AI Chip Statistics By Market Size, Funding and Facts (2025)

Updated · Dec 22, 2025

Table of Contents

- Introduction

- Editor’s Choice

- AI Chip Market Size

- AI Chip Market Revenue Globally

- AI Chip Company Performance, And Global Semiconductor Supply Chain Trends

- AI Chips In Consumer Electronics And Enterprise Use Cases

- Investments And Funding In AI Chip Startups

- Recent Developments In AI Chip Design And Innovation

- Conclusion

Introduction

AI Chip Statistics: The year 2025 will be a milestone in the history of AI, since then, the AI chips will no longer be a data center eggshell, but one of the main factors defining the worldwide semiconductor market value. Different types of chips (such as GPUs, TPUs, IPUs, NPUs, and custom ASICs) strategically placed in the computing stack are changing the overall value landscape.

Below, we present a glimpse of AI chip statistics for 2025 based on research: market sizes, investment and technology drivers, and the risks that are reshaping the next wave of innovation.

Editor’s Choice

- The AI chip market is rapidly expanding, reaching US$39B in 2025 and projected to grow to US$341B by 2033.

- The most important AI accelerator remains the GPU, and NVIDIA is leading the way with its Hopper and Blackwell series, while AMD and China-based vendors are gaining strength.

- High-tech approaches such as HBM, 2.5D/3D packaging, and chiplet architectures are moving to the forefront and improving performance across AI chips.

- AI chip revenues are expected to reach US$91.96 billion in 2025, with the market projected to exceed US$100 billion by the middle of 2026.

- In the tech companies market, large fluctuations in market value were observed, primarily driven by rapid revenue growth, except for Intel, which reported US$7.2 billion in revenue.

- NVIDIA is expected to generate US$49B in AI revenue in 2025; AMD’s target is US$5.6B, and Intel’s Gaudi 3 is anticipated to account for 8.7% of the AI training market.

- Google’s TPUs will add US$3.1B to the company’s value; Apple’s A19 Bionic provides 35 TOPS; and Qualcomm will sell over 800M AI-enabled chips in 2025.

- A substantial 28% of TSMC’s wafer production capacity was allocated to AI chips; Samsung achieved a 90% success rate in the 3nm GAA process; Intel has secured four new foundries for AI.

- Revenue from AI chip packaging reached US$4.7B, primarily due to 2.5D/3D stacking technology; the substrate shortage was resolved by mid-2025.

- The delivery period was reduced to 12 weeks, and Foxconn announced that two additional AI assembly plants would be built in Arizona.

- AI smartphones are set to surpass 980 million unit shipments, and 42% of laptops and tablets will be equipped with NPUs.

- Robotics, wearables, and enterprise servers powered by AI are strongly driving hardware demand, with the chip consumption of enterprise AI servers at US$21.6 billion.

- Investments worldwide in AI chip startups reached over US$11.6 billion in 2025, with Tenstorrent, Mythic AI, Cerebras, and Enflame among the companies that received the largest funding rounds.

- The semiconductor startup ecosystem in India saw an influx of US$410 million, while Graphcore was provided with a US$280 million bailout plus an innovation grant.

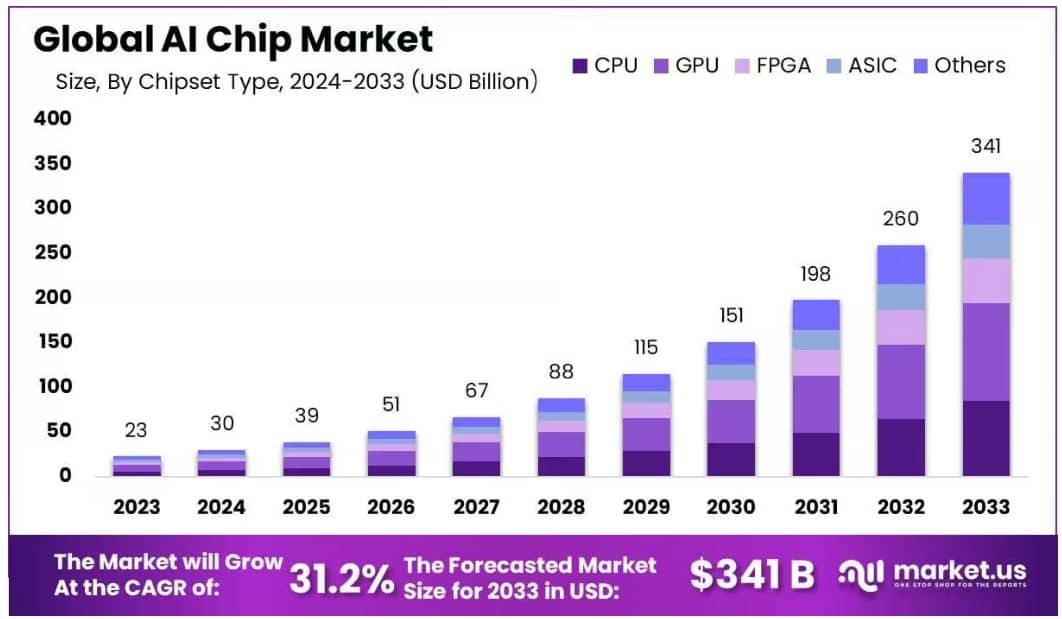

AI Chip Market Size

(Source: market.us)

- For quite a long time, the AI chip market has been undergoing a very strong and steady increase in demand.

- The market’s valuation of 23 billion USD in 2023, recorded early in the year, indicated that the industry had a strong likelihood not only of surviving but also of prospering.

- The following year’s growth saw the market size increase to 30 billion USD in 2024, thus indicating the rapid acceptance of AI technology across various sectors like data centers, automotive, smartphones, robotics, and edge devices.

- The rise of AI technologies and the concomitant demand for high-performance computing bode well for the market.

- The AI chip market is predicted to be worth 39 billion USD in 2025 and 51 billion USD in 2026, according to the forecasts.

- The growth trend is still ongoing. Experts foresee the market value will rise to 67 billion USD in 2027, 88 billion USD in 2028, and 115 billion USD in 2029. This slow growth is a strong indication that AI is becoming increasingly ingrained in business, consumer, and industrial contexts.

- If we look further into the future, the market size will be impressive over the next ten years.

- The AI chip market size in 2033 will be 341 billion USD, as per estimates, which is an enormous sum, and it clearly shows how AI chips are becoming the major supporting infrastructure of automation, analytics, personalized computing, and advanced AI applications.

- This ongoing growth trend signals the market’s position as a key player in future innovation and technology development.

- Graphics Processing Units (GPUs) are expected to have the highest demand in the chip market for AI in the coming years.

- Currently, the largest share is occupied by Graphics Processing Units (GPUs) due to their high performance in massive parallel processing, which is necessary for large-scale AI training and inference.

- The largest and most powerful AI systems, such as the hyperscale data centers and supercomputers, are very much dependent on GPUs.

- These systems are operated on a considerable scale, sometimes even reaching exaFLOPS performance, and can be located on-site or be part of a distributed cloud network.

- NVIDIA is the most prominent company in the GPU market with its Hopper series (H100 and H200) and the forthcoming Blackwell chips (B200 and B300) contributing to its major success.

- Moreover, AMD, the challenger, has strengthened its position by introducing the MI300 series, which includes the demanding MI300X and MI325X, designed for such AI workloads and other applications.

- Simultaneously, U.S. sanctions on China that restrict access to advanced chips have forced Chinese companies to intensify efforts to develop their own high-performance GPU solutions.

- The technologically advanced GPUs are heavily dependent on cutting-edge semiconductor tech to maintain their performance gains.

- This is the very subject of the IDTechEx report “AI Chips for Data Centers and Cloud 2025–2035: Technologies, Market, Forecasts.”

- HBM technology from major manufacturers such as Samsung, SK Hynix, and Micron, as well as advanced packaging processes such as 2.5D and 3D integration, are among the developments that are leading the way.

- Chipmakers and foundries that include TSMC, Samsung Foundry, and Intel are using sophisticated transistor processes and chiplet architectures to realize higher efficiency and performance.

- Together, these innovations show why GPUs remain at the forefront of AI computing and how the industry continues to evolve to meet growing demand.

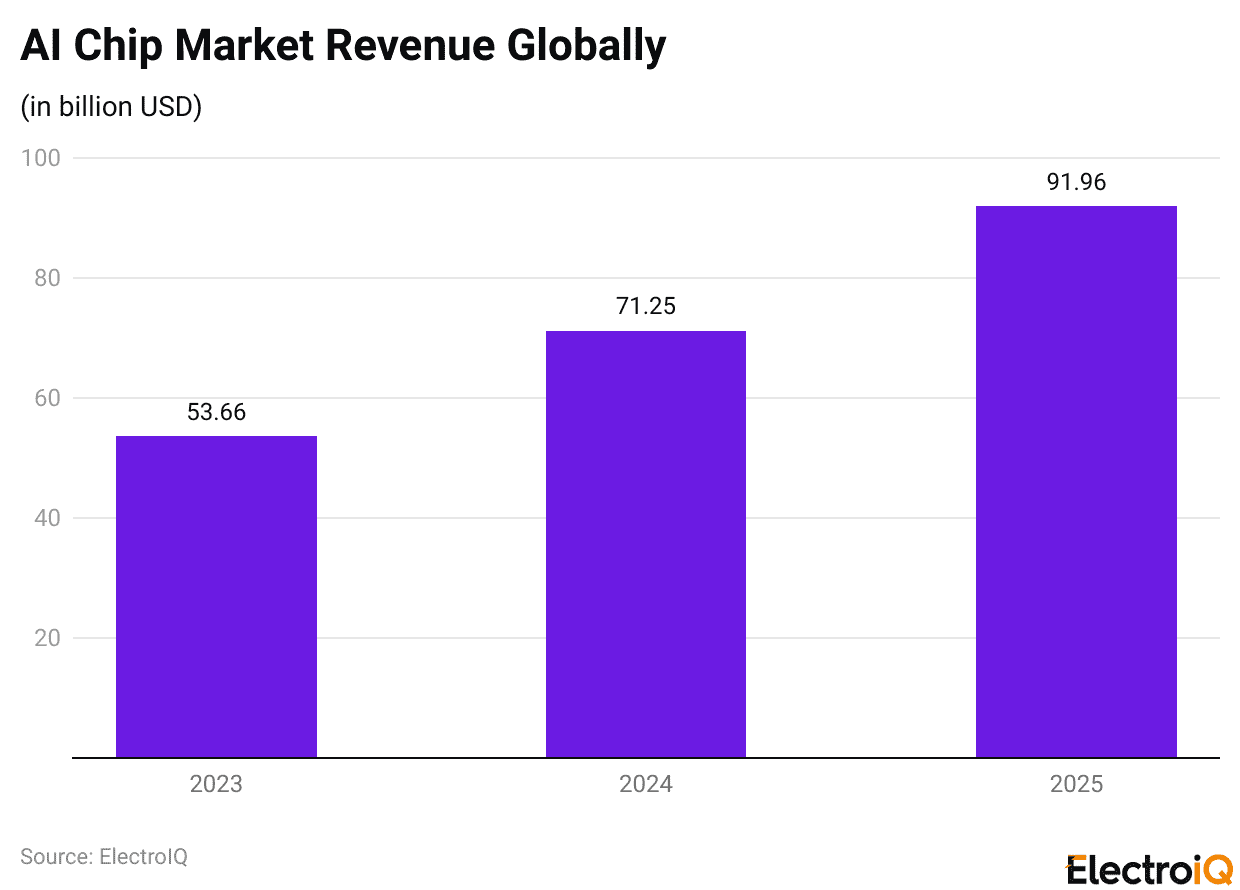

AI Chip Market Revenue Globally

(Reference: electronicsforyou.biz)

- Global demand for AI hardware is rising dramatically, and as a result, the AI chip market is likely to be valued at US$100 billion by the beginning of 2026, although large companies remain subject to significant market pressure.

- Reports from Stocklytics and Gartner predict that AI chip revenues will exceed US$91.96 billion in 2025, marking the third consecutive year of revenue growth exceeding 30%.

- Sales increased from US$53.66 billion in 2023 to US$71.25 billion in 2024, and then this year alone, there was a jump of almost US$21 billion.

- All this is occurring due to the rapid growth of generative AI, the continuous expansion of cloud infrastructure, and the influx of AI-centric startups.

- Advances in technology and machine learning, coupled with the aggressive innovation of firms such as NVIDIA, AMD, and Google, continue to produce the highest-quality chips.

- Demand has exceeded supply, export regulations have become stricter, and chip shortages have led to a surge in prices.

- Nevertheless, analysts maintain a positive outlook, and the market is not expected to exceed US$100 billion until the middle of 2026.

- The industry’s growth is significant, yet major chipmakers have experienced a sharp decline in their valuations.

AI Chip Company Performance, And Global Semiconductor Supply Chain Trends

- NVIDIA and Google each lost more than US$400 billion; Amazon and AMD’s valuations decreased by US$270 billion and US$30 billion, respectively. Intel is the exception, having added US$7.2 billion to its market capitalization after recovering from a difficult 2024.

- NVIDIA is expected to reach an astounding US$49 billion in AI-related revenue by 2025, which constitutes a hefty 39% increase from the previous year, thus bolstering its position as the leading accelerator supplier.

- AMD, too, should experience a significant growth, as the AI chip market it is going to serve will be worth US$5.6 billion, which means that the company will be able to double its share in data centers where the chips are used.

- Intel’s venture into the AI accelerator market is not going unnoticed, as its Gaudi 3 platform is expected to gain 8.7% of the AI training market by the end of 2025.

- Google is constantly reinforcing its proprietary hardware operations, with its TPU line thought to be worth US$3.1 billion this year.

- The A19 Bionic chip that has just been released by Apple marks a new benchmark for on-device intelligence, thanks to the 35 TOPS neural engine driving it.

- Qualcomm, still a mobile and edge AI premier, is estimated to distribute more than 800 million AI-enabled chips in the Internet of Things (IoT) by 2025.

- Amazon’s proprietary Trainium2 and Inferentia2 accelerators are envisioned to support 35% of the new AI workloads on AWS, thus marking their rising significance in cloud AI.

- TSMC will set aside more than 28% of its entire wafer capacity for AI chip production, thus affirming its vital position in the world’s supply chain.

- At the same time, Graphcore is expected to deliver 600,000 IPUs to scientists and academic institutions, while Tenstorrent’s licensing and design revenue is projected to hit US$240 million by 2025.

- The global revenue from packaging of AI chips ascended to US$4.7 billion, with the main factor being the great adoption of 2.5D and 3D stacking.

- The substrate shortages that earlier caused production disruptions considerably eased by Q2 2025, as a result of new capacities coming on stream in Taiwan and Malaysia.

- ASML delivered 57 EUV lithography systems to different companies, thus facilitating the attainment of the aggressive sub-5nm timelines set by the company’s major semiconductor foundries.

- The average lead time for AI chips shrank to 12 weeks owing to the application of more efficient inventory policies, while COB packaging’s growth was reported to be 38% compared to last year, particularly in the automotive and wearable markets.

- Foxconn pledged investments into two new AI-centric assembly plants in Arizona as a measure to reduce importation from other states and thereby support U.S. supply chain localization.

- NVIDIA’s agreements with TSMC and Samsung amounted to more than US$14 billion in wafer starts and backend services, which was a clear indication of the company’s huge production requirement.

AI Chips In Consumer Electronics And Enterprise Use Cases

- AI-integrated smartphones are likely to exceed 980 million unit shipments in 2025, largely due to on-device generative voice and imaging enhancement as the most prominent features.

- Consumer laptops and tablets with NPUs will account for 42% of the total consumer computing market. Global sales of smart TVs with AI content optimization are estimated to reach 135 million units.

- The revenue from components for wearables using AI in health monitoring and gesture detection will be US$2.3 billion, while the market for intelligent home robotics will have US$1.2 billion in sales.

- Enterprise AI servers will not consume more than a billion dollars’ worth of chips (US$21.6 billion), supported by demand from Fortune 500 companies.

- The deployment of AI collaboration devices, combined with AI-human interaction, would exceed 47 million units, and the retail market employing real-time AI analytics would reach US$1.6 billion in expenditure.

- The use of AI in security systems would require US$4.1 billion in chips, whilst the segment of the market devoted to artistic gadgets that use generative AI, such as smart cameras and audio processors, would be worth US$870 million by 2025.

Investments And Funding In AI Chip Startups

- Global investment in AI chip startups exceeded US$11.6 billion in 2025, and more than 140 funding deals had already been completed by mid-year.

- The total for the United States was US$5.1 billion, comprising several large Series C and Series D rounds.

- Tenstorrent, a company focused on RISC-V-based AI processors, raised 279 million in new financing, backed by Fidelity and the Samsung Catalyst Fund.

- Analog computing expert Mythic AI collected US$190 million, while Cerebras Systems’ worth climbed to US$2.2 billion after it closed a US$400 million Series F funding round.

- In the case of edge inference, Untether AI received US$140 million in growth financing, and Esperanto Technologies received US$115 million to broaden its energy-efficient 7nm RISC-V AI chip family.

- The Chinese firm Enflame Technology secured US$700 million through a combination of public and private investment streams, bolstering its local AI chip operations.

- The Indian AI semiconductor supply chain is also expanding quickly due to US$410 million in venture and strategic investments.

- At the same time, Europe’s Graphcore was granted US$280 million to support stability and fund innovation while coping with the challenges of restructuring and downsizing its operations.

Recent Developments In AI Chip Design And Innovation

- In 2025, NVIDIA’s Blackwell architecture was released, which provided a doubling of the transformer processing speed and better sparsity-based optimization handling.

- The Intel Gaudi 3 was introduced in early 2025 and concentrated on becoming an integral part of open software ecosystems, while at the same time delivering excellent power efficiency in terms of cost per watt.

- The Google TPU v5p was very efficient with the use of multi-slice matrix fusion, which led to a throughput increase of 35% for large model training in 2025.

- The AMD MI400X was a notable example of chiplet-driven modular design, enabling flexible, scalable AI workload distribution in 2025.

- Samsung’s 3nm GAA-based AI SoC, presented in 2025, achieved 22% higher energy efficiency than the previous generation.

- The IBM neurosynaptic chip, based on spiking neural computation, was in early testing in 2025 and was reported to reduce power consumption for certain AI tasks by a factor of 10.

- The ARM Cortex-X5 AI cores were successfully deployed and became part of more than 480 million mobile devices in 2025, thanks to their exceptional AI scheduling capability that enabled multitasking.

- The Meta MTIA v2, which was meant for the recommendation workloads, was released in 2025 and included an enhanced graph-based AI optimization, which led to a significant in-house adoption.

- In 2025, TSMC’s Backside Power Delivery (BSPDN) was the first in AI chip manufacturing, yielding up to 12% performance gains.

- Companies like Rebellions (Korea) and SiMa.ai (US), among others, launched edge AI processors that were customized for robots and healthcare applications in the year of 2025.

Conclusion

AI Chip Statistics: The AI chip scenario in 2025 marks a turning point for the semiconductor industry, as it is characterized by the most unprecedented market growth ever, insanely quick technological innovation, and a surge of global investment. The use of GPUs, NPUs, TPUs, and custom-made accelerators in data centres and consumer devices has already made AI hardware a foundation of digital transformation. Advances in packaging, memory, and fabrication processes are continually pushing performance boundaries, and demand is increasing for smartphones, enterprise servers, robotics, and edge AI.

Startups are receiving billions in funding, and the large ones are expanding aggressively; thus, the AI chip market is poised for a prolonged growth period that will not only shape the future of computing for the coming decade but also for years to come.

FAQ.

The AI chip market is forecasted to be worth US$39 billion by 2025, already displaying a strong upward trend from the previous years, and thus confirming its position as one of the fastest-growing segments in the semiconductor industry. If one also considers wider AI hardware categories, the revenue of AI chips is expected to reach US$91.96 billion in 2025, as per Gartner and Stocklytics estimates.

GPUs remain the dominant force due to their ability to perform parallel processing, which is a large-scale AI model’s training and inference requirement. NVIDIA remains the main player in the market with its Hopper (H100/H200) and Blackwell (B200/B300) architectures that are powering most of the hyperscaler AI farms. AMD is right behind with its MI300/MI325 GPUs, whereas China is speeding up the development of its local alternatives due to export restrictions.

NVIDIA is at the top with US$49 billion AI revenue anticipated for the year 2025, thus it will continue to be the most preferred training hardware supplier. AMD’s earning is estimated at US$5.6 billion, which will allow the company to increase its share in the data center market. Intel’s Gaudi 3 accelerators are predicted to get a strong 8.7% share in the AI training segment. Google’s TPUs will be worth US$3.1 billion, and Apple’s A19 Bionic will support 35 TOPS for AI on-device, and Qualcomm is going to deliver more than 800 million AI-ready chips.

The AI chip manufacturing sector experienced revolutionary advancements in 2025. TSMC, for instance, designated 28% of its wafer capacity for the manufacturing of AI chips, while Samsung’s yield for the cutting-edge 3nm GAA nodes reached 90%. The packaging market also reached US$4.7 billion, as the 2.5D/3D stacking method became more widespread, and the shortage of substrates was relieved by enhancing the production capacity in Taiwan and Malaysia.

AI chips have penetrated deeply into different sectors, making them mainstream. In fact, the consumer electronics sector will witness a shipment of over 980 million AI smartphones by 2025, and meanwhile, the NPUs will be present in 42% of laptops and tablets, allowing the latter to perform generative processing of the data right on the device. The application of AI chips in wearables, robotics, and smart TVs is the source of billions in revenue.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.