Bank Investment Product Uptake Statistics by Market Size, Traditional Preference, Trends, Insights and Facts (2026)

Updated · Jan 14, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Investment Banking Market Size

- Bank CDs And Time Deposits – Traditional Preference

- Money Market Funds – Cash Alternatives Gaining Traction

- Mutual Funds: Long-Term Core Holdings

- ETFs: Rapid Growth In Assets And Inflows

- Direct Indexing – Personalised Portfolio Uptake

- Managed Accounts – Expansion Of Advisor-Led Programs

- Conclusion

Introduction

Bank Investment Product Uptake Statistics: Banking Investment product uptake refers to the number of customers who initiate and maintain use of such products as mutual funds, bonds, and fixed deposits. Greater uptake helps banks earn more fee income and build stronger customer relationships. This further encourages customers to make regular savings and supports educational, homeownership, and retirement plans. In recent years, digital sign-up has become faster, mobile apps have become simpler, and as more products are available online, uptake has increased substantially.

However, many people still hold back due to fear of losses, unfavourable terms, and concerns about hidden fees or misadvice. This article introduces the key drivers and barriers to adoption, outlines how banks can responsibly increase uptake, and highlights steps to build trust and awareness.

Editor’s Choice

- Bank CDs/time deposits remained high: large time deposits at all commercial banks were about USD 2.34 trillion in Dec 2024 (2,341.6456 billion), according to FRED data.

- They are estimated to reach around USD 2.40 trillion in Nov 2025 (2,401.4805 billion).

- Small-denomination time deposits totalled USD 1.05 trillion in Nov 2025 (1,049.9 billion).

- ICI reported money market mutual funds at USD 7.67T for the six days ended Dec 23, 2025.

- By the end of Oct 2025, U.S. ETF assets had climbed to USD 13.08 trillion, and net inflows reached USD 1.14trillion.

- MMI further noted that managed account assets totalled USD 13.7 trillion as of Q1 2025 and that direct indexing could reach USD 1 trillion by the end of 2025.

- Meanwhile, Fortune Business Insights projects the robo-advice market to reach USD 10.86 billion in 2025.

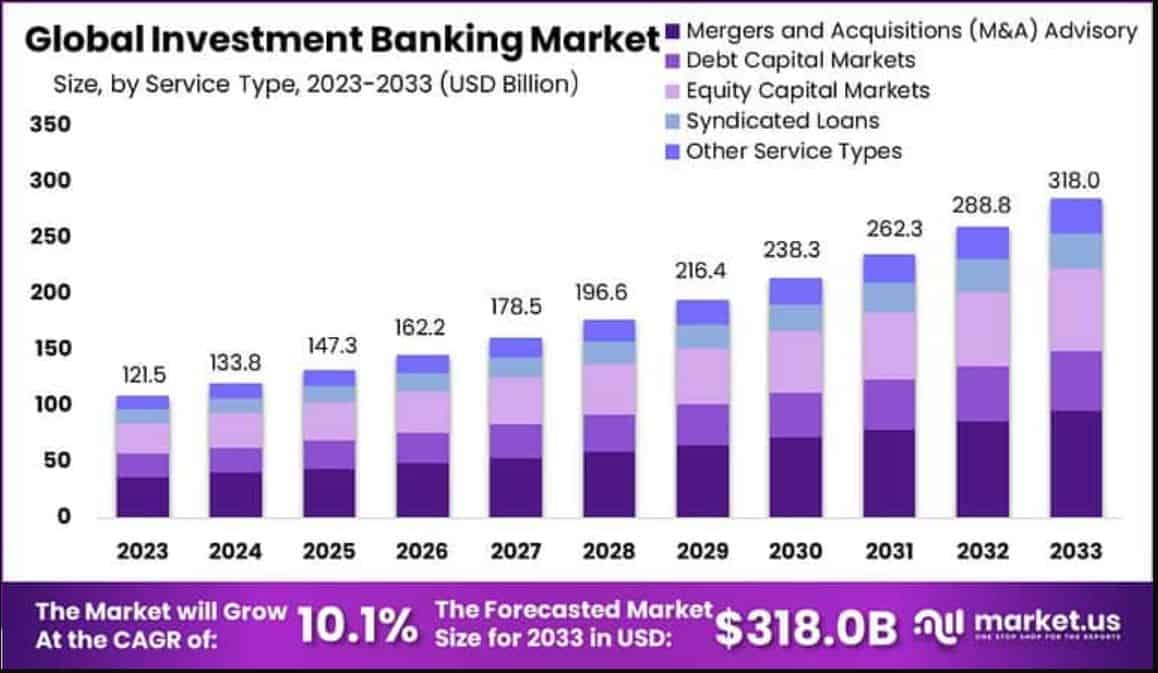

Investment Banking Market Size

(Source: market.us)

- The global investment banking market is projected to reach approximately USD 147.3 billion by 2025, up from USD 133.8 billion in 2024.

- Furthermore, investments are projected to increase in the coming years: USD 162.2 billion in 2026, USD 178.5 billion in 2027, USD 196.6 billion in 2028, USD 216.4 billion in 2029, USD 238.3 billion in 2030, USD 262.3 billion in 2031, USD 288.8 billion in 2032, and USD 318 billion in 2033.

- The market is estimated to grow at a CAGR of 10.1% from 2025 to 2033.

(Source: thefinancialbrand.com)

- As of June 2025, financial services firms measure engagement using product adoption (37%).

- Followed by customer retention (29%) and customer lifetime value (LTV) at 28%.

Bank CDs And Time Deposits – Traditional Preference

- According to FRED reports, in 2025, large time deposits at U.S. commercial banks remained between USD 2,390 billion and USD 2,400 billion.

- As of July 2025, it accounted for USD 2,395.1577 billion, followed by USD 2,403.2372 billion (Aug 2025), USD 2,394.4312 billion (Sep 2025), USD 2,391.6413 billion (Oct 2025), and USD 2,401.4805 billion (Nov 2025).

| Category | Metrics | Date | Value |

|

Large time deposits

(weekly, not seasonally adjusted) |

Large time deposits

|

November 19, 2025 | USD 2,401.186 billion |

| November 26, 2025 | USD 2,418.726 billion | ||

| December 3, 2025 | USD 2,411.088 billion | ||

| December 10, 2025 | USD 2,424.515 billion | ||

| December 17, 2025 | USD 2,422.485 billion | ||

|

Small-denomination time deposits

(under USD 100,000) |

Small-denomination time deposits

|

July 2025 | USD 1,065.3 billion |

| August 2025 | USD 1,073.5 billion | ||

| September 2025 | USD 1,077.5 billion | ||

| October 2025 | USD 1,064.3 billion | ||

| November 2025 | USD 1,049.9 billion | ||

|

FDIC national rate

(12-month CD, <100M) |

12-month CD national rate

|

August 2025 | 1.76% |

| September 2025 | 1.70% | ||

| October 2025 | 1.68% | ||

| November 2025 | 1.64% | ||

| December 2025 | 1.63% |

Money Market Funds – Cash Alternatives Gaining Traction

- ICI reported that in the week ended March 5, 2025, money market assets jumped USD 51.15 billion to a record USD 7.03 trillion (government USD 5,765.92 billion; prime USD 1,127.48 billion; tax-exempt USD 131.99 billion).

- Meanwhile, FRED logged USD 7,397,905 million in Q1 2025 and USD 7,481,232 million in Q2 2025.

| Updates | Total money market fund assets | Change | Government funds | Prime funds | Tax-exempt funds | Retail | Institutional |

| Week ended Oct 22, 2025 | USD 7,397.69 billion | +USD 30.37 billion | USD 6,043.42 billion | USD 1,214.97 billion | USD 139.30 billion | USD 2,997.36 billion | USD 4,400.33 billion |

| Six-day period ended Dec 23, 2025 | USD 7,673.39 billion | +USD 7.49B billion | USD 6,301.19 billion | USD 1,223.72 billion | USD 148.49 billion | USD 3,068.45 billion | USD 4,604.95 billion |

Mutual Funds: Long-Term Core Holdings

- According to ici.org, in mid-2025, U.S. mutual funds held around USD 29.7 trillion.

- In 2025, 53.9% of households (about 72.7 million) owned mutual funds, totalling 123.2 million shareholders, and these assets accounted for more than one-fifth of households’ financial assets.

- From May to June 2025 survey of 9,021 households, 4,861 (53.9%) reported owning mutual funds, with around a 1.4% margin of error at the 95% confidence level.

- In 2025, a typical fund-owning household will have USD 125,000 in income, USD 370,400 in financial assets, and USD 125,000 invested in three mutual funds.

- Additionally, 73% held funds in employer retirement plans, and 72% held them outside such plans.

- The primary purchasing channels were employer plans (54%), the sales force (34%), and direct marketing (12%).

ETFs: Rapid Growth In Assets And Inflows

- As of October 2025, ETFGI LLP reported that American ETF assets reached USD 13.08 trillion, followed by USD 186.19 billion of net inflows and USD 1.14 trillion in YTD inflows.

- By the end of November 2025, the assets had risen to USD 13.22 trillion.

| ETF provider | Assets (USD trillion) |

Share |

| iShares | 3.92 | 29.7% |

| Vanguard | 3.81 | 28.8% |

| State Street SPDR | 1.81 | 13.7% |

- ICI reported total U.S. ETF assets of USD 13.01 trillion in October 2025.

- Followed by domestic equity USD 8,451.6 billion, global/international equity USD 2,039.3 billion, bonds USD 2,170.7 billion, hybrid USD 50.0 billion, and commodities USD 301.5 billion.

- Meanwhile, with USD 557.8 billion gross issuance, USD 375.9 billion gross redemptions, USD 181.9 billion net issuance in October, and USD 1,090.6 billion net issuance YTD 2025.

- ICI also estimated USD 43.53 billion in net issuance for the week ended Oct 22, 2025 (equity USD 27.708 billion, bonds USD 10.674 billion, commodities USD 5.323 billion, hybrids USD 0.172 billion), and USD 51.63 billion for the week ended Dec 17, 2025.

- Globally, ETFGI reported USD 19.44T in ETF assets at the end of November 2025, with USD 218.24 billion in November inflows and USD 2.04T in YTD inflows.

- Moreover, the industry had 15,610 products from 949 providers on 83 exchanges in 65 countries.

Direct Indexing – Personalised Portfolio Uptake

- MMI-Cerulli reports also stated that managed account assets rose by 7.7% in the second quarter of 2025 to USD 14 billion, down by 0.2% from the first quarter.

- Total net flows amounted to USD 214 billion, including USD 69 billion to UMAs and USD 65 billion to SMAs.

- A press release dated October 7, 2025, reported that SMA assets totalled USD 3.86 trillion in Q1 2025, representing a 54.1% increase over the past two years.

- The same release reported average redemption rates of 21.1% for equity strategies and 15.9% for fixed income strategies.

- Natixis (Dec 17, 2025) reported that about 18% of advisors use direct indexing, with assets above USD 860 billion.

Managed Accounts – Expansion Of Advisor-Led Programs

- MMI-Cerulli’s Q1 2025 Advisory Solutions data says that, as the S&P 500 fell more than 4%, managed account assets dipped 0.2% to USD 13.7 trillion, and only rep-as-advisor (RA) programs fell because outflows outweighed inflows.

| Metrics | Key Descriptions |

| Growth & flows | ETF advisory programs +1.2%, UMAs +1.1%, and SMAs +1.0% led. |

| Q2 2025 assets | Assets rebounded 7.7% to USD 14.8 trillion; ETF advisory +9.6%, UMAs +9.4%. |

| Q2 2025 net flows | USD 214 billion, staying above USD 200 billion for the 4th straight quarter. |

| Direct index vs SMA sleeves | Direct index assets passed USD 1 trillion, ahead of muni fixed income, USD 645 billion and taxable fixed income, USD 396 billion. |

| SMA totals | Total SMA assets USD 3.86 trillion in Q1 2025 (incl. SMAs inside UMAs), up 54.1% in two years. |

| Redemptions | Average redemption rates: 21.1% equity, 15.9% fixed income; 23% and 25% say SMAs match mutual funds, 8% say higher. |

Conclusion

Bank investment product uptake is growing rapidly as more people seek safe and simple ways to grow their money. Easy online access, greater awareness, and numerous product options are prompting investors to consider mutual funds, fixed deposits, bonds, and insurance plans.

Still, trust, clear details, and right advice guide their choices. Banks can increase adoption by displaying fees openly, keeping processes simple, and providing strong customer support. Overall, steady education and user-friendly services will help more customers choose suitable investment products with confidence.

Sources

FAQ.

Many people choose banks because they perceive them as safe and reliable. Banks also make investing easy through branches and mobile/online services, and they offer many options in one place.

Banks commonly offer fixed deposits, recurring deposits, mutual funds, bonds, government-backed plans, ULIPs, and investment-linked insurance products.

Customers often decide based on product safety, the returns they may receive, the bank’s reputation, ease of purchase, interest rates, fees, and guidance from bank employees.

Apps and internet banking help people check products, invest quickly, track performance, and manage their money anytime, from anywhere.

Some people avoid the products because they do not understand them, worry about losing money, are unsure about fees, receive weak advice, or feel confused about what suits their goals.

Maitrayee Dey has a background in Electrical Engineering and has worked in various technical roles before transitioning to writing. Specializing in technology and Artificial Intelligence, she has served as an Academic Research Analyst and Freelance Writer, particularly focusing on education and healthcare in Australia. Maitrayee's lifelong passions for writing and painting led her to pursue a full-time writing career. She is also the creator of a cooking YouTube channel, where she shares her culinary adventures. At Smartphone Thoughts, Maitrayee brings her expertise in technology to provide in-depth smartphone reviews and app-related statistics, making complex topics easy to understand for all readers.