Insurtech Statistics By Market Size, Funding and Facts (2025)

Updated · Dec 02, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Insutrech Market Size

- InsurTech & AI Investment Trends

- Insurtech Vs Traditional Insurance

- Insurtech Change Through Innovations

- The Average Salary In The Insurance Industry

- Adjustments In Legal And Regulatory Environment

- Insutech Quarterly Funding

- Regional Distribution Of Insurtech Funding

- Annual Investment Into Property Related To Insurtech

- Top 10 Insutech Deals Worldwide

- Applicability Of AI In Insutrech

- InsurTech Investment Trends And Distribution (2012–Q2 2025)

- Emerging Economies’ Untapped Potential

- Recent Developments

- Conclusion

Introduction

Insurtech Statistics: Insurtech, a fusion of insurance and technology, continued its rapid changes in 2024. There was a cooling-off in some areas of the market, while AI-oriented companies continued to sell and attract skilled buyers to their businesses. The rapid progress in artificial intelligence, automation, and data analytics, along with new models of embedded insurance, has set new standards and changed customers’ expectations.

The areas of technology that are particularly AI-driven have, like others, been attracting attention from investors and insurers alike, though funding conditions have picked up a bit. The purpose of this article is to examine the insurtech statistics as measuring rods, the funding as a deluge, the technology applications as guns, the regional activity as hot spots, and the main developments of the digital transformation as reshaping the global insurance landscape.

Editor’s Choice

- The worldwide insurtech market is estimated to grow rapidly, from USD 11.8 billion in 2022 to USD 336.5 billion by 2032, driven by digital adoption, AI, and automation.

- Technological insurance for health, home, and auto is seen as a major growth driver, with health insurtech alone expected to reach USD 94.2 billion by 2032.

- To date, the total value of insurtech funding since inception is around USD 60 billion, while globally, AI investment amounts to approximately USD 1.6 trillion, indicating a significant capital shift towards AI.

- Approximately one-fourth of total insurtech funding has been allocated to AI-related technologies, and in Q4 2024, more than 40% of insurtech funding was allocated to AI-driven transactions.

- The digital-first insurers’ operational cost is reduced by as much as 60%, while the time taken for claims processing is cut by 65%, customer satisfaction is raised by 25% and the customer retention rate is increased by about 30%.

- The number of usage-based insurance clients has increased by over 60%, peer-to-peer insurance clients by around 35%, and wearable devices now account for up to 40% of new health insurance products.

- The decline in global insurtech funding in Q2 2025 amounted to USD 1.09 billion, with Property & Casualty funding down sharply, while Life & Health funding almost tripled.

- The North American region continued to enjoy the premier spot in global insurtech activities, accounting for approximately 60% of total deals, followed by Europe (21%) and Asia-Pacific (16%).

- The top 10 global insurtech deals of Q1 2025 totalled US$1.1 billion, a 59% year-over-year rise, with the US at the forefront and new representation from regions such as Africa and Latin America.

- Almost 42% of US states have already enacted extensive data privacy laws, and approximately half have also established AI-related guidelines for the insurance sector.

- Regulatory sandboxes in countries such as the UK, Singapore, and Africa are opening the door to controlled innovation in the development of digital insurance models.

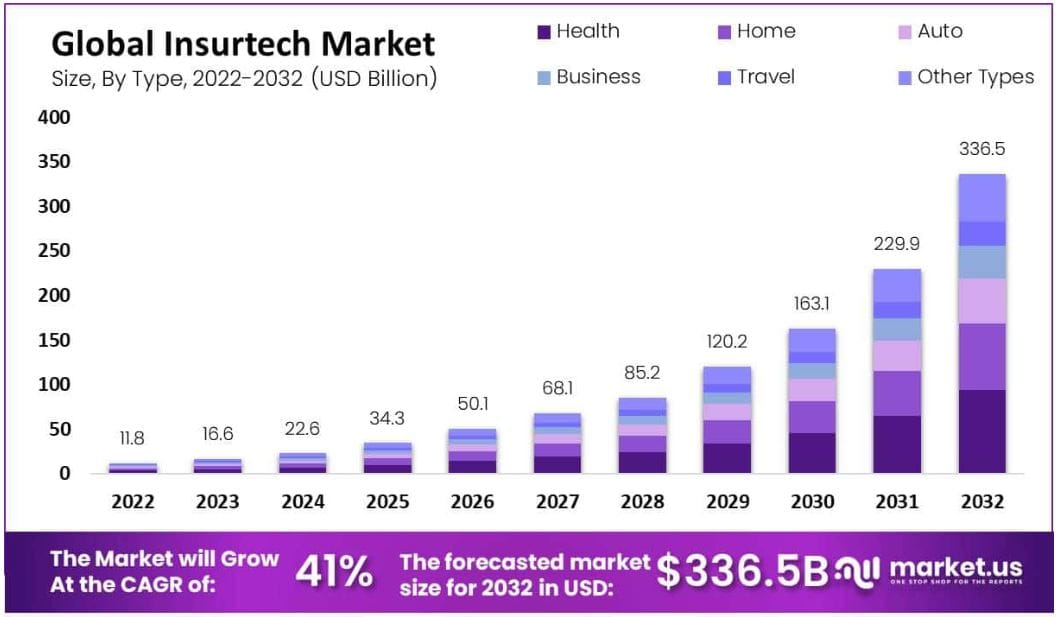

Insutrech Market Size

(Source: market.us)

According to market.us. The global Insurtech Market reached USD 16.6 billion in 2023 and is projected to grow to USD 336.5 billion by 2032, with a CAGR of 41.0% over the forecast period. The sector experienced a clear slowdown in funding activity in 2023, although technology adoption within insurance companies continued to rise steadily across major regions.

- It was observed that new insurtech funding fell to USD 916.71 million in the second quarter of 2023, reflecting a 34% drop from the previous quarter’s USD 1.39 billion.

- It was reported that cloud computing held a strong position, with a revenue share above 22.8% in 2022, as insurers relied on flexible, easy-to-deploy options to modernise operations.

- It was found that managed services accounted for more than 36% of total revenue, as insurers relied on external expertise to streamline processes and adopt new technologies.

- It was recorded that total insurtech funding dropped to USD 4.6 billion in 2023, marking the lowest level since 2017.

- It was reported that total funding declined 45% year over year from USD 8.3 billion in 2022.

- It was noted that 455 global insurtech deals took place in 2023, representing the lowest count in six years.

- It was indicated that Property and Casualty deals fell by 25% year over year, while Life and Health deals saw an even sharper decline.

- It was observed that early-stage deal values stayed stable at USD 3 million in 2023.

- It was recorded that early-stage deals accounted for 62% of all insurtech transactions, the lowest share in five years.

- It was highlighted that the United States accounted for more than 50% of global insurtech deals in 2023, regaining the leading position for the first time since 2020.

- It was projected that by 2024 more than 60% of insurance companies would adopt at least one insurtech solution.

- It was estimated that automated claims processing adoption would grow by 45% among insurers between 2022 and 2024.

- It was reported that around 55% of insurers planned to use insurtech tools for personalized recommendations and dynamic pricing by the end of 2024.

- It was projected that over 65% of insurtech platforms would support embedded insurance capabilities by 2024.

- It was anticipated that fraud detection and prevention solutions would grow by 40% among insurers between 2022 and 2024.

- It was expected that more than 60% of insurtech deployments in 2024 would include AI and ML for risk assessment and underwriting.

- It was noted that around 50% of insurers planned to deploy digital self service and customer engagement tools by the end of 2024.

- It was estimated that more than 70% of insurtech platforms would provide advanced data analytics and predictive models by 2024.

- It was projected that usage based insurance and telematics adoption would rise by 35% between 2022 and 2024.

- It was expected that over 55% of insurtech deployments would adopt blockchain for secure data sharing and smart contracts by 2024.

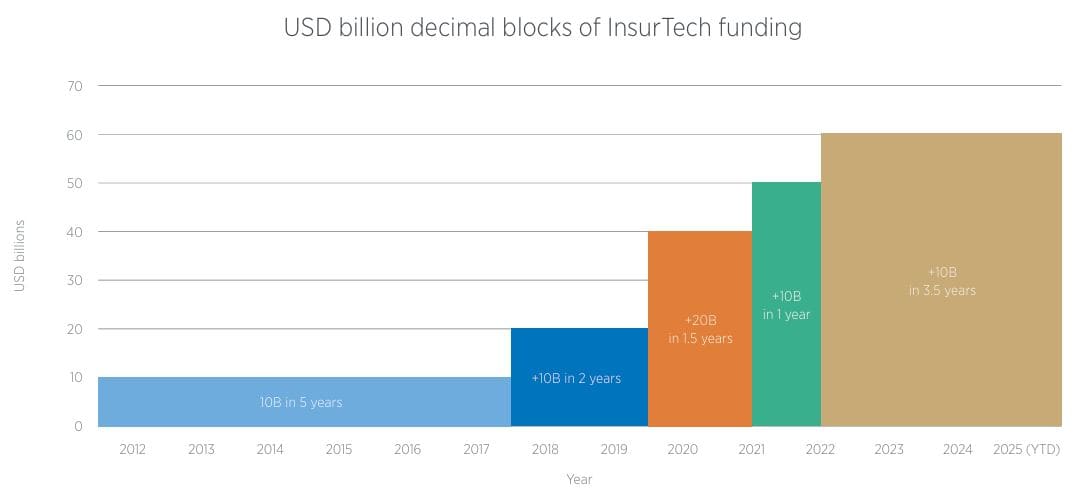

InsurTech & AI Investment Trends

(Source: ajg.com)

- If 2012 is taken as the starting point, the InsurTech industry took 5 years to attract its first US$10 billion in global funding.

- The next US$10 billion came in just two years, then US$20 billion more in only 18 months, meaning one and a half years of investment equated to the previous seven years of combined funding.

- After that peak, another US$10 billion was raised in just over a year, but the momentum slowed sharply, and it then took about three and a half years to raise the next US$10 billion, thus indicating a clear shift to more cautious investment.

- Of the US$60 billion invested in InsurTech, at least US$15 billion (25%) went to AI solutions.

- Just in Q4 2024, more than half of the world’s venture capital funding was attributed to AI companies, while 42% of InsurTech financing in the same quarter was specifically connected to AI-enabled transactions.

- In the first quarter of 2025, OpenAI raised nearly 31 times more funding than all InsurTech companies combined, indicating that capital is moving very much towards the future of AI.

- On the geographical front, the U.S. and Europe saw a rise in InsurTech deal volume in the first quarter of 2025, while only 4 deals were recorded in Asia.

- Silicon Valley investors accounted for 20% (1 out of 5) of all global InsurTech deals, and the region’s share of equity deals increased almost twofold to its highest point since the last quarter of 2023.

- Over 10% of InsurTech firms are located in California, further establishing the area as a global center for both InsurTech and AI.

Insurtech Vs Traditional Insurance

- Insurance platforms with a digital-first approach are far more efficient than those using traditional service models.

- By switching from manual to automated and AI-assisted processes, they can reduce operational and administrative costs by as much as 60%, enabling them to charge lower, very competitive prices.

- Automated underwriting and claims-processing systems alone cut the processing time by up to 65%, thus making the entire thing faster and user-friendly.

- Besides, they show up with more personalized services, owing to their access to customer data.

- Thus, the chances of their offering custom-made policies are three times those of traditional carriers.

- Consequently, customer satisfaction is about 25% higher, and retention rates are about 30% higher.

- Completely digital operations not only save costs but also promote eco-friendly business practices, while the integration of risk assessment tools has halved the divide between insurers, thereby cutting expenses.

Insurtech Change Through Innovations

- The description, sale, and administration of insurance products are all being changed by the new technologies.

- The upswing in the use of blockchain in insurance has been tremendous, with the market value estimated at US$3.11 billion in 2025, up from US$1.94 billion in 2024, driven by secure data handling and automated processes.

- Insurers are deploying smart contracts not only to ease policy issuance but also to tackle fraud by making it less opaque.

- Besides, around 20% of both property and auto insurance is governed by IoT technology, including smart home appliances and car telematics that keep insurers in the loop of real-time risk.

- The number of usage-based insurance models has exceeded 60% in 2025, with premiums based on customers’ actual behaviour rather than average usage.

- Also, peer-to-peer insurance coverage models are rising by almost 35% as customers are searching for risk-sharing among others.

- In the medical field, wearable tech affects around 40% of new health insurance products by both rewarding the insured for adopting healthier habits and helping the insurer with more accurate pricing.

- On the whole, data analysis driven by AI has the potential to raise customer engagement by 45% by providing them with more relevant and personalized insurance experiences.

The Average Salary In The Insurance Industry

- Salaries in the insurance industry give the impression of considerable disparity in earnings levels.

- The largest income group comprises almost 39% of workers who earn between 22.5k and 44.5k dollars yearly.

- Next are 20% of employees who earn between 44.5k and 66.5k, and then 15% who earn between 66.5k and 88.5k annually.

- The upper management, specialized underwriting, data, and executive positions are among the roles that the remaining 20% of the workforce earns US$88,500 or more, thus reflecting higher-paying roles.

Adjustments In Legal And Regulatory Environment

- The changing legal and regulatory environment for insurance and insurtech is getting more complicated and organized, mainly due to concerns regarding data, AI, and cybersecurity.

- By the middle of 2025, almost 42% of U.S. states had passed comprehensive data privacy laws, bringing the country closer to the global privacy standards that nearly 79% of the world’s population currently enjoys.

- The practice of regulatory sandboxes is becoming more widespread in places like the UK, Singapore, and certain parts of Africa, enabling patient product trials under regulators’ supervision.

- Around half of the U.S. states, New York, Colorado, and Connecticut, have started giving out the guidelines concerning the use of AI in the insurance sector, and regulators are also conducting frequent reviews of AI systems during market conduct examinations.

- At the same time, the strictest cybersecurity and data protection measures are being implemented worldwide.

- Moreover, anti-fraud and consumer-protection laws are heavily influenced by evolving regulatory models, such as the EU’s Digital Operational Resilience Act (DORA).

- Consequently, this entangled web of state, federal, and international regulations is making it harder for insurtechs to meet compliance requirements if they want to enter or grow in global markets.

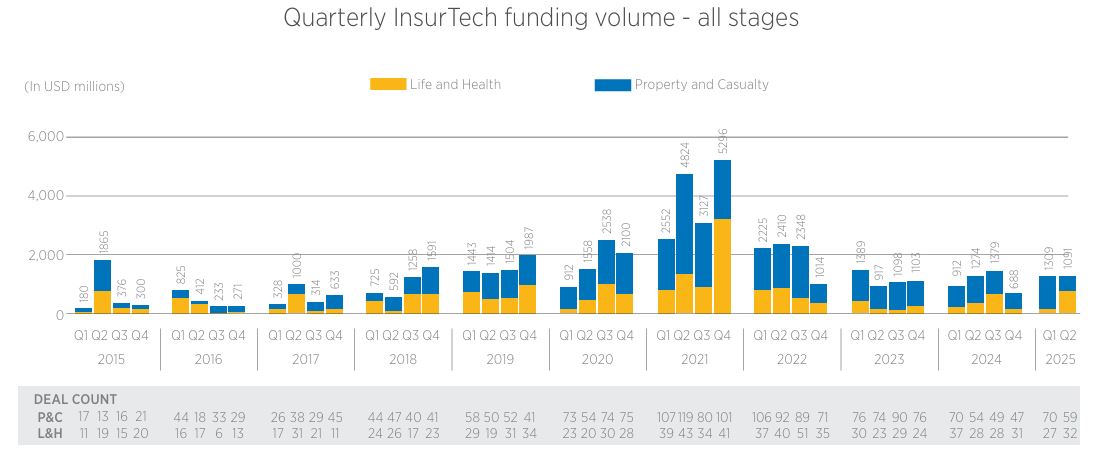

Insutech Quarterly Funding

(Source: ajg.com)

- The report indicates a significant global InsurTech funding dip in the second quarter of 2025, while a couple of emerging segments still exhibit strong performance.

- The total amount of global financial investments in the InsurTech sector fell 16.7% from the previous quarter to USD 1.09 billion.

- The Property and Casualty (P&C) sector was the most affected by the funding cut and has witnessed the lowest level of backing since Q1 2018.

- They could raise only USD 362.22 million, marking a steep 68% decline from the previous quarter.

- P&C companies accounted for only two of the top ten deals; as a result, the average P&C deal size fell by an astonishing 66.7% to USD 6.35 mil, a mark not seen since the first quarter of 2014.

- On the other hand, L&H InsurTechs have played it robustly. Their funding increased almost threefold, reaching USD 728.47 million, which is the highest level since Q2 2022.

- The quarter’s four biggest deals were all assigned to L&H companies, which included Gravio, Bestow, Chapter, and Empathy.

- This raised the average L&H deal to USD 26.02 million, and the number of L&H deals went up from 27 to 32.

- At the same time, early-stage InsurTechs were improving their position, having acquired USD 259.7 million and coming out of a near five-year low, where the specific rise in early-stage L&H funding was phenomenal.

Regional Distribution Of Insurtech Funding

(Reference: coinlaw.io)

- The data depicts how, throughout the second quarter of 2025, global insurtech investment activity was spread across the regions.

- The North American region is seen as the global leader, accounting for approximately 60% of all insurtech deals. This corresponds to the strong presence of venture capital in the region, the well-developed startup ecosystem, and the ongoing push towards digital innovation in the insurance sector.

- At around 21%, Europe retains the second-largest share, which indicates that the continent is still a major center for insurtech development and investment.

- The Asia-Pacific region is next to Europe, accounting for around 16% of global deal activity, with approximately US$22 million in total funding spread across 10 deals. This implies rising demand for tech-based insurance solutions, though total funding remains below that of North America and Europe.

- The insurtech market in Latin America is becoming increasingly active, but the latest reports show that investment volume remains modest.

- The insurtech market in Africa is still very young, and 2025 will not provide many public investment figures, which simply indicates a growing but underdeveloped ecosystem.

- The Middle East, on the other hand, is slowly becoming a focal point for digital health and travel insurance solutions, but reliable funding numbers for 2025 are still not widely reported.

- The global insurtech environment shows regional differences: North America and Europe are the principal players in deal activity, Asia-Pacific is consistently rising, and the rest of the world lags behind.

- Cross-border collaboration, especially between the US and Europe, continues to foster international growth, though the detailed metrics of these partnerships are still not fully shared.

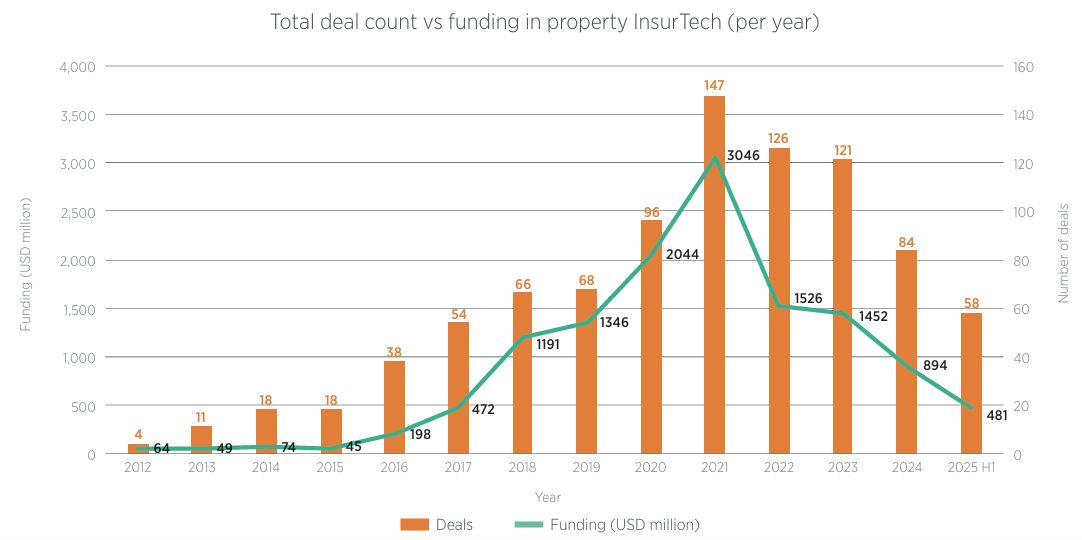

Annual Investment Into Property Related To Insurtech

(Source: ajg.com)

- Regarding investment activity, Anthemis is the most active investor with 26 transactions, followed by Y Combinator with 24 and Plug and Play Ventures with 22.

- MetaProp has been involved in 15 property InsurTech transactions, while Ribbit Capital and Hudson Structured Capital Management are behind each with 13.

- True Ventures is next with 12 deals, and Nationwide Ventures, Clocktower Technology Ventures, and Flourish Ventures have 11 transactions each, which indicates a competitive group of investors backing property-focused InsurTech startups.

- Next Insurance is the top company in terms of total capital raised, with around USD 1.15 billion.

- It is then followed by Hippo, which has approximately USD 709 million from a variety of sources.

- The amounts raised by PayMaya and Cambridge Mobile Telematics are each just above USD 500 million, being USD 503 million and USD 502.5 million, respectively.

- Lemonade has amassed a staggering USD 480 million in funding, with Digit Insurance being the next one at USD 479 million.

- Then comes ICEYE with a total of about USD 458.73 million, Kin with USD 453.09 million, and finally two companies, Openly and Ethos, with their USD 430.77 million and USD 413.96 million rounds, respectively.

- All these numbers give us a very close look at the property InsurTech ecosystem, where capital and investors have concentrated their activities.

Top 10 Insutech Deals Worldwide

(Source: fintech.global)

- The global InsurTech industry wowed everyone with its impressive funding in the first quarter of 2025, raising US$1.1 billion across 58 deals.

- This represented a strong recovery from US$718 million raised through 65 deals during the same period in 2024.

- Thus, there is a 59% year-on-year increase in funding even though the number of transactions declined a little.

- The fact that the capital invested went up even with fewer transactions shows that the market is moving towards larger investment rounds, and there might be a trend among investors towards established or high-potential InsurTech companies.

- The activity in terms of deals has slowed down, but the big increase in funding points to the investors coming back with confidence.

- One factor likely to foster such confidence is the growing interest in digital transformation and embedded insurance solutions.

- The U.S. not only held on to its top position in the global InsurTech market but also took five of the ten highest deals for the quarter.

- The U.K. did likewise, taking its share of the top deal from one in Q1 2024 to two in Q1 2025, hence cementing its position as Europe’s leading InsurTech hub.

- Some of the countries that were widely mentioned in Q1 2024 — like Germany, Indonesia, the Netherlands, and Cyprus — were nowhere to be seen in the top ten list of countries in Q1 2025.

- However, new entrants such as South Africa, Brazil, and Puerto Rico indicate that the trend of major InsurTech investments is no longer confined to traditional centres but is spreading to a broader geographic area.

- One of the remarkable deals was that a South Africa-based, AI-enabled digital insurance platform named Naked raised a US$38 million Series B2 round.

- This was the only African company to feature in the global top ten deals of the quarter.

- The round welcomed investment from the global impact firm BlueOrchard, which has always supported the company, as well as from Hollard, Yellowwoods, IFC, and DEG.

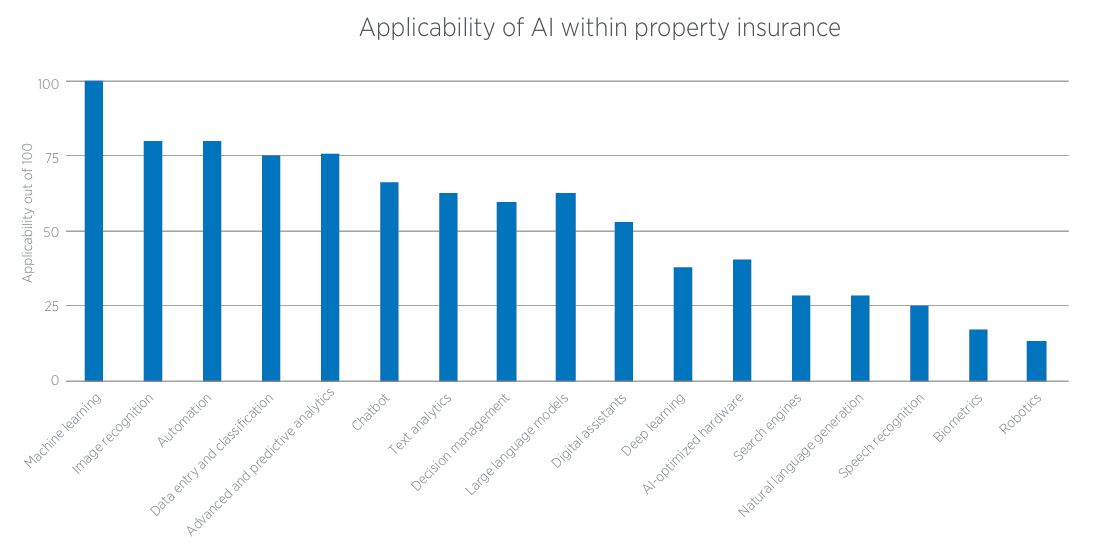

Applicability Of AI In Insutrech

(Source: ajg.com)

- The figure above shows that AI is slowly but surely becoming a necessity in property insurance, especially for detecting counterfeit claims.

- A continuous poll of InsurTech and AI professionals indicates that out of all the AI tools, machine learning, image recognition, plus automation are the ones that hold the greatest promise in this area.

- The aforementioned technologies, coupled with AI’s traditional strengths such as pattern recognition and data processing, are making fraud detection not only faster but also more precise and coordinated than traditional methods.

- AI-driven technology is able to interpret an enormous amount of data, take care of monotonous jobs with no human intervention, and discover hidden patterns in both past and unorganized data.

- Consequently, it can dramatically minimize false alarms and enhance the detection of genuine fraud situations in comparison with non-AI methods.

- The AI intervention in claims processing may involve steps such as scanning and assessing claim documents, matching them with the known fraud trail, and conducting facial recognition and biometric verifications as identity checks.

- Overall, the article accentuates that AI is changing the whole claims processing and fraud prevention dynamics in the insurance sector.

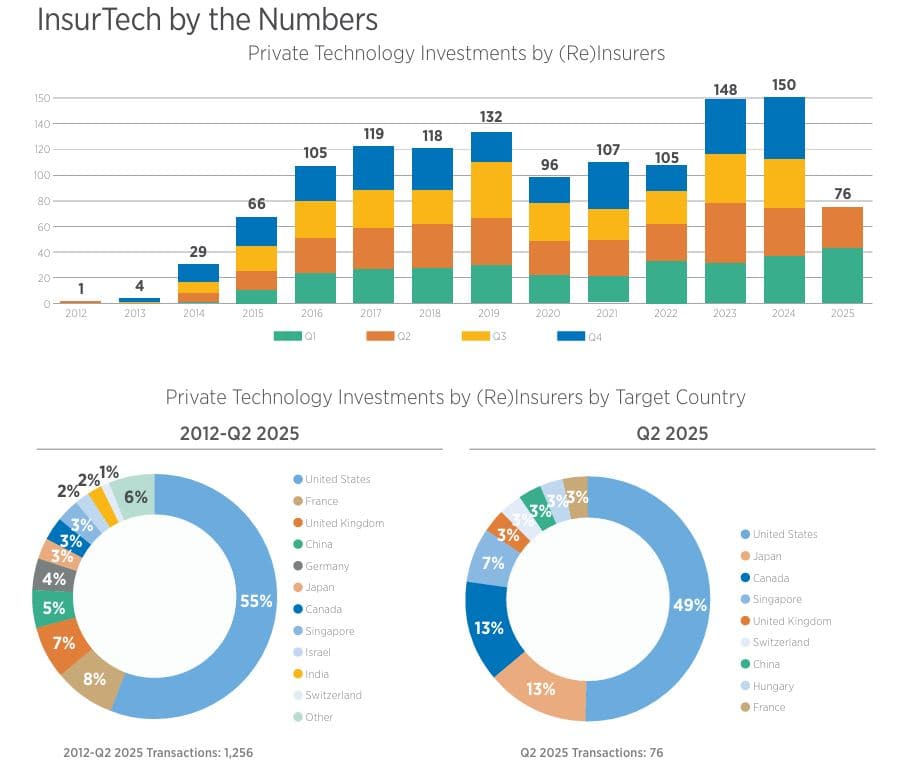

InsurTech Investment Trends And Distribution (2012–Q2 2025)

(Source: ajg.com)

- The above chart emphasizes that the private technological investments of the reinsurers and insurers have significantly increased in number since 2012, with the deal turning from almost nothing in the early years to more than 100 deals per year during the late 2010s and early 2020s.

- In 2024, investment volume hits an all-time high of around 150 transactions, then declines to 76 by 2025 (so far), which could point to a slowdown or to the year still being active.

- The yearly distribution of deals was such that for most of the time, the deal-making was similar in all quarters, but Q2 and Q3 were mostly the periods when a significant portion of total deals occurred.

- Geographic insurance investment trends, with the United States leading at around 55% of all transactions, have continued from 2012 to Q2 2025.

- The other countries that follow are France, the United Kingdom, China, Germany, and Japan, each with a very small single-digit share.

- Even in Q2 2025, the United States continues to be the leader with around 49% of the total transactions, but Japan and Canada have made noticeable strides in their respective positions, each contributing approximately 13% of the total, while the other countries, like Singapore, the UK, Switzerland, China, Hungary, and France, together form a smaller part.

- This suggests that, though the US remains the main market, the investment is slowly becoming more geographically diverse.

- Over the entire investment period, Series A rounds, which accounted for the largest share, received 28% of the total, followed by Series B (23%), Seed/Angel (11%), and Series C (11%), with Series D and later-stage funding accounting for smaller proportions.

- By the time we get to Q2 2025, the focus has been very clear on the mature companies, as Series B and A funding types dominate at 42% and 32%, respectively, while Seed/Angel drops to just 10%.

- This suggests that insurers and reinsurers are increasingly prioritizing scaling and proven InsurTech solutions rather than very early-stage startups.

Emerging Economies’ Untapped Potential

- By 2025, the legal and regulatory framework that governs the insurtech and digital insurance will be firmly in place and will be more demanding than ever.

- In the United States, data privacy laws have been enacted in around 42% of states, indicating a significant move towards enhanced personal data protection.

- This is part of a global trend: privacy regulations now affect almost 79% of the world’s population, and companies are consequently forced to implement stricter data-handling practices.

- Moreover, Governments and regulators are also supporting innovation in a controlled manner through regulatory sandboxes, especially in the UK and Singapore, and now also in Africa.

- These sandboxes allow the testing of new insurance technologies under regulatory supervision, thereby easing associated risks and enabling growth.

- Almost 50% of U.S. states, including major ones such as New York, Colorado, and Connecticut, have begun setting rules for AI.

- It is expected that these guidelines will be part of market conduct examinations, meaning insurers will have to explain and justify how they incorporate AI into their decision-making processes, such as underwriting and claims handling.

- Simultaneously, the world is witnessing tougher cybersecurity and data privacy regulations.

- There are new federal and state requirements in the U.S., along with increased enforcement, which means companies are under more scrutiny and face higher penalties for non-compliance.

- Furthermore, anti-fraud and consumer protection laws are becoming more transparent and are placing operational resilience at the forefront, influenced by international frameworks such as the EU’s DORA.

- The insurtech companies found themselves in a difficult compliance situation due to overlapping state, federal, and international requirements, which even compelled them to enhance their legal, risk, and compliance functions, thereby increasing their operating costs.

Recent Developments

- The insurtech sector has witnessed a flurry of activities, including mergers and acquisitions, new product launches, rounds of financing, and technological advancements in the past few years.

- The beginning of 2023 saw Swiss Re paying US$250 million for Zipari, a health insurance customer experience platform, with the goal of enhancing its digital capabilities and engaging customers with the help of advanced analytics and AI.

- Simultaneously, Munich Re also acquired TechAssure for US$150 million, reportedly to enhance its technology-oriented insurance solutions and to penetrate the digital insurance market.

- Some businesses have also introduced new products in response to changing customer demands.

- In the first quarter of 2024, Lemonade launched an auto insurance product that employs artificial intelligence and behavioural data to offer competitive rates and a less intrusive consumer journey with quicker claim handling and personalized plans.

- Next Insurance launched a workers’ compensation policy in 2023 for small businesses, offering flexible coverage, instant quotes, and an easier online claims process.

- Funding events have been major contributors to the growth and innovation of companies.

- Hippo Insurance secured US$350 million in a Series E round in 2023 to expand its product range, enhance its technology, and enter new markets.

- Policygenius, like this, managed to raise US$125 million in funding at the beginning of 2024 to improve its existing technology, hire more customer support staff, and develop new tools for comparing and buying insurance.

- AI and machine learning are gradually becoming major players in underwriting, enabling insurance companies to conduct the most accurate risk assessments, achieve the quickest policy approvals, and detect fraud most effectively.

- Besides that, the use of blockchain technology in claims processing aims to make the process more transparent, secure, and efficient, thereby enabling faster, more reliable transactions.

- On the regulatory side, the digital change is not leaving the governments and industry bodies behind.

- The European Union enacted its Digital Insurance Directive at the beginning of 2024 to foster innovation while also securing data and consumer trust.

- In the U.S., the NAIC published updated guidelines in 2023 to oversee the use of artificial intelligence and big data in insurance, prioritising ethics, privacy, and consumer protection.

- Not only are the research and development efforts limited to existing markets, but also going to newer areas.

- Through data collected from connected devices like smartphones and vehicle sensors, telematics based insurance is getting more personalized, allowing for usage-based policies.

- Moreover, the researchers are developing more advanced cyber insurance solutions to help businesses cope with the risk of digital attacks, providing wider coverage, better risk assessment, and faster incident response.

Conclusion

Insurtech Statistics: InsurTech no longer exists merely as a niche segment but rather is a fundamental element of the current insurance ecosystem. The transition of the sector from traditional ways of operation to more efficient, data-oriented and customer-centric models can be seen through the huge market growth projections, the rise of investment in AI-powered solutions, and so on. The funding situation has become tougher, but the more prominent and mature companies are the ones who get the most support, a sign of strength in scalable digital solutions.

The industry is further fortified by geographic expansion, regulatory changes, and cutting-edge technologies such as telematics, blockchain, and advanced machine learning. The insurtech would continue to be a major contributor in terms of articulating a smarter, quicker as well as a more customized insurance experience for the worldwide businesses and consumers as long as there is innovation and the risk environment keeps changing.

Sources

FAQ.

The major contributors are the increased reliance on digital technologies, hefty investments in AI and automation, sophisticated data analytics, and the use of embedded and usage-based insurance models. All these advanced technologies lead to increased efficiency, reduced costs, and more customized products; hence, global demand is accelerated.

AI is revolutionizing underwriting, claims handling, and fraud detection, the most significant areas of insurance tech. The likes of machine learning and image recognition tools enable insurers to detect fraud more accurately, speed up the claims process, automate repetitive work, and adjust pricing to each individual customer, resulting in better customer experience and lower costs in operations.

Investment in insurtech worldwide is going up, with North America leading in terms of the money put into it. The United States have about 60% of this market, Europe is second with 21%, and finally comes the Asia-Pacific with 16%. New players have started making an entrance in Africa and Latin America, but the United States continue to be a strong hub.

Insurtech companies use digital-first platforms to lower operational costs by as much as 60% and streamline claims processing by around 65%. They provide more personalized products, are loved more by the customers, and are more adaptive and efficient than traditional insurance companies.

Regulations on data privacy, AI usage, and cybersecurity are tightening. Around 42% of U.S. states have enacted comprehensive data privacy laws, with many introducing AI-related guidelines. Regulatory sandboxes and international frameworks, such as the DORA within the EU, dictate which ways insurtech firms may operate and innovate safely.

Joseph D'Souza founded ElectroIQ in 2010 as a personal project to share his insights and experiences with tech gadgets. Over time, it has grown into a well-regarded tech blog, known for its in-depth technology trends, smartphone reviews and app-related statistics.