Altcoin Market Statistics: Why Most Tokens Fail While Others Grow

Updated · May 20, 2026

Table of Contents

Scroll through CoinMarketCap on any given day in 2026 and you can watch the number of active tokens tick upward in real time. Yet for every fresh symbol blinking green, another quietly flat-lines. In 17 years, crypto evolved from an open-source curiosity into a $2.7 trillion asset class. Along the way, something both astonishing and brutal happened: more than half the coins ever minted have already died. Data-driven investors now want answers rooted in measurable reality rather than influencer hype. Where exactly is the statistical fault line between a token that collapses inside a month and one that compounds for years? We’ll unpack that question, moving systematically from raw failure counts to survivorship traits, then to regulation’s filtering effect, and ultimately to what an altcoin portfolio designed for 2026-2027 might look like.

From Hype to Hard Numbers: The 2025 Token Mass Extinction

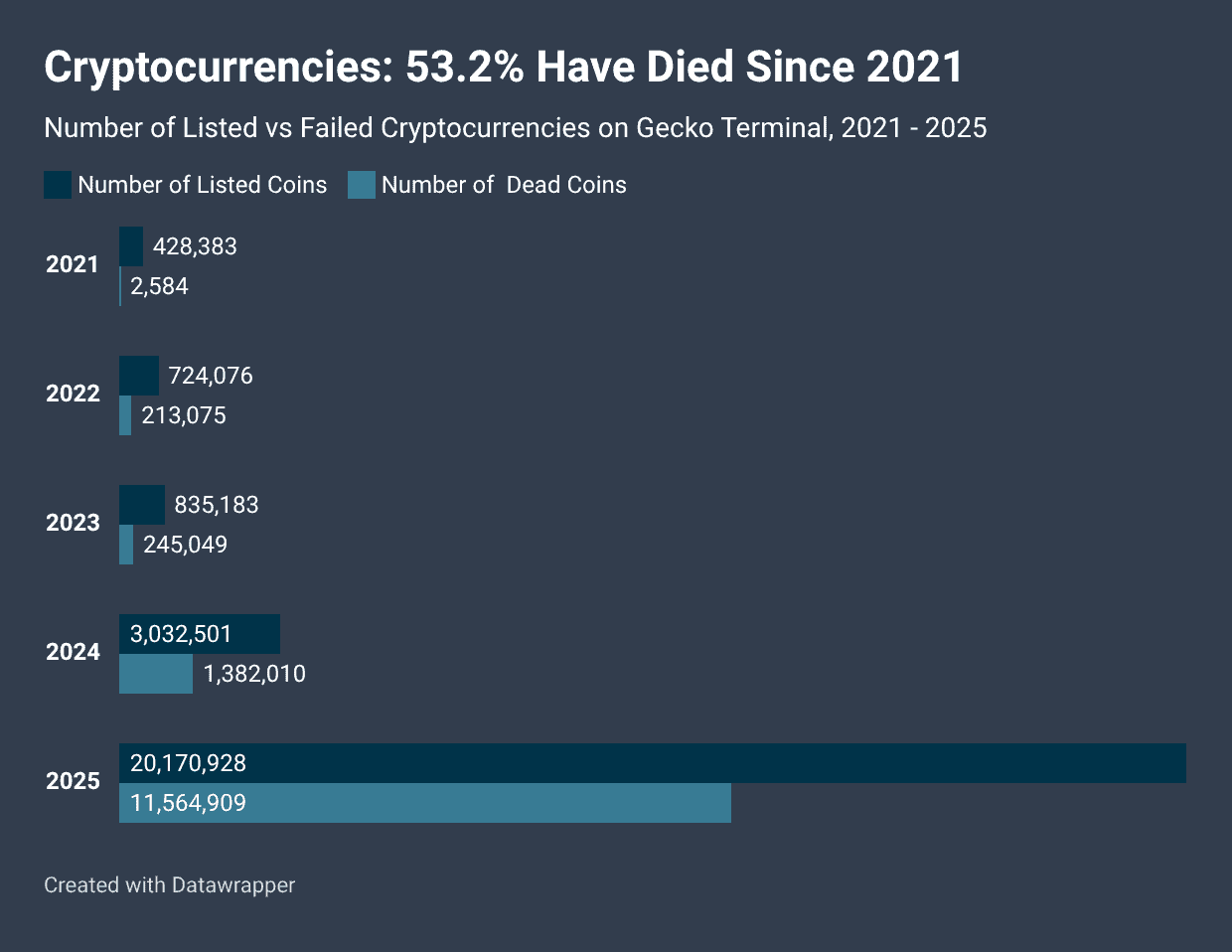

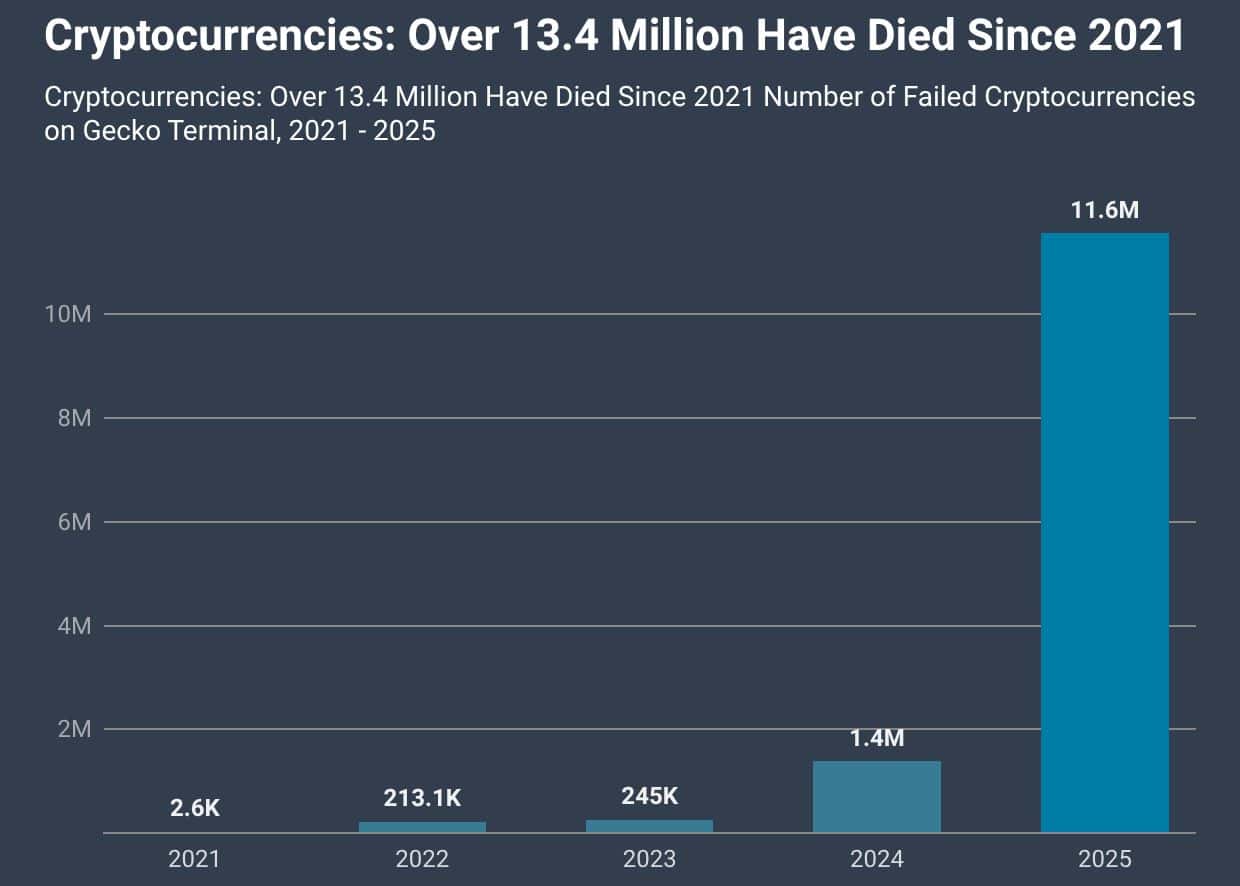

Topics like Verasity price forecast remain one of the top crypto community topics, proof that hope springs eternal. But the data behind token survivability is unequivocal. CoinGecko’s 2026 report shows that 53.2% of all cryptocurrencies ever listed on GeckoTerminal are already extinct, with an eye-watering 11.6 million failures logged in 2025 alone. Put differently, nearly nine out of ten dead tokens met their fate in a single calendar year. The October 10, 2025, cascade of liquidations resulted in the destruction of $19 billion in leveraged positions and led to 7.7 million project shutdowns, particularly in the fourth quarter of 2025.

Those numbers reverberated well beyond niche Telegram chats. Bitcoin dominance dropped from 65.1% in June 2025 to 56.7% by September, rotating massive capital into altcoins. The market had discovered the difference between scarcity and saturation, and saturation clearly won.

Many newcomers still ask whether they can buy Solana with credit card directly, avoiding the paperwork normally tied to centralized exchanges. Yes, they can. Over the past year, ramp providers have embedded instant card-to-SOL flows into Solana Pay and Phantom. The result is that a user in Paris can enter a €250 Visa transaction and receive native SOL in less than a minute. From a survivability perspective, frictionless fiat on-ramps expand the token’s buyer base, deepen liquidity, and reduce slippage during drawdowns – features that statistically correlate with longer life spans for any L1 or L2 network token.

That brings us to the most uncomfortable chart in crypto. By 2025, the total number of listed crypto projects surged past 20.2 million, yet daily altcoin spot trading volume eventually collapsed to roughly $26.5 billion. The oversupply ratio has never looked worse. In equity terms, imagine millions of penny stocks listing on Nasdaq while dollar turnover plummeted. Price discovery breaks, making crashes inevitable. That is precisely what occurred in 2025, when a record 11.6 million tokens collapsed.

Why Do Half of All Altcoins Die? The Three Statistical Killers

A token’s obituary rarely lists a single cause of death; instead, multiple pathologies converge. Still, three quantitative killers appear again and again in post-mortems.

Oversupply and Meme Mania

Before low-code launchpads like Pump.fun or Solpad, token launches required developer chops, community buy-in, and often six-figure audits. The barrier acted as a quality filter. But by Q3 2025 anyone with 50 USDC could mint a meme coin in minutes. That democratization was exciting – right up until millions of near-identical coins competed for the same finite liquidity pool.

To visualize how oversupply crushes price stability, consider the following stylized math. If every one of the 20 million 2025-vintage coins hoped for just $10,000 in liquid demand, the market would need $200 billion of incremental capital, roughly the size of all non-top-10 altcoins combined. Absent that capital, order books hollow out, spreads widen, and price volatility skyrockets. Projects that don’t provide real utility or revenue streams quickly see depth dry up and charts flatline to zero.

Below is an illustrative list of supply-side accelerants that fueled the extinction wave. Notice how they span technology, psychology, and market structure:

- No-code launchpads that removed technical hurdles.

- Viral meme templates that let any creator “reskin” a dog coin in an hour.

- Airdrop farming guilds dumping tokens immediately after snapshot claims.

- Liquidity pool incentives funded with new token emissions rather than earned revenue.

- Social media algorithms that rewarded outrageous price targets over sober analysis.

The first three points magnified token count; the last two eroded buy-side conviction. Together they formed the perfect storm. And as we’ll discuss later, regulators barely flinched until the carnage was already historic.

Liquidity Evaporation

CryptoQuant’s buy/sell delta shows ex-BTC/ETH altcoin selling pressure hit – $209 billion over 13 months – the most extreme negative reading in five years. That delta became a gravity well pulling small-cap charts downward. Even tokens with promising technology couldn’t escape because each new sell wall forced market makers to widen spreads, scaring off fresh entries.

Order-book analytics confirm the spiral. During the worst week of October 2025, the average 2% depth on 1,200 micro-caps fell below $20,000. At such a low depth, a single six-figure sell order can nuke the price 50 percent. Retail holders, seeing red candles without obvious news, panic-sold, worsening the gap. Eventually dev teams abandoned Telegram channels, websites went offline, and the chain explorer links turned into 404 pages.

Dangerous Tokenomics

Structural design flaws sealed the fate of many 2025 launches. Stacy Muur famously called it “short-volatility token engineering.” Coins opened with sky-high, fully diluted valuations, but only 3-5% of the supply floated in the market. Early investors or insiders held the rest under six-month lockups. As growth projections evaporated, cliffs hit, and float ballooned right as demand vanished. The result was a guaranteed supply shock – only in the wrong direction.

Staking incentives compounded the problem. Many protocols promised triple-digit APYs paid in their own token. Those rewards acted like perpetual secondary offerings, diluting holders daily. Without external fee revenue, stakers simply printed more claim tickets on an asset that fewer traders wanted each week.

Blueprints for Survival: What the Data Says About Winning Tokens

While millions of coins vaporized, a statistically significant minority not only survived but posted triple-digit returns. The difference was never luck; it was measurable fundamentals.

Real-World Asset (RWA) Tokenization

Put a boring yield onto a flashy blockchain, and magic happens. The RWA sector ballooned to $30.2 billion by Q2 2026, a 420% surge in just 16 months. Tokenized T-bills from Ondo Finance and BlackRock’s BUIDL fund gave cash-rich DAOs a regulated 5% yield without leaving the chain. Because redemptions settle into the same legal wrapper as issuances, these tokens trade close to NAV, reducing volatility and inviting bigger market-making books.

Interestingly, RWA issuers also generate off-chain cash flows – transfer agent fees, origination spreads, or custody charges. That revenue lets teams buy back and burn tokens or fund real operations, breaking the dependency on inflationary incentives. Survival odds climb as a result.

Layer-2 and DeFi 2.0

Ethereum gas prices were around $5.90 in early 2024 but in 2025, users were paying only pennies on rollups such as Arbitrum. This efficiency was seen by both users and liquidity. In the 2025 Half-Year Report, Token Terminal projects that optimistic rollups continued to dominate the market, with Arbitrum and Base showing promise in terms of fee generation, demonstrating that the fundamental value has prevailed over the market hype.

Developer mindshare acts like a leading indicator. More builders create more dApps, which grow on-chain activity, which drives fee revenue, completing a flywheel that makes token inflation sustainable. Projects missing any link in that loop rarely last two cycles.

AI-Native Chains

When NVIDIA crossed $2 trillion, AI tokens rallied, but only those with provable machine learning utility kept their gains. Bittensor was the first to introduce pay-per-inference markets, where model owners are rewarded for accurate predictions. Quarterly AI revenue was about $43 million by early 2026. Because rewards come from external demand (developers paying for inference), emissions funded by block subsidies shrink as a share of total token flows, a dynamic that tempers sell pressure.

For investors using DCF-style models, fee reliability matters. AI-integrated chains delivered that reliability, which is why RNDR, FET, and AKT notched 3-5x rallies even as meme caps imploded. The market rewarded actual utility over narrative alone.

Regulation as a Filter, Not a Foe

To a 2019 crypto OG, ‘regulation’ is a dirty word. By 2026, it’s a protective moat. The July 2025 GENIUS Act imposed 1:1 stablecoin reserve requirements and created the PPSI license. Certain that on-chain dollars wouldn’t break the buck, institutional allocators reopened risk budgets, driving BTC and ETH volatility down nearly 20% within six months.

That stability spilled over – selectively. The new taxonomy and the March 2026 SEC-CFTC joint interpretation drew a demarcation line. Tokens meeting commodity criteria (decentralized, no managerial “efforts of others”) gained exchange listings and custody solutions from regulated brokers. Tokens resembling securities faced delistings and legal headwinds.

Regulators worldwide have enacted policies that fall into several practical buckets. Understanding which bucket a token occupies is a prerequisite for estimating whether liquidity will deepen or disappear:

- Passportable compliance regimes (EU MiCA) that automatically allow trading across all member states once a single license is secured.

- Prudential reserve mandates (U.S. GENIUS) compelling issuers to hold low-risk collateral against circulating supply.

- Commodity classifications (SEC/CFTC Joint Interpretation) that pre-clear specific tokens for futures and spot ETF inclusion.

- Safe-harbor exemptions for micro-cap experimentation (Singapore’s Regulatory Sandbox Plus) limiting retail exposure but accelerating institutional pilots.

Projects aligned with the first three buckets saw spreads tighten after rules took effect; those stuck outside saw market makers withdraw. In 2025, tokens delisted for compliance risk lost on average 72% of market cap within thirty days, according to Bitwise tracking. That statistic alone explain why many teams now hire policy counsel before hiring solidity engineers.

Regulation’s filtering isn’t only punitive. Explicit requirements on disclosures and reserves decrease the information gap and thus the risk premium that more advanced desks require. The lower risk premiums correspond to less volatility, and consequently lower option prices and more liquidity – the virtuous mirror image of the 2025 extinction spiral.

Looking Ahead to 2027: A Market That Finally Rewards Fundamentals

With half the field already culled, the survivors face a less crowded but more scrutinizing marketplace. Sell-side research is beginning to resemble equity coverage: discounted cash-flow projections for protocol fees, sensitivity tables for validator rewards, and sum-of-the-parts analysis for modular chains. The days when a clever dog meme could 50-× on social media virality alone are fading.

One demographic shift further tilts the field toward fundamentals: Gen Z. Having grown up on Venmo, Revolut, and one-tap Apple Pay, these investors expect FIAT on-ramps as smooth as the credit-card-to-Solana flow we discussed earlier. A 2026 Morning Consult survey revealed that 90% of consumers do not currently own stablecoins, and 80% have never owned them at all. L1s or L2s that solve this UX bottleneck may capture the next billion wallets.

In the meantime, the venture is turning a corner. The Q1 2026 crypto VC funding totaled $5 billion, with infrastructure and stablecoin platforms seeing a significant preference compared to retail speculation, per DefiLlama data. Due to the nature of capital, tokens related to throughput, compliance or real-world yields are now valued at higher multiples.

For the pragmatic investor assembling a 2026-2027 altcoin basket, a data-backed checklist could look like this:

- Does the project generate non-inflationary revenue today?

- Is that revenue denominated in a stable reference asset rather than its own token?

- What percentage of supply is already circulating, and how steep are future unlock cliffs?

- Does the token fall under a friendly regulatory category (commodity, PPSI-linked stablecoin, etc.)?

- Are there at least two independent market makers providing double-digit million-dollar daily depth?

- Is developer activity trending upward in the last six months, as measured by GitHub commits or full-time contributors?

Passing five of these six tests doesn’t guarantee moonshots, but statistically it avoids 90% of the traps that claimed those 11.6 million failed tokens. The point is not perfection; it’s survivability.

Armed with that framework, investors can filter noise from narrative. For example, if a new AI chain promises 1,000x upside but fails the non-inflationary revenue test, it’s likely a rerun of 2025 playbooks. Conversely, a mid-cap RWA issuer with only modest social buzz but strong regulatory standing and on-chain cash flows may offer asymmetric upside with drastically lower downside.

Conclusion

Altcoin history used to be authored by meme lords; in 2026 it is increasingly co-written by accountants and policymakers. The statistics speak louder than any influencer clip: oversupply, liquidity evaporation, and untenable tokenomics annihilated millions of projects in record time. At the same moment, tokens tied to real-world yield, scaling infrastructure, or AI-backed utility drew fresh institutional capital and survived. Rather than suffocating innovation, regulation acted as a sieve, one that strains out under-collateralized gimmicks while channeling capital toward builders with durable roadmaps.

The next alt-cycle will probably feel slower, almost boring at times, because sustainable growth always does. That boredom is a feature, not a bug. When the market finally rewards fundamentals – cash flow, compliance, and community utilit – investors who still rely on gut feel will be outpaced by those armed with spreadsheets and legal cheat sheets. By internalizing the failure math and the survival blueprint laid out here, you’ll stand a better chance of compounding through whatever headlines the next two years throw at the digital-asset frontier.

Sources

Aruna Madrekar is an editor at Smartphone Thoughts, specializing in SEO and content creation. She excels at writing and editing articles that are both helpful and engaging for readers. Aruna is also skilled in creating charts and graphs to make complex information easier to understand. Her contributions help Smartphone Thoughts reach a wide audience, providing valuable insights on smartphone reviews and app-related statistics.