Cross-Border Payment Statistics By Market Size, Region and Technology (2025)

Updated · Nov 04, 2025

Table of Contents

- Introduction

- Editor’s Choice

- General Statistics

- Cross-Border Payment Market Size

- Global Cross-Border Payment By Region

- Top Technologies To Solve Cross-Border Payment Problems

- Main Types of Cross-Border Payments

- Wholesale Cross-Border Payments Market Size

- Retail Cross-Border Payment

- Demand From Consumers To Increase Cross-Border Transactions

- Technological Innovations

- Regulatory Landscape

- Recent Developments

- Conclusion

Introduction

Cross-Border Payment Statistics: Cross-border payments refer to the transfer of money across national borders – something that covers everything from the remittances that migrants send home to invoices issued to other businesses, to online purchases made from a foreign website.

This year saw remarkable cross-border payment growth, with major facilitators changing the landscape: In many countries, remittances reached record levels; non-bank money transmitters have gained a lot of market share in small P2P flows; and the industry has been pushing for cheaper, faster, and more transparent rails.

This article provides a summary of the key cross-border payments statistics and trends in 2025.

Editor’s Choice

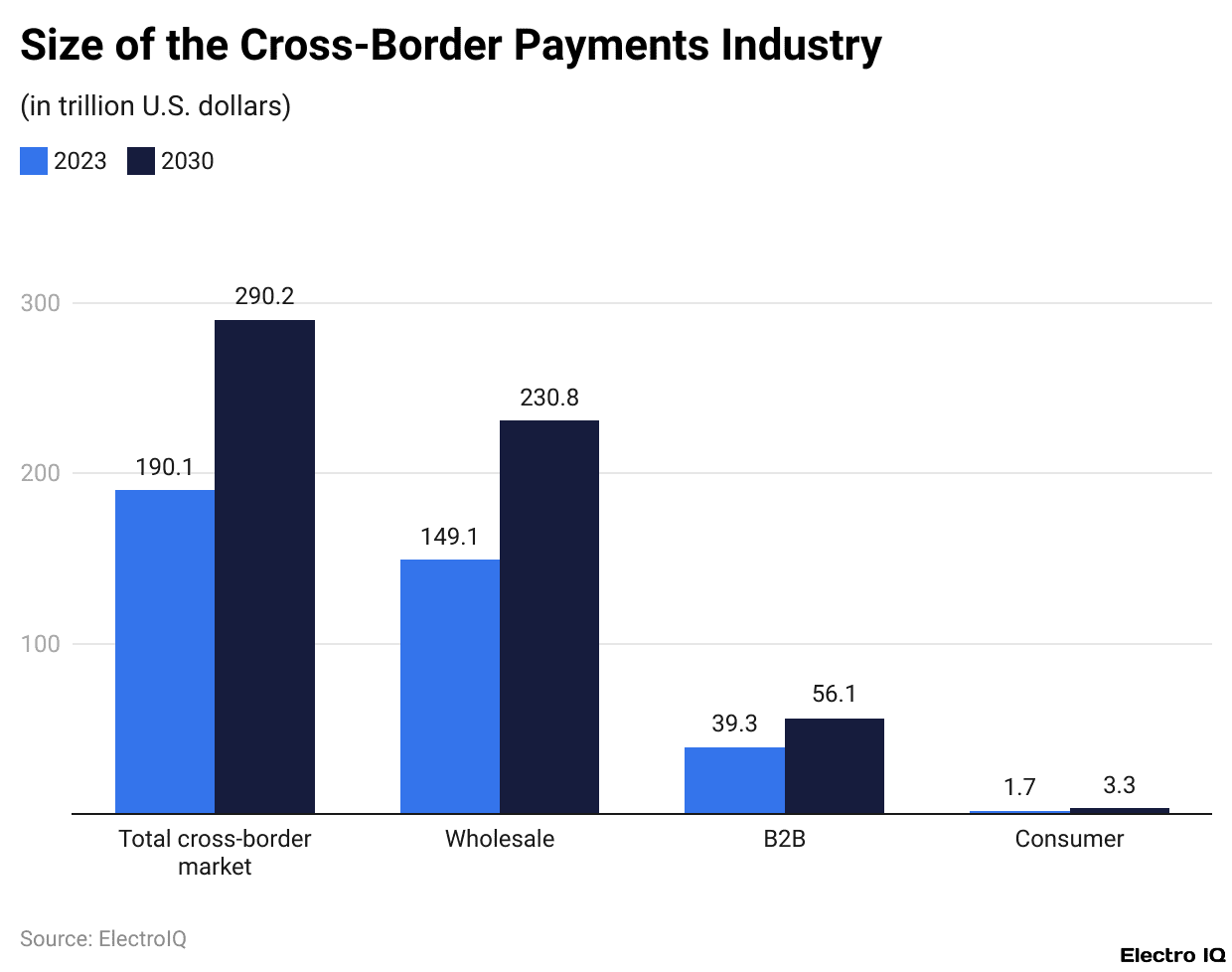

- Cross-border payments reached US$190 trillion in 2023 and are expected to increase to US$290 trillion by 2030 (FXC Intelligence).

- Corporate cross-border payments are sized at US$23.5 trillion annually, with transaction costs greater than US$120 billion.

- The cross-border payment industry generated US$193 billion in revenue in 2023, with revenues from B2B payments accounting for 80%.

- North America and Asia-Pacific have been leading the world in cross-border revenues at 28% and 26%, respectively, while Europe reaped some awards from the adoption of SEPA and SCTinst.

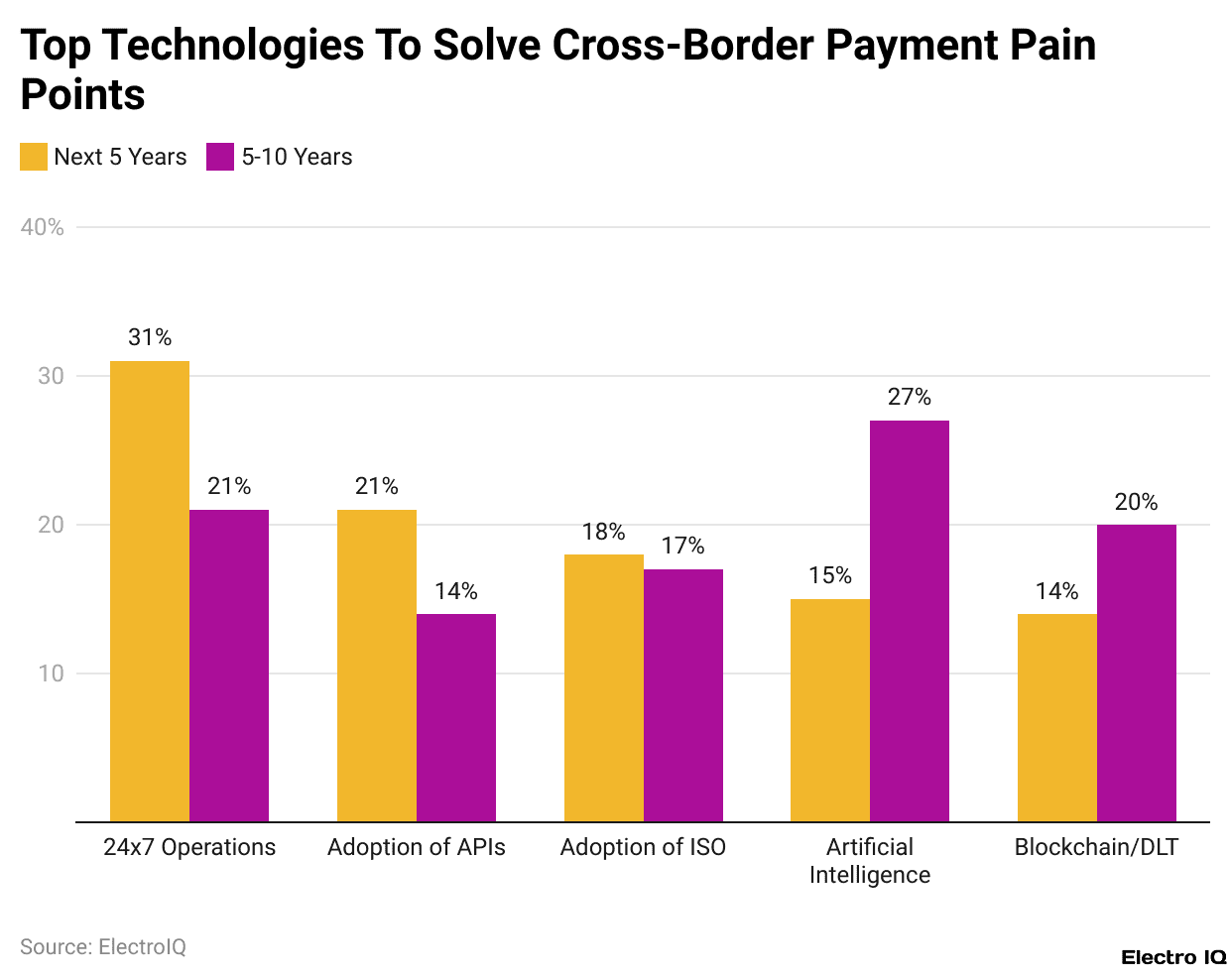

- “24×7 operations (31%), APIs (21%), and ISO standards in the near term (18%) are banks’ short-term priorities. AI (27%) and blockchain (20%) are long-term interests.

- The wholesale cross-border payment market reached US$44.1 trillion in 2023 and is expected to hit US$65 trillion by 2030.

- B2B e-Commerce payments are anticipated to climb from US$10 trillion in 2023 to US$21.9 trillion by 2030 (CAGR, 12%).

- SMBs’ cross-border payments may decline from US$17.2 trillion in 2023 to US$11.4 trillion by 2030, with weak growth ahead.

- Retail payments are pushing out fast: 63% of consumers use real-time services for remittances and 51% for cross-border shopping.

- India supposedly tops (79%) in the global intent to send more cross-border transactions, while Germany, Canada, and the UK lead in the low side of the intent spectrum.

- The frothiest activity in 2024 is global investments into real-time payments tech, amounting to US$15 billion, giving a 25% boost over the year.

- Machine learning prevented US$8 billion in losses annually in fraud cases, representing a 40% decrease in fraud losses.

- RTGS systems now settle faster, from 3 days earlier down to 12 hours (80% faster).

- Russia’s idea to use crypto for cross-border flows to dodge sanctions is indicative of a huge policy shift.

- With the entry of Revolut and Monzo in the US$24 trillion US banking landscape, competition and innovation are set to increase.

General Statistics

- Cross-border payments are gaining traction as e-commerce grows and as COVID-19 restrictions disappear.

- As per a Statista report, cross-border card spending accounts for about 6% of total card spending, with regional variations.

- In 2025, financial service providers need to keep watch over how transaction cost, speed, and customer expectations are changing, for almost three in ten clients will still be identifying cross-border imposition of efficiency as a pain point.

- B2B cross-border payments are much bigger in value than retail payments, as businesses can make high-value transfers, whereas both B2B and retail face high fees and complicated processes.

- The G20 is targeting retail cross-border payment costs to be at 1% by 2027 and remittance costs at 3% by 2030, but the current costs still far exceed these goals.

- Regulatory fragmentation, customs compliance, and localized payment habits add another layer of complexity for international transactions.

- Access gaps matter, too-high regional variance in banking penetration means that a major number of individuals remain unbanked-they cannot participate in any cross-border financial systems.

- Another uncertainty for businesses is unfavorable exchange rate movements. These also impose hidden costs on cross-border transactions.

- Technology is being put to the test as a possible solution: central banks set up pilot CBDCs to enhance interbank settlements while private entities experiment with stablecoins for international transfers, such as PayPal’s PYUSD and Visa’s USDC.

- These companies, including Wise, also increase efficiency through partnerships with big financial institutions like Morgan Stanley and Standard Chartered.

Cross-Border Payment Market Size

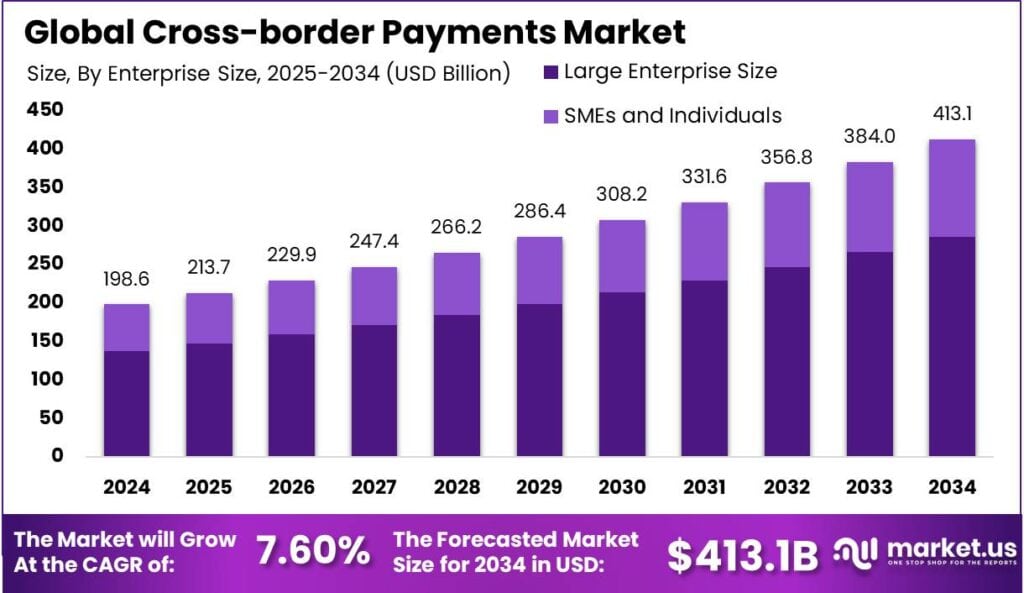

- The Global Cross-border Payments Market is projected to reach USD 413.1 billion by 2034, rising from USD 198.6 billion in 2024, with a growth rate of 7.60% CAGR between 2025 and 2034.

- In 2024, North America led the market with a 38.6% share, generating USD 76.6 billion in revenue.

- The U.S. market was valued at USD 68.9 billion in 2024 and is expected to expand at a 5.9% CAGR, supported by trade, remittances, and e-commerce.

- The growth of smartphones and remote lifestyles is driving the adoption of e-payments because of their convenience and time savings.

- According to GSMA, in 2024 there were 4.88 billion smartphone users worldwide, an increase of 635 million new users compared to the previous year, and this growth trend is expected to continue.

- Research from KarbonCard shows that 97% of cross-border payments are B2B transactions, driven by global trade and e-commerce activity.

- Currently, cross-border payment flows exceed USD 150 trillion annually, underlining their importance in global economic growth.

- By 2027, these flows are expected to increase by 60%, reaching over USD 250 trillion.

- Investment opportunities are strongest in regions like Asia-Pacific, where digital transformation, favorable policies, and e-commerce growth support the adoption of fintech solutions.

- Recent trends include the rise of real-time payment systems for instant transfers and the use of blockchain for secure and transparent transactions.

- Central Bank Digital Currencies (CBDCs) and other digital currencies are emerging to reduce costs and speed up international payments.

- In 2024, the B2B segment dominated the cross-border payments market with more than 52.7% share.

- The large enterprise segment accounted for over 69.4% share in 2024.

- Bank transfers were the leading payment method, holding a share of over 73.4% of global cross-border payments in 2024.

(Reference: omg.one)

- Those numbers you mention paint the picture of how huge and fast-growing the payments industry is.

- Total global payments in value amounted to ~US$190 trillion in 2023, and it is expected to reach US$290 trillion by 2030, according to the FXC Intelligence report on cross-border payments statistics.

- This growth is reflective of increasingly expanding trade, e-commerce, remittances, and business activity worldwide.

- Out of this enormous market, companies alone transfer almost US$23.5 trillion across borders annually.

- Every time money crosses a border, it goes through the banks, payment providers, and messaging networks, who all add to fees.

- On the other hand, foreign exchange emoluments do not seem to account for these costs.

- Indeed, these are the noted transaction costs exceeding US$120 billion each year for corporate cross-border payments.

- In essence, these transactions are expensive and a great money-making avenue for financial institutions and payment companies, even though the flows are the lifeline for global commerce.

- Also analogous to these payments is the greater impetus for faster, cheaper, and transparent processes.

Global Cross-Border Payment By Region

(Reference: paymentscardsandmobile.com)

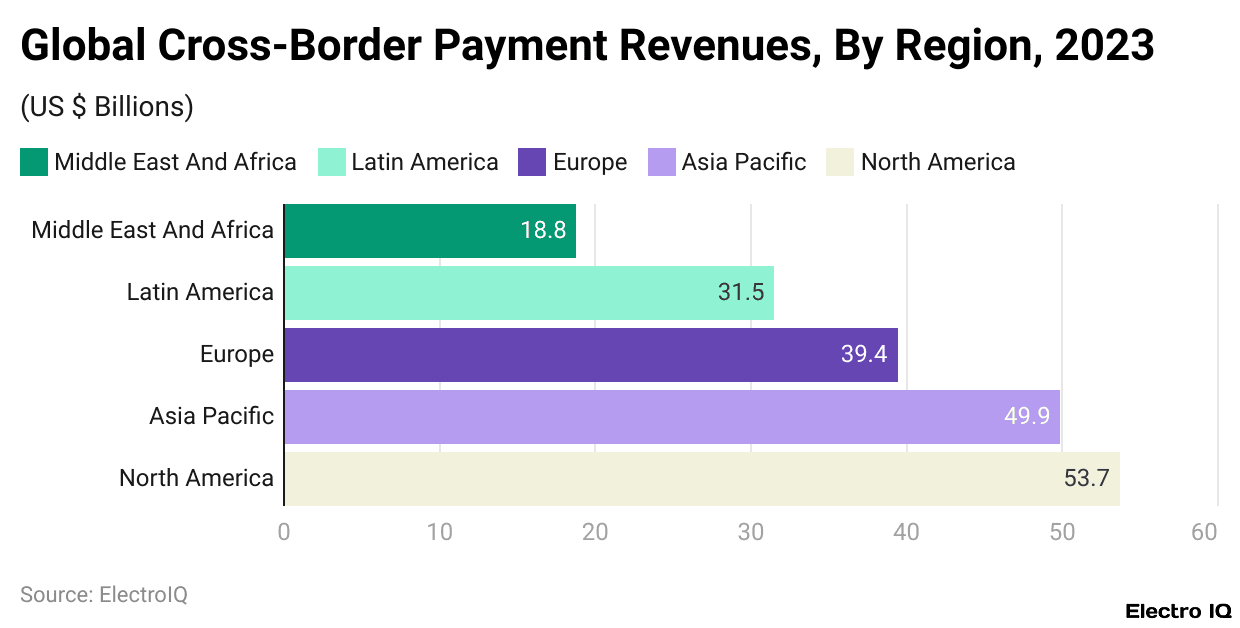

- As per the Payment Cards and Mobile, cross-border payments statistics show that in 2023, the revenues of cross-border payments will touch around US$193 billion, mostly from transaction fees and foreign exchange margins.

- Taking 80% of these revenues, B2B is the segment where the majority of the big-value corporate transactions are handled by banks.

- With the growth in B2B e-commerce and an inclination toward the digitization of payment systems across businesses, this segment is projected to see further expansion and position itself as the largest sub-sector by 2030.

- Yet interestingly, while quite large, B2B payments generally yield low revenue margins vis-à-vis consumer payments, which involve more intermediaries and additional services.

- The consumer’s side witnessed C2B transactions blossoming further onboard the e-commerce boom during the pandemic.

- Although it remains the smallest, the B2C payments segment is also growing as more enterprises adopt digital platforms for paying consumers.

- When regional dynamics come into perspective, North America took 28% of the cross-border revenues in 2023 on account of its robust technological infrastructure and conducive regulations.

- Riding on the back of fintech adoption and digital infrastructure investment, the other Asian giant, labeled as the Pacific-claimed 26% in revenues, is coming at a fast pace.

- Europe, in turn, benefits from initiatives like SEPA, lowering fees and making payments easier, as the advent of SCTinst will, in turn, increase cross-border activity in the region.

- Latin America is gaining momentum on the world stage with its brisk adoption of digital payments during the pandemic.

- Africa and the Middle East are handicapped by infrastructure issues, but are growing, especially in remittances, which still form the bulk of their cross-border flows.

Top Technologies To Solve Cross-Border Payment Problems

(Reference: coinlaw.io)

- With 24×7 operations urgently, 31% of banks consider their attention for the next five years.

- APIs are also major short-term considerations, cited by 21% of respondents who seem to be less interested in the longer run: a drop to 14% after five to ten years.

- ISO standards are considered consistently important, with 18% of banks eyeing them for the next five years, but still 17% see them as worthwhile in the long term.

- Artificial Intelligence, in the near term, is not the first top priority at only 15%, becoming the biggest technology in the long run, as 27% mentioned it as key over the next five to ten years.

- Blockchain and distributed ledger technology find lower rankings in the short term at 14% but gain confidence over the longer term, with 20% of banks expecting increased importance then.

Main Types of Cross-Border Payments

- Wholesale cross-border payments are large-value transfers from one bank to another, to support international trade activities of corporations and governments, as well as lending, foreign exchange, and commodities.

- They are necessary for moving money across borders so that money can be deposited for imports, exports, and liquidity management.

Wholesale Cross-Border Payments Market Size

(Source: softjourn.com)

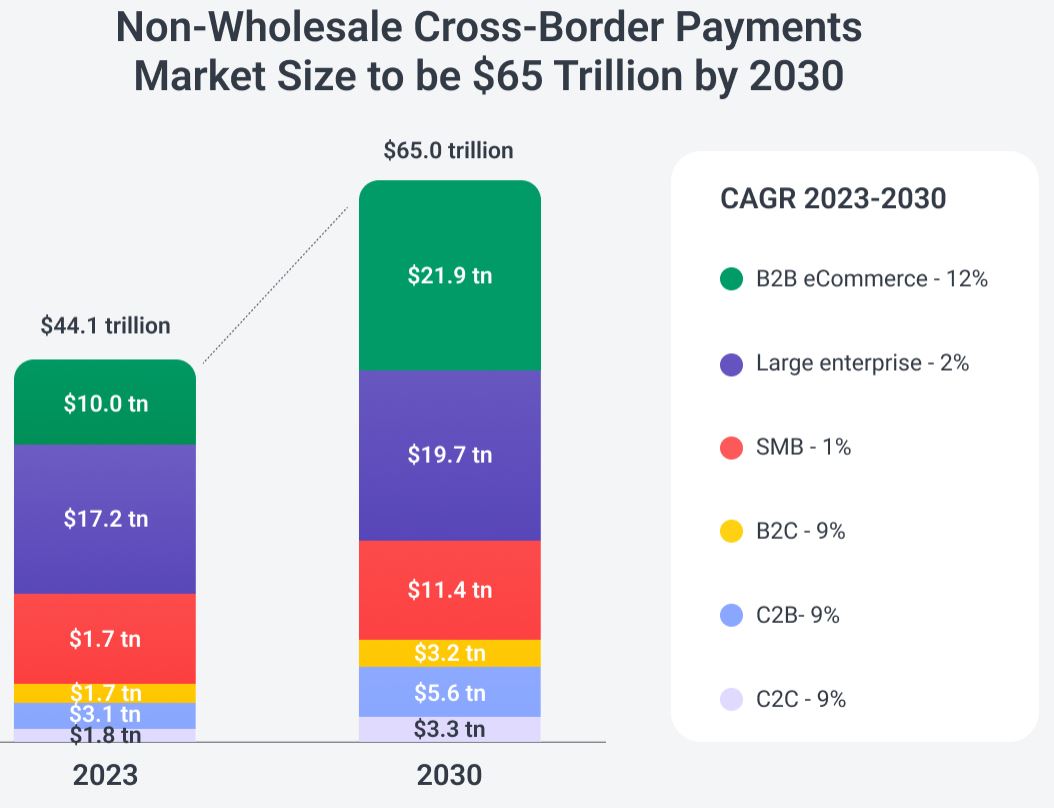

- In 2023, the valued market for wholesale cross-border payments was US$44.1 trillion, with a forecast of hitting US$65 trillion by 2030.

- On a breakdown, B2B e-commerce payments accounted for US$10 trillion in 2023 and are expected to more than double to US$21.9 trillion by 2030, on a strong annual growth rate of 12%.

- Large enterprise payments in 2023 also veered around US$10 trillion and are expected to increase steadily to US$19.7 trillion by 2030, at a CAGR of about 2%.

- Payments involving SMBs, however, were larger at US$17.2 trillion in 2023 but are expected to decline to US$11.4 trillion in 2030, growing slowly at about 1% annually.

- On the consumer side, cross-border B2C payments, though smaller in value, are growing fast -US$1.7 trillion in 2023, with a forecast to hit US$3.2 trillion by 2030, at 9% CAGR.

- Similarly, C2B payments will rise from US$3.1 trillion to US$5.6 trillion and C2C flows from US$1.8 trillion to US$3.3 trillion, all exhibiting about 9% CAGR growth rate.

- This statistic shows that the overall wholesale payment segment will experience heavy expansions; however, B2B e-commerce and consumer-related flows will grow the fastest, while the SMB payments may remain flat or even decline.

Retail Cross-Border Payment

- The term retail cross-border payment denotes everyday international transactions performed by individuals and small businesses.

- They include remittances where the ones sending money to their relatives live abroad, as well as paying online from foreign merchants.

- These are essential for global e-commerce since they allow consumers to buy goods and services outside their local markets.

- According to data from GlobalData’s 2024 Financial Services Consumer Survey, about 63% of consumers worldwide use real-time international payment services to send money to family and friends.

- Almost 51% use such services for making cross-border payments for goods and services.

Demand From Consumers To Increase Cross-Border Transactions

- There is a lot of variation between countries when it comes to the consumer demand for cross-border transactions.

- India stands strongest in terms of momentum, with 79% of consumers who plan to send money more than ever becoming the global head in sender intent.

- Brazil stands out as a growth story, being balanced 70% of senders and 68% of receivers anticipating more activity, thus showing very strong demand on both ends.

- South Africa also exhibits high interest, having 56% of senders and 64% of receivers looking to transact more.

- Other such countries include the Philippines, Colombia, and Mexico, with over half of senders and receivers intending to increase usage for both parties.

- In contrast, intent is much weaker in Germany, Canada, and the UK, with roughly only 19%–22% of senders and 26%–30% of receivers planning growth.

- Globally, the averages are 41% for senders and 48% for receivers, which reflects an uneven, albeit significant, upward trend in the global flow of money.

Technological Innovations

- Real-time payments technology spending across the world hit US$15 billion in 2024, a 25% increment over 2023.

- Blockchain systems are fast becoming popular for cross-border payments and now process roughly US$5 billion a year, and are growing at a sharp 17% CAGR.

- APIs are becoming very popular as well, with over 60% of fintechs embracing them to ease cross-border payments for customers.

- AI-based learning has been able to somewhat prevent fraud and hence reduce losses by almost 40%, saving the industry about US$8 billion each year.

- Cloud-based platforms for payments also saw 30% growth, giving the providers even faster and larger processing capabilities.

- These actions together will give system compatibilities a bump of about 50% in 2025 when moving to ISO 20022 standards.

- This seizure gives a huge kick to RTGS systems, which makes payments monumental and faster, slashing their settlement time from three days to 12 hours, which is an 80% uplift in efficiency.

Regulatory Landscape

| Regulatory Development |

Value/Statistic

|

| AML/KYC compliance costs | 15% of costs |

| ISO 20022 adoption |

Mid-2025 efficiency improvement

|

| CBDC pilot projects |

Over 20 central banks

|

| Data localization impact |

Higher complexity in India and Brazil

|

| SWIFT-blockchain hybrid transparency |

40% of transactions

|

| Open banking push |

Smoother cross-border transactions

|

(Source: coinlaw.io)

- As per Coin Law, cross-border payment statistics show that many laws and regulations govern cross-border payments. AML and KYC currently constitute about 15% of the industry’s compliance costs.

- ISO 20022 is forecasted by mid-2025 to govern the efficiency of communication between global financial systems.

- In consequence, the regulators in the EU and the US are currently strengthening regulations on cross-border crypto transactions, hoping to stop financial crimes.

- CBDCs are looked upon as the solution, with more than 20 central banks running pilot projects to improve both regulation and interoperability.

- In contrast, in other ambitious Asian countries such as India and Brazil, localization laws are in place, which insist on companies storing payment data locally: this poses a grave compliance challenge.

- Collaboration between SWIFT and blockchain platforms has resulted in the establishment of certain hybrid systems, thereby increasing the transparency of nearly 40% of all transactions.

- Governments are supporting open banking models to ease cross-border transfers while also providing safeguards to customers.

Recent Developments

- Major banks and fintechs like Bank of America, Standard Chartered, PayPal, Revolut, and Stripe have started entering the stablecoin market.

- Through cryptocurrencies, it is envisaged that cross-border payments should be faster and cheaper, thereby providing a boost to emerging markets.

- In Russia, the government is looking at using cryptocurrencies to get around Western sanctions that restrict international payment flows.

- This marks a big shift in Russia’s approach towards digital assets and might well reverberate throughout global payment systems.

- In the UK, Revolut and Visa are challenging the Payment Systems Regulator in court over its proposed cap on interchange fees for cross-border online payments.

- The decision could define how cross-border transactions are regulated, not only in the UK but perhaps also elsewhere.

- Eying the US$24 trillion American banking sector for income, UK fintechs like Revolut and Monzo also intend to go across the pond.

- This migration could add greater competition and innovations to the international payments space.

- Meanwhile, the UK regulator is busy investigating its proposed maximum limits to card fees across borders between British merchants and European buyers.

- The review will attempt to strike a balance between the interests of credit card companies and retailers; the decision might have an impact on the cost of making cross-border payments in that area.

Conclusion

Cross-Border Payments Statistics: Cross-border transactions are seeing rapid growth and transformation by virtue of e-commerce, remittance, and international trade in 2024. The industry is bursting with opportunities and challenges, with value projections standing at US$190 trillion in 2023 and going up to US$290 trillion by 2030. Until recently, high cost, difficult regulations, and fragmented systems were barriers.

However, disruptions through real-time payment, blockchain, stablecoins, and CBDCs have changed the dynamics for good. There is a rise in demand from consumers globally, with a big wave coming from emerging markets like India and Brazil. Cross-border payments are extremely important for global financial inclusion and digital commerce as banks, fintechs, and regulators work toward setting up faster, cheaper, and transparent payment systems.

FAQ.

According to FXC Intelligence, the cross-border payments market was valued around US$190 trillion in 2023 and is anticipated to reach US$290 trillion by 2030. The majority of this cash flow is from businesses, conducting transactions of almost US$23.5 trillion annually, generating US$120 billion in transaction costs.

North America generated 28% of global revenues in 2023, followed by Asia-Pacific with 26%, reflecting strong fintech adoption. Meanwhile, Europe still benefits from SEPA and SCTInst initiatives while Latin America and Africa observe growth fueled by digital payments and remittances.

Key technologies include around-the-clock banking hours, APIs, ISO 20022 standards, AI, and blockchains. And real-time settlement systems have reduced the hammering from 3 days to just 12 hours, and machine learning cut down fraud losses by 40%, thereby saving US$8 billion each year for the industry.

Consumer demand has been surging, with 63% of the population running real-time services for remittances and 51% for shopping. 79% of Indian consumers are looking to increase international transactions, while Brazil has strong two-way movements from both senders and receivers.

Major banks and fintechs such as PayPal, Revolut, and Stripe, are adopting stablecoins to reduce costs. Russia is using crypto to discount sanctions, and UK fintechs are breaking into the US$24 trillion US banking market. Regulatory reviews in the UK and the EU could also change fee structures for cross-border payments.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.