Seagate Statistics By Revenue, Employees and Facts (2025)

Updated · Nov 12, 2025

Table of Contents

- Introduction

- Editor’s Choice

- About Seagate

- History of Seagate

- Fun Facts About Seagate

- Seagate Revenue And Profits

- Seagate GAAP And Non-GAAP Financial Overview

- Seagate Price Targets

- Seagate Shipping

- Seagate Inventory

- Seagate Employees Demographics Statistics

- STX’s Margin Details

- STX’s Balance Sheet And Cash Flow

- STX’s Strong Fiscal Q2 Business Outlook

- Recent Performance Of Competitors

- Risk And Concern

- Conclusion

Introduction

Seagate Statistics: By 2025, Seagate will be synonymous with storing huge amounts of data in a cost-effective and trustworthy manner. The organization made a strong push for the new generation of high-capacity HDDs, acquired a key player in the equipment manufacturer sector, and, at the same time, recorded an increase in quarterly revenue due to the increase in demand driven by cloud and AI workloads. Below, you will find a concise, data-driven narrative of Seagate’s 2025 statistics, including revenue, price targets, shipping, inventory, and key metrics that indicate the company’s direction.

Editor’s Choice

- Seagate’s total revenue for the financial year 2025 reached USD 9.1 billion, a 39% increase over USD 6.55 billion in 2024.

- The net profit for the year 2025 amounted to USD 1.47 billion, in contrast to USD 335 million for 2024 — a more than fourfold increase.

- In the last quarter of fiscal year 2025, the company reported USD 2.44 billion in revenue, representing a 30% increase compared to the same period last year. However, the quarterly profit decreased by 4.9% to USD 488 million.

- USD 831 million was the adjusted EBITDA, and the non-GAAP operating margin grew to 29%.

- Cash and cash equivalents reached USD 1.1 billion (up from USD 891 million), while long-term debt decreased from USD 5.0 billion to USD 4.9 billion.

- Operating cash flow was USD 532 million, while free cash flow remained unchanged at USD 427 million.

- The company paid out USD 153 million in dividends and repurchased 153,000 shares at an average price of USD 187, for a total cost of USD 28.7 million.

- The policy at the organization is to return no less than 75% of the free cash flow to the shareholders.

- Revenue forecast for Q2 FY2025: USD 2.7 billion ± USD 100 million, which is roughly 16% growth compared to the previous year.

- The non-GAAP EPS is projected to be USD 2.75 ± USD 0.20; the expected operating margin is ~30%.

- In Q2 FY2025, Seagate shipped 150.8 exabytes of HDD storage — this was an increase of 13.3 exabytes compared to the previous quarter and of 55.7 exabytes when looking at the year.

- Days Inventory Outstanding (DIO) was reported at 86 days, which is approximately 10 days longer than the company’s five-year average.

- Average one-year price target: USD 111.62 (high: USD 150, low: USD 60), implying ~47% upside from USD 75.78. Seagate’s total debt is approximately USD 5 billion, which is roughly five times its cash reserves of USD 891 million.

About Seagate

- Seagate has been driving innovation for over 45 years, maintaining a strong presence in data storage technology and hardware solutions.

- The company operates seven manufacturing facilities worldwide, ensuring stable production and supply across regions.

- There are 4 dedicated R&D sites actively developing advanced storage technologies and next-generation drive architectures.

- In 2024, Seagate produced a total of 550 exabytes (EB) of storage, reflecting its continued dominance in the global storage industry.

- The company reported USD 9.10 billion in revenue for fiscal year 2025, indicating stable financial performance amid evolving market conditions.

- Seagate’s Mozaic drives achieved a milestone with over 1 million units shipped, demonstrating rapid adoption of its latest technology.

- Each drive incorporates 50 different periodic elements, showcasing Seagate’s use of diverse materials for high precision and durability.

- The company applies nano-level engineering, using recording heads as small as 20 nanometers or less, which enhances storage density and performance.

- Seagate holds 3,703 active U.S. patents, highlighting its strong intellectual property portfolio in data storage technology.

- Within that portfolio, 592 patents specifically cover HAMR (Heat-Assisted Magnetic Recording) technology, underscoring its leadership in advanced storage innovations.

- Global data generation driven by AI applications is expected to reach 394 zettabytes (ZB) by 2028, a key driver for future storage demand.

- Seagate’s future drive capacity is projected to reach 50 terabytes (TB) by 2028, aligning with the industry’s need for high-capacity, energy-efficient data solutions.

History of Seagate

- 1978: Incorporated as Shugart Technology on November 1. The name was later changed to Seagate Technology to avoid conflict with Xerox’s Shugart Associates.

- 1979: Operations commenced in October under founders Al Shugart, Tom Mitchell, Doug Mahon, Finis Conner, and Syed Iftikar.

- 1980: Introduced the ST-506, the first 5.25-inch, 5 MB HDD; its interface and form factor became an industry standard.

- 1981: Shipped the ST-412 (10 MB), which helped secure major PC OEM supply positions in the early 1980s.

- 1983: Emerged as a leading independent HDD supplier as HDDs began appearing broadly in PCs such as the IBM XT.

- 1989: Acquired Imprimis Technology (Control Data’s HDD business) in a deal valued around USD 450 million, expanding head-technology capabilities and share.

- 1992: Introduced Barracuda, the first 7,200 RPM HDD; an inflection in performance for mainstream 3.5-inch drives.

- 1995: Announced a merger agreement to acquire Conner Peripherals in a roughly USD 1 billion stock deal.

- 1996: Completed the Conner Peripherals acquisition, creating the world’s largest independent disk-drive maker.

- 1998: Leadership change; founder Al Shugart exited the CEO role and Stephen Luczo became chief executive amid industry pricing pressure.

- 2000: Undertook a complex take-private transaction led by Silver Lake and partners in a deal valued near USD 20 billion, separating the Veritas stake from the drive operations.

- 2002: Returned to public markets; initial public offering priced at USD 12 per share on December 10.

- 2006: Completed the acquisition of Maxtor; integration accelerated portfolio scale and channel reach.

- 2006: Commercialized key recording advances including perpendicular magnetic recording in mobile drives, reinforcing areal-density leadership.

Seagate Investors - 2010: Changed legal domicile from the Cayman Islands to Ireland; the move became effective on July 3, 2010.

- 2011: Global HDD supply chain disruption occurred due to the Thailand floods, causing 20–40% price spikes and constraining output across the sector.

- 2011: Samsung HDD business acquisition announced in April and completed in December; Samsung received an equity stake in Seagate.

- 2012: Reached the one terabit per square inch areal-density milestone in a public technology demonstration; also acquired a controlling interest in LaCie.

- 2014: Continued integration of LaCie within Seagate’s premium external-storage portfolio.

- 2016–2017: Implemented cost-reduction initiatives, including workforce reductions and factory consolidation, to align capacity with demand.

- 2022: Announced additional restructuring, with ~3,000 job cuts, to address demand softness and inventory adjustments.

- 2024–2025: Advanced HAMR road map; prepared high-capacity drives (up to 32 TB) on the Mozaic 3+ platform for cloud and AI storage workloads.

Fun Facts About Seagate

- Seagate was founded in 1979 by Alan Shugart, Tom Mitchell, Doug Mahon, Finis Conner, and Syed Iftikar in California. The firm began life as “Shugart Technology” before adopting the Seagate name.

- The first product, the ST-506 hard drive introduced in 1980, set the 5.25-inch HDD form factor that became a PC standard.

- The company is legally domiciled in Dublin, Ireland, with operational headquarters in Fremont, California.

- Seagate’s popular Barracuda drive line debuted in the early 1990s and has remained a mainstream desktop HDD family for decades.

- In 2000, Seagate executed what was then one of the largest tech buyouts, taking the company private in a complex $20 billion transaction tied to its stake in Veritas.

- Seagate returned to public markets in December 2002 at $12 per share in its IPO.

- The acquisition of Maxtor was completed in 2006, consolidating two major hard drive makers.

- In 2011, Seagate acquired Samsung’s HDD business in a deal valued at about $1.4 billion.

- Cumulative shipments surpassed 3 zettabytes of HDD capacity by 2021, and between 2015 and 2024, Seagate reports shipping 4 zettabytes of storage.

- Seagate brought HAMR technology to mass availability in 2025 with 30 TB Exos and IronWolf Pro drives, marking a major capacity step for data centers and NAS.

- As of 2025, Seagate’s global workforce comprises approximately 30,000 employees.

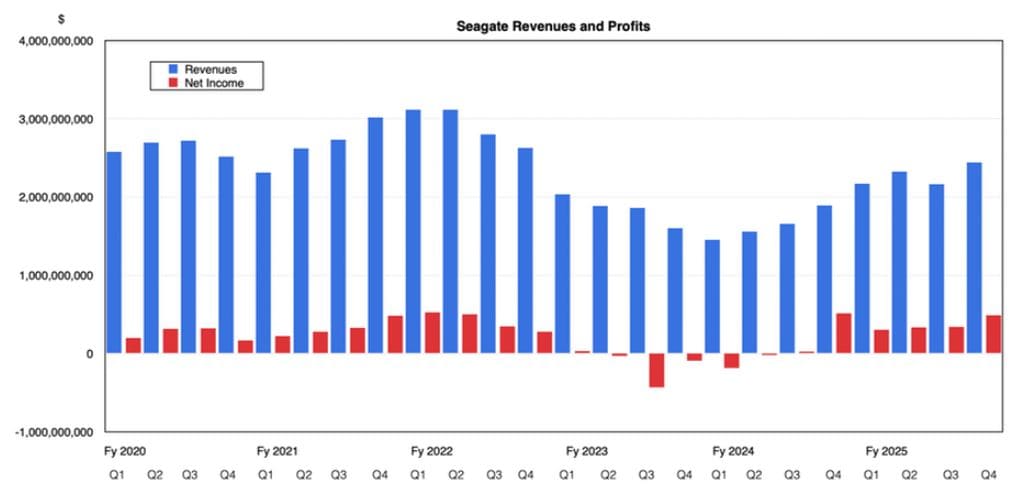

Seagate Revenue And Profits

(Source: blocksandfiles.com)

- Seagate had a very strong recovery in fiscal year 2025. The company’s total revenue for the year was USD 9.1 billion, representing a nearly 39% increase from the previous year’s revenue.

- The net profit was more than five times higher, as the company reaped USD 1.47 billion in profits, a stark contrast to the previous year’s USD 335 million.

- Seagate had an excellent fiscal year close (ending on June 27, 2025) as the last quarter saw its earnings jump approximately 30% over the prior year’s quarter, with quarterly revenues reaching USD 2.44 billion.

- Nevertheless, net profits decreased slightly—by 4.9% to USD 488 million—even though sales were up.

- Such a small decline may indicate that higher costs, product transition expenses, and other short-term factors might have slightly affected margins amidst the strong overall growth.

Seagate GAAP And Non-GAAP Financial Overview

(Source: blocksandfiles.com)

- According to the data, Seagate experienced a significant financial recovery in fiscal year 2025, as it was able to regain some of the lost revenue from the previous years, 2024 and 2023.

- Total revenue increased by approximately 39%, demonstrating a clear sales recovery. The company also managed to improve its profitability across all key measures significantly.

- Under GAAP accounting, by much more profit on each dollar gained in sales, Seagate’s gross margin — the percentage of revenue left after production costs — soared from 23.4% to 35.2%.

- It reached 6.9% and then 20.8% in operating margin, indicating that cost control and operational efficiency had improved significantly.

- The net income, which is the company’s bottom-line profit, grew by more than four times, from USD 335 million in 2024 to USD 1.47 billion in 2025.

- Shareholders were therefore rewarded with a significant increase in earnings per share (EPS), which rose from USD 1.58 to USD 6.77.

- The financial performance on a non-GAAP basis — which eliminates particular one-off expenses or accounting adjustments — is even stronger.

- The gross margin improved from 25.5% to 35.8%, and the operating margin rose from 10.3% to 23.4%, both indicating very robust gains in profitability.

- The net income increased from USD 272 million to USD 1.73 billion, and concurrently, the non-GAAP EPS skyrocketed from USD 1.29 to USD 8.10, confirming a dramatic improvement in Seagate’s overall performance.

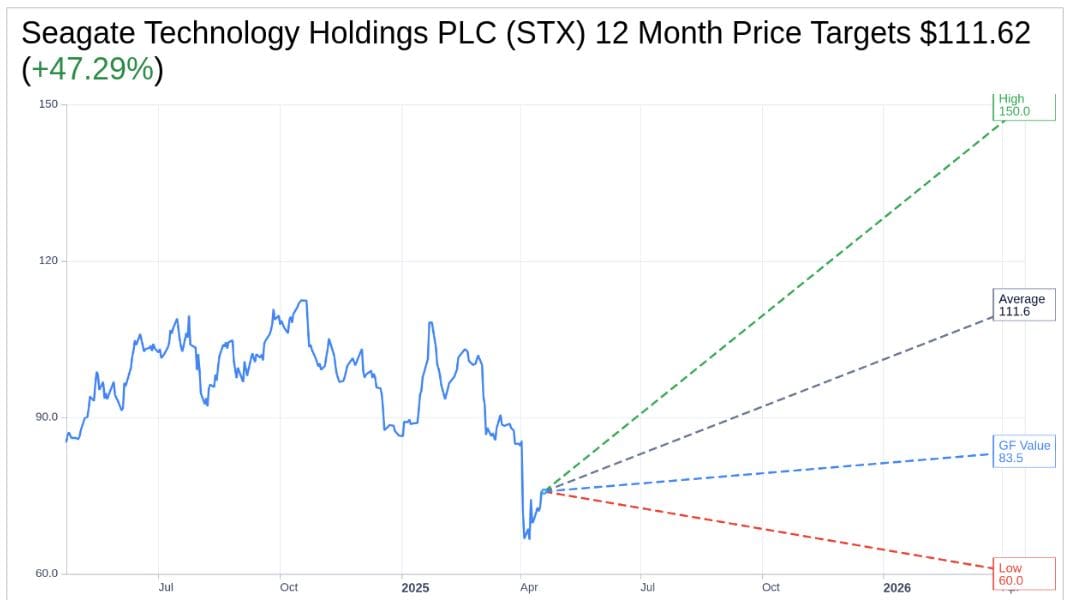

Seagate Price Targets

(Source: gurufocus.com)

- Financial experts remain optimistic about Seagate’s stock performance in the coming year.

- The average price target for Seagate’s stock over the next year is USD 111.62, based on reports from as many as 19 analysts, with the most optimistic forecast at USD 150.00 and the most pessimistic at USD 60.00.

- As Seagate’s stock price was around USD 75.78, the upside targets imply an average hike of about 47% if the consensus forecast unfolds.

- If one considers the broadest brokerage suggestions, 24 companies give Seagate a composite score of 2.2, where 1 is equivalent to “Strong Buy” and 5 is equivalent to “Sell.”

- A rating close to 2 indicates that analysts expect the firm to outperform the market, meaning its stock is likely to rise at a rate higher than the overall market average.

- Another viewpoint comes from GuruFocus, a research tool that determines a company’s “fair value.” It rates Seagate’s GF Value at USD 83.50, based on factors such as historical earnings, trading, and future performance expectations.

- Compared to the current stock price of USD 75.78, this implies a minor but still positive upside of 10.19%.

- In short, the majority of specialists consider Seagate as a safe bet in 2025 with an increasing share price — some predicting large gains while others consider it to be modest.

- The blockbuster theme is that the investors’ trust in Seagate’s future growth remains high.

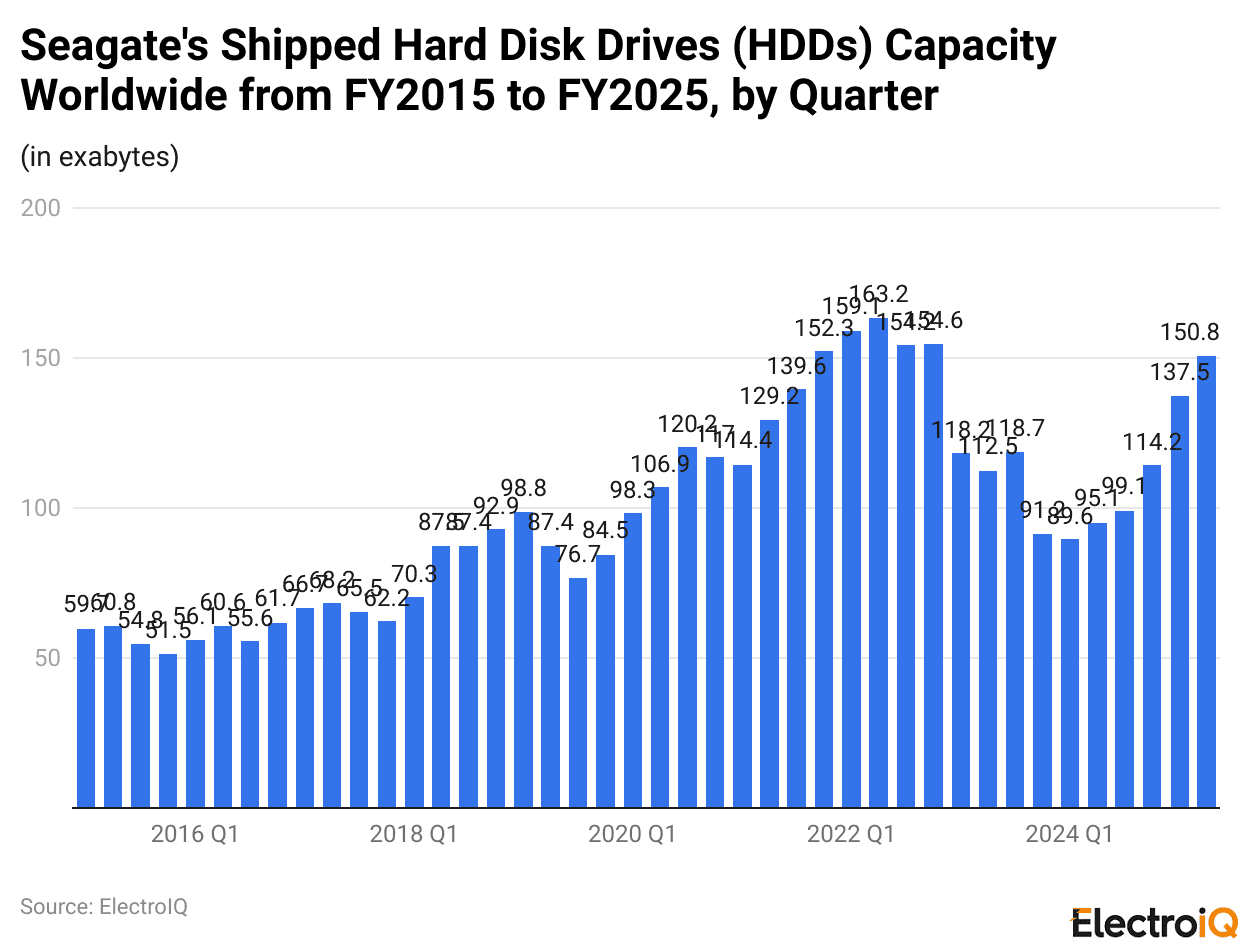

Seagate Shipping

(Source: blocksandfiles.com)

- In the second quarter of Seagate’s fiscal year 2025, the company sold approximately 150.8 exabytes of hard disk drive (HDD) storage to global markets.

- The current quarter is reported to have a total shipment of 13.3 exabytes, exceeding the previous quarter, thus demonstrating healthy quarter-to-quarter growth.

- The current quarter also has a total of 55.7 exabytes more than Seagate shipped in the same quarter of 2024, which is a strong indicator of a year-over-year increase in the storage capacity delivered.

- Seagate was able to sell and deliver significantly more data storage in early 2025 than ever before, which reflects not only increasing customer demand but also the company’s ability to scale up production, most likely supported by its new high-capacity HAMR drives.

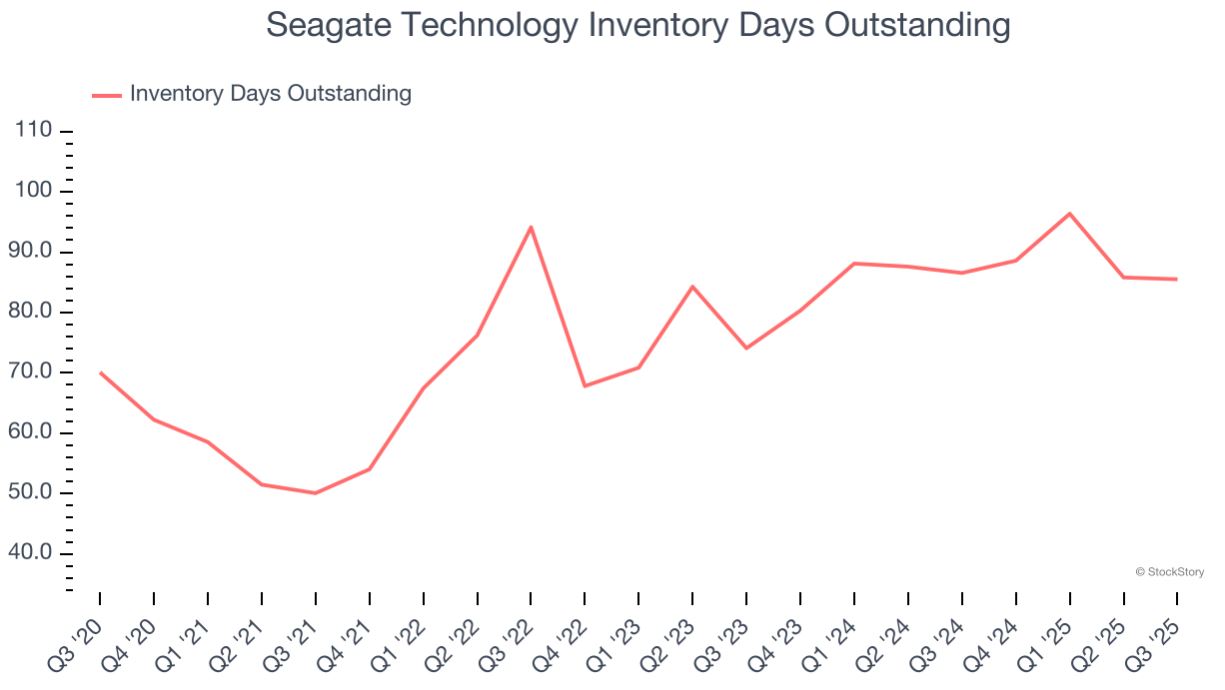

Seagate Inventory

(Source: theglobeandmail.com)

- Seagate’s recent stock data reveals an essential aspect of the company’s operational equilibrium between output and consumption.

- The Days Inventory Outstanding (DIO) — the metric used to calculate the period for which a product remains in the warehouse before it is sold — was recorded at 86 days this quarter.

- This number is almost 10 days longer than Seagate’s five-year average, indicating that the current stock level is slightly above the company’s historical mark.

- In the semiconductor and data storage industry, a high DIO can mean different things. If the demand for a product is very high and the supply is low, the inventory level would either remain stable or even decline, giving companies more power in terms of pricing.

- On the other hand, if the DIO increases, it may imply that the products are taking longer to move out of the warehouses or that sales are slow, and therefore, the stock remains unsold.

- For Seagate, the extension to 86 days is not yet a significant problem, but rather a warning sign. It may imply that, after strong growth, demand is now stabilising, or that the faster production took sales by surprise while awaiting future orders.

- If inventory levels continue to rise in the next few quarters, Seagate may have no option but to reduce production to align with actual market demand.

- Thus, the company’s high DIO emphasizes the fragile interaction between supply, demand, and production planning in the cyclical data storage industry.

Seagate Employees Demographics Statistics

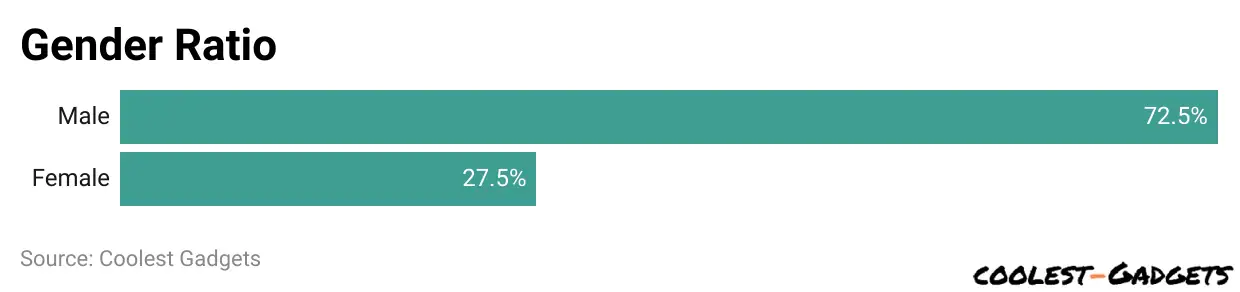

- Seagate Technology employs approximately 40,000 people worldwide, comprising a large and diverse workforce.

- Around 28% of employees are women, while 72% are men, showing a higher male representation within the organization.

- In terms of ethnicity, 53.2% of Seagate’s employees are White, making it the largest group in the company. 19.8% identify as Asian, 14.8% as Hispanic or Latino, 6.5% as African or Black American, and 5.6% fall under the category of unknown ethnicity.

| White | 53.2% |

| Asian | 19.8% |

| Hispanic or Latino | 14.8% |

| African or Black Americans | 6.5% |

| Unknown | 5.6% |

- The average annual salary of a Seagate employee is USD 101,694, reflecting competitive compensation within the technology sector.

- Most Seagate employees tend to support the Democratic Party, according to internal demographic insights.

- On average, employees stay with Seagate for about 6.6 years, suggesting strong employee retention and satisfaction.

- Seagate’s workforce is linguistically diverse, with several languages spoken across its offices worldwide. The most common foreign language is Spanish, spoken by 26.1% of employees.

- Other languages spoken include Chinese (10.9%), French (10.1%), Mandarin (9.4%), Portuguese (8.0%), Hindi (4.3%), German (4.3%), Cantonese (3.6%), and Japanese (3.6%).

- Smaller groups of employees also speak Carrier (2.9%), Vietnamese (2.2%), Thai (2.2%), Italian (2.2%), Dutch (1.4%), Hmong (1.4%), Malay (1.4%), Tagalog (1.4%), Hebrew (1.4%), Dakota (1.4%), and Arabic (1.4%).

| Language | Percentage |

| Arabic | 1.4% |

| Dakota | 1.4% |

| Hebrew | 1.4% |

| Tagalog | 1.4% |

| Malay | 1.4% |

| Hmong | 1.4% |

| Dutch | 1.4% |

| Italian | 2.2% |

| Thai | 2.2% |

| Vietnamese | 2.2% |

| Carrier | 2.9% |

| Japanese | 3.6% |

| Cantonese | 3.6% |

| German | 4.3% |

| Hindi | 4.3% |

| Portuguese | 8.0% |

| Mandarin | 9.4% |

| French | 10.1% |

| Chinese | 10.9% |

| Spanish | 26.1% |

STX’s Margin Details

- Seagate’s latest results showed remarkable growth in margins. The non-GAAP gross margin of the company reached an all-time high of 40.1%, representing an approximate 220 basis points (bps) increase compared to the previous quarter and 680 bps more than the same period last year.

- The major factor behind this strong development was the increase in demand for Seagate’s high-capacity nearline hard drives, combined with the company’s consistent pricing strategy.

- Non-GAAP operating expenses were USD 291 million, representing a 2% quarter-on-quarter increase and a 3.5% year-on-year decrease, remaining within the company’s forecast range.

- The small rise is a sign that the firm has been able to keep costs down even as sales volumes have increased.

- Non-GAAP income from operations was $763 million, representing a significant increase from $442 million one year ago.

- Consequently, the non-GAAP operating margin expanded by 860 basis points year-over-year to 29%, while adjusted EBITDA reached USD 831 million, reflecting strong operational robustness and profitability.

STX’s Balance Sheet And Cash Flow

- Seagate’s finances remained stable, with a stronger cash position and reduced debt.

- The corporation’s cash and cash equivalents as of October 3, 2025, were USD 1.1 billion, an increase from USD 891 million at the end of June 2025.

- The company’s long-term debt (including the current portion) was USD 4.9 billion, a slight improvement from USD 5.0 billion previously, indicating disciplined debt management.

- The cash flow from operations was USD 532 million, an increase from USD 508 million in the previous quarter, and it is an indicator of the company’s ability to generate cash through its regular activities.

- The cash flow from operations was USD 427 million, which is the same as in the last quarter. However, Seagate anticipates an increase in the next quarter (December), when revenues are also expected to rise.

- The corporation still distributed a portion of its cash flow to the stockholders. It distributed USD 153 million in dividends and repurchased 153,000 shares at an average price of USD 187 per share, totalling USD 29 million.

- Seagate reaffirmed its commitment to return at least 75% of its free cash flow to stakeholders in the form of dividends and share repurchases over the long term.

STX’s Strong Fiscal Q2 Business Outlook

- Management of Seagate anticipates that the demand will not only be good but that the data centre storage of the cloud will be the major area, as these data centers expand the volumes of storage.

- Furthermore, the company predicts significant increases in its revenue, as well as the margin of its next-gen high-capacity storage solutions, following their adoption by customers.

- Revenues of approximately USD 2.7 billion, plus or minus USD 100 million, are projected by Seagate for the fiscal second quarter.

- The non-GAAP earnings per share (EPS) are anticipated to be around USD 2.75, with a possible range of ± USD 0.20. The company expects non-GAAP operating expenses of around USD 290 million.

- Seagate, at the midpoint of its guidance, foresees a non-GAAP operating margin of around 30%, thus reinforcing the idea of continued profitability growth alongside rising demand for new products.

Recent Performance Of Competitors

International Business Machines Corporation (IBM)

- IBM delivered remarkable results for the third quarter of 2025, with both the company’s adjusted earnings and revenue exceeding analyst estimates.

- The non-GAAP net income, excluding one-off effects, from continuing operations was USD 2.65 per share, which was USD 0.21 above the Zacks Consensus Estimate, up from USD 2.30 in the same quarter of the previous year, and above the Zacks Consensus Estimate by USD 0.21.

- The total revenue for the quarter increased from USD 14.97 billion to USD 16.33 billion due to high demand for hybrid cloud and AI solutions, primarily benefiting the Software segment.

- In constant currency terms, revenue increased by 7% year-over-year, and total revenue exceeded the consensus estimate of USD 16.1 billion.

Cadence Design Systems (CDNS)

- The third quarter of 2025 proved to be stellar for Cadence, as the company reported non-GAAP EPS of USD 1.93, surpassing the Zacks Consensus Estimate by 7.8%.

- This was a year-on-year rise of 17.7%, and certainly above the management’s guidance, which was in the range of USD 1.75 to USD 1.81.

- The company’s revenue was USD 1.339 billion, which exceeded not only the consensus estimate (by 0.9%) but also the guided range of USD 1.305 billion to USD 1.335 billion.

- Revenue increased 10.2% year over year, driven by strong and broad-based demand, primarily for Cadence’s AI-driven design solutions, resulting from the high design activity across the semiconductor industry.

Synopsys (SNPS)

- The business announced a non-GAAP profit of USD 3.39 per share, which is less than the Zacks Consensus Estimate of USD 3.84 and the company’s own guided range of USD 3.82-USD 3.87.

- It represents a 1.2% decline over the year for the same quarter. However, at the same time, the company had an earnings miss;s, its revenues were up by 14% every year to USD 1.74 billion, which was just a little short of the consensus estimate of USD 1.768 billion.

- The primary reason for the growth in sales was the increase in sales in the company’s Time-Based and Upfront Product segments; however, the lower-than-expected earnings indicated that the company’s margins were squeezed during the quarter.

Risk And Concern

- The near-term stock performance of Seagate is likely to be influenced by several major risks, despite the company’s overall profitability remaining quite strong.

- The first risk is related to the company’s gross profit margin, which is still below the market average but remains healthy. The arrival of the margins will gradually erode investor confidence, and the company may be forced to trade at a price lower than its market competitors due to this.

- Another source of risk for the company is its full dependence on the hard disk drive (HDD) market, which is a structural risk. HDDs are still the backbone of major data center cloud storage systems, but the rapid progress in flash-based storage technology and its decrease in cost is a long-term challenge.

- The competition between companies like Micron is intensifying as they invest heavily in flash and solid-state drive (SSD) technologies.

- A quick drop in price for flash, initiated by the suppliers, would eventually lead to a decline in demand for HDDs, thus taking away a portion of Seagate’s market.

- Seagate has a small stake in the flash and SSD segment, but this is just a fraction of its main HDD business.

- Another critical issue is the technology execution risk associated with the company’s HAMR (Heat Assisted Magnetic Recording) product launch.

- HAMR is considered the future of Seagate’s storage technology; however, the entire process of scaling up production and achieving widespread use involves intricate engineering and manufacturing challenges.

- Any postponed or interrupted changeover in this case, whether in scaling, customer qualification, or manufacturing yield, might not only result in the market losing interest but also cause the company’s growth expectations to be lowered.

- In terms of finance, Seagate is a company with a moderate level of debt, as its total debt obligations amount to approximately USD 5 billion, which is significantly higher than its cash reserves of around USD 891 million.

- The company’s stock, however, remains fundamentally undervalued in spite of these risks.

- Quite opposite, if Seagate is good at keeping up with its HAMR roadmap, having stable margins, and at the same time, the cloud storage demand is still there, then the upside potential could be greater than the current risk count.

- In this case, investors could collect remarkable returns; thus, it can be said that even if caution is a must, the stock presents an attractive long-term opportunity, should these challenges be managed properly.

Conclusion

Seagate Statistics: Seagate made an extraordinary comeback in the financial and operational sectors in 2025, with a record shipment of HDDs, remarkable revenue increase, and growing profit margins as main factors. The annual revenue of Seagate reached USD 9.1 billion, and the company’s net profit was USD 1.47 billion, representing a 339% increase compared to the previous year.

There was a clear link between the company and the growing demand for cloud and artificial intelligence storage. However, challenges such as high debt, inventory buildup, and competition from SSD manufacturers still persist. All in all, Seagate finishes the year 2026 in a robust position, that is, profitable, innovative, and capable of fulfilling the ever-increasing global demand for data storage.

Sources

FAQ.

Seagate reported US$9.1 billion in revenue for fiscal 2025, which is a 39% increase over the previous year when the revenue was US$6.55 billion. The significant growth was primarily contributed by the sales of the new HAMR (Heat-Assisted Magnetic Recording) drives that were utilized in the cloud storage and AI-related workloads, where the demand was boosted. It is a strong rebound following two years of declining revenue.

The net profit of Seagate increased to US$1.47 billion, which is more than a 339% increase compared to the previous year’s US$335 million. The company’s gross margin under GAAP rose from 23.4% to 35.2%, and its operating margin improved from 6.9% to 20.8%. On a non-GAAP basis, the operating margin was 23.4%, which underlines the efficient cost control and operational efficiency.

In the second quarter of the fiscal year 2025, Seagate had shipped about 150.8 exabytes of hard drive storage globally— an increase of 13.3 exabytes compared to the previous quarter and 55.7 exabytes compared to the same quarter of 2024. This increase is a clear indication of worldwide demand for Seagate’s high-capacity HDDs, primarily from large-scale data center and cloud service providers.

GuruFocus (2025) states that the average one-year price target for Seagate’s share is US$111.62, which includes a high estimate of US$150 and a low estimate of US$60. Since around US$75.78 was the share price of Seagate, this implies a 47% upside potential. Most analysts classify Seagate as “Outperform,” indicating that they have a strong belief in the company’s future growth.

Seagate has a number of major risks to face: reliance on the HDD market, competition with flash and SSD, and difficulties associated with the upscaling of its new HAMR technology. Similarly, a perfect US$5 billion debt would not be a big deal during a low-interest-rate environment compared to being about 5 times its cash reserves.

Maitrayee Dey has a background in Electrical Engineering and has worked in various technical roles before transitioning to writing. Specializing in technology and Artificial Intelligence, she has served as an Academic Research Analyst and Freelance Writer, particularly focusing on education and healthcare in Australia. Maitrayee's lifelong passions for writing and painting led her to pursue a full-time writing career. She is also the creator of a cooking YouTube channel, where she shares her culinary adventures. At Smartphone Thoughts, Maitrayee brings her expertise in technology to provide in-depth smartphone reviews and app-related statistics, making complex topics easy to understand for all readers.