ATM Withdrawal Frequency and Cash Usage Statistics and Facts (2026)

Updated · Jan 14, 2026

Table of Contents

- Introduction

- Editor’s Choice

- ATM Cash Withdrawal Market

- ATM Transaction Volume Statistics

- ATM Transaction Value Statistics

- ATM Withdrawal Frequency And Ticket Size

- ATM Adoption Rates And Decline Trends

- Annual ATM Cash Withdrawal Value In The EU-27 2000-2024, In Euros And By Country

- Indian ATMs Statistics By Daily Withdrawal Limits, 2025

- The Impact of Digital Payment Systems On ATM Usage

- Conclusion

Introduction

ATM Withdrawal Frequency and Cash Usage Statistics: Smartphones do everything from buying groceries to making government payments, which leads to the assumption of cash disappearance. However, in 2025, in the millions, daily ATM withdrawals continue to occur worldwide, with physical currency remaining the primary means of payment for shoppers in the developing world.

This article offers a comprehensive overview of ATM Withdrawal Frequency and Cash Usage Statistics, trends, and economic factors that illuminate the current situation and the next destination of cash.

Editor’s Choice

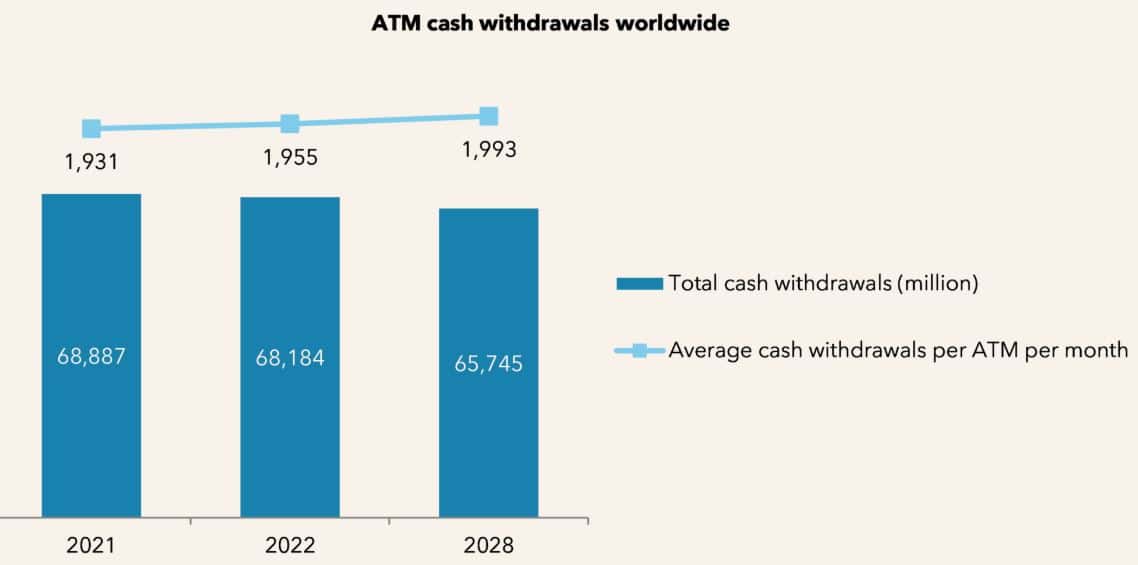

- Global ATM cash withdrawal volumes have declined slowly but steadily, from 68,887 million transactions in 2021 to an estimated 65,745 million by 2028.

- Average ATM withdrawals will increase from 1,931 per month in 2021 to 1,993 by 2028, indicating fewer, more heavily used ATMs.

- Consumers are visiting ATMs less frequently but withdrawing larger amounts each time, which has become an indicator of ATM network consolidation and greater efficiency.

- In India, the number of debit card ATM withdrawals per month remains approximately 490 million in 2025, despite the rapid growth of UPI and other digital payments.

- The average cash dispensed per ATM in India increased from ₹1.02 crore in FY2017 to ₹1.30 crore in FY2025, indicating that ATMs are being used more frequently.

- The total value of ATM cash withdrawals in India increased from ₹28.9 lakh crore in FY2020 to ₹30.6 lakh crore in FY2025, indicating steady demand for cash.

- Germany led Europe with the highest ATM withdrawals of €384 billion in 2023, reflecting the country’s strong cultural preference for cash.

- Digital payment systems led to a 5.7% reduction in ATM usage in 2025 in leading economies such as the US, the UK, and Germany.

- Peer-to-peer platforms like Venmo and Zelle reduced ATM visits among Gen Z by 22%, replacing routine cash withdrawals with instant transfers.

- Contactless payments led to a 10.8% decline in cash withdrawals across developed countries in 2025.

- QR code-based payments increased by 19.5% globally, particularly in urban areas, further reducing reliance on ATMs.

ATM Cash Withdrawal Market

(Source: datos-insights.com)

- In 2021, there were 68,887 million transactions, indicating a strong reliance on ATMs for cash access.

- In 2022, the number of transactions declined slightly to 68,184 million, indicating that digital payment methods were gaining popularity.

- By 2028, the projected total withdrawals are 65,745 million, indicating a steady decline in ATM cash withdrawals at the aggregate level.

- On the other hand, the average monthly cash withdrawal per ATM shows a different picture altogether. In 2021, ATMs processed 1,931 withdrawals per user per month.

- Despite a reduction in total transactions, the number of withdrawals per month increased to 1,955 in 2022.

- Moreover, the average is projected to further increase to 1,993 withdrawals by the end of 2028.

ATM Transaction Volume Statistics

- ATM use in India has not changed significantly, indicating that cash remains the preferred payment method among customers who are not comfortable with digital payment systems.

- In March 2025, there were approximately 488 million withdrawals made through debit cards at ATMs, which is a slight decrease from the 492 million in February.

- ATM transactions average approximately 490 million per month, reflecting consistent and strong demand.

- According to data from CMS Info Systems, the average cash dispensed by ATMs increased substantially from ₹1.02 crore in FY2017 to ₹1.30 crore in FY2025.

- The total amount of cash withdrawn through ATMs nationwide during FY2020 was ₹28.9 lakh crore, which increased marginally to ₹30.6 lakh crore during FY2025.

- Among others, Bihar, Delhi, Uttar Pradesh, and Himachal Pradesh reported increases in ATM usage of up to 8%, thereby confirming that ATMs remain the most reliable means of obtaining small cash for everyday needs.

ATM Transaction Value Statistics

- In monetary terms, ATM cash withdrawals totalled ₹30.6 lakh crore in FY2025, a significant increase from ₹28.9 lakh crore in FY2020.

- The consistent upward trend in the average cash-out per ATM to ₹1.30 crore indicates increasing reliance on that machine.

- Notably, both the number and the value of transactions indicate a gradual yet pronounced dependence on cash, rather than a sudden decline.

ATM Withdrawal Frequency And Ticket Size

- It was reported that in March 2025, 490 million debit card transactions were processed at ATMs, indicating that ATM visits remain frequent despite the increasing use of UPI.

- The majority of customers appear to use ATMs occasionally rather than making daily visits, particularly in areas with limited access to digital channels.

- The increase in per-ATM disbursements likely indicates either fewer withdrawals but larger amounts, or more visits with smaller ticket sizes. At the state level, it indicates a shift in cash reliance in certain areas.

ATM Adoption Rates And Decline Trends

- While the demand for cash remains strong, the number of ATMs in India continues to decline.

- The overall ATM count decreased by approximately 4,000 to about 215,000 in 2024, from 219,000 in the previous year. By the end of September 2024, the number of ATMs was 255,078, indicating a slightly more than 1% annual decline.

- The countryside experienced the largest decline, at 2.2%, followed by the metropolitan regions, at 1.6%.

- Although there are fewer machines, the higher cash dispensed per ATM indicates greater use of the existing infrastructure.

- This trend is indicative of the fact that banks are shifting resources from expanding ATM networks to branch optimization and digital-first strategies.

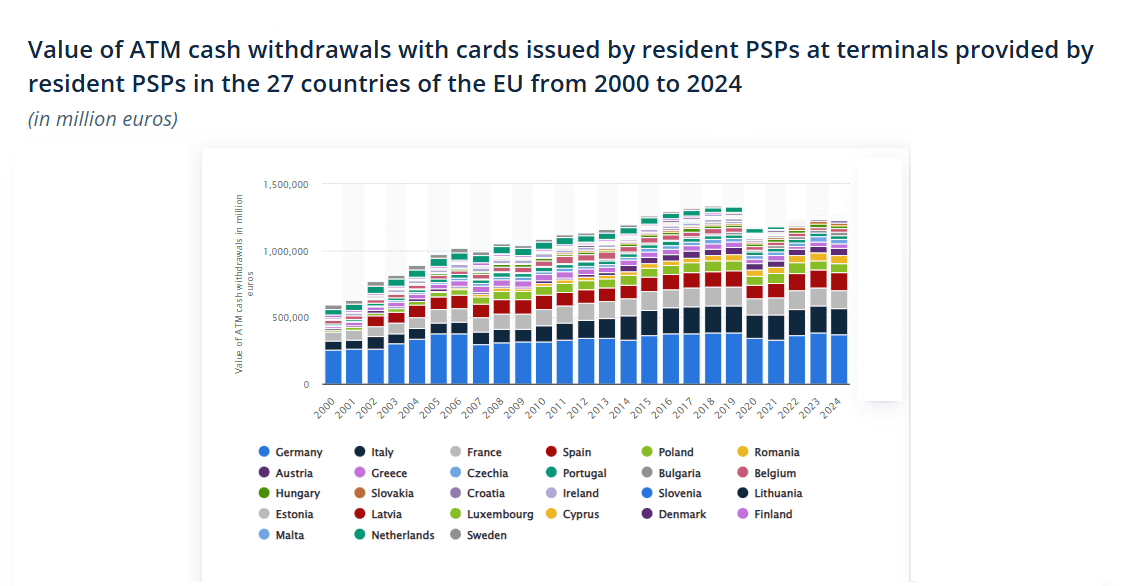

Annual ATM Cash Withdrawal Value In The EU-27 2000-2024, In Euros And By Country

(Source: statista.com)

- Cash withdrawal amounts via ATMs across Europe vary substantially from one country to another.

- This is a consequence of differences in population size, consumer payment habits, and cash reliance.

- The statistics relate exclusively to ATM withdrawals made at machines operated by local payment service providers (PSPs), with cards also issued by local PSPs, and exclude e-money transactions to ensure the figures represent traditional cash usage only.

- In this scenario, Germany is the most significant market. The total value of cash withdrawn at ATMs in Germany in 2023 using domestically issued cards reached €384 billion, the highest among European countries.

- This indicates that Germany remains oriented toward cash for daily transactions, even as digital and card-based payments are increasing in popularity in the region.

- The number not only reflects Germany’s large consumer base but also its cultural preference for cash, making it a key driver of Europe’s overall ATM withdrawal volume.

Indian ATMs Statistics By Daily Withdrawal Limits, 2025

- The Indian ATM ecosystem is a hybrid of digital payments and cash access, with the transition to digital payments progressing rapidly, yet cash remains important.

- To ensure that customers from all walks of life can use banking services, Indian banks have established various daily withdrawal limits based on card type, customer segment, and account status.

- For instance, State Bank of India, a public-sector bank, offers debit card limits ranging from ₹40,000 for standard cards to ₹100,000 for platinum international cards, thereby making the service accessible to all and providing premium users with higher limits.

- Private-sector banks, such as HDFC, ICICI, and Axis Bank, offer much higher credit limits to their best customers, with some high-end cards allowing users to withdraw up to ₹300,000 per day, thereby catering to wealthy and business customers.

- Cards in the mid-tier category across different banks typically permit cash withdrawals of between ₹50,000 and ₹150,000 per day; however, basic and classic cards limit daily withdrawals to ₹10,000-₹25,000.

- This is to ensure that cash consumption is controlled and that an appropriate risk management system is in place.

- Specialized cards like junior accounts or entry-level digital banking products offer very low limits of cash withdrawal, sometimes even as low as ₹2,500 to ₹5,000 per day, in order to motivate users to be responsible and safe.

The Impact of Digital Payment Systems On ATM Usage

- The data indicates a global trend in the way consumers access and use their money, which is caused mainly by the quick adoption of digital payment systems.

- In 2025, all the economies which are biggest and most important economies, like the US, UK, and Germany, saw a decrease of 5.7% in ATM usage as people switched to mobile wallets, contactless cards, and peer-to-peer payment platforms, which altogether replaced cash for everyday transactions more and more.

- In 2025, the use of Venmo and Zelle among Gen Z caused a cutting down of ATM transactions by 22% as the conventional small withdrawals were replaced by quick digital transfers.

- The same thing happened with the use of contactless payments through Apple Pay everywhere, which was one of the contributing factors for the 10.8% decline in cash withdrawals in developed countries, thus lessening the need for carrying cash.

- One more thing that has a role in the elimination of cash is the coming of QR code-based payments, which saw a 19.5% increase in usage worldwide in 2025.

- Some nations signify the farthest point of this trend. For instance, in Sweden, the utilization of ATMs has gone down by 82% in the last ten years, and it is predicted that by 2025, cashless transactions will account for 99% of the total, thus making ATMs and cash of little importance.

- On the level of policy-making, the increase in the number of countries, which the central bank digital currency (CBDC) projects, has been made from 10 to 18 in 2025 which is thereby speeding up the gradual extinction of physical cash and traditional ATM networks.

- In Africa, cash is still used for over 89% of consumer transactions in 2025 due to the lack of digital infrastructure and financial inclusion.

- In these areas, ATMs are necessary for community economic activity, salary withdrawals, and ordinary business transactions, thereby confirming a global divide where the use of digital payments exists alongside the dependence on cash.

Conclusion

ATM Withdrawal Frequency and Cash Usage Statistics: The trends related to ATM withdrawals for the year 2025 signify a financial ecosystem that is undergoing a change instead of a decline. Even if digital payments still cut down on the number of cash withdrawals, cash is still a big part of the daily financial transactions in various regions. The statistics point towards a decline in the number of ATM visits but an increase in the usage per machine.

This change is due to the consolidation of networks and also larger withdrawals being made. While India and certain areas of Europe show their continuing reliance on cash, the developed economies are moving faster towards the cashless system. In total, ATMs still take the center stage as the major players in the process of financial inclusion, though they are at the same time linking the digital innovation with the continued but practical need for physical currency.

Sources

FAQ.

The use of cash is going down very slowly in terms of the frequency of withdrawal, but it is not going to be completely wiped out. The number of ATM transactions worldwide is expected to drop from 68,887 million in 2021 to 65,745 million by 2028. The increases per ATM in cash withdrawal amounts indicate that customers are withdrawing cash less frequently but in more considerable sums, thereby causing a shift in the withdrawal pattern.

It is due to the fact that banks are cutting down on the number of ATMs with low transactions, while at the same time setting up new ones in areas of high foot traffic. Consequently, the number of ATMs has gone down, but each is doing more transactions than before, and in turn, users make fewer visits but withdraw larger sums, hence raising the average amount withdrawn per ATM.

Regardless of the growing presence of UPI in the country, ATMs are still very much a part of India, with around 490 million debit card withdrawals each month in 2025. The total ATM withdrawal value in FY2025 reached ₹30.6 lakh crore, thus showing that cash is still an important player along with digital payments.

Germany is at the forefront of Europe regarding cash withdrawals from ATMs, with a total of €384 billion withdrawn in 2023. This large amount is an indication of the strong consumer preference for cash in Germany, which therefore also becomes the EU’s largest contributor to ATM withdrawal value.

Digital wallets, contactless payments, and peer-to-peer platforms have led to a decrease of 5.7% in ATM usage in the major economies by 2025. Among the younger generation, the Gen Z users are the least dependent on ATMs, whereas in some regions like Africa, cash is still king, hence the need for ATMs.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.