Iveco Statistics By Future Growth And Strategies (2026)

Updated · Mar 30, 2026

Table of Contents

Introduction

Iveco Statistics: Iveco Group entered the 2025-2026 period navigating a triad of headwinds: cooling European demand, large-scale asset divestitures, and an accelerated pivot toward electrification. As a dominant force in the global commercial vehicle market, the company reported a contraction in earnings and margins throughout 2025, primarily driven by a downturn in truck sales and macroeconomic volatility. Through cost management, electric vehicle expansion, and the strategic USD 4.4 billion sale agreement with Tata Motors, Iveco built its future market position.

The newest data from Iveco shows that they face immediate challenges, but their sustainable mobility efforts and operational efficiency programs will drive future growth in the changing transportation industry.

Editor’s Choice

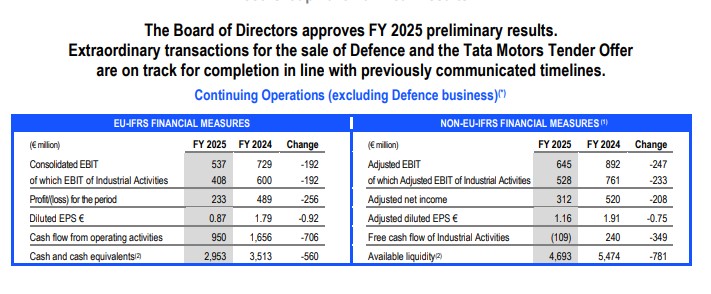

- Iveco Group FY2025 EBIT declined 26% YoY to €537M, reflecting margin pressure.

- Industrial activities’ EBIT to €408M demonstrates that core business operations face difficulties.

- Net profit dropped 52% YoY to €233M, signaling a sharp earnings contraction.

- Diluted EPS drops to €0.87 from €1.79, which results in lower returns for shareholders.

- Operating cash flow decreased to €950M from €1.66B (−42.6%) yet remained resilient.

- Adjusted EBIT decreased by 24% to €645M, which shows that company operations experienced major disruptions.

- Cash reserves decreased by 14% to €4.69B because the company used funds for operations and ongoing restructuring efforts.

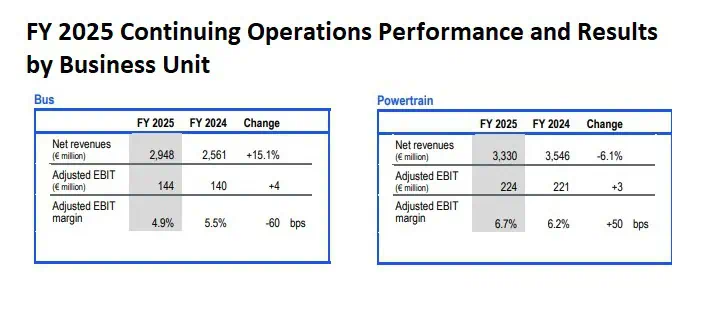

- Bus segment revenue increased by 15.1% to €2.95B because of rising demand for electric buses.

- Bus EBIT margin decreased to 4.9% (−60 bps) because of rising operational expenses.

- Powertrain revenue dropped 6.1% to €3.33B, but margin improved to 6.7%.

- Total assets decreased by 2.9% to €18.9B because of strategic portfolio management.

- Working capital decreased by approximately 12.5% to €2.51B, which demonstrates better operational productivity.

- Defence business sold for €1.7B (~5.4x book value), unlocking shareholder value.

- The total value of the deals reached over €19.8 per share, which resulted in a premium between 22 and 25%.

- The combined revenue after Tata Motors integration will reach approximately €22 billion with 540000 vehicle sales each year. nually.

Financial Performance Snapshot

(Source: ivecogroup.com)

- The financial metrics for FY2025 demonstrate a pattern of declining earnings and decreasing cash flow, which continues despite ongoing business operations.

- The consolidated EBIT for the company decreased to €537 million from €729 million in FY2024, which resulted in a €192 million decrease that represents a 26% annual drop and demonstrates the impact of operational costs on primary business activities.

- The operational activities of the industrial sector experienced a significant drop in EBIT, which decreased by €192 million to reach €408 million, showing a decline in profitability for the company’s main operational area.

- The company reported a net profit decline because the profit/loss per period decreased from €489 million to €233 million, which represents a 52% loss, while the diluted EPS decreased from €1.79 to €0.87, which demonstrates a decrease in value creation for shareholders.

- The company maintained decent operating cash flow at €950 million because it only declined from €1,656 million, which shows that the company can maintain its cash flow operations during a period of declining earnings.

- The non-IFRS metrics show that adjusted EBIT fell to €645 million, which represents a 24% decline from the previous year, and this fact shows that all areas of business operations experienced a decrease in performance.

- The company reached adjusted net income of €312 million, while adjusted EPS fell to €1.16, which showed that earnings across adjusted financial measurements faced increasing pressure.

- The company experienced a liquidity reduction of 14% because its available liquidity declined from €5.47 billion to €4.69 billion, while its cash reserves decreased by €560 million, which shows how the company spends cash and how it deals with its financial resources.

Iveco Segment Performance

(Source: ivecogroup.com)

- The financial performance of Iveco Group shows positive revenue growth according to its three business segments, although they face challenges with operational efficiency.

- The Bus segment delivered strong revenue growth of 15.1%, reaching €2.95 billion compared to €2.56 billion in FY2024, signalling robust demand momentum, likely driven by public transport electrification and fleet renewal cycles.

- The adjusted EBIT increased to €144 million, and the EBIT margin decreased from 5.5% to 4.9% by 60 basis points.

- The company faces two cost challenges, which include rising operational expenses and demands from customers, resulting in decreased profit margins despite increasing production output.

- The Powertrain segment shows improved profit margins through its operational activities, although its financial performance shows reduced sales.

- The net revenues declined 6.1% to €3.33 billion, which indicates that engine and components markets face either reduced customer interest or a temporary market downturn.

- The adjusted EBIT increased to €224 million, and the EBIT margin reached 6.7% after expanding by 50 basis points.

- The organisation achieved high profitability through its ability to manage costs, its operational efficiency, and its success in developing new products.

Iveco Assets and Liabilities

(Source: ivecogroup.com)

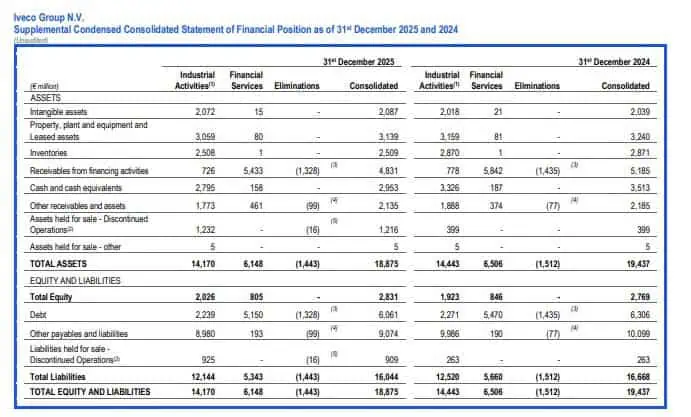

- Iveco Group’s consolidated statement of financial position for FY 2025 shows its balance sheet management through asset efficiency and debt reduction, together with better capital structure utilization.

- The total asset value dropped to €18.9 billion for 2025 after reaching €19.4 billion in 2024 because of portfolio changes and asset sales, which caused approximately 2.9% decrease.

- The analysis of asset makeup shows that intangible assets grew to €2.1 billion through ongoing investments in technology and research development and digital skill development, which serve as essential resources for future business competitiveness.

- The reduction of property, plant, and equipment (PP&E) assets to €3.1 billion indicates that the organization restricted its capital spending while achieving better operational efficiency. The company experienced a decrease in cash and cash equivalents of €560 million to reach €2.95 billion since it used its cash reserves for both strategic projects and debt obligations.

- The company shows substantial debt reduction through its current liability management practices.

- The total liability amount decreased to €16.0 billion after the company reduced its debt obligations from €6.31 billion to €6.06 billion and cut its other payable obligations from €10.1 billion to €9.07 billion.

- Equity demonstrates a minor increase to €2.83 billion, which exceeds the previous total of €2.77 billion because retained earnings and better profitability metrics provided support.

- Iveco Group shows its 2025 financial position as part of a strategic transition period, which requires it to manage three essential processes: cost reduction, asset optimisation, and liquidity control.

- Although the company faces immediate risk due to decreasing cash and shrinking assets, its debt reduction, better inventory management, and core business focus will enable it to achieve sustainable growth.

Iveco Group’s Strategic Divestment

- The IVECO Group will hand over its Defence Business operations to Leonardo S.p.A. through its divestiture, which will lead to fundamental changes for the company that will redefine its strategic direction while generating substantial value for its shareholders.

- The electric vehicle market, together with operational costs and market fluctuations, drives the development of IVECO commercial vehicle products, while their defence business, which includes IDV (Iveco Defence Vehicles) and ASTRA, operates within a market that shows ongoing expansion.

- From 2024 to 2025, Defence revenues increased from €1.1 billion to €1.4 billion, showing approximately 27%growth while keeping a double-digit EBIT margin,s which made it IVECO’s most profitable business unit.

- By integrating IDV’s vehicle platforms—such as advanced armoured systems—with Leonardo’s expertise in defence electronics and command systems, the combined entity enhances its competitiveness in a €28 billion European land defence market, projected to reach USD 39 billion by 2033 (4.0% CAGR).

- The agreement establishes strong alignment with macroeconomic trends because NATO defence spending increased by 19.6% in 202,5 reaching USD 574 billion, while member states pledged to spend up to 5% of their GDP until 2035, which secured steady market requirements for the future.

- The Defence Business had a book value of €313 million, which produced a valuation multiple of approximately 5.4 times its enterprise value to book value ratio, which proved the quality of its assets and the timing of its transaction.

- The company declared an extraordinary dividend between €5.7 and €5.8, which comes from an initial estimate that the company increased and now provides instant cash to shareholders, while the company uses its capital return plan as a major theme.

- The divestiture enabled Tata Motors to make a voluntary tender offer that valued Iveco at €14.10 per share, which priced its remaining commercial vehicle operations at about €3.8 billion.

- Shareholders will receive a value proposition that exceeds €19.8 per share through the combination of the extraordinary dividend and other company returns, which creates a total value exceeding this amount.

- Leonardo acquired the company through an all-cash transaction, which operated without debt to show its financial strength and its ability to manage capital expenditures.

- The decision of Iveco Group to sell its Defence Business to Leonardo S.p.A. creates a major corporate transformation that moves the company towards new strategic goals while creating substantial value for its shareholders.

- The transaction value of €1.7 billion for enterprise value, which becomes €1.6 billion after adjustments, shows the company reached maximum asset value at the best time during the global defense spending period.

- The defence division of the company, which includes IDV and ASTRA, operates in a market that shows continuous development.

- The revenue from defence operations increased from €1.1 billion in 2024 to €1.4 billion in 2025, which resulted in a growth rate of approximately 27 %.

- The defence operations of the company achieved double-digit EBIT margins, which made it the most profitable industrial segment for Iveco.

- The company combines IDV’s vehicle platforms, which include advanced armoured systems, with Leonardo’s defence electronics and command systems expertise to develop products that improve their competitive position in the upcoming European land defence market, which has an estimated value of €28 billion that will increase to USD 39 billion by 2033 through a 4.0 % compound annual growth rate.

- The deal gets support from macroeconomic factors, which enable NATO member nations to raise their defense expenditures by 19.6 % to USD 574 billion in 2025, while committing to spend up to 5 % of their GDP until 2035, which will create long-term demand visibility for their defense needs.

- The transaction brings significant financial benefits to the Iveco shareholders through its financial impact. Defence Business carried a book value of €313 million, which showed that its assets had strong value through a 5.4x EV/book multiple and current transaction timing.

- The company declared an extraordinary dividend between €5.7 and €5.8 per share, which increased from its original guidance to provide shareholders with instant cash while supporting the company’s capital return strategy, which serves as a primary focus area.

- The divestiture enables Tata Motors to execute its voluntary tender offer, which values Iveco at €14.10 per share, resulting in an approximate total company valuation of €3.8 billion for its remaining commercial vehicle business operations.

- The total value proposition for shareholders reaches values above €19.8 per share when combining the extraordinary dividend with other elements, which results in a 22%–25% premium over pre-announcement trading levels.

- The company uses a dual-transaction structure to implement its corporate finance strategy, which achieves a legal balance between divestment proceeds and acquisition-driven consolidation efforts.

- The carve-out process needed extensive operational changes, which included creating IDV Group S.r.l. and dividing global assets among six production facilities, twelve commercial offices, and seven research and development centers.

- Through an all-cash acquisition that Leonardo executed without using debt, the company demonstrates its financial strength while showing its commitment to responsible capital management.

Future Outlook – The Tata Motors Integration (2026–2027)

- The introduction of the Iveco Group to Tata Motors through their upcoming integration will create a new unified vehicle market for all global commercial vehicle markets.

- The voluntary tender offer, which will end in Q2 2026, begins a multi-year period during which both integration processes and value creation activities will take place.

- The acquisition of IVECO by Tata Motors will lead to the company’s removal from Euronext Milan, which will thereafter function as a complete subsidiary of Tata Motors’ Commercial Vehicle division.

- The combined entity will generate approximately €22 billion in annual revenue and over 540,000 vehicle sales, positioning it among the top global truck manufacturers. The company achieves its strategic advantage because its revenue sources span multiple regions, including Europe (50%), India (35%), and the Americas (15%).

- The agreement makes Tata Motors the fourth-largest global player in the >6-tonne truck segment because it enables Tata to acquire market share at an accelerated pace that would take several years to achieve through organic growth.

- The global commercial vehicle industry has a market value of USD 1.29 trillion in 2025, which will grow at a 6.5% compound annual growth rate to reach USD 2.3 trillion by 2034.

- The present moment benefits from strong economic conditions, which include the growth of logistics operations and the rise of e-commerce businesses.

- The European and Latin American markets where Iveco operates, along with Tata’s 35.5% market share in India, create a distribution network that does not compete with existing routes.

- The company establishes immediate cross-selling channels because Tata can sell IVECO’s premium trucks through its existing distribution network while IVECO expands Tata’s market reach in Western countries.

- The advanced portfolio of Iveco, which includes battery-electric, hydrogen, LNG, and HVO solutions together with FPT Industrial’s innovative powertrain technologies, places the company as a leader in current decarbonisation trends.

- The electric commercial vehicle market, which will reach USD 280 billion by 2030 after starting from USD 67 billion in 2021, will become an essential revenue stream when this technology integration occurs.

- Tata Motors has obtained €3.8 billion in bridge financing, which will support its complete debt elimination within four years through operating cash flows and asset monetisation.

- The two-year protection covenant guarantees workforce stability and brand continuity for Iveco while it maintains its European identity.

Conclusion

The 2025 performance of Iveco Group shows that the company is undergoing a transformation that involves changing its operations to maintain profitability while it implements strategic changes and invests in new initiatives. The company experienced a decline in earnings, margins, and liquidity because of macroeconomic conditions and decreased demand for trucks.

The company achieved value creation for shareholders through its defense business divestiture and Tata Motors integration, which enhanced its worldwide market presence. The company has established a solid base for long-term growth through its focus on electrification and alternative fuels and geographic expansion, although execution risks and margin recovery need to be addressed for financial stability to be maintained.

Sources

FAQ.

Iveco’s profit fell 52% due to lower truck demand, higher costs, and macroeconomic volatility.

The defence unit was sold for €1.7 billion, implying a strong valuation multiple.

The combined entity will generate ~€22B revenue and sell over 540,000 vehicles annually.

The Bus segment grew 15.1% in revenue, driven by electrification demand.

The company reduced working capital by ~12.5% and lowered total liabilities, improving balance sheet strength.

Tajammul Pangarkar is the co-founder of a PR firm and the Chief Technology Officer at Prudour Research Firm. With a Bachelor of Engineering in Information Technology from Shivaji University, Tajammul brings over ten years of expertise in digital marketing to his roles. He excels at gathering and analyzing data, producing detailed statistics on various trending topics that help shape industry perspectives. Tajammul's deep-seated experience in mobile technology and industry research often shines through in his insightful analyses. He is keen on decoding tech trends, examining mobile applications, and enhancing general tech awareness. His writings frequently appear in numerous industry-specific magazines and forums, where he shares his knowledge and insights. When he's not immersed in technology, Tajammul enjoys playing table tennis. This hobby provides him with a refreshing break and allows him to engage in something he loves outside of his professional life. Whether he's analyzing data or serving a fast ball, Tajammul demonstrates dedication and passion in every endeavor.