ATM Usage Decline Statistics and Facts (2026)

Updated · Dec 23, 2025

Table of Contents

- Introduction

- Editor’s Choice

- ATM Managed Services Market Size

- Attempted Check Fraud By Deposit Channel

- Decline In the Number Of ATMs Installed

- Decline Of Cash Usage And Change In Payment Mix

- Differences In The Use Of ATMs In Urban And Rural Areas

- Demographic Differences In ATM Usage Decline

- ATM Transaction And Usage Up To Now

- Security, Fraud, And Their Impact On ATM Use

- Advanced Vs. Emerging Economies

- Recent Developments

- Conclusion

Introduction

ATM Usage Decline Statistics: Throughout its long history, the Automated Teller Machine (ATM) has been widely regarded as a symbol of convenient cash access, ubiquitous, reliable, and easy to use. It has brought financial independence to the suburbs as well as to the most remote parts of the developing world. But now, with the financial industry moving towards digital payments, mobile wallets, and real-time transactions, the once-mighty ATM is standing at a crossroads.

ATM usage in 2025 is unlikely to vanish overnight; however, data indicate a clear downward trend in the number of machines and cash transactions in many parts of the world. Changing withdrawal habits are also part of the trend, as users mostly withdraw larger amounts but make fewer visits. This article examines the latest statistics on the decline of ATMs, the reasons for the decline, and the broader implications for both customers and banks.

Editor’s Choice

- The global ATM count has declined to approximately 2.95 million, with annual declines of approximately 1.4%-1.8% as more ATMs are removed than installed.

- Third-party ATM management and banks’ reliance on it are increasing, with the outsourcing service growing by 13.2%, while the smart ATM market with video and biometric features is growing at a rate of 5.8% per year.

- There are more than 39,000 cryptocurrency ATMs worldwide, with an annual growth rate of 6%, and more than 80% are located in the U.S.

- Almost 70% of customers use ATMs for deposits, balance checks, and bill payments; thus, ATMs remain significant even for non-cash services.

- Although fewer people use ATMs, the average amount withdrawn per visit has increased to approximately US$157, indicating that people are making fewer transactions but each transaction is for a larger sum.

- In the U.S., UK, and German markets, ATM use has decreased by approximately 5.7%, primarily due to the rise of mobile wallets, contactless payments, and peer-to-peer applications.

- Gen Z and Millennials account for nearly half (45%) of all digital payments, while approximately 30% of the U.S. population reported not withdrawing any cash from an ATM in the last month.

- Cash remains the primary payment method in developing countries; for instance, in Africa, ~89% of transactions are in cash, and in Latin America ATM cash withdrawals have increased by 7%.

- The Asia-Pacific region encompasses more than half of the world’s ATMs, with India and Indonesia being the most significant players among these countries.

- Approximately twice as many ATMs are used in cities as in the countryside, but people in the countryside still rely heavily on cash withdrawals, often because banks are not located in the area.

- Across the globe, over 85% of ATM transactions are cash withdrawals, and over 70% of cash dispensed consists of USD 20 and USD 50 notes.

- The total value of global ATM transactions will surpass USD 1 trillion annually by 2025, indicating continued high usage, despite a decline in ATM visits.

- Global losses from ATM fraud reached approximately US$2.05 billion, primarily due to skimming, which accounted for roughly 77% of cases and resulted in losses of US$1.58 billion.

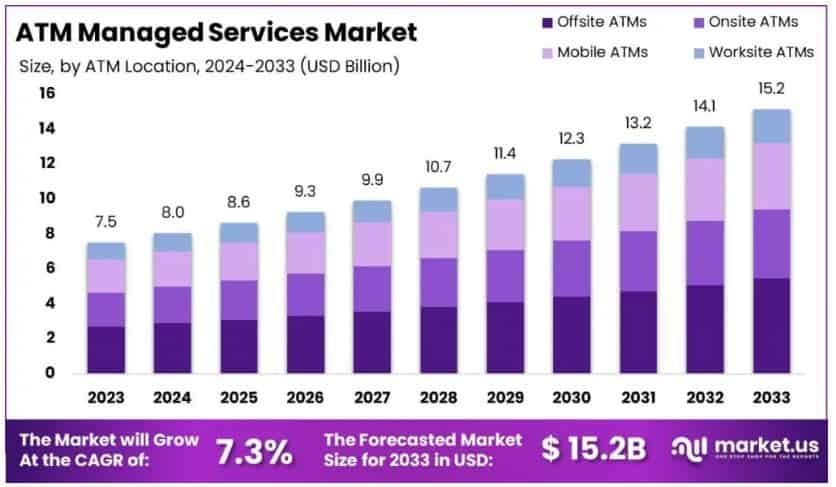

ATM Managed Services Market Size

(Source: electroiq.com)

- The global ATM managed services market has been growing steadily and will continue to do so, despite declining demand for traditional ATM services.

- The market size is projected to be approximately USD 8.6 billion by 2025 and USD 15.2 billion by 2033, indicating steady long-term demand.

- The long-term annual growth rate is 7.3% for the period 2025 to 2033, primarily due to banks seeking to operate and maintain their ATM networks more efficiently.

- On the other hand, by 2025, the number of ATMs worldwide is expected to decrease to approximately 2.95 million, as a result of bank mergers that lead to branch closures and a reduction in physical infrastructure.

- To offset costs, many banks and other financial institutions are selling off their ATMs and switching to third-party service providers, a move that has led to a 13.2% increase in the outsourcing of ATM services.

- Additionally, the market is being shaped by technological advancements; for instance, smart ATMs are projected to grow at 5.8% per annum through 2029 as biometric identification and video assistance become more widely available.

- Despite the general decline in traditional machines, cryptocurrency ATMs are still on the rise and have already numbered 39,000 worldwide, with the US holding more than 80% of them.

- Moreover, it is noteworthy that ATMs remain widely used, with about 70% of the public using them for cash deposits, balance inquiries, and bill payments.

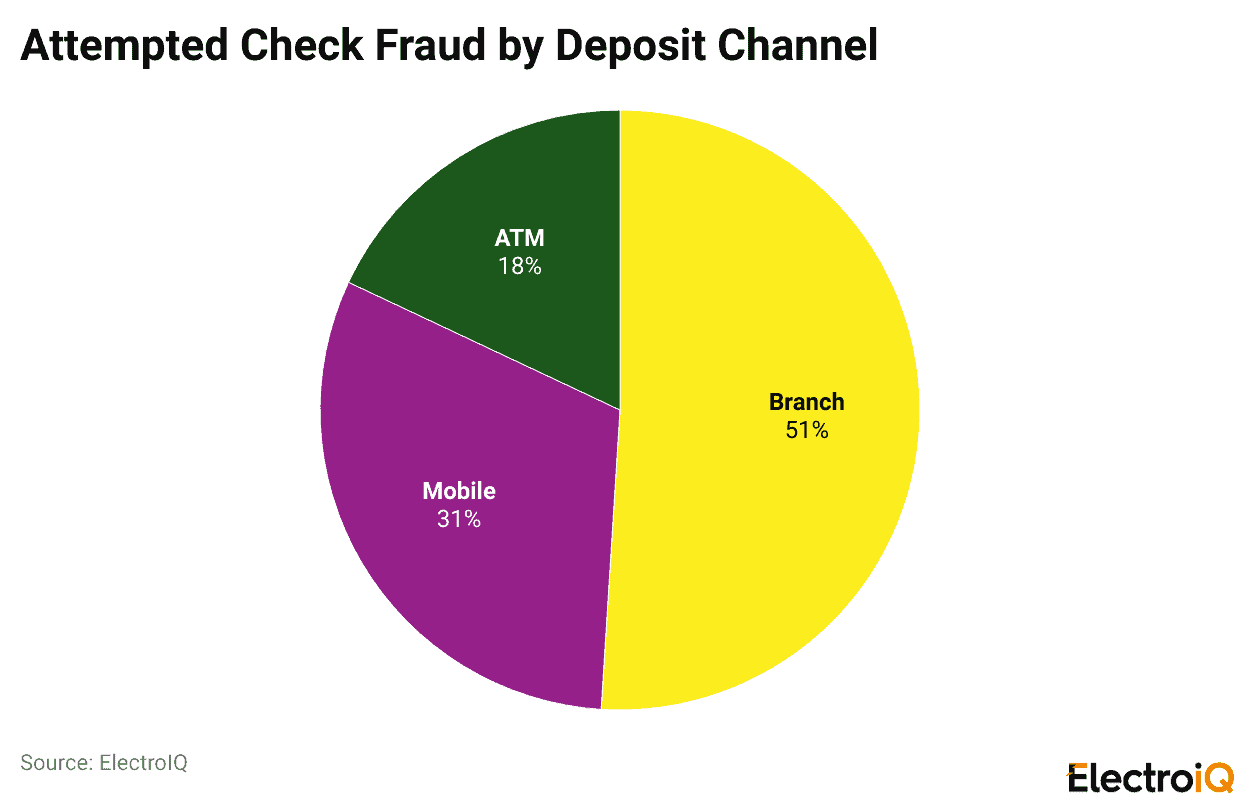

Attempted Check Fraud By Deposit Channel

(Reference: coinlaw.io)

- The risk of check fraud varies greatly depending on the method of deposit used.

- In-person banking continues to be the most accessible and, thus, the highest-risk channel for attempted check fraud, with bank branches alone contributing to 51% of the total attempted check fraud by value despite the in-person verification process.

- After bank branches, mobile deposit ranks second with 31%, pointing to the fact that electronic and imaging-based check deposits pose the highest risk as more customers embrace digital banking.

- The share of attempted fraud via ATMs is the lowest at 18% indicating that ATMs are not completely risk-free but rather offer more security compared to branches and mobiles in terms of check deposits.

- This scenario calls for stronger controls against fraud, particularly in branches and mobile banking channels.

Decline In the Number Of ATMs Installed

- Due to the advent of digital payments that are gradually replacing cash, the global ATM network is slowly going out of the picture.

- The global ATM count fluctuates between 2.9 and 3.0 million units, with data indicating a year-on-year decline of approximately 1.4% to 1.8% in recent years.

- In several developed nations, the rate at which ATMs are being removed is now more than the rate at which new ones are being installed, indicating a long-lasting change rather than a temporary retreat.

- Off-site ATMs, such as those located in retail stores and public places, have declined from approximately 97,000 units to just over 82,000, whereas on-site ATMs within bank branches or premises still account for about half of the total worldwide.

- The basic, traditional ATMs are being withdrawn from the market earlier than the advanced, high-end terminals that can process deposits, payments, and a variety of other services.

- While the general trend has been a decline in cash usage, cryptocurrency ATMs remain a notable exception, as they continue to grow.

- The total number of installations has exceeded 39,000, and the annual growth rate is approximately 6%, indicating persistent interest in cryptocurrency access, although demand for ATMs for conventional cash has declined.

- The machine landscape in ATMs has been shaped by consolidation, with fewer machines but with a greater focus on functionality and specific use cases.

Decline Of Cash Usage And Change In Payment Mix

- In 2025, there was a significant drop in ATM usage during the year in the U.S., the UK, and Germany, which are the main developed markets, where the decline was about 5.7% as people day by day were moving more towards mobile wallets and contactless payments.

- Everyday transactions became swifter and easier thanks to Apple Pay and Google Wallet, which led to a 10.8% decline in regular cash withdrawals.

- Cashless transactions using QR codes also increased by about 19.5% worldwide, thereby reducing the need to carry cash and visit ATMs.

- The younger generation has been using apps for peer-to-peer payments, such as Venmo and Zelle, more frequently; consequently, the rate of ATM use among Gen Z may have declined by 22%.

- The situation remains markedly different in many regions of Africa, where cash remains the primary means of payment: in 2025, approximately 89% of consumer transactions were still in cash.

Differences In The Use Of ATMs In Urban And Rural Areas

- There are considerable differences in ATM use between urban and rural areas.

- Activity in urban ATMs is approximately twice that in rural areas, attributable to higher transaction volumes and a more extensive banking infrastructure.

- Urban areas account for about 10% of ATM transactions, which users typically make of digital bank cards, and these transactions are usually cash withdrawals.

- In rural areas, where more than 70% of ATM transactions are cash withdrawals, physical currency remains very important.

- For instance, rural India accounts for approximately 65% of the population and only 20% of the country’s ATMs.

- The Pico ATM in the Philippines program is an example of how off-site ATMs can help underserved areas.

- 94% of total transactions happen outside Metro Manila, and almost two-thirds of the users are women in the regions.

- Urban areas experienced a more dramatic increase in cash withdrawals than rural areas, but ATMs remain necessary infrastructure in rural regions, particularly in areas where 45% of the population lives without any bank branches nearby.

Demographic Differences In ATM Usage Decline

- The younger generation is leading in the adoption of digital finance, making approximately 45% of their payments via mobile wallets.

- A survey conducted in the U.S. found that approximately 30% of Americans had not made any ATM withdrawals in the previous month, reflecting a trend toward reduced reliance on cash.

- The older population paid even more with cash; among those aged 55 and older, about 19% of total payments were made in cash.

- Households with annual income below US$25,000 are also cash-dependent, with cash used in approximately 24% of their transactions.

- Mobile banking apps are already a strong preference among the younger generation: 64% of Gen Z and 67% of Millennials.

- More than half of Millennials prefer using an ATM to a bank teller, while 42% of Gen Z consider the availability of an ATM when selecting a bank, indicating that access to cash, even digitally, remains a key factor in the “digital-first” era.

ATM Transaction And Usage Up To Now

- ATM activity remains significant worldwide, despite the substantial growth of digital payments.

- Global ATM transactions are likely to exceed US$1 trillion annually for the first time by 2025, indicating the continued importance of cash access.

- US ATMs processed more than 60 billion transactions in 2023, indicating that each ATM accounted for approximately 50,000 transactions annually, underscoring the continued demand for these devices.

- In Canada, the average person uses an ATM about 20 times a year, whereas in Africa there was a remarkable 25% increase in ATM usage, indicating the gradual spread of access to banking services.

- Worldwide, cash withdrawals remain the leading ATM service, accounting for more than 85% of all transactions.

- The UK is one of the countries in which cash withdrawals from ATMs account for approximately 35% of total cash payments, underscoring the importance of ATMs in the daily payment process.

- Another factor that affects the usage is the location. In cities, ATM use is typically twice that in rural areas, and about 10% of transactions involve digital banking cards rather than cash withdrawals.

- On the other hand, ATMs have been used for more than cash: ATM use for checking accounts has increased by 25% over the past three years, and approximately 35% of ATM transactions are now deposits, particularly in retail areas.

- Meanwhile, the widespread use of mobile payments has led to a decrease of about 12% in cash withdrawals in urban areas of Japan.

- There are definite seasonal patterns that characterise ATM usage. Between 10 AM and 2 PM is the most active time, and it accounts for almost 40% of total daily transactions.

- Transaction volumes also double and often go up by as much as 50% when the occasion is a holiday compared to that of a normal month.

- Where banks are scarce, better ATM access alone has led to an estimated 20% increase in access to banking services over the past five years.

- In terms of cash transactions, the USD 20 and USD 50 bills are the global champions and together account for more than 70% of all the cash that is taken out of ATMs.

Security, Fraud, And Their Impact On ATM Use

- Security issues are still one of the biggest factors determining ATM usage worldwide.

- The world’s financial losses caused by ATM-related fraud are estimated to be about US$2.05 billion, and skimming is the major loss as well as the most common case.

- Skimming alone accounted for about US$1.58 billion in losses, thus being the top ATM threat.

- On the other side of the coin, fraud cases have been recorded much more frequently in certain areas. Europe, for example, reported an increase of 32%.

- It is estimated that 68% of the newly installed ATMs are already equipped with end-to-end encryption, while biometric authentication is used in approximately 18% of the automatic teller machines worldwide.

- Notably, the implementation of EMV chip cards has helped to decrease ATM fraud by almost 30% in developed countries.

- Moreover, AI-based fraud detection systems and remote monitoring tools have been instrumental in reducing fraud losses by 16.1% and 11.3%, respectively, thereby increasing user trust and system resilience.

Advanced Vs. Emerging Economies

- The trends of ATM usage vary considerably between the developed and the underdeveloped markets.

- In the US, UK, and Germany, which are considered advanced economies, the use of ATMs has decreased by about 5.7%.

- On the other hand, Western Europe suffered an even greater decline of 7.5%.

- This decrease is attributable to the widespread adoption of digital wallets, mobile banking, and contactless payments.

- An additional 5% reduction in ATM installations is anticipated for the North American region.

- On the other hand, cash remains the primary means of payment in developing economies.

- The Asia-Pacific region, including India and Indonesia, accounts for more than half of global ATM deployments.

- In Africa, 89% of consumer transactions are still made in cash, whereas in many emerging markets the corresponding figure is 84%.

- A 7% increase in ATM transactions has been observed in Latin America, indicating ongoing demand.

- The United States, however, is the leader in the crypto ATM market, accounting for more than 80% of installations worldwide.

Recent Developments

- Recent data indicate that ATM use is evolving rather than ceasing.

- The number of ATMs globally decreased by 1.8%, to approximately 2.95 million, down from 3 million.

- The total transaction volume also went down slightly to 86.7 billion transactions.

- People may be visiting ATMs less frequently, but they seem to be withdrawing more each time, with the average withdrawal reaching US$157, which is a 4.2% increase from the previous year.

- Contactless ATM transactions grew by 19%, while cardless withdrawals via mobile apps increased by 17.8%, indicating their integration into digital banking habits.

- Despite this, total ATM visits have decreased by 11.2%, alongside an increase in digital payments.

- Higher out-of-network fees, averaging US$4.86 per transaction, have been making it difficult for frequent users.

- As a consequence, banks are expanding their ATMs beyond cash by offering services like deposits and bill payments so that the machines remain relevant in an ever-increasing digital financial landscape.

Conclusion

ATM Usage Decline Statistics: ATMs are no longer the primary channel for daily payments, yet they still play a significant role in the global financial system. The number of ATMs and their total usage may be declining in developed regions. Still, the need for cash access, deposits, and basic banking services in emerging and rural areas remains high. The gradual decline of ATMs due to digital wallets and contactless payments is evident, as usage has shifted toward fewer visits and larger withdrawal amounts. The ongoing push for security, innovative features, and a non-cash approach suggests that ATMs are transforming to remain relevant rather than go extinct.

Sources

FAQ.

No, ATMs are not going away completely. Their presence and usage are shrinking in many developed countries, but they still play a crucial role in cash withdrawals, deposits, and basic banking services, especially in rural and developing areas. Besides, ATMs are developing along the line of features like deposits, bill payments, and cardless transactions to remain pertinent.

The main reason for the downfall of ATM transactions is the quick embrace of mobile wallets, contactless payments, QR-based payments, and peer-to-peer platforms. These digital methods discourage people from taking cash out frequently, especially the youth of Gen Z and Millennials.

Yes, ATMs are still very much in use in developing countries. In areas like Africa, Asia-Pacific, and some parts of Latin America, cash is still the king in daily transactions. For instance, in Africa, almost 89% of consumer transactions involve cash, with ATM usage rising in certain locations.

Banks are investing in smart ATMs with advanced features such as biometric authentication, video assistance, contactless access, and cardless withdrawals. They are also expanding non-cash services like deposits and bill payments, while outsourcing ATM management to reduce costs and improve efficiency.

ATMs account for a smaller share of attempted check fraud compared to branches and mobile deposits. Although fraud risks like skimming still exist, security improvements such as encryption, EMV chips, AI-driven fraud detection, and remote monitoring have significantly reduced losses and improved user trust.

Aruna Madrekar is an editor at Smartphone Thoughts, specializing in SEO and content creation. She excels at writing and editing articles that are both helpful and engaging for readers. Aruna is also skilled in creating charts and graphs to make complex information easier to understand. Her contributions help Smartphone Thoughts reach a wide audience, providing valuable insights on smartphone reviews and app-related statistics.