Rural Vs Urban Banking Access Statistics and Facts (2026)

Updated · Jan 12, 2026

Table of Contents

Introduction

Rural vs. Urban Banking Access Statistics: In 2025, the economic rebound from global disruptions and the adoption of digital transformation have made access to banking a key indicator of financial inclusion and socio-economic development. Through banking services, people in both the busy financial districts of cities and the isolated rural areas can assess their capacity to save, borrow, invest, and participate in the digital economy. While urban areas typically have the strongest access to banks and digital financial services, rural areas are not far behind, with the gap between them narrowing thanks to mobile technologies, government policies, and financial inclusion programs.

This article presents the latest figures on banking accessibility in rural and urban areas. Rural vs. Urban Banking Access Statistics for 2025 is a very interesting and informative way to see the global progress and challenges that remain.

Editor’s Choice

- Rural India is undergoing a significant transformation towards digital payments, especially among the younger population, with UPI rising as the leading channel for banking access.

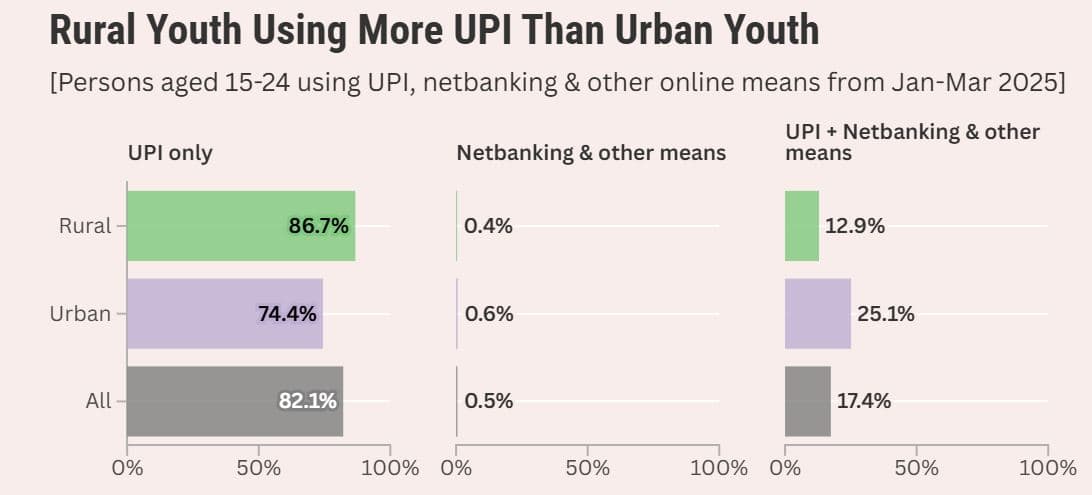

- In January to March 2025, 86.7% of rural youth (ages 15-24) used UPI, compared with 74.4% in the city, indicating greater digital engagement in villages than in cities for daily payments.

- Net banking adoption among youth remains marginal, with usage at 0.4% in rural and 0.6% in urban areas, underscoring the dominance of UPI.

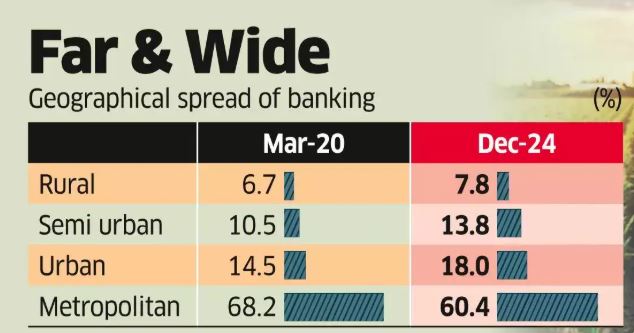

- The distribution of Indian bank credit across regions has become more even, as evidenced by a decline in the share of metro areas to about 60% by December 2024, from approximately 65% five years earlier.

- Rural regions increased their outstanding bank credit quota to 7.8% from 6.7%, while semi-urban and urban areas also saw considerable gains.

- The physical presence of banks remains a major factor, with 42% of new bank branches in FY24 established in areas with populations of fewer than 50,000.

- Private-sector banks are diversifying their operations by area, as evidenced by the opening of 66% of new branches in fiscal year 2024, with over 40% in rural and semi-urban locations.

Rural Youth More Likely To Use UPI

(Source: thesecretariat.in)

- The survey indicates a distinct shift in the digital payment preferences of rural Indian youth, with UPI already more popular than its alternatives in cities.

- From January to March 2025, 86.7% of villagers aged 15-24 used UPI for payments, compared with 74.4% of urban dwellers in the same age bracket.

- This means UPI has won customers’ hearts for small, casual transactions, such as buying tea from a local dhobi, especially in rural areas.

- Among the factors contributing to this trend is the government’s commitment to digital literacy initiatives and bonuses for small retailers in the countryside.

- Along with a local phone number and the internet, UPI has become a convenient payment option, and even the most hesitant people are using it to some extent.

- The idea of showing a QR code and being instantly credited to your account is very appealing to young people who are always seeking quick, easy solutions.

- On the contrary, net banking and other non-UPI payment methods among young people remain minimal.

- Only 0.4% of rural youth and 0.6% of urban youth used net banking during the same period, underscoring UPI’s vast reach as the most user-friendly digital payment method.

- With limited availability of both debit and credit cards, banks being very careful about lending to younger consumers, and small vendors lacking point-of-sale devices, UPI’s dominance is further established.

- Together, these factors are why UPI has become the digital payment method of choice for rural Indian youth.

Geographical Spreading of Banking Access

(Source: economictimes.indiatimes.com)

- The banking system in India has become more user-friendly since the COVID-19 pandemic, with credit availability gradually expanding to smaller towns and rural areas.

- Still, metro areas remain the primary region for bank loans, but their outstanding bank credit share has dropped to about 60% by December 2024, down from roughly 65% five years earlier.

- This change signifies a gradual but steady shift of formal finance from metro to non-metro areas. The rural sector has seen a small but significant increase in its share of bank credit, rising to 7.8% from 6.7%.

- The semi-urban and urban centres have experienced even larger increases in their shares, to 13.8% from 10.5% and 18% from 14.5%, respectively.

- The pandemic-driven migration back to rural areas increased demand for borrowing in these areas, as people returned to their villages and smaller towns and needed more housing, consumption, and small-business credit.

- Customer engagement has remained very much physical branch-centric despite the increasing attention on digital banking.

- In FY24, approximately 42% of new bank branches were established in areas with populations under 50,000, thereby significantly increasing banking penetration in smaller towns and villages.

- Importantly, private-sector banks, which used to focus on metros, are now moving aggressively beyond large cities.

- In FY24, they were responsible for 66% of the new branches, and among those established, 44% were in rural and semi-urban areas, indicating a financial inclusion strategy to deepen penetration in rural areas of India.

Influential Factors of Urban Banking

- Urban banking access in 2025 is the result of a combination of traditional banks, digital-first institutions, regulators, and technology providers, who together determine how easily people living in cities can get formal financial services.

- Public sector banks are still the major players in the urban banking access market. Their considerable number of branches and customers enable them to easily target a vast market of salary earners, small businesses, and low to mid-income families.

- These banks are very crucial in connecting the inhabitants with the government-linked financial inclusion programs through direct benefit transfers or basic savings and credit products. Thus, even in the case of the most populated urban places, there will be at least one banking outlet.

- Urban private banks are rapidly turning out to be the main actors in the urban area through their fast-paced innovations and quality of service.

- They lead and control in sectors like retail lending, credit cards, wealth management, and SME financing. In 2025, private banks are leading the line in digital onboarding, instant credit approvals, and app-based banking, making access faster and more convenient for urban consumers who value speed and personalization.

- Fintech firms and digital banks have managed to become quite powerful in providing urban people with access to banking services.

- Fintechs reach younger, tech-savvy urban populations and gig workers who may not rely heavily on traditional branches through mobile apps, UPI-based payments, digital wallets, and embedded finance.

- Their collaborations with banks enable significantly underserved urban micro-segments, such as micro-merchants and freelancers, to access credit, payments, and insurance.

- One of the most important groups of payment infrastructure providers consists of UPI platforms, card networks, and POS/QR solution providers.

- Their widespread use in urban areas enables smooth transactions and supports cashless ecosystems, reducing entry barriers for both consumers and small urban merchants to participate in official banking.

- Technology and data providers are the last but the most vital industry players who are hiding in the back.

- Cloud services, cybersecurity firms, credit bureaus, and analytics providers make it possible for banks to scale securely, evaluate credit risk more accurately, and offer customized products to a variety of urban populations.

Key Players of The Rural Banking Market

- A diverse set of institutions supports the rural banking market focused on improving financial access, agricultural credit, and rural livelihood development in the least-served areas.

- In India, NABARD is the primary source of such support, as it helps shape rural credit policy, refinance banks, and promote financial inclusion for farmers, SHGs, and rural entrepreneurs.

- NABARD’s intervention further strengthens the rural banking sector as a whole rather than directly targeting retail customers.

- Specialized and cooperative institutions also play a big role. Bharatiya Mahila Bank, merged with the State Bank of India at present, worked towards women’s financial inclusion through custom-made credit and savings products for rural women and small entrepreneurs.

- The Kangra Central Cooperative Bank Ltd. represents the cooperative banking model that facilitates community banking by backing local agriculture and small businesses in a rural area of Himachal Pradesh.

- Bandhan Bank Ltd. has already expanded microcredit from cities to rural areas in India, providing small loans, savings, and insurance to low-income households that were previously excluded from the formal banking sector.

- Grameen Bank of Bangladesh is a landmark institution globally, demonstrating that microcredit can not only reduce poverty but also empower rural communities.

- BRAC Bank Limited, on the other hand, takes the same model further by applying it dualistically to rural-urban outreach and SME financing.

- Globally, agriculture-focused banks have a wealth of expert knowledge. Rabobank, with its agricultural and food systems financing expertise gained worldwide, credits the global economies in rural areas to the extent of the location where it is situated.

- In emerging markets, CRDB Bank Plc in Tanzania and Agribank in Vietnam are key players, providing farmers and rural businesses with easy-to-use financial services that enhance capacity and help stabilise incomes.

- In fact, these entities, in close cooperation, demonstrate how the rural banking community depends on a mix of policy-supported, cooperative, microfinance, and agriculture-specialist models for satisfactory inclusive rural growth.

Conclusion

Rural vs. Urban Banking Access Statistics: In 2025, the gap between rural and urban banking access is narrower, as digital innovations and tailored policy actions for the unbanked have been implemented. Still, urban areas are the first to benefit from the most complex banking systems and fintech services, while rural area children are quickly moving towards using digital payment methods such as UPI, sometimes even at a higher rate than city children.

The slow-motion transfer of bank credit, putting up branches in lesser towns, and the increased importance of microfinance and cooperative banks are all part of a more equal financial ecosystem. The union of digital platforms with friendly regulation and different banking models has led to a situation where everyone can take part in the financial world, thus resulting in the economic growth of both urban and rural communities, which is also more inclusive.

Sources

FAQ.

Government-supported digital literacy programs, perks for rural traders, and UPI’s ease of use for minor transactions account for rural youth being more engaged with UPI. Furthermore, the unavailability of cards and POS devices has turned UPI into the most user-friendly digital payment option for rural areas.

The metropolitan area still has the majority of the share in bank credit, but the share has dropped to around 60%. On the contrary, rural, semi-urban, and smaller urban areas gradually gaining access to credit is the reflection of the shift taking place towards a more geographically balanced banking situation.

Absolutely. Physical banks are still very necessary, mainly in the smaller towns and cities. An estimated 42% of new bank branches in the fiscal year 2024 were at places where the population is less than 50,000, thereby increasing trust, access, and customer engagement.

Public and private banks, fintechs, payment infrastructure providers, regulators, and tech companies together make up the main forces behind urban banking access. They are responsible for giving the cities digital onboarding, instant payments, and advanced financial services, among others.

NABARD, co-op banks, microfinance banks such as Bandhan Bank, and banks targeting agriculture like Rabobank are the main actors supporting rural banking. These institutions cater to agricultural credits, microloans, and financial access for the underbanked in rural areas.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.