Asana Statistics By Revenue, Employees, Financial Outlook, Fiscal Performance and Facts

Updated · Mar 26, 2026

Table of Contents

Introduction

Asana Statistics: Asana, an organization that develops work management software, has emerged a little slow since its growth became apparent in 2024, when a sudden emphasis on innovation and customer satisfaction drove revenue growth.

This article concerning Asana’s 2024 state outlines the Asana statistics performance indicators in its financial performance, customer expansion, product use, and strategies.

Editor’s Choice

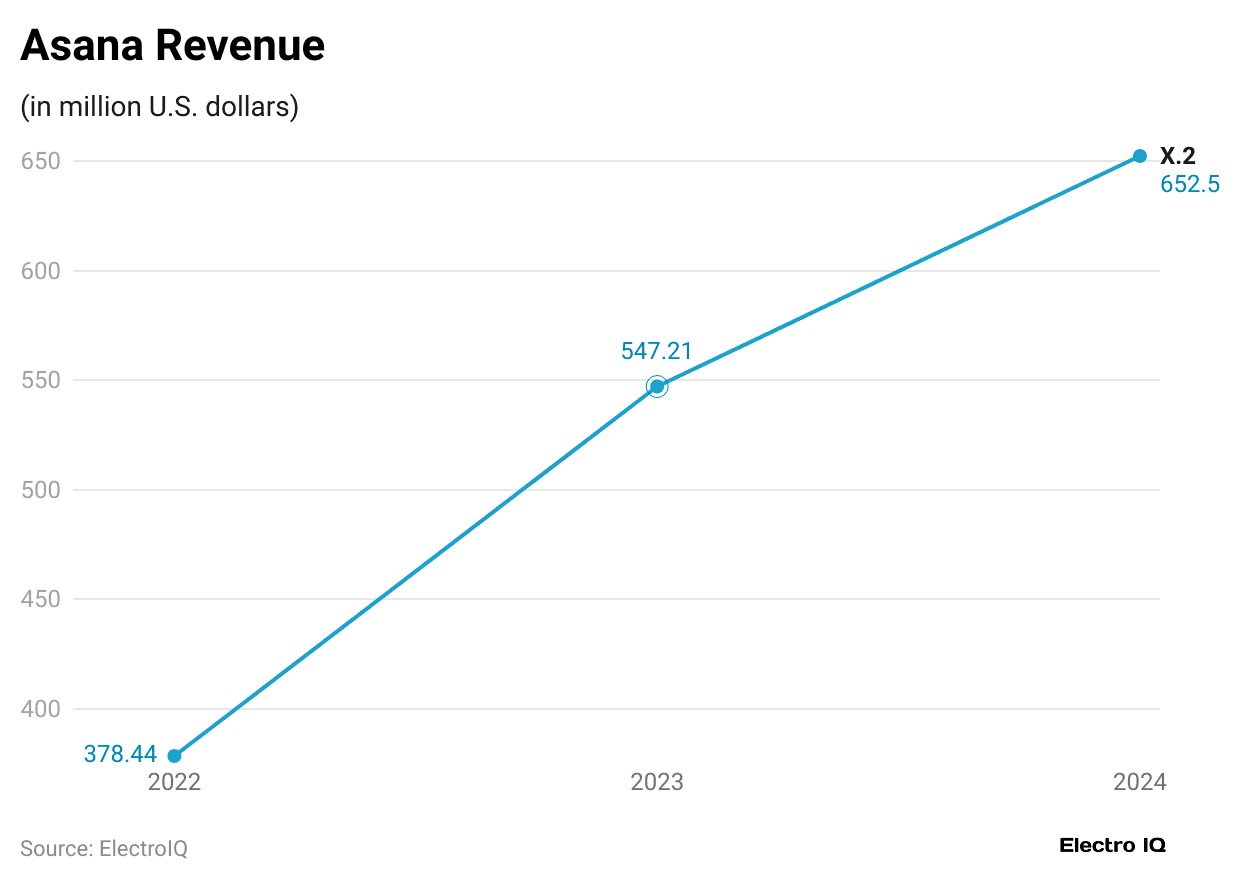

- According to Asana statistics, Revenues of Asana amounted to USD 652.5 million in 2024, representing a 19% increase from USD 547.21 million in 2023 and a growth of 72% from USD 378.44 million in 2022.

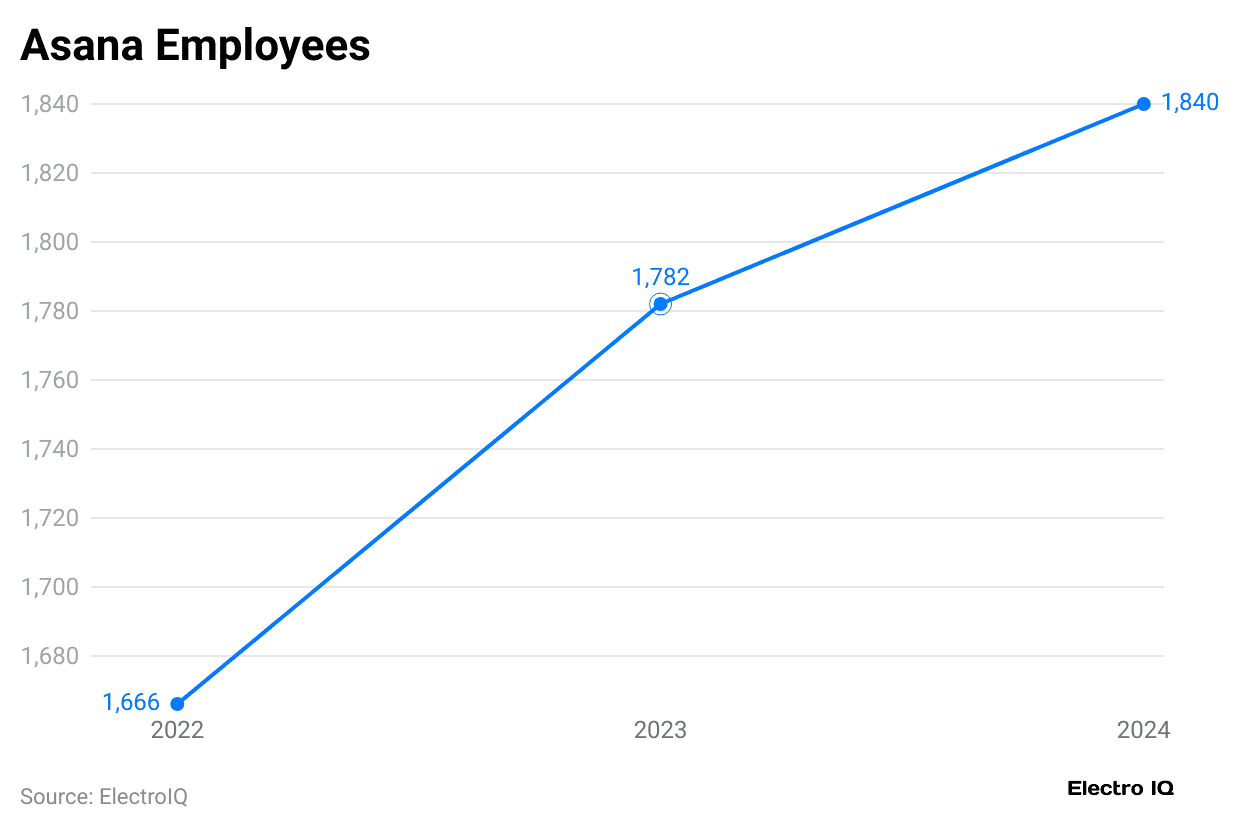

- In 2024, Asana’s strength reached 1840 employees, which represents a remarkable growth from 1782 in 2023 and 1666 in 2022.

- The gross profit moved up to USD 153.7 million for the fourth quarter of 2024 from USD 135.0 million in the same quarter of 2023, and gross profit for the entire year reached USD 588.0 million.

- Research and development for the year pushed higher to USD 324.7 million from USD 297.2 million in 2023 for continued investments in innovation and new products.

- There was an improvement in efficiency and cost optimization, thereby reducing sales and marketing costs from USD 435.0 million in 2023 to USD 392.0 million in 2024.

- Asana statistics show that General and administrative costs were lowered from USD 166.3 million in 2023 to USD 141.3 million in 2024, indicating good control of expenses.

- Asana reported a GAAP operating loss of USD 67.9 million in Q4 2024 (40% of revenue), an improvement from a loss of USD 99.2 million (66% of revenue) in Q4 2023.

- The Non-GAAP operating loss for Q4 2024 declined to USD 15.6 million (9% of revenue), down from USD 37.4 million (25% of revenue) in Q4 2023.

- Asana statistics state that GAAP net losses were USD 95.0 million in the fourth quarter of 2023 and USD 62.4 million in the fourth quarter of 2024, with GAAP net loss per share declining from US $0.44 to USD 0.28.

- For fiscal year 2024, non-GAAP net loss reduced to USD 10.1 million from US $33.2 million in Q4 2023; non-GAAP net loss per share improved from USD 0.15 to USD 0.04.

- Operating cash flows improved slightly at negative USD 15.3 million compared to negative USD 31.1 million in Q4 2023; free cash flows have greatly improved from negative USD 26.5 million to negative USD 17.0 million.

- Total core customers, generating revenue of at least USD 5,000, signed nearly 11%; revenues from these 21,646 customers grew 16%.

- Asana statistics indicate that the number of larger accounts with Asana doing USD 100,000 and above a year increased by 20% to 607, with strong dollar-based net retention north of 100%.

- Asana has set up a new office in Warsaw, Poland, the 13th worldwide and the 6th in the EMEA region.

- Hosted the Work Innovation Summit and published The Work Innovation Lab research, shedding light on collaboration technology.

- For fiscal year 2025, revenues will be in the range of US $716.0–USD 722.0 million, and the projected non-GAAP operating loss will be in the range of USD 61.0–USD 55.0 million.

- For 2025, it expects a non-GAAP net loss per share in the range of USD 0.22 to USD 0.19, with approximately 230 million shares outstanding.

Asana Revenue

(Reference: fourweekmba.com)

(Reference: fourweekmba.com)

- Asana has witnessed a retail boost in the last three years, which indicates its expanding presence and acceptability in the work management platform market.

- By 2024, the company’s generated revenue stood at USD 652.5 million, compared to USD 547.21 million in 2023, a rise of approximately 19% year-on-year increase, signifying new client acquisitions and growing service offerings against existing accounts.

- Further, 2024 continued showing revenues-on-growth based on something solid from the strong past motion of years.

- In 2022, Asana’s revenue was USD 378.44 million, and the company had an above 45% increase in 2023 from that figure.

- Such drastic growth is attributed to the many customers, increasing enterprise market penetration, and ongoing fine improvements to its product offerings, including better AI tools and workflow automation.

- The swing from USD 378.44 million in 2022 to USD 652.5 million in 2024 created a grand growth of nearly 72% over the entire period.

- This exemplifies the ability of the company to efficiently scale the business and compete with others in the industry of work management.

Asana Employees

(Reference: fourweekmba.com)

(Reference: fourweekmba.com)

- Asana statistics state that by the year 2024, Asana had grown its workforce to 1,840 employees, steadily growing its headcount over the years.

- In contrast, in 2023, the company employed 1,782 employees, thus adding 58 employees in one year. This growth signifies that Asana is scaling up operations via investments in new hires to serve its growing customer base.

- Looking back further, Asana had 1,666 employees in 2022, which puts the increase in employees for the company at 174 over two years.

- The slow but steady increase in employees suggests that the company has been scaling its teams across departments, including product development, customer support, and sales.

- This can also mean the financial stability of Asana to invest in human capital despite fluctuations in the market.

- As the company adds more offerings and expands its reach worldwide, more people are being hired so that service will remain at high standards, support an ever-increasing customer base, and further drive innovation.

- The gradual expansion of headcounts from 2022 to 2024 thus underscores long-term vision and sustainable growth in the work management software industry in which the company competes.

Asana Financial Performance and Cost Management

(Source: asana.com)

(Source: asana.com)

- Asana statistics show that costs related to revenues connected with the expenses incurred to provide Asana services have also increased.

- This amount increased during the three months from USD 15.2 million in 2023 to USD 17.4 million in 2024.

- For the full year, the increase was from USD 56.6 million to USD 64.5 million. The increase, notwithstanding, gross profit was up most significantly, coming at USD 153.7 million for the last quarter, compared with USD 135.0 million for the same period in 2023.

- For the full year, gross profit was USD 588.0 million, compared with USD 490.7 million in 2023.

- Asana maintained investment in some key focus areas, principally research and development, which recorded a rise in expenditures from USD 297.2 million in 2023 to USD 324.7 million in 2024, indicating continuous efforts to develop the platform and release new features.

- The decrease in sales and marketing expenses reflects improved efficiency in this area.

- In the last quarter, sales and marketing expenses dropped from USD 114.7 million in 2023 to USD 103.9 million in 2024.

- For the full year, expenses fell from USD 435.0 million to USD 392.0 million, a sign of cost optimisation. General and administrative expenses were also down.

- These expenses were USD 34.8 million this quarter versus USD 38.2 million last year. For the full year, expenditures fell from USD 166.3 million in 2023 to USD 141.3 million in 2024.

- The cutbacks reflect Asana’s efforts in streamlining operations and effective cost management. Total operating expenditures fell, inclusive of all expenses of operating the business.

- In the last quarter reported, total expenses included USD 221.7 million versus USD 234.2 million a year ago.

- Over the whole year, operating expenditure was USD 858.0 million, compared with USD 898.5 million in 2023.

- Asana statistics demonstrate Asana’s balanced focus on growth while still exercising cost control and maintaining investment in key areas of the business.

Asana Fiscal Performance in Quarter 4

- Significantly, Asana’s financial performance for the fourth fiscal quarter of 2024 had evolved remarkably over time by comparison with that of the same period last year.

- According to Asana statistics, the GAAP operating loss of the company amounted to USD 67.9 million, equivalent to 40% of revenue. This was a notable improvement from last year’s GAAP operating loss of USD 99.2 million, or 66% of revenue.

- The operating loss was then reduced to USD 15.6 million on a non-GAAP basis, or 9% of revenue, compared with a non-GAAP operating loss of USD 37.4 million, or 25% of revenue, in the fourth quarter of fiscal 2023. Asana had also reduced its net loss.

- The GAAP net loss for the period was USD 62.4 million, read as USD 95.0 million net loss for the same quarter of the previous fiscal year.

- The third measure on a per-share basis was a GAAP net loss of USD 0.28, compared with USD 0.44 during the fourth quarter of fiscal 2023.

- There was also a non-GAAP measure of progress with a net loss of USD 10.1 million compared to USD 33.2 million in the prior year’s fourth quarter. Non-GAAP net loss per share was USD 0.04, compared with USD 0.15 in the previous year.

- Cash flow followed suit with the trend. Cash flows from operating activities were -15.3 million at the end of the year, compared with -31.1 million in the fourth quarter of fiscal 2023.

- Free cash flow went negative at -USD 17.0 million as opposed to last year’s same quarter, which was -26.5 million.

- They clearly show that Asana still incurs losses but has reduced the amount of its financial deficits and improved its cash management.

Business Highlights

- Asana statistics reveal that in the last quarter, Asana was able to grow its customer base well. 21,646 core customers spent at least USD 5,000 per year, and this showed an increase of 11% compared to the previous year.

- For these customers, revenue also increased by 16% compared to that in the previous year.

- The 607 high-end valued customers, who spent a minimum of USD 100,000, represented an increase of 20% over the previous year.

- Overall, Asana was able to enjoy a dollar-based net retention of more than 100%, which is indicative of customer loyalty.

- Among core customers, it stood at 105%, while it was even higher, at 115%, among those spending USD 100,000 or more.

- As part of its continued global expansion, Asana opened an office in Warsaw, Poland, the company’s 13th office in total and sixth in the EMEA region.

- The event also hosted the biggest event for the year, the Work Innovation Summit, which brought together company personnel, customers, and industry experts to look into the future of work.

- Asana has further released new research through The Work Innovation Lab, which gave businesses insights into the state of collaboration tech.

- Among other outputs, it highlighted data-driven strategies that organizations could adopt to streamline and optimize technology tools toward better efficiencies.

Financial Outlook

- According to Asana’s statistics, Asana disclosed an outlook on their finances for Q1 and the entire fiscal year 2025, indicating the organization is on a steady growth path and continues to reduce losses.

- For Q1 FY2025, Asana’s revenue projections were for USD 168 million to USD 169 million, a year-on-year improvement of 10% to 11%.

- In spite of the loss prospects, Asana expects a non-GAAP operating loss of USD 23 million to USD 21 million, with an operating loss margin of 13.7% to 12.4%.

- In other words, the company still makes losses, but its losses are becoming smaller. The anticipated non-GAAP net loss per share is set between USD 0.09 and USD 0.08 based on approximately 226 million shares.

- For the entire fiscal year 2025, Asana expects total revenues in the range of USD 716 million to USD 722 million, portraying similar growth of 10% to 11% as in Q1.

- The operational loss in non-GAAP terms for this period is expected to be in the range of USD 61 million to USD 55 million, with a greater operating loss margin between 8.5% to 7.6%. This shows that Asana is slowly recovering from losses and is in the process of achieving operational profitability.

- The company, however, expects a non-GAAP net loss per share between USD 0.22-USD 0.19 with approximately 230 million shares.

- In a nutshell, this would suggest that Asana is improving revenue on a steady basis and, at the same time, working on lowering losses.

- The company appears to be on track financially, striking the right balance between growing revenues and improving cost management.

Conclusion

As per Asana statistics, the year 2024 was transformational for Asana. It witnessed strong growth and profit, expansion into new customer bases, and development of innovative products. With its two-pronged approach of enhancing work management through AI integration and global reach, Asana is now being recognized as an industry leader.

Continued growth and innovation in strategic initiatives and fiscal outlook for 2025 align with the flexible and dynamic nature of the world’s modern organizations.

Sources

FAQ.

Asana went on to make US$652.5 million in revenue for 2024. This represents a 19% increase from US$547.21 million in 2023 and a 72% growth from US$378.44 million in 2022.

Asana focused more on efficiency moving forward, cutting costs by also reducing sales and marketing spending from US$435.0 million in 2023 to US$392.0 million in 2024, general and administrative expenses from US$166.3 million to US$141.3 million while also decreasing from US$95.0 million in Q4 2023 to US$62.4 million in Q4 2024.

The number of core customers spending at least US$5,000 annually rose to 21646, an 11% increase since 2023; High-value customers spending US$100,000 or more annually grew by 20% to 607, with funding straight from Asana seeing over 100% of dollar-based net retention.

Asana opened its 13th global office in Warsaw, Poland, in 2024, which is its sixth office in the EMEA region. The company continues to grow in international markets.

The Company is expecting revenue for fiscal 2025 to be in the range of US$716.0 million to US$722.0 million and a non-GAAP operating loss between US$61.0 million and US$55.0 million. The company expects a non-GAAP net loss per share of US$0.22-US$0.19 on about 230 million weighted shares outstanding.

Saisuman is a skilled content writer with a passion for mobile technology, law, and science. She creates featured articles for websites and newsletters and conducts thorough research for medical professionals and researchers. Fluent in five languages, Saisuman's love for reading and languages sparked her writing career. She holds a Master's degree in Business Administration with a focus on Human Resources and has experience working in a Human Resources firm. Saisuman has also worked with a French international company. In her spare time, she enjoys traveling and singing classical songs. Now at Smartphone Thoughts, Saisuman specializes in reviewing smartphones and analyzing app statistics, making complex information easy to understand for readers.