Peer-to-peer Lending Statistics By Market Size and Facts (2025)

Updated · Dec 08, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Peer-to-Peer Lending Market Size

- Value of Global Peer-to-Peer Lending

- Peer-to-Peer Lending Market By Region

- How Credit Scores Influence Personal Loan Sources

- Default Rates and Risk Assessment

- Top Reasons Why Peer-to-Peer (P2P) Lending Platforms Fail

- Recent Developments

- Conclusion

Introduction

Peer-to-peer Lending Statistics: Peer-to-peer (P2P) lending, also known as marketplace lending, is a process in which individual and institutional investors are directly connected to borrowers via online platforms. The process is expected to offer borrowers quicker access to credit and investors greater returns than traditional loans. Nevertheless, the acceptance, exposure, and regulation of the practice are region-dependent factors.

The main points of this article focus on assumptions and predictions about Peer-to-Peer lending statistics in 2024 — market values, market size, credit scores, and the main trends shaping the industry.

Editor’s Choice

- The global P2P lending market is expected to reach USD 176.50 billion by 2025 and grow to more than USD 1,380.80 billion by 2034, with a CAGR of 25.73%.

- The rapid growth is due to high demand for education loans and healthcare financing, quick approvals, flexible terms, and favourable economic policies.

- The market was only USD 3.5 billion in 2013, but rose rapidly from USD 9 billion in 2014 to USD 64 billion in 2015, indicating that adoption of the service accelerated early on.

- According to forecasts, the P2P lending market will reach nearly USD 1 trillion by 2050, underscoring its long-term potential.

- In the USA, 26% of the population is already using P2P payments, and the value of mobile P2P payments is expected to go up from USD 9 billion in 2014 to USD 86 billion in 2018.

- The P2P payment user base in the United States was projected to expand from 53 million in 2014 to 126 million by 2020, indicating strong adoption of digital payment methods.

- North America holds the largest share of 37% in the global P2P market, followed by Europe with 28% and Asia-Pacific with 24%.

- Consumers with poor credit ratings (300–579) are mostly dependent on online lenders, with approximately 45% of them availing such loans.

- On the other hand, high scorers (800–850) predominantly choose traditional banks for loans, with around 72% opting for them.

- Credit unions always and everywhere favour all credit groups with their services, even though their use ranged from 25% to 33% only.

- The average P2P default rate in 2023 was 4.5%, while consumer loans had a 3.2% and small business loans had a 5.8% default rate.

- 60% of P2P platforms have already incorporated AI for risk scoring, leading to a reduction in default rates by nearly 15%.

- Lenders now have security over 20% of high-risk segments through collateral-backed loans.

- Crypto-backed loans are treated as defaulting loans at 7%, which presents a risky situation for investors.

- Defaulting on the P2P loan mainly involved covering existing bank debt (33%), followed by home renovation (14%) and credit recycling (11%).

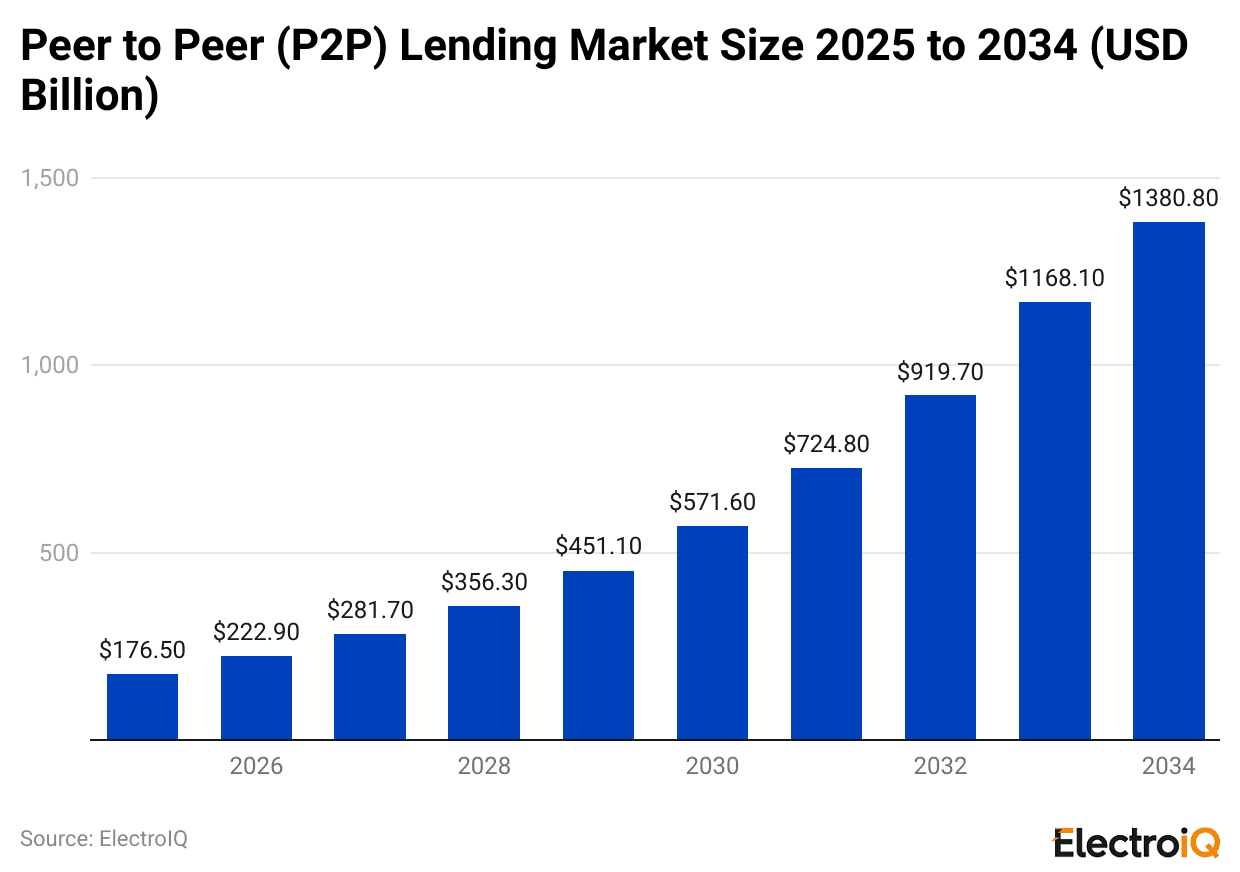

Peer-to-Peer Lending Market Size

(Reference: precedenceresearch.com)

- The data shows that the expected growth of the global peer-to-peer (P2P) lending market during the next decade is quite rapid.

- The market was valued at USD 176.5 billion in 2025 and is expected to grow to USD 222.9 billion by 2026.

- The market is expected to reach around USD 1380.8 billion by 2034, indicating exceptional growth.

- This growth corresponds to a compound annual growth rate (CAGR) of 25.73% from 2025 to 2034, indicating the market will grow by more than three times over this period.

- One of the main reasons for this demand trend is the increase in educational loans and healthcare financing.

- The P2P platforms are preferred by many borrowers as a source of funds due to the quick approvals, fewer restrictions, and more flexible terms that they offer compared to traditional banks.

- Besides, strong economic factors, such as high GDP, supportive government policies, and early adoption of financial innovations across several regions, are facilitating the further lessening and recognition of P2P lending.

- These factors together are forming an ecosystem where the peer-to-peer platforms can swiftly grow and become a significant part of the global financial system.

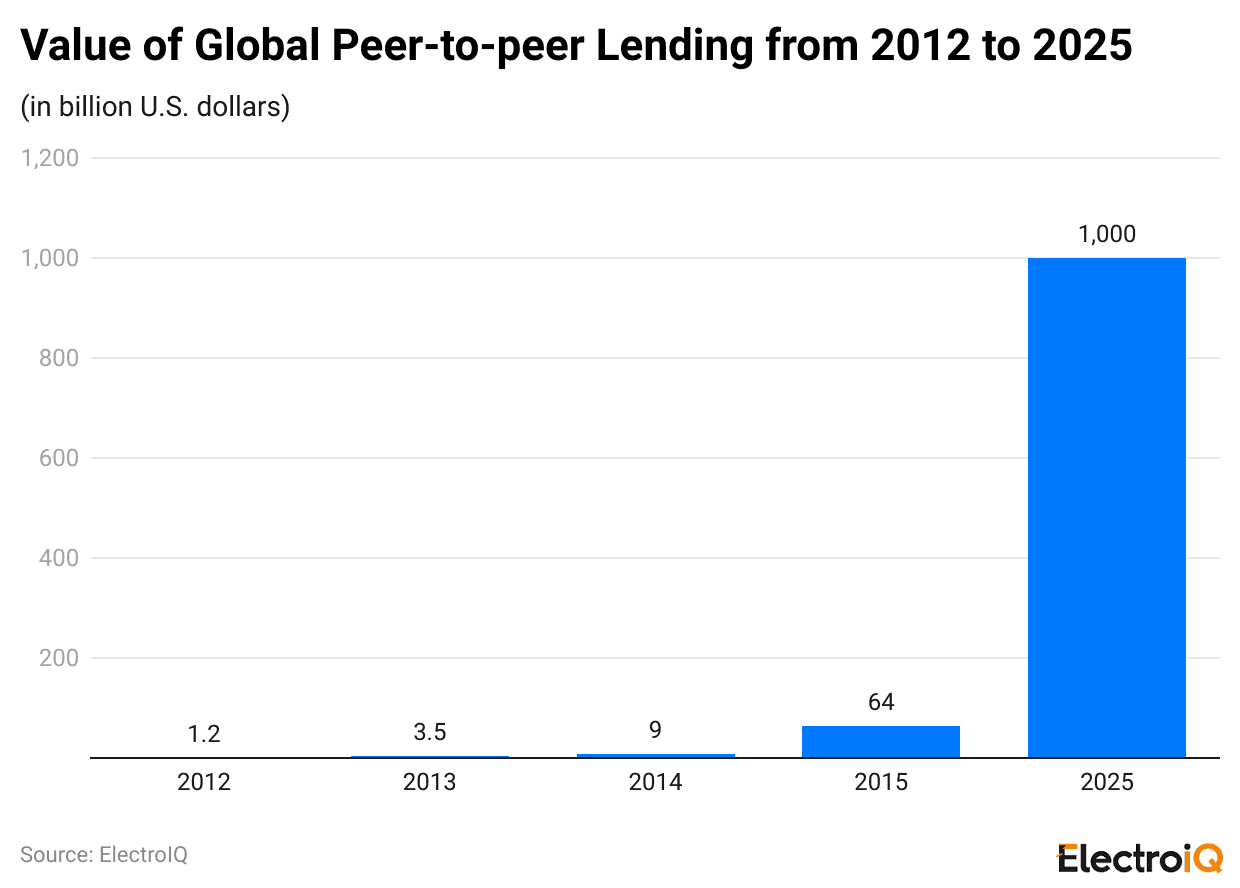

Value of Global Peer-to-Peer Lending

(Reference: statista.com)

- The data narrates the speedy growth and increasing importance of the peer-to-peer (P2P) lending and payments over the years.

- During the first few years, the worldwide P2P lending market was still quite small, with a value of around 3.5 billion U.S. dollars in 2013.

- However, this changed very fast as the number of people and businesses using online platforms to lend and borrow money directly, without going through banks, kept rising.

- The period from 2014 to 2015 saw the global P2P lending value forecast to increase by leaps and bounds, from 9 billion to 64 billion U.S. dollars.

- This sharp ascent is a clear indicator of the rapid growth in trust and popularity of the concept. Looking even further into the future, the market is never to be over, with projections even predicting it could reach near one trillion U.S. dollars by 2050.

- One can also consider peer-to-peer lending as a component of the “sharing economy” concept, as it eliminates the middleman by letting everyone connect and trade financial services digitally.

- These platforms bring together lenders who want their money to work and borrowers looking for funds, often offering more flexible rates and faster processing than traditional banks.

- Reported usage of peer-to-peer payment services was at 26%, indicating that over a quarter of the total population had accepted P2P payments.

- US mobile P2P payments reached $ 9 billion in 2014 and were expected to soar to $ 86 billion in 2018.

- User count predictions were similarly optimistic, as users were expected to grow from 53 million in 2014 to 126 million by 2020.

- Such consumer behaviour changes indicate that people are increasingly going towards mobile and digital payment methods for their daily transactions.

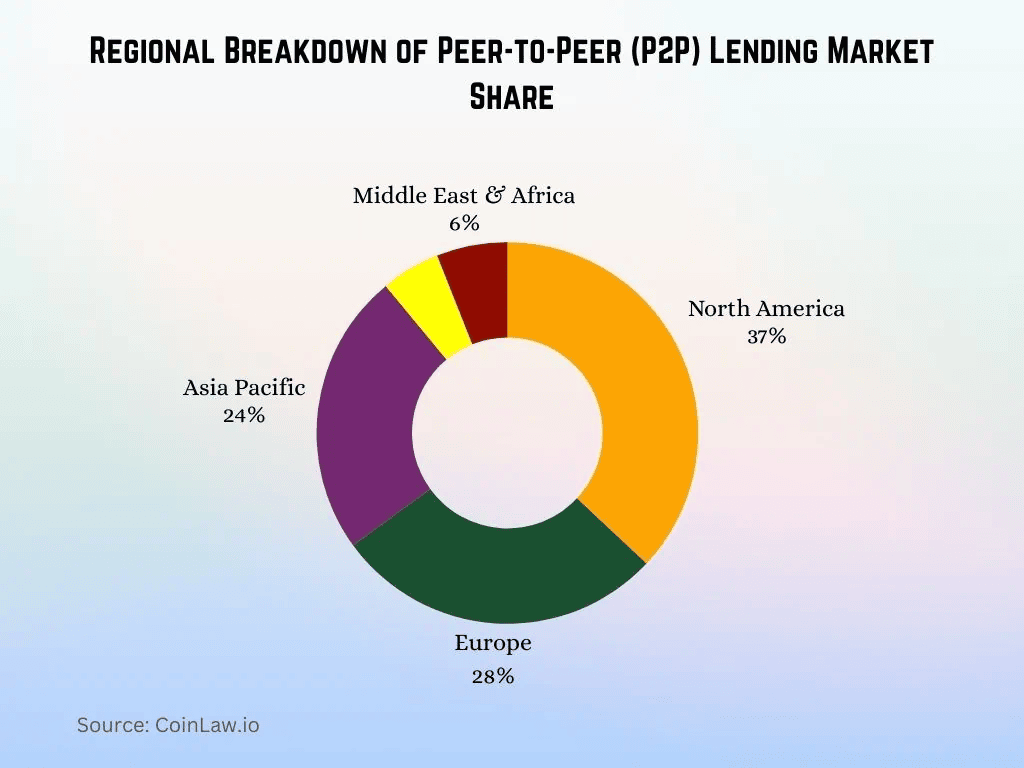

Peer-to-Peer Lending Market By Region

(Source: coinlaw.io)

- The global peer-to-peer (P2P) lending market is analyzed in terms of its geographical distribution, and areas having the highest adoption rate and growth potential are spotlighted.

- North America controls 37% of the market and is thus the most dominant region in P2P lending.

- A key contributor to such a scenario is the region’s modern financial infrastructure, the widespread use of digital platforms, and the strong consumers’ trust in fintech solutions.

- The second-largest market share belongs to Europe, accounting for 28%.

- It is due to the ever-growing adoption of alternative finance platforms and the presence of clear regulatory frameworks that help P2P platforms operate more securely and efficiently that this share is being maintained.

- Asia Pacific comes next with a 24% share and is expected to undergo tremendous growth in the near future. This has been made possible by the rapid digital transformation, growing smartphone penetration, and the emergence of fintech ecosystems in countries like India, China, and Southeast Asia that are already contributing to the overall growth.

- The Middle East and Africa (MEA) has a small 6% market share compared to other regions, indicating that P2P lending is becoming more popular in areas where traditional banking services are scarce.

- By 2023, Latin America would still account for 5% of the market; however, it has significant potential for future growth, driven by support from financial inclusion programs and the expansion of digital banking across the region.

- Thus, P2P lending is expanding its presence not only in existing markets but also in developing ones.

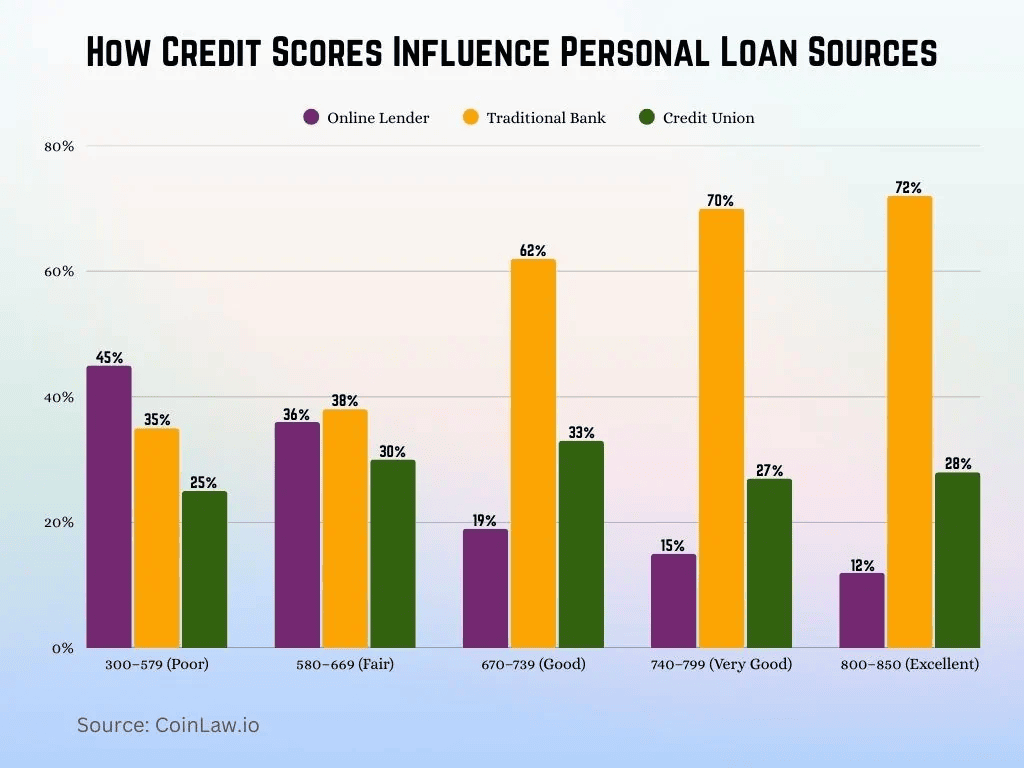

How Credit Scores Influence Personal Loan Sources

(Source: coinlaw.io)

- People with low credit scores, particularly those in the 300–579 range, are much more inclined to use an online lender.

- This category has about 45% of its borrowers using online lending platforms, the highest share across all credit groups.

- Moreover, once a credit score improves, online lenders’ dependency drops significantly, with only around 12% of the best credit score holders (800–850) choosing this route.

- The implication is that online lenders often serve the same clientele that would have been refused traditional financing.

- On the other hand, they are heavy users of traditional banks and are ordinary borrowers with high credit scores.

- The tendency to opt for a bank loan steadily increases with higher creditworthiness.

- Around 62% of good credit (670–739) lenders rely on traditional banks, rising to 70% for very good (740–799) and peaking at 72% for excellent scores.

- Conversely, among those with poor credit, only about 35% are bank users, indicating that banks’ lending policies are quite strict.

- Credit unions are consistently used, regardless of a person’s credit score.

- The percentage share of credit unions among borrowers usually ranges from 25% to 33%, depending on their credit score.

- Good credit customers are slightly more inclined toward credit unions, with around 33% choosing them, but on the whole, credit unions cater to a wide range of customers and are not particularly associated with either high or low credit scores.

Default Rates and Risk Assessment

- Risk management is a top priority in the P2P lending business, as platforms must ensure lenders’ long-term sustainability.

- In 2023, P2P loan default rates worldwide averaged 4.5%, suggesting that, through the application of newer technologies and better screening methods, loan failures are being controlled.

- Consumer loans are generally considered less risky, with a default rate of 3.2%, compared to small business loans at 5.8%.

- To minimize these risks, around 60% of the P2P platforms are now using artificial intelligence-based credit-scoring systems.

- These systems process borrower data more precisely and have been instrumental in reducing default rates by an average of 15%.

- Besides, losing the principal amount to defaults doesn’t mean the investor won’t get anything back; they can still recover roughly 55% of the loan value due to advancements in recovery and collection, as well as established processes.

- Thus, after considering defaults and recovery rates, peer-to-peer investors still get a risk-adjusted return of about 6.5% which is why P2P is an attractive alternative investment option.

- The share of these loans in riskier areas is approximately 20%, and lenders receive further assurance that their loans are backed by an asset in the event of borrower default.

- Nevertheless, there are still riskier segments of the market, such as cryptocurrency-backed loans, with a default rate of 7%. Thus, this market requires an extremely careful risk assessment while investing.

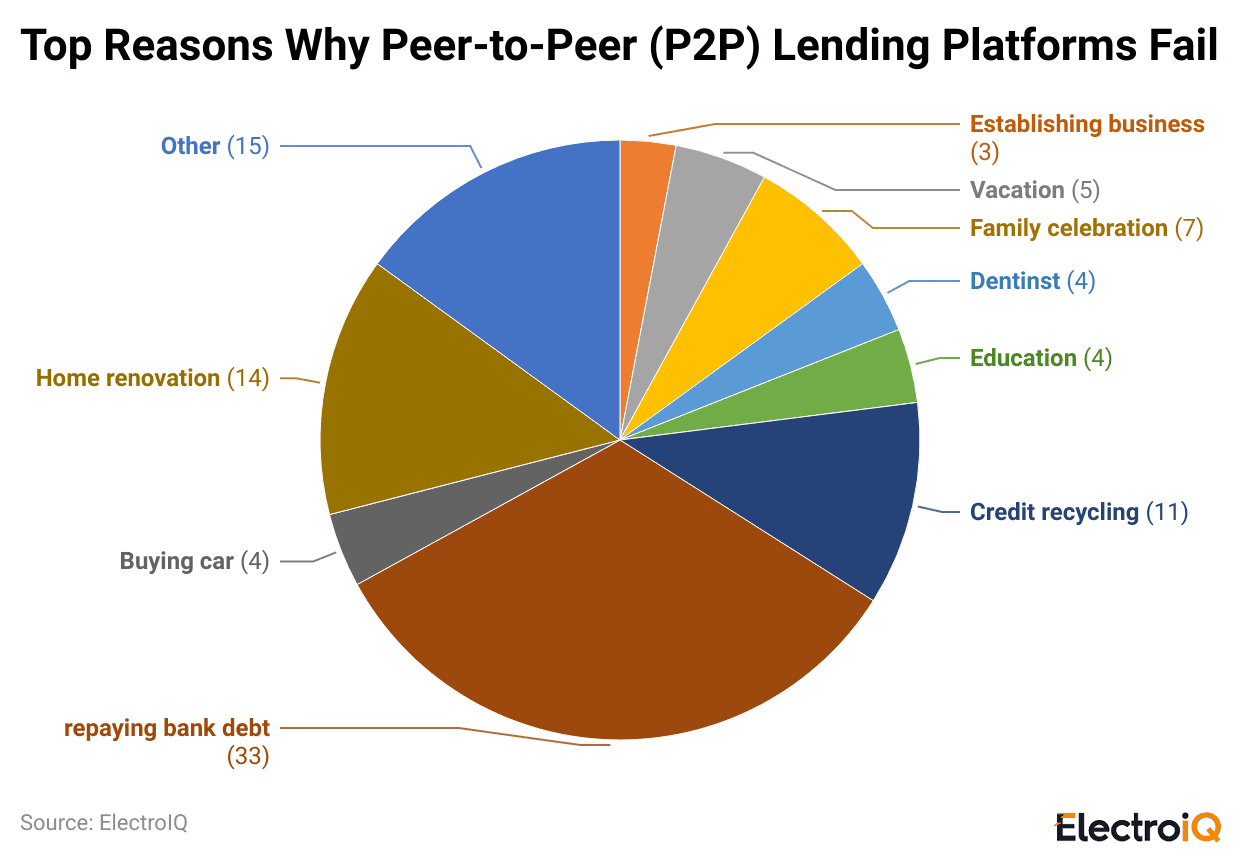

Top Reasons Why Peer-to-Peer (P2P) Lending Platforms Fail

(Reference: coinlaw.io)

- The use of funds by borrowers is one of the most important factors leading to quarantined P2P loan failures.

- The most frequent cause is taking out loans to consolidate existing bank debt, which accounts for up to 33% of the overall default rate.

- Another 15% of borrowers simply say they were unable to repay their loans due to personal or financial issues, indicating that, in this case, it is very difficult to anticipate unexpected situations.

- Among the reasons for defaults, home renovations are a major one, accounting for 14%. Such projects usually cost much more than initially planned.

- Credit recycling, which means using a new loan to pay off an old one, is responsible for 11% of defaults and makes borrowers’ financial situation even worse.

- Discretionary family celebrations account for 7% of loans, while vacations account for 5%, indicating that such loans are risky to use for non-essential purposes.

- Besides, there are other reasons, such as purchasing a car (4%), undergoing dental treatment (4%), and taking educational loans (4%), which might not always lead to quick financial gains.

- A new business venture corresponds to 3% of defaults, indicating the high risk associated with business start-ups.

- These factors together indicate that both poor financial management practices and unexpected life events are the primary reasons P2P loans default.

Recent Developments

- Funding Circle, which was a pioneer in retail peer-to-peer lending, bounced back strongly by July 2025.

- The UK firm, through its significant credit issuance in H1 2025 compared to last year, brought the company back to profitability after restructuring and exiting the U.S. market.

- A new management not only required the company to change its funding strategy to institutional financing but also turned a huge loss into a small profit and projected a path to hike pre-tax profits and sales by 2026, a move indicative of the rebound in investor trust.

- The Carlyle Group, on June 12, 2025, through Citigroup, formed a partnership to offer asset-backed financing specifically for fintechs and P2P lenders.

- The hybrid structure of Carlyle’s infrastructure financing expertise and Citi’s private credit is set to cater to the growing demand for scalable funding by the upcoming lending platforms, thus indicating the increasing confidence of the institutional investors in the sector.

- In January 2025, Indian P2P platform LenDenClub unveiled a “Daily Earning Loan” product. This loan provides lenders with daily interest payments and the option to make early principal repayments, with a minimum tenure of 9 months, thus offering greater flexibility and quicker returns.

- In October 2024, IndiaP2P introduced its “Monthly Income Plan-Plus”, keeping in line with the Reserve Bank of India’s revised guidelines regarding faster settlements. Investors are to receive a maximum of 18% per annum as monthly pay-outs.

- In December 2024, Defender Global set up its own P2P lending platform, where it had to raise US$235,000 to invest in real-world, asset-backed projects.

- The company plans to capitalise on the rising interest in more tangible, investment-grade P2P projects.

Conclusion

Peer-to-Peer Lending Statistics: Peer-to-peer lending has now developed into a rapidly growing global industry with significant potential for the long term. The rise in market size, the growing number of users, and expanding participation across regions are making P2P platforms a significant part of the financial ecosystem. The presence of defaults among borrowers and misuse of funds are among the risks. Yet, the enhancement of AI-powered solutions in credit scoring, collateralization, and recovery is gradually cementing the trust of the platforms and the investors.

Moreover, recent trends, such as institutional engagement and the creation of innovative products, indicate the sector’s maturation and its ability to attract serious financial support. To sum up, the P2P lending sector is poised to become a major player in the future of digital finance.

FAQ.

The market is being driven by higher demand for educational and medical loans, digital approvals being faster, terms being more flexible, government policies being more lenient, and global fintech platforms being more widely adopted. All these factors are contributing to the industry’s projected CAGR of 25.73% until 2034.

North America is in the lead with a 37% market share, followed by Europe with 28% and Asia-Pacific with 24%. The Asia-Pacific region is expected to experience significant growth owing to the digital transformation in developing economies.

Poor credit scorers are primarily inclined to the online P2P lenders (nearly 45%), while borrowers with excellent scores are mainly attracted to the traditional banks (approx. 72%). Credit unions, on the other hand, do not differentiate among credit groups, and thus their market share is between 25% and 33%.

The typical default rate is approximately 4.5%. Consumer loans are less risky than small business or crypto-backed loans. AI-assisted credit scoring and collateral-backed loans are decreasing the danger, and investors continue to receive a risk-adjusted return of around 6.5% per annum.

The foremost reason is utilizing loans for paying off existing bank debts (33%), and then come home renovations (14%) and credit recycling (11%) as second and third reasons, respectively. Other causes are holiday trips, health expenses, buying cars, and embarking on startups, among others.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.