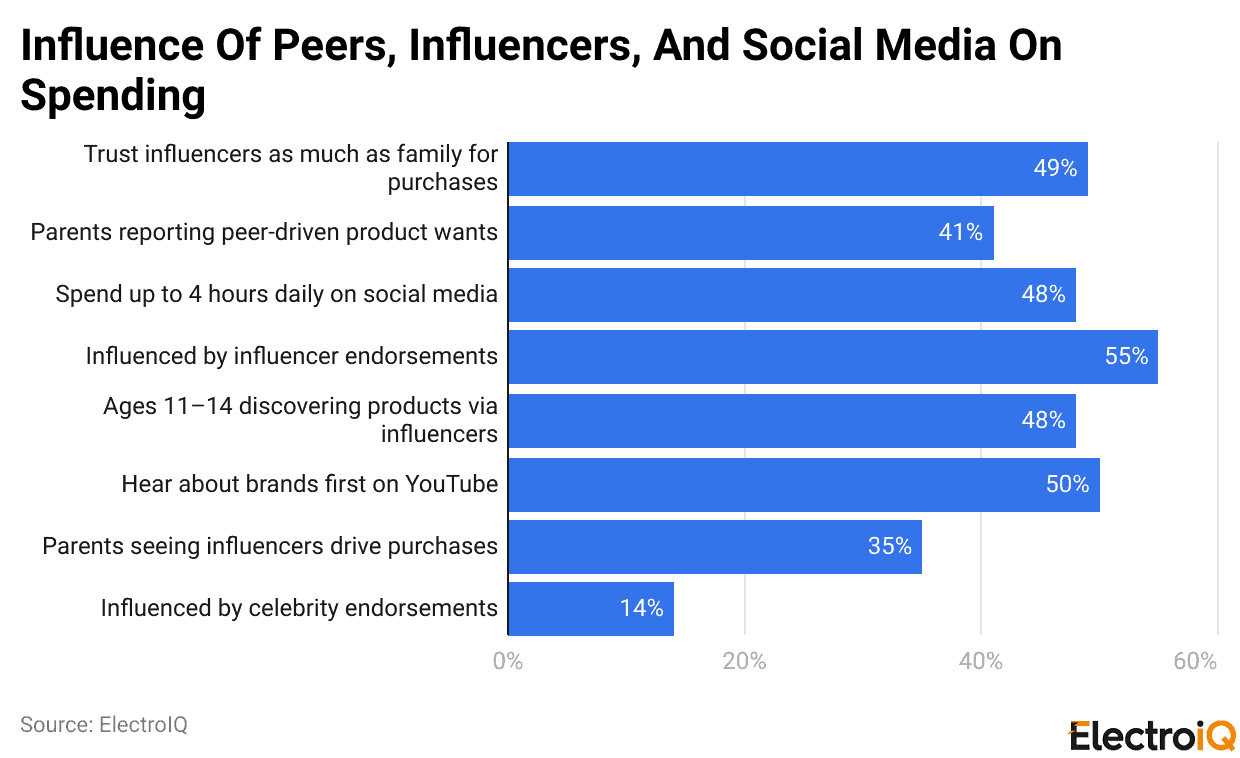

Influence Of Peers, Influencers, And Social Media On Spending

(Reference: coinlaw.io)

- The opinions of peers, influencers, and social media platforms have a significant impact on the purchasing decisions of the younger generation.

- An influencer’s trust among children is nearly the same as that of their family regarding product selection; furthermore, parents often cite children’s peers as the source of their children’s purchase requests.

- Gen Alpha spends considerable time on social media platforms, where influencer advertising often shapes brand recognition and purchase intention.

- YouTube’s power in brand discovery is substantial, whereas celebrity endorsements have a more minor but discernible impact.

- All in all, socializing, whether it is online or offline, is the primary way for Gen Alpha to find out about, judge, and select what to buy.

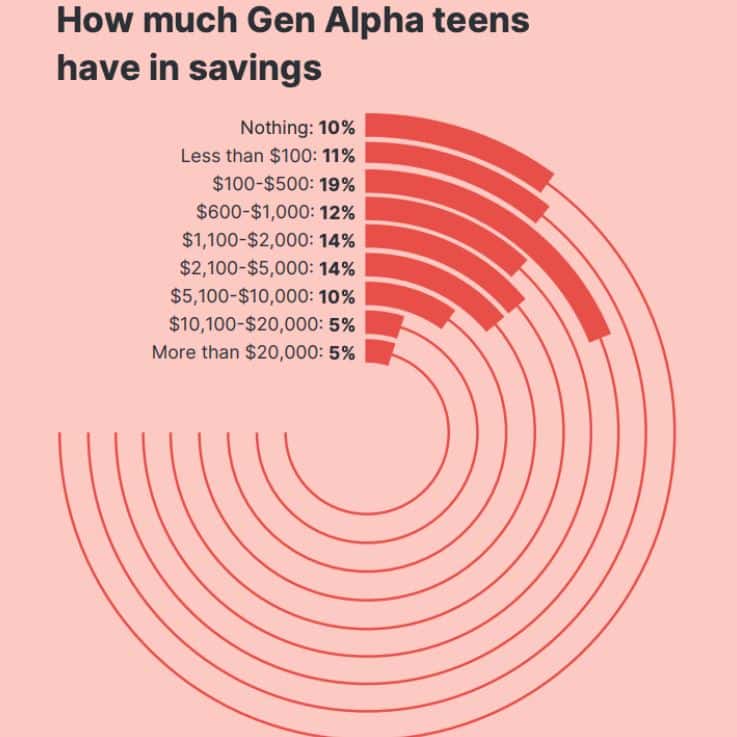

Gen Alpha Teens And Early Savings Readiness

(Source: askattest.com)

- In general, Gen Alpha teenagers have already developed a strong financial consciousness.

- Nearly 50% of them, and even more in some cases, have savings accounts with US$1,000 or more. This indicates that they are much better than Gen Z at saving money, suggesting good control over spending and a strong commitment to saving.

- Besides, this baby boom in savings is presumably a result of the parenting style of Millennial and Gen X parents who have undergone various economic challenges and thus prioritize financial stability.

- A study also supports this argument, stating that being an early saver typically results in becoming a long-term wealthy person by virtue of building up assets.

- Some adolescent savers are not numerous but are significant enough to be considered a group, who sometimes receive their savings through trust funds or parent-managed accounts.

- Youngsters from well-off families are by far the largest group of big savers, while those from poor families are often the ones with very little or no savings and very limited access to formal savings products.

Gen Alpha’s All-Digital Lifestyle

- Generation Alpha teenagers are digital natives, and the majority of their free time is spent on digital platforms, with social media as the primary one.

- More than 50% of them spend more than three hours per day on apps such as TikTok, YouTube, and Snapchat, which constantly expose them to a variety of global ideas, cultures, and viewpoints.

- Such a wide exposure is a key factor that helps them form their own opinions, stay socially aware, and even become trend-setters and discourse-shapers rather than mere consumers of the popular media.

- However, all the time spent on the internet has downsides, such as the risk of social depletion and other negative effects.

- Besides social media, gaming is another big area of activity where quite a few youngsters devote several hours a day to this pastime and even use it as a medium for socializing with friends.

- TV still has an audience, but not as many as in previous generations, while music and podcasts occupy listeners’ ears during shorter, more casual moments.

- Overall, Gen Alpha’s spare time can be seen as a hallmark of a heavily digital, interactive, and socially connected lifestyle.

Recent Changes In Financial Power And Habits Of Gen Alpha

- Recent statistics indicate that the influence of Gen Alpha on family finance has grown significantly, with the children affecting approximately 42% of consumption choices in the U.S., primarily in food and entertainment.

- Alongside regular pocket money, which averages about US$45 per week and can reach US$100 in high-income families, today’s children are more financially savvy and more financially powerful than their peers from previous generations.

- Most of the kids belonging to Gen Alpha are getting involved with the financial system at an early age, sometimes earning savings or debit accounts at 12-14 years old.

- These practices are common among children whose parents experienced economic hardship; consequently, they are more inclined to teach their children financial security.

- Consequently, Gen Alpha is attracted to animated and gamified financial tools, and their propensity to save is strongly correlated with early financial education.

Conclusion

Gen Alpha Financial Behavior Statistics: Generation Alpha is rising as a group of consumers who are financially aware, fluent in digital, and influential in a great way, even before coming of age. Their early access to money, complemented by strong parental counselling and constant exposure to digital platforms, is responsible for developing saving, spending, and earning habits in them earlier than in any previous generation. Their increasing impact on family purchases, ease with digital payments, and use of financial tools all point towards a long-term economic influence.

Financial preparedness may vary across income levels, yet the overall pattern is toward greater financial skills and autonomy. The behaviors of Gen Alpha will thus at no point cease to be a factor for the industries, youth finance and global markets in general.