Google Cloud Platform Statistics And Facts (2025)

Updated · May 06, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Key Facts

- Google Cloud Platform Revenue

- Market Share Of Leading Cloud Service Providers

- Google Cloud Platform Global Customers

- Growth Of Google Cloud Platform Statistics

- Google Cloud Platform Customer Base By Industry

- GCP Cloud Computing Trends And Strategic Insights For IT Leaders

- Conclusion

Introduction

Google Cloud Platform Statistics: Google Cloud Platform (GCP) has witnessed profound growth and evolution in 2024, vis-à-vis its development into a sizeable partner in the world cloud computing ecosystem.

This article curates comprehensive Google Cloud Platform statistics from the past year, considering statistics, financials, and strategic profile developments that have influenced the path taken by GCP.

Editor’s Choice

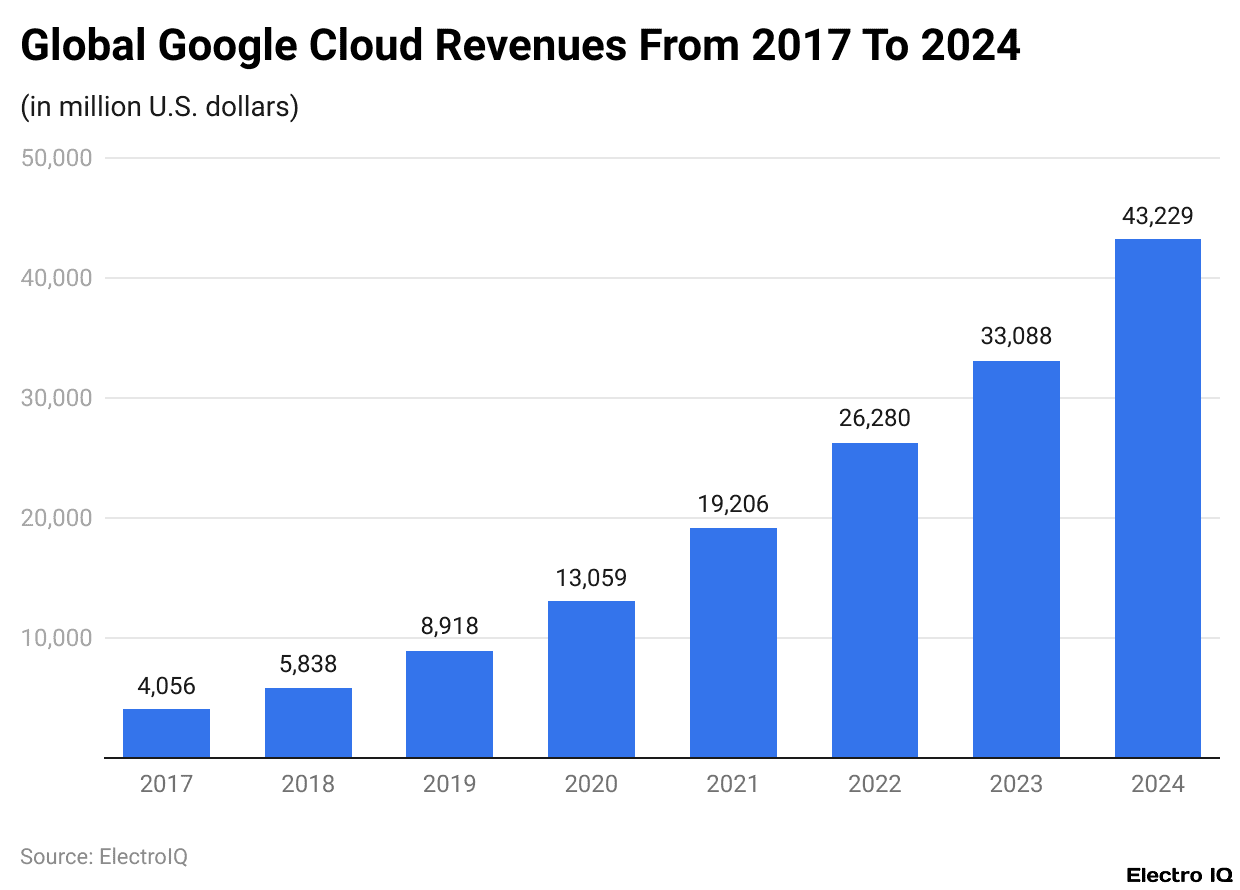

- According to Google Cloud Platform statistics, in 2023, Google Cloud achieved revenues of US$43.22 billion, representing over 10% of total earnings for Google.

- GCP has been continuously growing as the adoption of cloud computing for digital transformation grows. Flexible infrastructure and competitively priced pay-as-you-go deals will sustain the increase in AI adoption on the cloud.

- The cloud infrastructure market is led by AWS, holding 30% of the market share, followed by Microsoft Azure at 21% and Google Cloud at 12%.

- Cloud infrastructure spending increased by US$17 billion in the fourth quarter of 2024, bringing the total annual spending to US$330 billion.

- Google Cloud Platform statistics state that in North America, there are 497,199 customers (51.8% of the total); in EMEA, there are 272,256 (28.4%); in APAC, there are 141,555; and in LATAM, there are 48,319.

- GCP runs 40 cloud regions comprising 121 zones and 187 network edge locations in more than 200 countries.

- New cloud regions have opened recently in Germany, Qatar, Saudi Arabia, and South Africa, with additional ones expected in Mexico, Malaysia, Thailand, and so on.

- GCP’s fastest-growing vertical, startups, grew their customers by 28.1% in 2023-2024, while SMBs saw growth of 8.7%.

- Google Cloud Platform statistics show that significant expenditures were made by the Internet sector on GCP, including 10.5% of the consumers subscribing for more than US$5,000 a month.

- More than 50% of organisations are hiring or upskilling employees for cloud cost optimisation.

- 37.1% of organisations are at the earlier stages of implementing cloud FinOps, while only 19.5% have achieved full maturity.

- Cloud cost optimisation and value-driven cloud use cases could generate an EBITDA value of US$1 trillion in savings for Fortune 500 companies by 2030.

- By 2027, over 50% of enterprises are expected to adopt industry-specific cloud platforms.

- Google Cloud Platform statistics reveal that more than 40% of technical and business professionals are using automation to optimise cloud spending and reduce wastage.

- 54% of decision-makers will look for cloud providers that increase revenue or minimise costs, while 50% will consider those that provide industry-specific solutions and infrastructure support.

Key Facts

- It’s under Google Cloud, but it was formerly known as App Engine; therefore, it was launched in 2008 to counter growth from Amazon Web Services (AWS).

- From offering only Platform as a Service for a few years, GCP today provides Infrastructure as a Service (IaaS) and Software as a Service (SaaS) services to markets across the globe.

- It is quite specialised in the development and maintenance of employee-specific applications hosted and deployed from its own hyperscale data centers.

- Google Cloud earned more than US$33 billion in gross revenue in 2023, contributing nearly 10% to Google’s total income.

- Google Cloud has become one of tens of thousands of data centers that deliver services and infrastructure over the globe.

- Google customers can use the console or API to access the compute, storage, networking, and security capabilities of this entire space.

- The various deployment models supported by these infrastructures include public cloud, hybrid cloud, multi-cloud, and edge cloud.

- Launched in March 2023, Bard was renamed Gemini and was reportedly intended to compete with other generative AI companies.

- Google Cloud Platform statistics reveal that in 2024, Google Cloud introduced Gemini, a program that enhances its Vertex AI platform to further ease the work of organisations in developing and deploying enterprise-grade AI.

- GCP houses over 10,000 tools and products in its cloud marketplace, with more than half of them claimed by specific vendors to have artificial intelligence and machine learning capabilities.

- Enterprises can train and deploy AI models or use pre-trained ML APIs, including Vision AI and Natural Language API.

- Embracing an open-cloud paradigm, Google Cloud advocates open-source technologies for better user empowerment.

- GCP is one of the best cloud vendors, along with AWS and Microsoft Azure, to which it is widely considered a major competitor.

- Google Cloud Platform statistics show that GCP has historically focused less on enterprise customers than the other two cloud providers but holds around 10% of the market.

- Fewer services offer GCP, which skews its cloud model toward software developers.

- Increasing enterprise IT integration is reflected in a growing proportion of enterprise customers now on GCP.

- It shows how powerful the technology is, and that brings in other major customers such as Spotify and Goldman Sachs.

Google Cloud Platform Revenue

(Reference: statista.com)

- In 2023, the US cloud giant, Google, brought in revenues worth US$43.22 billion, which would now generate more than 10% of Google’s total earnings out of the Cloud segment. This main revenue driver from the cloud segment is Google Cloud Platform, which offers cloud computing services that run entirely on Google’s infrastructure.

- GCP was developed significantly because companies began to adopt cloud computing for their digital transformation initiatives over the years. This rapid expansion is due to an increased demand for cloud-based solutions, scalable cloud infrastructure reliance, and the growing trend toward microservices.

- However, with fierce competition between major cloud service providers such as Microsoft Azure and Amazon Web Services, all players in the industry will be required to innovate and bring out new services continuously to attract and retain customers.

- Consumers will also want more of the emerging technology like artificial intelligence (AI), which is limitless in making the need for cloud infrastructure soar. Cloud platforms make developing, deploying, and managing AI much easier because they offer the necessary storage and processing tools, along with easy integration of machine learning within the AI model.

- Pay-as-you-go pricing on the cloud platforms provided by the providers for AI consumption is also encouraging acceptance of the cloud in that it favors easy access and less costly development for enterprises.

(Source: statista.com)

- AWS has consistently remained at the helm in the cloud infrastructure market, as it has yet been known to be trailing its rivals. As AWS, this is the company’s online retail giant cloud computing arm, still significantly gaining profits and dominance.

- According to estimates from Synergy Research Group, AWS conquered the global cloud infrastructure market with a 30 % share at the end of the fourth quarter of 2024.

- For Microsoft, the same quarter referred to Azure with a second-ranked value of 21%, while Google Cloud was rated at 12% in the same reference.

- The dominant three, however, made up more than 60% of the developing cloud market, where the other players had single digits to sing about.

- Worldwide spending across cloud infrastructure services soared to US$17 billion from the close of 2024, a growth of 22% over the same period last year. In total, during the third quarter, it reached US$91 billion.

- For the full year, revenues generated by cloud infrastructure services totaled US$330 billion, thereby emphasising the severe competition between the providers.

- Even with such a large share of the market, growth remained quite buoyant in the year, with year-on-year expansion accelerating through 2024.

Google Cloud Platform Global Customers

(Source: hginsights.com)

- GCP has a very large clientele around the globe, but the strongest concentration by far is in North America, where it has 497,199 buyers, making it 51.8% of the total. Next is Europe, the Middle East, and Africa (EMEA), with 272,256 buyers, who represent 28.4% of the total.

- Countries in the Asia-Pacific region (APAC) collectively account for 141,555 buyers, while Latin America (LATAM) has 48,319 buyers.

- All these numbers show that GCP is present strongly in North America and EMEA, with a comparatively smaller but steadily increasing number of customers in APAC and LATAM.

- Google Cloud has a wide network of infrastructure consisting of 40 cloud regions, 121 zones, and 187 network edge locations where its services are available in more than 200 countries and territories. This infrastructure ensures users worldwide high-availability and low-latency service.

- Google Cloud Platform statistics state that in 2023 and early 2024, global expansion included four new cloud regions in Berlin (Germany), Doha (Qatar), Dammam (Saudi Arabia), and Johannesburg (South Africa). Several other locations earmarked for future expansions are Mexico, Malaysia, Thailand, New Zealand, Greece, Norway, Austria, and Sweden.

- All these continuous expansions increase the reach and evidence of Google Cloud’s commitment to making its infrastructure more accessible and utilising it worldwide.

Growth Of Google Cloud Platform Statistics

(Source: hginsights.com)

- The steady customer growth enjoyed by Google Cloud Platform year-on-year has been among businesses of all sizes. The largest increase from 2023 to 2024, however, was among startups and was greater than 28.1%, thus being the fastest-growing segment.

- GCP also saw an 8.7% increase in customers coming from small and medium-sized businesses.

- Certainly, this defines GCP’s solid attractiveness to smaller or emerging businesses as it further solidifies its position as a leading cloud provider for startups and SMBs that are on the lookout for flexible and innovative solution offerings.

Google Cloud Platform Customer Base By Industry

(Source: hginsights.com)

- By segmenting Google Cloud Platform customers by industry across five major verticals- Media, Manufacturing, Internet, Education, and Financial Services analysis of spending across these industries indicates non-uniform levels of investment in cloud infrastructures.

- According to Google Cloud Platform statistics, the Internet tends to have a larger proportion of those monthly expenses from customers spending significant amounts on Google Cloud services: 10.5% of buyers spend US$5,000 or more monthly.

- The heavy reliance of these companies in the sector is shown to be significant on GCP for their infrastructure and computing needs.

- Spending patterns across industries give an insight into which sectors invest most in cloud technology, with Internet-based businesses in the lead on the heavier tier of consumption.

GCP Cloud Computing Trends And Strategic Insights For IT Leaders

- The cloud is becoming the port of call for IT leaders to sail through future vagaries. Per the macroeconomic conditions, the cloud leaders include 41.4% who have started utilising more cloud-based services and products, 33.4% who have transitioned from legacy enterprise software to the cloud, and 32.8% who migrated from on-premises to the cloud.

- They give priority to cloud cost optimisation, and over half of them either employ new staff or retrain existing staff on managing cloud spend. They have largely not executed cloud FinOps yet.

- Around 37% of the survey conducted by FinOps on practitioners of FinOps are called “Crawl”, and 41.7% have passed to the “walk” stage, where practices are established but incomplete. Just 19.5% qualify for the advanced “run” stage, where FinOps is fully integrated into operations.

- Cloud adoption across almost all industries brings mammoth financial opportunities.

- Google Cloud Platform statistics suggested a figure of more than a trillion dollars that Fortune 500 companies would be able to realise by 2030 due to optimisation and business use of the cloud in terms of run-rate EBITDA.

- By 2027, more than half of enterprises will have deployed industry-specific cloud platforms to enhance agility, accelerate innovation, and bring value.

- Automated cost optimisation in cloud computing has become more popular, with over 40% of technical and business professionals having in place policies to shut down workloads after hours and optimise instances that are underutilised.

- These strategies are saving time, reducing unnecessary expenses, and ensuring optimal resource management in the cloud. When picking their strategic partner in cloud computing, decision-makers are looking for three main characteristics.

- The majority of people, say 54%, want partners who are able to assist in formulating strategic technology approaches meant for increasing revenue or cutting costs.

- Google Cloud Platform statistics show that 50% are concerned with those partners who understand industry trends and have forward-thinking solutions, while the very same 50% also greatly value service organisations to help these cloud partners with infrastructure implementation and maintenance.

Conclusion

As per Google Cloud Platform statistics, it is growing impressively as a result of various investments in AI and infrastructure. GCP strengthens its standing in the cloud platform competition. It is great that the platform is not only expanding but also putting in such a huge amount of expenditure, and all of this is a matter of concern for investors and regulators.

GCP continues to stretch its innovations to enhance expansion; however, at this stage, shifts in concentration from rapid growth to financial prudence and regulatory compliance will be vital for maintaining its upward thrust in the field.

Sources

FAQ.

Google Cloud earned US$43.22 billion in revenue in 2023, which contributed to more than 10% of Google’s overall earnings.

Amazon Web Services leads with a 30% market share in Q4 of 2024, followed by Microsoft Azure at 21%, while Google Cloud accounts for 12%.

With 10.5 % of the buyers from the Internet sector spending US$5,000 or more per adoption month, the rest as Media, Manufacturing, Education, and Financial Services.

Google Cloud laid down a new cloud region in Berlin (Germany), Doha (Qatar), Dammam (Saudi Arabia), and Johannesburg (South Africa) between 2023 and early 2024, with further planned expansions in Mexico, Malaysia, Thailand, New Zealand, Greece, Norway, Austria, and Sweden.

The result is that over 50% of all organisations are retraining or hiring headcount for cloud cost optimisation, while 40% of professionals use automation to eliminate unnecessary expense, such as switching workloads off after a day and optimising underutilised instances.

Barry Elad is a passionate technology and finance journalist who loves diving deep into various technology and finance topics. He gathers important statistics and facts to help others understand the tech and finance world better. With a keen interest in software, Barry writes about its benefits and how it can improve our daily lives. In his spare time, he enjoys experimenting with healthy recipes, practicing yoga, meditating, or taking nature walks with his child. Barry’s goal is to make complex tech and finance information easy and accessible for everyone.