Digital Wallet Fraud Statistics And Facts (2025)

Updated · May 12, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Global Digital Payment Fraud

- Regional Analysis of Fraud Incidents

- Digital Wallets and Crypto Are Most Targeted Fraud Frontiers For 2025

- Prevalence of Each Type of Payment Fraud

- Business Impacts of Fraud

- With New Technology Comes More Sophisticated Fraud

- Modern Challenges For Financial Institutions

- Mobile Payments Driving The Surge In Digital Fraud

- Real-Time Fraud Monitoring Becomes A Top Priority Across Industries

- Recent Digital Wallet Fraud Developments

- Conclusion

Introduction

Digital Wallet Fraud Statistics: Digital wallets like Apple Pay, Google Wallet, PayPal, Samsung Pay, and dozens of bank or app-based wallets provide customers with a shared bank account from which funds are debited or credited with a single tap on their mobile devices. The convenience factor makes life easy, but at the same time, it’s quicker and cheaper for criminals to commit fraud.

In 2025, fraudsters shift from old tricks (card-skimming, cloned plastic) to sleek attacks that target phones, identity systems, one-time passcodes, and onboarding flows that open new wallet accounts. Below is a crystal-clear, number-packed view of Digital Wallet Fraud Statistics in 2025.

Editor’s Choice

- Circa 75% of worldwide digital payment fraud incidents in 2025 happened on mobile devices.

- Cross-border payment fraud surged 20% on a year-on-year basis, with over US$50 billion in confirmed actual fraud from US$1.5 trillion in flagged transactions.

- Digital wallets and cryptocurrencies are the top targets for fraud, with 48% and 38% of the organizations citing them as being the most vulnerable.

- Credit card fraud remains the most predominant fraud in the world (35%), but synthetic identity fraud has skyrocketed by over 100% in just about two years since 2022.

- By 2025, CNP fraud will be half of all e-commerce fraud.

- Regions worldwide lose different percentages of revenues to e-commerce fraud, from 2.4 to 4.6%, with Latin America at the top of this loss chart.

- Phishing in this case has been made successful by 30% using AI and machine-learning automation, while 7% of social engineering attacks now have deepfake scams behind them.

- Fraudulent transactions with cryptocurrency wallets grew by 25%, QR scam attacks by 51%, and fraud through the Internet of Things makes up 12% of worldwide cases.

- Most fraudulent losses encountered by e-commerce in the United States and Canada are because to mobile payments. Increasingly, QR codes, digital wallets, and P2P apps are being targeted. In response to these escalating threats, b2b fraud prevention strategies have become a critical priority for enterprises aiming to protect digital transactions and reduce exposure to increasingly sophisticated attack vectors.

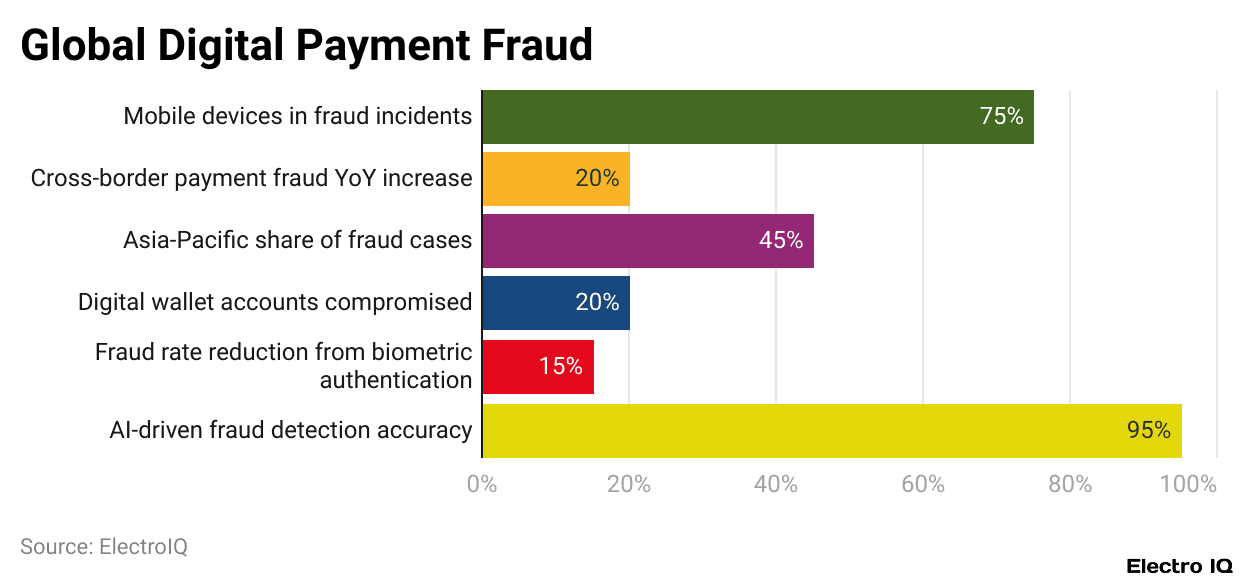

Global Digital Payment Fraud

(Reference: coinlaw.io)

- As per Coin Law, digital wallet fraud statistics show that the global report warned that digital payment frauds increasingly have the mobile element attached nowadays, with almost three-quarters of all incidents considered to be associated with mobile devices.

- Cross-border payment fraud is also seeing a sudden rise, having risen by 20% from the previous year.

- Out of the more than US$1.5 trillion in digital payments worldwide accused of fraud, approximately US$50 billion resurface as actual instances of fraud.

- The Asia-Pacific region continues as the most-fraud-affected one, representing approximately 45% of all cases worldwide.

- About 20% of all digital wallet accounts underwent one form of compromise or another by 2025, sustaining the growing vulnerabilities of mobile and online payment systems.

- However, the further adoption of biometric authentication methods, such as fingerprint or facial recognition-installed a reduction in fraud incidences of about 15% among the users adopting such technologies.

- In tandem with this, AI-powered fraud detection systems are proving themselves to be a force throughout the world, with a near 95% accuracy in identifying suspicious transactions and loss prevention.

Regional Analysis of Fraud Incidents

- Digital payment fraud differs in form, size, and manner from one region to another: In North America, losses exceed US$15 billion, and credit cards remain the most common method assaulting fraudsters use.

- In Europe, phishing is rising 35% amid an increase in contactless and remote payments.

- The Asia-Pacific region is also marked as pathological, taking nearly half-48% of all digital fraud incidents.

- This sharp rise is largely linked to the mass adoption of mobile wallets and the rapid growth of digital payment avenues in the region.

- In Africa, we witness a 28% increase in mobile money fraud, reflecting the growing challenges mobile banking systems face during their expansions.

- Latin America has also been seeing sharp growth, with e-commerce payment frauds going 25% upward alongside the booming online retail market in the region.

- In the Middle East, there has been a 22% rise in cross-border fraudulent transactions, particularly with regard to international trade and financial transfers.

- On the other hand, Australia and New Zealand serve as good examples of disappointment, having reported a 15% drop in fraud losses as a direct result of stronger regulatory frameworks.

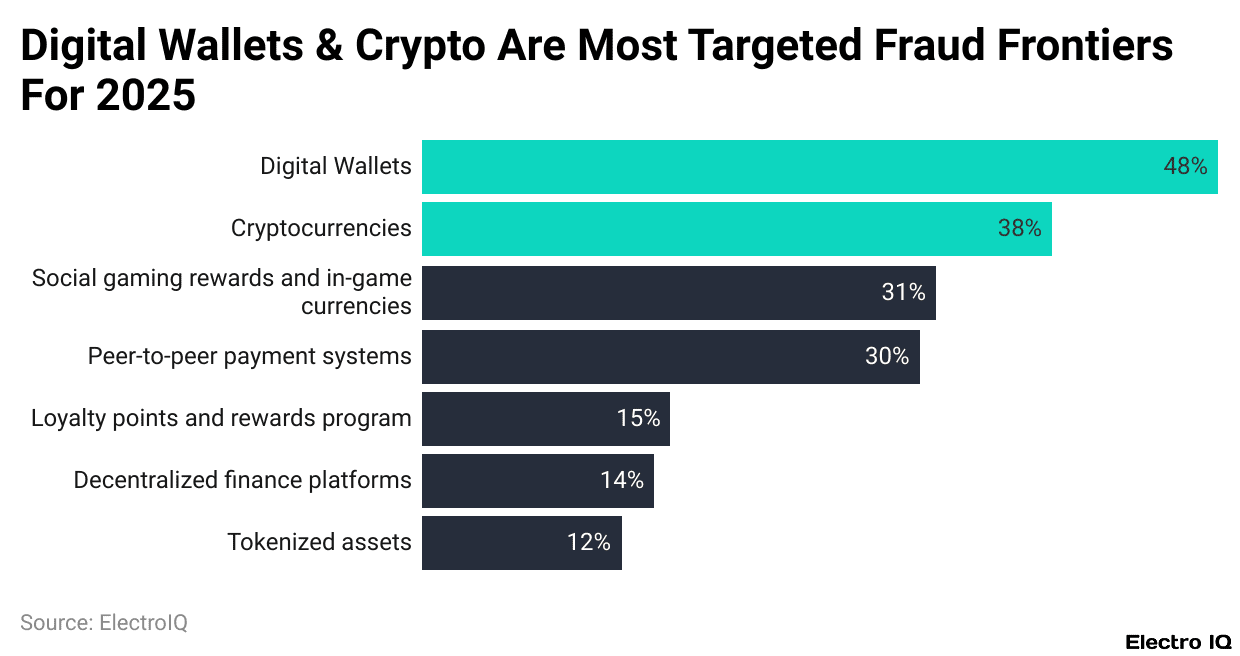

Digital Wallets and Crypto Are Most Targeted Fraud Frontiers For 2025

(Reference: learn.seon.io)

- Throughout 2025, digital wallets and cryptocurrencies have been seen as the greatest points of fraud.

- Nearly half of organisations, about 48%, agreed that digital wallets would possess the greatest vulnerabilities in the coming year.

- This is mainly attributed to the increasing use of mobile-based payments and the sheer volume of sensitive data held within these platforms.

- Next in line were cryptocurrencies, with 38% of respondents viewing them as major fraud risks, probably because of their decentralised nature and the continued difficulty in tracing illicit transactions.

- Other emerging areas of interest include social gaming awards and in-game currency (31%) and peer-to-peer payment systems (30%), both becoming more attractive to fraudsters as online interactions and digital economies grow.

- In contrast, 15% of the respondents cited loyalty points and reward programs as vulnerable, while 14% viewed DeFi platforms as the next potential fraud spots.

- Tokenized assets came in last at 12%, but with growing urgency-as tokenisation gains further traction in digital asset markets.

Prevalence of Each Type of Payment Fraud

- Globally, credit card fraud continues to be the most common, constituting 35% of all fraud cases in 2025.

- With increases of 30%, account takeover (ATO) frauds cause a great sort of problems for online retailers and subscription-based businesses, as, through ATO, fraudsters gain unauthorised access to customer accounts.

- Phishing and smishing scams using fraudulent emails and text messages together contribute to a good share, some 18%, of the recorded fraud attempts, now growing more sophisticated and harder to detect.

- There has been an explosive increase of over 100% in synthetic identity fraud cases since 2022, making it one of the fastest-growing types of fraud globally.

- Refund fraud also increases by 28%, especially targeting online merchants during high-return periods.

- Meanwhile, peer-to-peer payment platforms have seen an increased frequency of fraud by 22%, with classic stories of users reporting unauthorised or misleading transfers.

- Card-not-present (CNP) fraud also remains a big threat-taking half of e-commerce fraudulent cases in 2025.

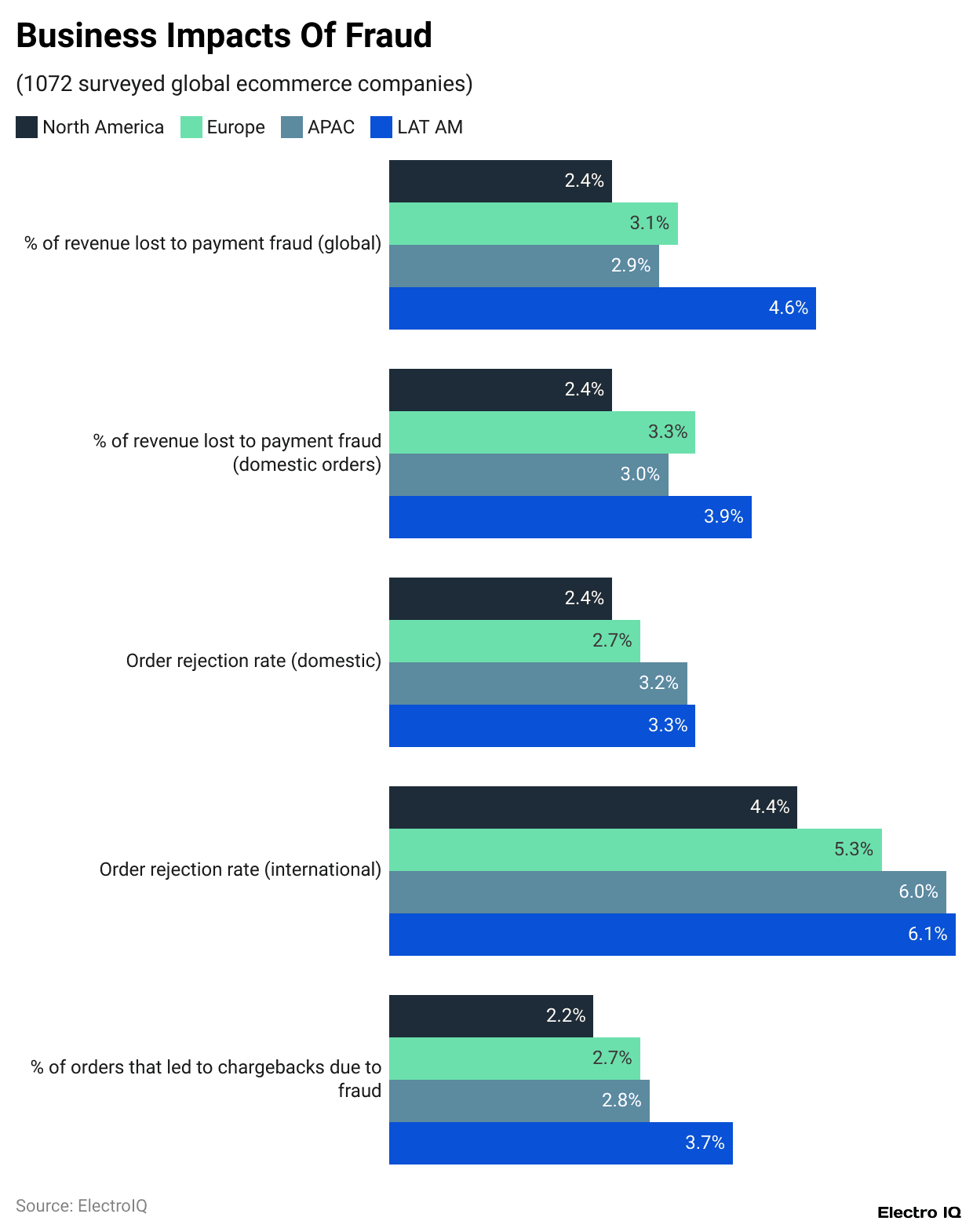

Business Impacts of Fraud

(Reference: coinlaw.io)

- Globally, e-commerce entities are losing between 2.4% and 4.6% of revenue through fraud, with the highest level of losses occurring in Latin America at 4.6%.

- Domestic orders also suffer fraud-related revenue losses between 2.4% and 3.9%; at 3.3%, Europe suffers an average loss, while Latin America leads again at 3.9%.

- Domestic order rejection rates vary from 2.4% in North America to 3.3% in Latin America, many seeing this as a reflection of tighter controls in higher-risk markets.

- For international orders, rejection rates are higher still- ranging from 4.4% in North America to 6.1% in Latin America-as a reflection of the increased risks in cross-border transactions.

- Fraud chargebacks afflict somewhere between 2.2% and 3.7% of all orders, with Latin America topping that range once again, reflecting that the region encounters disproportionate problems in managing and forestalling fraudulent payments.

With New Technology Comes More Sophisticated Fraud

- New technology is heralding the rise of highly complex, very difficult-to-detect types of fraud.

- For example, with deepfake technology, criminals can basically impersonate their victims or trusted executives in around 7% of social engineering scams.

- The use of AI and machine learning has taken phishing campaigns to a whole new level-fraudsters are automating such attacks, which have increased their success rates by some 30%.

- There has been a 25% increase in wallet fraud in the cryptocurrency domain, with cybercriminals exploiting vulnerabilities in blockchain systems and wallet security.

- IoT-based fraud is also evolving as a significant threat, penalising approximately 12% of all cases of global fraud.

- QR code fraud has gained in momentum as well, with a growth rate of about 35%, as attackers trick users into divulging payment information via malicious codes.

- Synthetic identity fraud-using AI-driven identities, has increased by 45%, making it more difficult for financial systems to detect.

- The use of tools and stolen data on the dark web has also been a catalyst for a 28% increase in cyber-enabled payment fraud, exemplifying how technology has assisted in scaling up both the size and the sophistication of modern fraud tactics.

Modern Challenges For Financial Institutions

- Modern institutions face an ever-changing threat landscape.

- Some 70% place regulatory compliance amongst one of their key challenges since regulation and fraud prevention require attempting to keep pace with digital innovation.

- The increasing acceptance of systems for real-time payments has actually increased the risk the exposed windows to instant fraud increased by 25% because of the limited time window for detecting and acting.

- Legacy technology has remained a weak spot, with 35% still relying on systems that do not provide modern security features.

- Insider fraud is turning into a rising problem for financial institutions, with offences rising by some 40% over the preceding year.

- Integrations with third-party fintech have also aggravated vulnerabilities, with 25% of financial organisations attributing fraud instances to those partnerships.

- Cross-border fraud in the financial area rose by 20% in 2025, denoting the broader outreach of international fraud networks.

- Consequently, more than 80% of banks now hold the view that fighting fraud effectively will henceforth require perpetual investment in technology.

Mobile Payments Driving The Surge In Digital Fraud

- Mobile and digital payments have very rapidly assumed the leading role in contributing to more fraud incidents all across the world.

- With consumers moving toward the mobile app, QR Codes, digital wallets, and P2P transfers, fraudsters are just following the money and using their skills with rapid technological changes to exploit every weakness in these payment channels.

- In the U.S., most fraud costs being met in e-commerce are now being met in mobile and online transactions.

- About 53% of all fraud losses are accounted for by online purchases, and another 30% are accounted for by mobile payment channels.

- More than 80% of all dollars lost to fraud in U.S. e-commerce now result from digital transactions.

- Mobile payment methods are linked to 41% of e-commerce fraud costs in the country, which shows the shift of fraud away from traditional credit card channels toward mobile and app-based payments.

- In the United States, 20% of fraudulent activities involve QR Code Payments, 15% Digital Wallets, and 6% Peer-to-Peer Payment Apps.

- Higher numbers are such numbers in Canada, with 25% of fraud cases standing in connection to QR Code Payments, 16% to Digital Wallets, and 7% to Peer-to-Peer Transactions.

- These statistics present a serious issue for businesses: payment systems that are real-time in customer interaction are evolving at a rate that has outpaced the development of most security tools.

- Fraudsters use this window to commit fraud due to the immediate transaction speeds and inadequate verification checks.

- Such data clearly makes the point that with the rise of mobile payments, these channels must be protected by merchants and financial institutions at all times.

Real-Time Fraud Monitoring Becomes A Top Priority Across Industries

(Source: learn.seon.io)

- The prediction about AI and ML in the payments sector is a bit striking – almost 51% of companies invested, because they see AI and ML as being able to catch subtler forms of the kind that their own traditional systems might typically overlook.

- Another half is focused on real-time monitoring so that fraudulent activity can be tracked and stopped in the act.

- About 44% improve automation tools to lessen manual reviews and speed up the workflow of fraud prevention.

- eCommerce ranks higher for AI investments than the payments industry.

- Due to the sheer volume of transactions and customer data processing, online retailers view automation and intelligence as bona fide necessities.

- Real-time monitoring improvements are being focused on by almost 45% of the operators, and 43% are looking into improving automation tools to manage fraud more efficiently during online shopping’s busiest periods.

- In financial services, 47% of firms invest in AI and ML, while 46% spend more on prevention technologies.

- Banks and other financial institutions deal with extremely sensitive customer data and with transaction volumes running into millions, so proactive defence becomes a must.

- About 43% are working to improve integration tools that ensure seamless communication in real-time between disparate systems, from transaction processing to fraud detection.

- Fintech is not far behind. Around 53% are going for AI and ML investment to deploy intelligent algorithms that will keep up with chillingly fast-changing fraud tactics.

- Another 47% will beef up their prevention budgets, while 43% will work on integrating tools to achieve a single view of fraud detection at the platform and API level.

Recent Digital Wallet Fraud Developments

- In 2025, we will again witness the evolution of digital payment fraud alongside emerging technologies and new-age financial services.

- As digital assets grew in popularity, the number of crypto-related fraud cases grew by 20%, pointing to loopholes in wallets and exchanges.

- The same interfacing with victims was enhanced through an upsurge of 25% in deepfake scams where AI-generated videos impersonate individuals.

- Embedded finance service fraud went up by 18%, with integrated platforms connecting banking, payments, and commerce opening new attack surfaces for exploiters.

- QR code payment scamming soared by 51%, especially at public places like restaurants and transit hubs, where users do not feel the need to check the code for authenticity.

- AI-powered hacking tools are a major contributor to another 30% jump in cyber-enabled payment fraud, which speaks volumes about the increasing complexity of automated attacks.

- Heavily contributing thereto is an increase by 28% in the “fraud-as-a-service” platforms, which advanced the availability of fraud tools in making it so easy for criminals that they need very little technical expertise to launch complex schemes.

Conclusion

Digital Wallet Fraud Statistics: As evidenced by digital wallet fraud in 2025, the mobile and online payments arena bears increasing risks, as fraudsters keep innovating with technology to exploit gaps. While mobile-based fraud accounts for 75% of incidents and cross-border attacks rise, the most targeted platforms remain digital wallets and cryptocurrencies. Detection gets harder with AI-driven scams, QR code attacks, and synthetic identities, while the biggest losses are seen at e-commerce and financial institutions.

Real-time monitoring, AI, and automation are becoming pertinent factors in staying ahead of the curve on threats. Defending mobile payment channels, investing in next-gen detection solutions, and reinforcing security frameworks are the top priorities henceforth for businesses and financial institutions around the globe.

Sources

FAQ.

With digital wallets considered 48% most vulnerable and cryptocurrencies considered 38% most vulnerable by respective organisations, these systems remain the principal targets of attacks. Rewarding social games, P2P payment systems, and DeFi platforms are also in danger.

In almost 75% of fraud cases, mobile devices come into the picture. Mobile payments, QR code, digital wallet, and P2P app user fraud cases are among the highest loss cases of crimes and in the United States and Canada, signalling a further shift from traditional card-based fraud.

AI and machine learning would help in the fraud aspect and its solutions. Fraudsters automate mass phishing campaigns and other attacks using deepfakes. On the other hand, organisations use AI, real-time monitoring, and automation processes to detect and prevent fraud with a 95% detection rate.

At a global level, e-commerce companies have their earnings diminished between 2.4%–4.6% due to fraud, with the highest losses being suffered by Latin America acquirers; chargebacks, dispute fees, and cross-border fraud further add to the heavy cost to merchants and financial institutions.

Organizations invest very heavily in AI and real-time monitoring, and automation for instant detection of fraud. E-commerce, fintech, and financial services, in turn, are investing in upgrading systems, integrating platforms, and making continuous investments in advanced technologies to address the threats as they evolve.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.