Faraday Statistics By Market And Performance (2026)

Updated · Apr 17, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Faraday Future 2025 Financial Performance

- Faraday Future Loss Compression Efforts, Capital Reliance, and Strategic Transition

- Faraday Future 2026 Strategic Outlook

- The FX ‘Bridge Strategy’ – 2026 Mass Market Pivot

- Faraday EAI Robotics – First-Quarter Gross Margin Analysis

- Conclusion

Introduction

Faraday Statistics: Faraday Future currently stands as the most ambitious electric vehicle (EV) business, which operates with unpredictable market performance. The company began its path to commercial expansion through its main product, Faraday Future FF 91, which became available between 2025 and 2026 after initial development work. The company operates advanced technology that combines artificial intelligence with luxurious transportation solutions and exceptional operational capabilities, but it struggles with financial difficulties, decreased manufacturing output, and business process challenges.

Faraday Future manages its premium electric vehicle business through this period, which represents a crucial turning point as the company struggles to secure funding to support its growth. This article will examine the trending Faraday statistics and its financial performance in the EV field.

Editor’s Choice

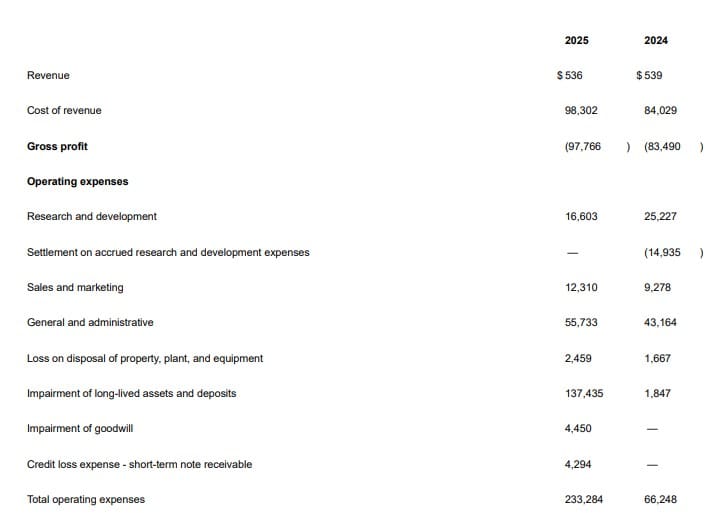

- The revenue between 2025 and 2024 remained stable, with a revenue total of USD 536 million for 2025 and USD 539 million for 2024.

- A revenue cost increase, which reached USD 98.3 billion, resulted in a gross profit loss of USD 97.8 billion.

- Total operating expenses increased to USD 233.3 billion from USD 66.2 billion YoY.

- The company recorded a long-lived asset impairment of USD 137.4 billion, which resulted in substantial write-downs.

- A goodwill impairment of USD 4.45 billion occurred because of poor asset value estimation.

- Research and development expenses reduced from USD 25.2 billion to USD 16.6 billion, which demonstrates effective financial management.

- Sales and marketing spending increased by 33% compared to the previous year, which brought total costs to USD 12.3 billion.

- A large increase in its general and administrative expenses, which reached USD 55.7 billion.

- A full operating loss of USD 331 million, which included a fourth quarter loss of USD 32.3 million.

- The adjusted operating loss reached USD 185 million because of initial effects from the restructuring process.

- An operating cash outflow of USD 107.5 million for the year 2025.

- Financing inflows of USD 161.4 million, which represented a 100% increase from the previous year, because the company depended on funding.

- The stockholders’ equity declined to USD 7.7 million, which demonstrated that the company had poor balance sheet financial strength.

- FX strategy targets 400,000–500,000 vehicle sales over five years (~80,000–100,000 annually).

- Robotics division shipped 22 units in Q1 2026 and targets 1,000 units by year-end.

Faraday Future 2025 Financial Performance

(Source: investors.ff.com)

- The 2025 financial results of Faraday Future’s annual report 2025 demonstrate that its electric vehicle business operates at a high-risk level because it needs to recover from its current financial difficulties, which stem from rising expenses and asset losses, while bringing in only limited revenue.

- The company achieved minimal revenue growth with 2025 revenue at USD 536 million, which shows no improvement from the previous year when 2024 revenue reached USD 539 million because the company continued to invest in product development and market expansion efforts.

- The company experienced a massive revenue increase, which brought its total cost of revenue to USD 98.3 billion, while it suffered a USD 97.8 billion gross profit loss because of production inefficiencies and insufficient production capacity.

- The financial burdens increase through operating expenses, which create additional financial difficulties. Total operating expenses ballooned to USD 233.3 billion in 2025, up sharply from USD 66.2 billion in 2024, driven largely by extraordinary charges.

- The most notable is impairment of long-lived assets at USD 137.4 billion, alongside goodwill impairment of USD 4.45 billion, signaling asset revaluation and weak future cash flow expectations.

- The main expense categories show different financial patterns. R&D expenses declined to USD 16.6 billion (from USD 25.2 billion), suggesting cost rationalization or constrained innovation spending, while sales and marketing rose to USD 12.3 billion (+33% YoY), reflecting efforts to build brand presence.

- The company experienced an increase in general and administrative costs, which reached USD 55.7 billion. Additional administrative expenses resulted in this increase.

- The company faces additional financial burdens, which include credit loss expenses that total USD 4.3 billion and losses that result from asset disposals. These expenses create problems for the company, which affect both its cash flow and its ability to run operations.

- The company needs to meet two requirements before it can achieve profitability, because it lacks both substantial revenue growth and effective cost management.

- Faraday Future has strategic execution challenges that depend on external funding sources, which makes their path to profitability extremely unpredictable.

Faraday Future Loss Compression Efforts, Capital Reliance, and Strategic Transition

- The 2025 financial profile of Faraday Future shows that the company needs to manage its costs while dealing with financial needs and structural problems.

- The company suffered an operating loss of 32.3 million dollars during the fourth quarter of 2025 and experienced a total annual loss of USD 331 million, which resulted from asset impairments, revenue costs, and high general and administrative expenses, according to company filings.

- The adjusted operating loss decreased to 185 million dollars after removing one-time items, which showed that the company made initial progress with its cost management and operational improvement efforts.

- The company recorded a major loss because of strategic asset impairments, which occurred during its shift from the FF 91 program to the enhanced FF 92 and FX Super One platform, thus showing a portfolio change instead of operational challenges.

- Faraday experienced an operating cash outflow of 107.5 million dollars during 2025 because of its working capital needs and expenses related to increasing production capacity.

- The company secured financing cash inflows worth USD 161.4 million, which increased by 100 % compared to the previous year, thus proving that FF can still obtain outside funding even though the EV capital market faces difficulties.

- The stockholders’ equity reached only USD 7.7 million, which shows that the company has limited capital resources and faces financial risk from convertible instruments and fair value changes.

- The company depends on equity-linked financing methods, which create risks that will result in earnings fluctuations and shareholder dilution.

- The company seeks external capital through strategic investments while aiming to enhance its capital structure during its 2026 capital strategy implementation.

- The company achieved its goal of reducing potential dilution through the cancellation of 44.6 million warrants, which served as evidence of its active management of the balance sheet.

- The upcoming USD 500,000 stock purchase program demonstrates internal confidence among employees and executives who will buy company shares to create management incentives that mirror shareholder objectives.

- A Nasdaq deficiency notice in March 2026 for failing to maintain a USD 1.00 minimum bid price, which required the company to achieve compliance within 180 days because of this condition.

Faraday Future 2026 Strategic Outlook

- The 2026 forecast of Faraday Future shows that the company will shift its operations from electric vehicle manufacturing toward building an artificial intelligence robotics system, which includes software components, because this approach helps them to solve their existing issues with cash flow and business expansion.

- EAI Robotics at the company drives this transition through its shipment goal of 1000 units, which it needs to achieve by December 2026, while reaching positive gross margins, which serve as an important target because of its history of losing money, according to company projections.

- The company needs to complete the FX Super One product delivery through its scheduled implementation phases, which focus on developing products that will compete effectively in the market while maintaining continuous revenue streams.

- The essential change occurs because FF wants to develop a DeviceDataBrain system that will function like the business models developed by Tesla and other top companies.

- The system connects hardware systems with data collection operations and artificial intelligence model creation to establish a persistent loop that speeds up product development and financial performance enhancement.

- FF is making technological progress through its EAI Brain platform and open-source developer ecosystem, which it develops together with top U.S. research institutions.

- The centralized data training center construction, which will finish by Q3 2026, will boost AI abilities and autonomous systems development and robotic intelligence progress, enabling FF to enter fast-expanding markets, which include humanoid robotics, edge AI, and intelligent automation.

- The management team wants to show that EAI Robotics needs fewer funds for its operations compared to EV production, which demonstrates that the company will grow by using a cost-effective growth strategy.

- The company intends to achieve revenue diversification through software monetization and AI services, which will create software-related revenue streams that it expects to generate in 2026.

- FF aims to rebuild investor trust through financial recovery while fulfilling regulatory requirements, which include reaching the Nasdaq minimum bid price within 180 days.

- The company is also pursuing strategic institutional investments to improve liquidity, reduce dilution, and lower financing costs.

The FX ‘Bridge Strategy’ – 2026 Mass Market Pivot

- Faraday Future’s FX Bridge Strategy marks a decisive pivot from its historically narrow ultra-luxury EV positioning toward a scalable, volume-driven mass-market EV model, anchored by the FX Super One MPV and the upcoming FX 4 crossover.

- The FX Super One system, which uses the WEY Gaoshan platform as its foundation, achieves faster market launch times while decreasing both development risks and development costs.

- The FX lineup aims to enter high-volume markets, which differs from the USD 300,000 FF 91, according to management, which predicts that 400,000 to 500,000 vehicles will sell during the next five years.

- The company expects to achieve annual sales between 80,000 and 100,000 units, which will make FX its first viable route to achieving positive operating cash flow within three years.

- The company recorded approximately 2,500 B2B pre-orders for the Super One, together with more than 11,000 non-binding reservations and 1,200 robotics deposits, which demonstrate the company’s progress in establishing a multi-product ecosystem.

- The current numbers show limited progress compared to industry standards, which require accurate execution results because FF has only managed to deliver 16 vehicles before the start of 2025.

- The company considers its partnership with Hebei Huanzhou Automobile Sales Co., Ltd. as a fundamental component of its operational framework.

- The seven-agreement framework—covering procurement, engineering, IP, and after-sales—creates a low-cost supply chain backbone, potentially enabling target gross margins of ~20%, comparable to leading EV players like BYD.

- The hybrid system for China and the United States combines Chinese manufacturing capabilities with American AI software that complies with regulations, which provides distinct regulatory benefits under ICTS systems.

- The phased rollout strategy, which includes testing 50 units during Q2 of 2026, conducting limited B2B operations during Q3, and delivering products to all consumers before the end of 2026, helps the company restore investor trust through sequential accomplishment proof points.

- The company expands internationally into markets such as the UAE, which charges approximately USD 84,000 for its products to create immediate revenue streams while gathering practical market information.

- The FX 4 functions as a RAV4 disruptor, which enables FF to pursue its goal of becoming a mainstream electric vehicle producer in the United States market that generates approximately 400000 annual vehicle sales.

- The FX Bridge Strategy develops into a high-risk, high-reward transformation for the company, which employs asset-light manufacturing and artificial intelligence technology to create unique products and operate international supply chains.

- The success of the system depends on the ability to execute tasks, and the company needs to develop execution discipline and scaling capacity while securing funds throughout the period from 2026 until 2028.

Faraday EAI Robotics – First-Quarter Gross Margin Analysis

- Faraday Future’s Q1 2026 EAI Robotics performance represents a structural inflexion point, not because of scale, but because of unit economics transformation and business model validation.

- The division shipped 22 cumulative units by March 2026, which exceeded its internal target of 20 units.

- The company achieved a positive product gross margin during its first commercial quarter, which represents a milestone after nine years of operation.

- The performance of this milestone stands in direct opposition to the electric vehicle sector, which shows that the FF 91 model produces negative gross profits of 15.6 million dollars during the fourth quarter of 2025.

- The field of robotics shows initial profitability through its current operational performance because the company concentrates on developing high-margin artificial intelligence hardware and software systems.

- The robotics rollout, launched in February 2026, introduced three product lines—Futurist, Master, and Aegis—targeting education, home security, and entertainment verticals.

- Hardware startups typically need to sell thousands of units before they reach breakeven, yet this company achieved a positive gross margin after selling only 22 units.

- The management team aims to ship 1,000 units during fiscal year 2026, which requires a 45x increase from the first quarter shipment volume.

- The ability to execute operations effectively becomes the primary performance metric that investors should monitor.

- The robotics system will evolve from proof-of-concept status to generate revenue, which will produce multi-million-dollar revenue growth based on different average selling price (ASP) projections.

- The company uses a monetization strategy that generates revenue through multiple channels that extend beyond its hardware products. FF is building a “Device + Software + Data” revenue stack, where recurring income streams—AI subscriptions, skills licensing, and data services—could significantly enhance lifetime value (LTV) per unit.

- The company uses its Device–Data–Brain system to create a flywheel effect, which uses robot data to enhance AI models that boost product value, which drives future sales.

- The educational sector, through its United States K-12 educational system and University of California institutions, functions as an effective business-to-business channel that provides educational institutions with budget-friendly purchasing options and generates ongoing software income that sets it apart from companies that develop consumer robotics products.

- FF achieved its financial growth through stockholders’ equity improvement after completing a USD 100 million debt restructuring process, which enabled the company to reach its first stage of positive equity and positive gross margin, which serves as the fundamental requirement for achieving long-term business viability.

- The company needs to develop its manufacturing and supply chain systems while meeting regulatory standards because its production targets will increase from 22 units to 1,000 units, which represents a significant scaling challenge.

- Faraday faces multiple operational hazards, which may result in reduced profit margins that it gained during its initial phase of business operations.

Conclusion

Faraday Future operates as a high-risk, high-reward electric vehicle manufacturer. The company is currently undergoing a major transformation from a capital-intensive automotive business model to the development of an AI and robotics-based ecosystem. The financial records show major operational inefficiencies, which lead to negative profitability, and the company needs to secure funds from outside sources. The business shows potential for strategic advancement because the company has achieved two positive results through its decreased financial losses and its profitable robotics operations.

The company can generate additional revenue through its FX Bridge Strategy and its robotics expansion while achieving better financial performance through improved unit economics. Company operations continue to face three major obstacles, which include execution difficulties, limited operational capacity, and financial resources. The organization needs to increase production levels while keeping operational costs low and maintaining the trust of its investors in order to achieve its long-term goals.

Sources

FAQ.

Faraday Future reported revenue of approximately USD 536 million in 2025.

High production costs, asset impairments, and low vehicle volumes drive significant losses.

It is a mass-market EV plan targeting 400,000–500,000 vehicle sales over five years.

Yes, its EAI Robotics division shipped 22 units in Q1 2026 and targets 1,000 units in 2026.

The company faces major dangers because it depends on funding while having low production capacity, negative cash flow and operational difficulties.

Tajammul Pangarkar is the co-founder of a PR firm and the Chief Technology Officer at Prudour Research Firm. With a Bachelor of Engineering in Information Technology from Shivaji University, Tajammul brings over ten years of expertise in digital marketing to his roles. He excels at gathering and analyzing data, producing detailed statistics on various trending topics that help shape industry perspectives. Tajammul's deep-seated experience in mobile technology and industry research often shines through in his insightful analyses. He is keen on decoding tech trends, examining mobile applications, and enhancing general tech awareness. His writings frequently appear in numerous industry-specific magazines and forums, where he shares his knowledge and insights. When he's not immersed in technology, Tajammul enjoys playing table tennis. This hobby provides him with a refreshing break and allows him to engage in something he loves outside of his professional life. Whether he's analyzing data or serving a fast ball, Tajammul demonstrates dedication and passion in every endeavor.