Medical Debt Statistics By Usage, Age Groups And Parental Status, and Recent Developments (2025)

Updated · Dec 30, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Medical Services Used By People With Medical Debt Platforms

- Medical Debt By Age Groups

- Medical Debt By Parental Status

- Total Medical Debt Owed

- Top Procedures Leading To Medical Debt In The U.S.

- Medical Debt In Collections

- Medical Debt On Credit Reports

- Cost As A Deciding Factor For Medical Care

- Mental Health And Its Relationship With Medical Debt

- Surprise Billing And Medical Debt

- Recent Developments

- Conclusion

Introduction

Medical Debt Statistics: The issue of medical debt – which refers to the financial burden on individuals when they pay for healthcare – has become the most significant economic stressor of the 21st century. In the year 2025, healthcare costs will be higher than before. However, many families and individuals will still be caught in the web of unpaid bills, delayed medical care, and unhealthy financial situations, reaching millions.

In this paper, we have presented the medical debt statistics of 2025. These statistics give a picture of the problem in terms of distribution, economic impact, groups affected, government actions, and health and economic consequences. The statistics reveal a very disturbing trend. There is an upward movement in costs, care becoming more inaccessible, and a loud demand for reform.

Editor’s Choice

- More than 62% of personal bankruptcies are related to medical bills or income loss from illness or caregiving, with 15% connected to a child’s illness.

- Young adults and those in their working years are the most affected, as in the past year, 18% of people below 50 years old had to borrow money for medical reasons.

- People between 50 and 64 years have more medical debt than seniors, because they typically incur high out-of-pocket costs before they get Medicare coverage.

- Medical debts are not only found among the uninsured—22% of covered people still report having medical debt at the moment.

- Those with very young children (38%) and Gen Y (32%) are the most affected by medical debts.

- Being from a higher income group does not mean that one is safe from medical debt—almost one-third of the households with an annual income of US$100,000 or more report medical debts.

- The amount of the medical debt in collections in the U.S. has been estimated to be around US$194–195 billion, which represents 58% of the entire consumer debt in collections.

- Medical debt is reported in one out of five credit reports, frequently for amounts less than US$500, which illustrates how small bills can turn into big ones.

- The first two places of debt in medical treatments are emergency department service (44%) and hospitalization (31%).

- It is estimated that 36% of families are in debt due to medical services, and 21% have at least one medical bill that is past due.

- The majority of the families pay the doctors through instalment plans or by relying on credit, with 17% using loans or credit cards and 15% being contacted by debt collectors. Medical debt is the main reason behind 36% of adults’ postponement or skipping of medical care.

- Last year, 31 million Americans took out US$74 billion in medical bills. Credit reporting policy changes resulted in the elimination of paid-up debts and balances under US$500, helping millions to prevent long-term credit damage.

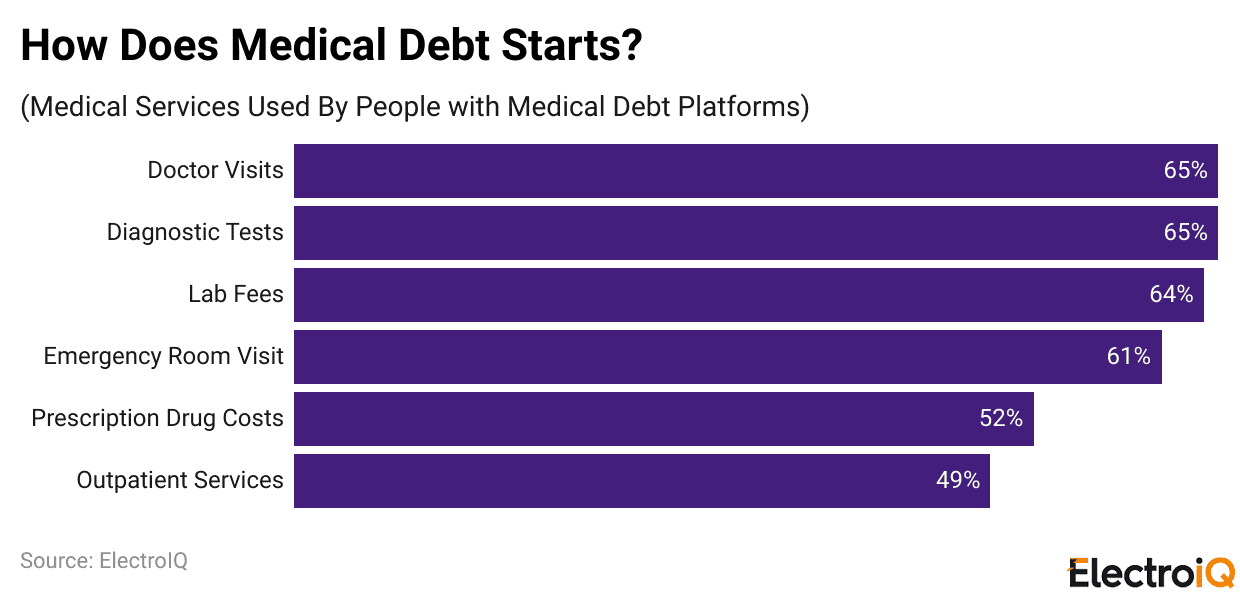

Medical Services Used By People With Medical Debt Platforms

(Reference: singlecare.com)

- According to the survey results, medical debt is quite often the main reason for serious financial difficulties and, in some cases, even bankruptcy for a large portion of Americans.

- A key factor is the combo of hefty medical bills and income loss due to either sickness or taking care of someone sick.

- More than 62% of the people who went through bankruptcy stated that medical expenses or income loss due to sickness or taking care of someone were the main reasons for their bankruptcy.

- Even the families with kids face financial pressure due to medical costs, and nearly 15% of medical bankruptcies were caused by a child’s disease.

- The findings also suggest that medical debt is not always associated with extreme medical expenses. A survey reported that about 10% of people who had trouble paying their medical bills owed US$500 or less, which indicates that even the small amounts can turn out as unmanageable and that too especially for the financially troubled households.

- Survey results showed that routine and commonly used healthcare services ranked among the top contributors to medical debt.

- Doctor visits, diagnostic tests, lab fees, and short hospital stays each affected around two-thirds of the respondents.

- Emergency room visits, prescription drugs, outpatient services, and dental care were also very common causes.

- The overall picture painted by these findings is that financial stress and long-term debt are not only the results of major medical events, but also that everyday healthcare needs can trigger such situations.

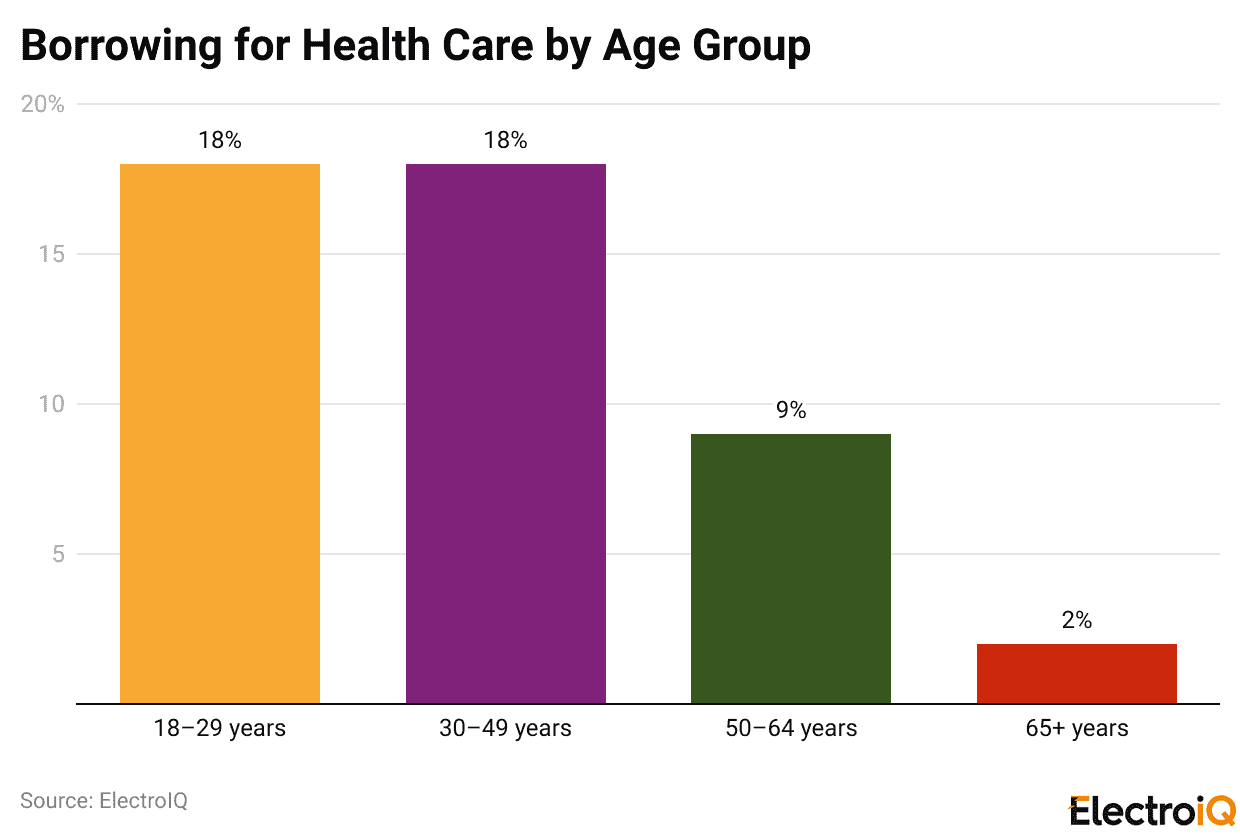

Medical Debt By Age Groups

(Reference: coinlaw.io)

- The data clearly illustrate the differences between the various age groups regarding health care costs and medical debt management among Americans.

- The younger and working-class adults are significantly more inclined to resort to loans to meet medical expenses.

- Last year, nearly 18% of people aged 18 to 29 and the same percentage of people aged 30 to 49 indicated that they needed to borrow money for health care, which is indicative of having limited savings and undertaking continuous financial responsibilities like paying rent, taking care of children, or repaying student loans.

- With ageing, however, the need for borrowing money for medical care decreases very quickly, at a rate of only 9% among individuals aged 50–64 and 2% among people aged 65 or over.

- On the other hand, lesser borrowing amongst seniors does not automatically imply lesser financial pressure for them.

- People aged 50-64 have greater medical debt than those aged 65 and above, mainly because they are not yet eligible for Medicare and, therefore, have to pay higher out-of-pocket costs.

- Young households are most exposed to this situation since they are the ones most likely to accumulate medical debt or resort to borrowing to finance their expenses.

- It is worth mentioning that medical debt is not only a problem for the uninsured, as 22% of insured people admit having medical debt, thus emphasising the issue of access to health care and its affordability.

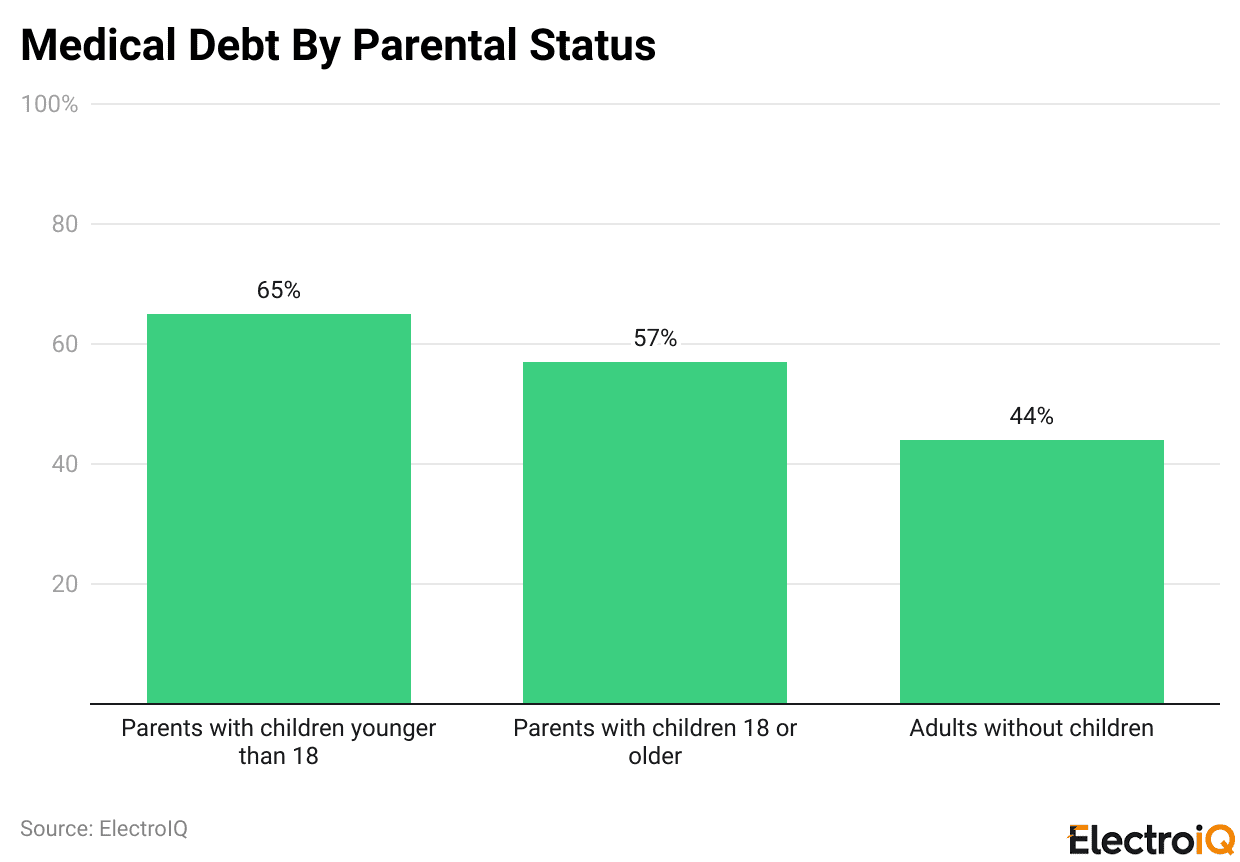

Medical Debt By Parental Status

(Reference: lendingtree.com)

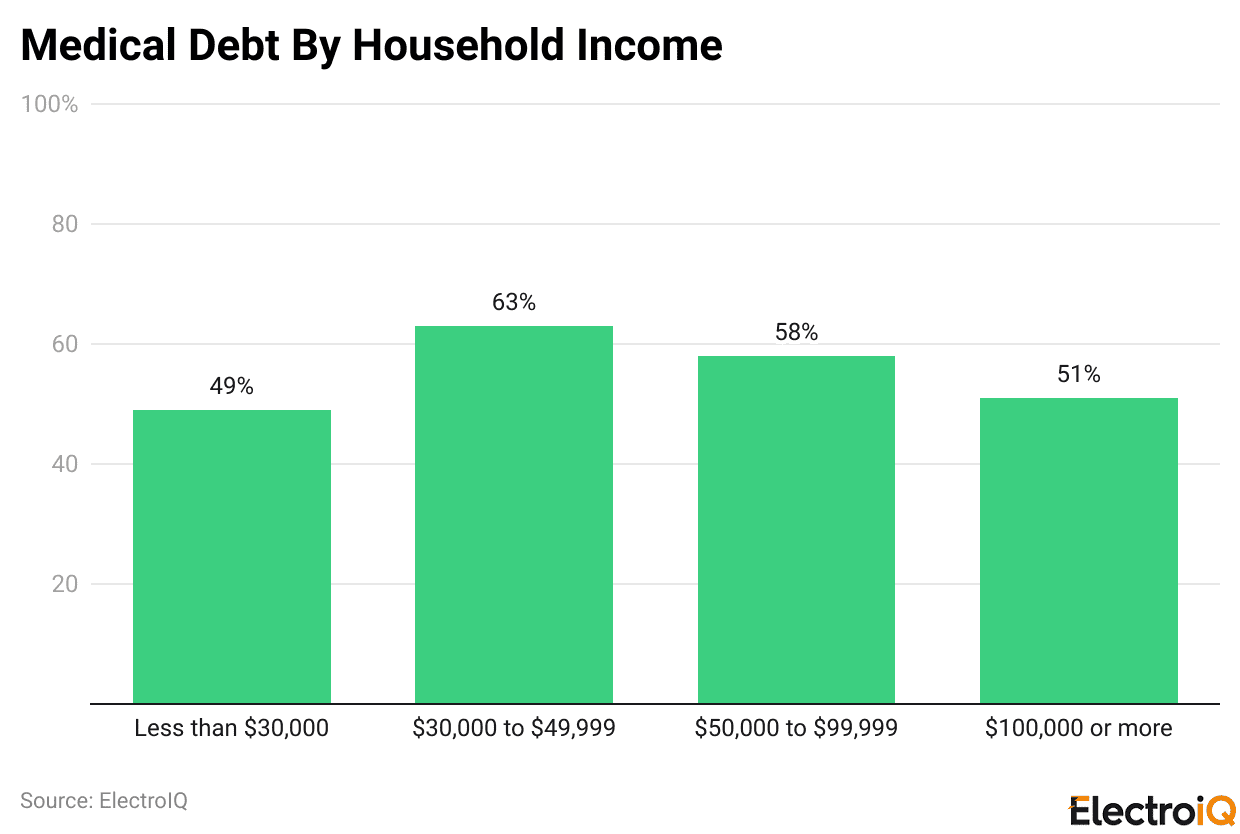

By Household Income

(Reference: lendingtree.com)

- The research demonstrates that the medical debt issue is most prevalent in households with young kids and millennials.

- Medical debt is being confronted by 38% of parents and 32% of adults aged 28 to 43, respectively. The financial burden of high medical bills can be compounded by the health care needs of these people, plus other major financial obligations such as childcare, housing, and education, which they have to pay at the same time.

- The statistics indicate that the medical bills problem is widespread beyond low-income families. To be precise, the medical debt issue is quite common among the higher-income groups as well, with a statistic stating that almost a third of people earning US$100,000 or more are affected by the medical debt issue, as opposed to one-fourth of people earning less than US$30,000 who are affected by the same.

- This implies that the medical costs in question can even be a problem for households that are considered to be relatively affluent.

- According to the survey, the medical debt issue has an equal impact on men and women.

- There is a slight difference between the genders when it comes to reporting medical debt, with men being the ones to report it more often than women, and women being a little more likely to claim never experiencing it.

- The discrepancies between the genders are not as pronounced as the large income differences that still exist regarding the medical debt issue, which goes to show that the issue is more a result of lack of finances and high healthcare costs than gender bias.

Total Medical Debt Owed

- Medical debt is a major and widespread financial burden in the United States.

- An estimated US$194–195 billion in medical debt is currently in active collections, making it one of the largest sources of consumer debt, although the true total may be even higher because not all medical bills are formally reported or sent to collections.

- Medical debt dominates the collections landscape, accounting for about 58% of all debt in collections—more than any other type of consumer debt.

- Medical debt, which poses a huge problem already, still affects a huge portion of the people. One credit report out of five contains a medical collection debt, which is again a bigger percentage than that of student loan and credit card debt put together.

- Even though sometimes the debt collection amount can reach into thousands, the majority of medical bills still remain small; that is, people are often unable to pay under US$500 bills, resulting in a strain on their finances.

- People in the lower-income category are the most affected ones, as medical bills constitute over 70% of such households’ entire collection of debts.

- With around 38% of households admitting to choosing the former method of payment, which is partly paying off medical bills rather than clearing them all at once, the slow process of such costs becoming inactive is evident.

- It is more severe in rural areas where the average medical debt is higher and more than 50% of such debts arise from hospital admissions or ER visits, thus indicating the high price of urgent care.

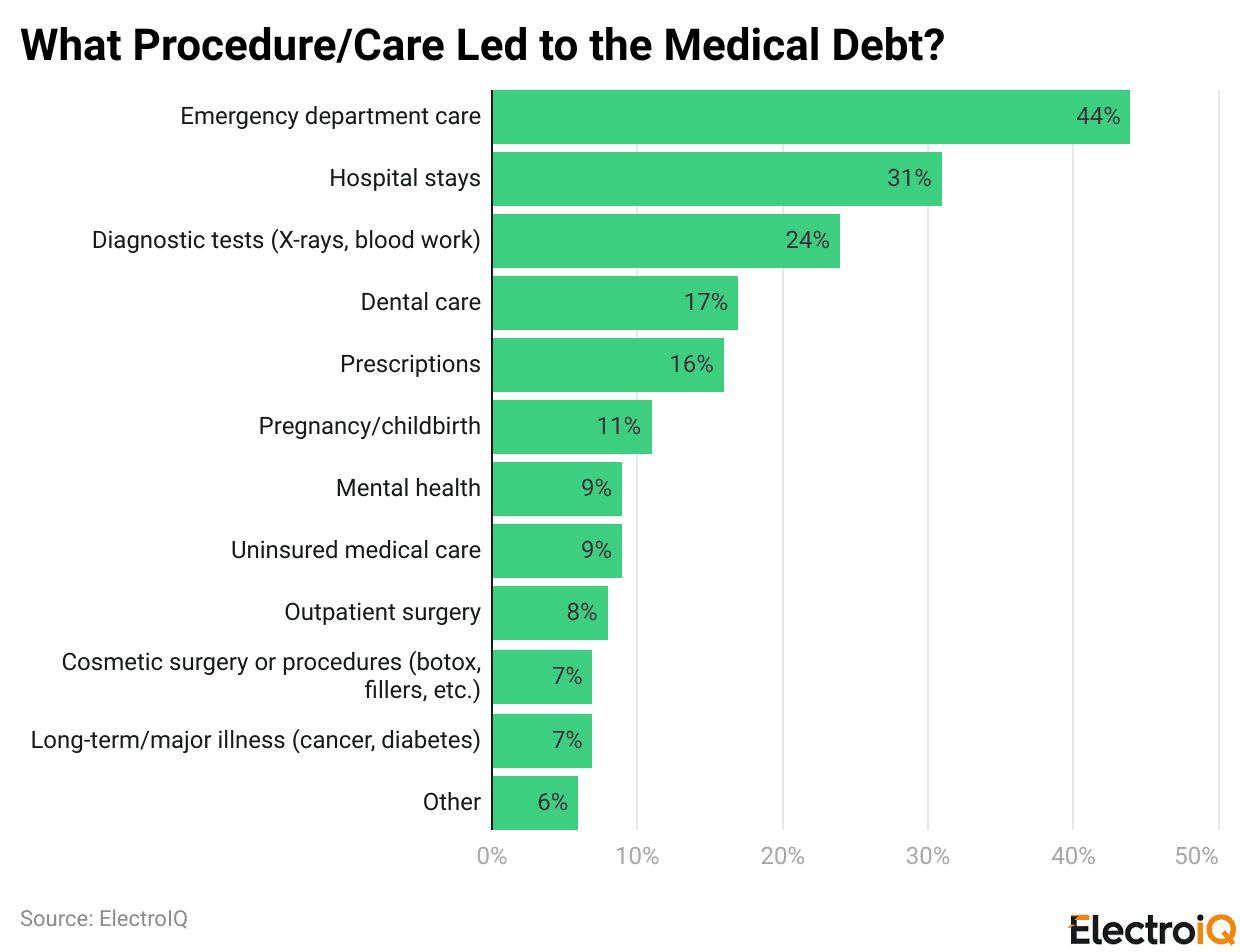

Top Procedures Leading To Medical Debt In The U.S.

(Reference: lendingtree.com)

- In the United States, medical debt usually arises from services that are deemed necessary and sometimes even unavoidable, rather than from optional treatments.

- Emergency department care emerged on top as the main source of medical debts, as the total of 44% who were surveyed marked it as the main reason for their financial obligation to the hospital, which indicates the high costs of urgent and unplanned care.

- Hospital admissions are placed at 31% as the second most common cause of debt, thus, once again, pointing to the fact that inpatient care can swiftly lead to huge bills.

- Almost a quarter of the respondents mentioned diagnostic procedures like X-rays and blood tests as being significant factors in the accumulation of their medical debts, while 17% of the debts were for dental services, thus pointing to the inadequacies in dental insurance coverage.

- The problem of high-priced prescription drugs touches 16% of the population, and costs related to pregnancy and childbirth are responsible for debt for 11%, thus proving the point that even the most routine or event-related medical care can turn into a financial burden.

Medical Debt In Collections

- The information indicates that medical debt is a general phenomenon, and the handling of it is such that it creates confusion between medical care and consumer finance.

- Approximately 36% of households claim to have some medical debt, while 21% admit to having at least one overdue medical bill.

- A significant portion of people resort to paying over time instead of paying all up front. 23% of the patients are paying in instalments, and 17% are using credit cards or personal loans for hotel medical bills, etc.

- Thus, 15% of the adults have been approached by a debt collector, and 12% have one or another medical bill reported on their credit reports, with “5% having added new medical debts during the preceding year”.

- Allowing payment plans, medical and dental providers are increasingly acting as informal lenders.

- The fact that many medical debts do not go through formal collections or credit reports means that the overall problem is likely to be much more than what has been indicated.

Medical Debt On Credit Reports

- In consumer credit distress, medical debts have the largest share.

- Medical collections constitute 58% of the total consumer debt in collections, making it the leading cause of such debts, followed by no other debt type.

- The majority of medical collection balances are quite small, and lately, during the past couple of years, the limit for what is regarded as a small debt has been lifted to 500.

- Nevertheless, the problem is that many medical debts are still not reported, or, when reported, they are either misclassified or handled inconsistently.

- For people with reported medical debt, the average balance is generally between US$2,456 and US$7,931.

- So if you have a medical debt of even a small amount, it will still hurt your credit score, and thus it will become more difficult for you to get a house, automobile, or other types of loans.

Cost As A Deciding Factor For Medical Care

- The high medical costs are having a direct impact on people’s health decisions.

- It is estimated that during the years 2024-2025, 36% of adults would have been doing non-vital medical checkups or treatments due to money issues.

- Women are more prone than men to postpone treatment, which can be seen in the statistics, where 38% of women, as opposed to 32% of men, reported that there were indeed delays.

- Even people who have medical insurance through their employer are indirectly affected, since 34% to 39% of adults insured with medical debt have avoided treatment on account of the costs they incurred.

- Preventive measures and mental health treatment are the most frequently avoided, and low-income families often suffer by reducing their necessities like food, rent, and electricity.

- Households with medical debt are very likely to smoke in care, which may result in deteriorating the condition of chronic diseases and, hence, poor health over the long run.

Mental Health And Its Relationship With Medical Debt

- There is a strong correlation between medical debt and people neglecting their mental health needs and suffering psychologically.

- It has been noted that about 33.8% of individuals with medical debts refrain from receiving mental health care, while only 6.3% of people without debts do so.

- The existence of debts for medical reasons brings about a 17.3% rise in mental health needs that have not been met.

- It’s been found that among the people with depression and medical debt, more than one-third postponed therapy, and nearly 38% entirely skipped the treatment.

- The same is true for those suffering from anxiety, where almost 40% of people delayed or avoided taking care of their health.

- On the other hand, only about 17% of individuals without medical debt faced the same or similar problem concerning mental health treatment.

- The financial pressure, uncertainty, and burden of serious illnesses like cancer have a way of compounding the mental health problem.

Surprise Billing And Medical Debt

- Despite the implementation of the No Surprises Act, which was an attempt to fully eradicate surprise medical bills, the phenomenon still exists and continues to be a main cause of medical debt.

- Privately insured patients have gained from the Act through a reduction of out-of-pocket costs by around US$567 to US$600 per year; however, the occurrence of unexpected bills is still there.

- In the state of Connecticut, for instance, 26% of the adult population claimed that they had received an unexpected medical bill within the last year, while 37% of these adults experienced financial strain, like loss of savings or being subject to collection actions.

- A percentage of 23 hundredths of the population reported being in debt because of medical expenses, the majority of which owed in the range of US$1,000 to US$2,499.

- In a great number of instances, the debt is the result of insurance covering only a fraction of the services; thus, the patients are left with unmanageable balances.

- 2024 witnessed a remarkable increase in disputes under the No Surprises Act, with the providers emerging victorious in most of the arbitration cases and consequently getting paid a lot more.

- Among the patients who take hospital services, which include labs and imaging, as the primary cause of most medical debt, those with disabilities and young adults aged 25-34 years are the ones suffering most from the debt burden.

Recent Developments

- Medical debt is still a major financial problem for a lot of people in the U.S., according to recent statistics.

- An approximate number of 31 million Americans borrowed about US$74 billion to pay for medical bills during the last year, which clearly shows that it is not unusual for households to depend on credit, loans, or payment plans to bear the cost of health care.

- Insurance coverage is not a guarantee for individuals to afford care, especially people with high-deductible health plans who have to incur significant out-of-pocket expenses before coverage becomes effective.

- Concurrently, the revisions in credit reporting regulations have mitigated some of the long-term impacts of medical debt.

- The three primary credit reporting agencies have ceased reporting medical debts of less than US$500, in addition which the new regulations now allow the removal of paid medical collections and debts under one year old from the credit reports.

- Consequently, these actions have prevented millions from suffering permanent credit score damage, though still, 15% of American adults claim that they have been contacted by medical debt collectors during the last year.

- Easing through these services, mental health has remained the major source of unpaid bills due to a lack of affordability and coverage.

Conclusion

Medical Debt Statistics: Medical debt continues to be a huge problem in the U.S. healthcare system in 2025. It is still affecting millions of people regardless of age, income, or insured status. Routine care is one of the causes that the data shows triggering long-term financial strains. This leads to households being pushed into debt, taking longer to treat essential health issues, thus resulting in worse physical and mental health outcomes.

The impact of recent credit reporting changes and government actions has not wiped out the financial harm totally. However, it has reduced the burden to a large extent, especially for the working population, parents, and those who need urgent or chronic care. Solving the issue of medical debt will require comprehensive reforms. These reforms should target affordability issues, coverage gaps, and the introduction of healthcare cost shock management.

Sources

FAQ.

The United States is estimated to have a medical debt of about US$194-195 billion, which is being actively collected. The total amount is probably more because a lot of medical bills are paid in instalments, on credit cards, or are never electronically reported.

Medical debts take their toll on people of different incomes and ages; however, they are most frequently seen in working-age adults, parents with kids, and millennials. Even those in the higher-paid jobs are also affected, as close to one-third of the people who earn US$100,000 or more admit to having medical debt.

Medical debt usually originates from the emergency room treatment (44%), followed by hospitalization (31%), and then diagnostic testing, dental care, medications, pregnancy and childbirth, and mental health care interventions. Most of the medical debt is for necessary medical care rather than elective procedures.

Medical debt represents 58% of all debts sent to collection agencies and is included in every fifth credit report. The recent changes in the rules have taken away the smallest debts and the debts that have been paid from the credit reports. Still, open balances can lower the credit score, and the borrower has less access to housing, loans, and even employment.

Financial burdens resulting from medical care push people to avoid necessary treatments and even to skip preventive and mental health services. It is found that the individuals suffering from medical debt are often a lot more likely to experience anxiety, depression, and even failures in receiving mental health services, which makes the situation worse as financial stress negatively affects health outcomes.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.