Microfinance Statistics By Market Size, Growth, Leading Companies, Trends, Insights and Facts (2025)

Updated · Nov 24, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Microfinance Market Size Globally

- Key MFI Performance Metrics

- By Gender and Microfinance

- Client Demographics And Outreach

- Leading Companies & Market Share Insights

- Global Performance of MFI

- Sources of Funds for Different Microfinance Institutions

- Challenges And Risks

- Recent Development

- Conclusion

Introduction

Microfinance Statistics: Microfinance is an activity that offers microloans, savings accounts, as well as other financial services to individuals who are mostly not in a condition to get a loan. By 2025, the total amount of microfinance will be large and still growing rapidly. Microfinancing is a helping hand for countless people, letting them either start or expand their little enterprises, to pay for their children’s education, and to survive the likes of sickness.

Nonetheless, stress in the sector is characteristic in some countries, and the statistics are not the same across the board. We are showing you the most significant microfinancing statistics for the period from 2023 to 2025.

Editor’s Choice

- The global microfinance industry recorded US$279.22 billion as its market value in 2024 and is expected to continue increasing, reaching around US$310.10 billion by 2025, with projections of US$797.11 billion for 2034 as a result of the CAGR of 11.06% in long-term forecasts.

- Microfinance institutions(MFIs) are a major source of financial access by bringing to the very low-income populations micro-savings and micro-insurance to serve over 50 million customers, as they drive financial inclusion.

- In 2023, one out of four microfinance loans was given through digital channels, which is a clear indicator of a very rapid digital financial platforms.

- Women make up 70% of all microfinance customers, and that is why loans granted had a positive effect on the establishment and growth of over 100 million female small business owners.

- MFI-supported women-led firms experienced growth that was 12% higher than male-led businesses.

- Financial literacy training has become accessible to over 15 million women and 10 million borrowers worldwide, which has resulted in better financial management and empowerment.

- Microfinance lending has the capacity to create more than 20 million jobs around the globe, mainly in the poorest regions and rural areas.

- Younger clients who are below 35 years old represent 65% of the total clients, indicating that youth entrepreneurs are very actively participating in the business.

- Half of the borrowing clients are from the countryside, and among them, 80% are from the low-income bracket.

- Agricultural credits constitute 30% of the total amount of microfinance offered in the market, thereby supporting the farming community in their struggle for a livelihood brought about by the food crisis.

- Digital lending in small amounts is expected worldwide to be 30% more by the year 2024, with the main contributors being Kenya and India.

- Among the big transactions, the US$75 million purchase of Madura Microfinance by CreditAccess Grameen (2023) and the US$3 billion takeover of Gruh Finance by Bandhan Bank (2022) are the most noteworthy ones.

- Accion Microfinance obtained US$100 million in funding (2023), while the Grameen Foundation was granted US$50 million by the Bill & Melinda Gates Foundation.

Microfinance Market Size Globally

(Reference: precedenceresearch.com)

- The global microfinance market reached a valuation of around US$279.22 billion in 2024, which is an indication of how big and well-established the industry is.

- The market is projected to increase further to about US$310.10 billion in 2025, which is a reflection of the continued demand for small-scale loans and financial inclusion programs across developing and emerging markets.

- The market, on the other hand, analysts forecast a possible US$797.11 billion by 2034, which is almost tripling the size of the market in nine years.

- This growth in the very long term amounts to a compound annual growth rate (CAGR) of approximately 11.06% from 2025 to 2034.

- To put it differently, the market will be expanding just a little over 11% per year on an average basis.

- The factors that are likely to support this growth are digital lending platforms, the increasing penetration of smartphones, favourable government policies, and the constant requirement of financial access for the low-income groups, among others.

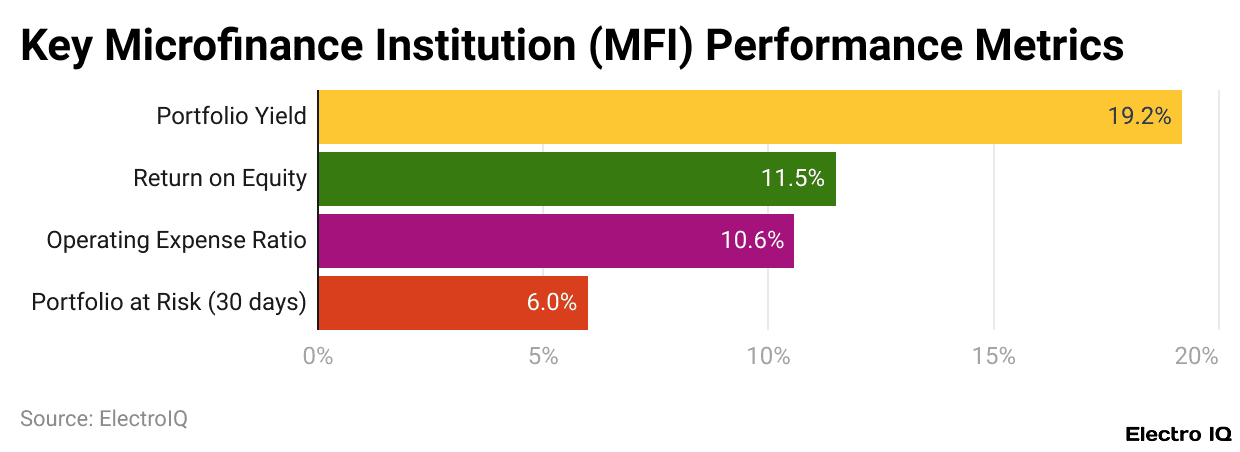

Key MFI Performance Metrics

(Reference: coinlaw.io)

- One of the main indicators, the portfolio yield, was 19.2% at its highest, revealing that the MFIs had a very good level of income from the amount lent.

- The reporting of 11.5% as return on equity (ROE) indicated how good the institutions were in converting the equity of the shareholders into profit.

- Talking about the expenses, the operating expense ratio was 10.6%, which implies that just slightly more than one-tenth of the total income was allocated to running the business, i.e., the operation was still very efficient.

- On the flip side, concerning the risk, the determination of the portfolio at risk (30 days) was done at 6.0%, indicating the proportion of the loans that had not been cleared for more than 30 days overdue.

By Gender and Microfinance

- Women are the key players in the sparking and sustaining of the microfinance revolution on a global scale.

- They were and still are the bulk of the total clients of microfinance to the extent of 80% while the institutions are granting loans to female entrepreneurs.

- This strategy is not only effective in society but also in terms of finances—it has always been the case that women would repay their loans higher than men; thus, they are considered to be the best and dependable borrowers.

- Women’s involvement in microfinance in South Asia has a huge impact. This area’s women account for about 90% of the borrowers, with Bangladesh and India taking the lead in the financial inclusion of females.

- With the help of these programs, the financial resources that were once inaccessible to millions of women have been opened up, thus empowering them to create small enterprises, enhance the living standards of their families, and acquire autonomy.

- A study released in 2023 reported that female entrepreneurs assisted by micro-financial institutions (MFIs) experienced a 12% higher growth rate than their male counterparts.

- It has been estimated that over 100 million women worldwide have benefited from the microfinance loans during the past years, which have allowed them to fully participate in socio-economic life by starting or enlarging their businesses.

- To further promote female entrepreneurship, many MFIs extend interest rates that are 5-10% lower for female-led businesses.

- In addition to loans, MFIs also fund the education sector, whereby financial literacy training of over 15 million women globally has actually taken place, which has enhanced their budgeting, saving, and money management skills.

- Approximately 40% of women who were granted microloans there transitioned from informal to formal employment, thereby attaining financial stability and long-term economic empowerment.

Client Demographics And Outreach

- Microfinance is drawing a customer base that is young and full of energy.

- The data shows that approximately 65% of the microfinance clientele are below the age of 35, which clearly indicates that most of the loans taken are by young adults who either want to upgrade their standard of living or start small firms.

- Almost half of the world’s microfinance clients (50%) live in the countryside; traditional banks hardly ever go there. Hence, by going into these neglected areas, MFIs grant people financial access who happen to be in the most need.

- In 2023, youth-oriented microfinance programs saw a surge of 15% thus empowering young entrepreneurs with the tools to get startups going or to keep small businesses running.

- An impressive 80% of the microfinance clients belong to underprivileged families, proving that the industry is still committed to serving the financially weakest segments of the population.

- Retail and trade sectors absorb nearly 35% of urban borrowers’ funds, thus helping small vendors, shopkeepers, and service providers extend their range of operations and also contributing to the local economies.

- Agriculture is still an indispensable part of the microfinance portfolio that takes a 30% share of all loans.

- Grameen Bank is one of the biggest microfinance institutions in the world, serving 9 million clients and holding a 4% market share in 2023, mainly across Bangladesh and Asia.

- BancoSol in Bolivia manages a loan portfolio worth $1.5 billion, representing 3% of the microfinance market in Latin America.

- Bank Rakyat Indonesia (BRI) controls 40% of the microfinance sector in Indonesia, serving around 30 million clients nationwide.

- SKS Microfinance in India increased its loan book by 12% in 2023, providing services to nearly 4 million clients in rural areas.

- Equitas Small Finance Bank, also in India, grew its client base by 10% and now holds a 2% market share within the South Asian microfinance market.

- Compartamos Banco in Mexico disbursed loans totaling $1 billion in 2023, supporting over 3 million borrowers.

- KWFT Microfinance Bank in Kenya grew its loan portfolio by 15% and now serves more than 1 million clients, placing it among the top institutions in Africa.

| Microfinance Institution | Country/Region | Clients Served | Loan Portfolio / Disbursements | Market Share / Growth | Year |

| Grameen Bank | Bangladesh & Asia | 9 million | — | 4% market share | 2023 |

| BancoSol | Bolivia | — | $1.5 billion | 3% market share in Latin America | 2023 |

| Bank Rakyat Indonesia (BRI) | Indonesia | 30 million | — | 40% of Indonesia’s microfinance sector | — |

| SKS Microfinance | India | 4 million | — | 12% loan growth | 2023 |

| Equitas Small Finance Bank | India | — | — | 10% client growth, 2% market share in South Asia | — |

| Compartamos Banco | Mexico | 3 million | $1 billion | — | 2023 |

| KWFT Microfinance Bank | Kenya | 1 million | — | 15% loan portfolio growth | — |

Global Performance of MFI

- The world over, micro-finance institutions keep performing excellently with an impressive loan repayment rate of 96% on average. The reason behind such a high repayment rate is that the majority of the borrowers pay back their dues, thus showing the trust and reliability that have developed in the sector.

- In the year 2023, the MFIs collectively disbursed around US$130 billion of loans to borrowers all over the world.

- The Asian region is still the largest and most vibrant area for microfinance, where more than 60% of global microfinance assets are located. India and Bangladesh are the countries that prevail in this sector as they have large MFI networks and their respective governments’ support for financial inclusion.

- The Latin American and Caribbean region holds about 16% of the global market share, with Mexico and Bolivia being the most significant players in terms of loan disbursement.

- In Sub-Saharan Africa, the number of clients served by microfinance institutions grew to 18 million in 2023, which is a 12% increase compared to the previous year. This growth is an indicator of the rising contribution of MFIs to bettering the living standards in the region.

- However, Europe and Central Asia continue to struggle, holding around 6% of the global portfolio, with Eastern Europe primarily contributing 8% annually into the region’s micro-lending services, which constitute the major part of the total growth.

- By the year 2024, global micro-lending is likely to be 30% higher than even at the present time, with African countries like Kenya and the Indian sub-continent leading in mobile-based financial services.

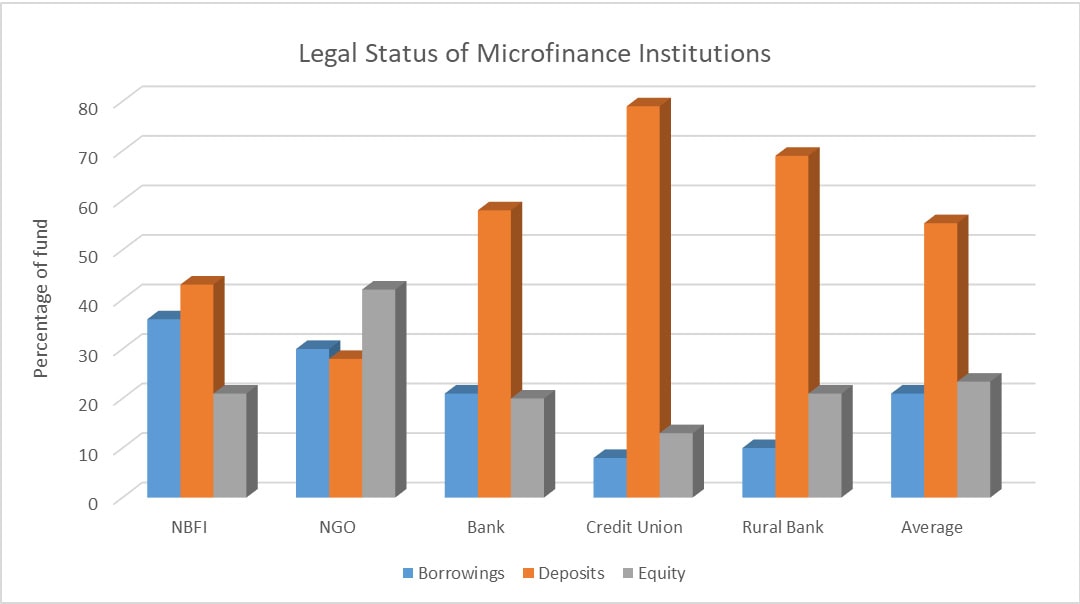

Sources of Funds for Different Microfinance Institutions

- Credit Unions get most of their money from deposits, which make up 80% of their total funds.

- Rural Banks mainly use deposits too, covering about 70% of their funding.

- Banks use a mix of sources, with 60% from deposits and 25% from borrowings.

- NGOs depend mainly on equity, which forms 50% of their total funds.

- Non-Banking Financial Institutions (NBFIs) have a balanced structure, receiving 40% from borrowings and 50% from deposits.

- On average, microfinance institutions get 55% of their funds from deposits, 30% from equity, and 25% from borrowings.

Challenges And Risks

- The microfinance sector is being challenged by a number of critical issues that may negatively affect its sustainability and growth.

- High operational costs are the primary issue that the sector faces; it is especially difficult for institutions providing services in remote and rural areas where digital infrastructure is poor.

- In order to provide services to the remote area clients, the institutions have to conduct physical visits, manual processing, and hire additional staff, which increases costs and decreases profitability.

- The issue of over-indebtedness among borrowers is another concern that is increasing over time. A transfer of loans is one of the major factors contributing to the existence of such a cycle.

- About 10% of microfinance clients in some areas are reported to be taking out loans from multiple lenders to pay off their debts.

- The regulators are forcing more and more compliance and reporting through the governments, which are becoming ever stricter.

- The new regulations will, in turn, increase the overall market transparency and consumer protection, but will be quite costly and time-consuming for the smaller MFIs to absorb and implement.

- The scenario of change in climate change is another risk factor, which is more so for the agricultural borrowers only.

- Farmers may be left repaying their loans if extreme weather conditions like droughts, floods, or storms have already inflicted losses on their crops or livestock.

- Not only does this put the farmer’s family in distress, but it also puts the lender who has highly invested in agricultural finance.

Recent Development

- The early part of 2023 saw one of the most important events when CreditAccess Grameen completed the US$75 million takeover of Madura Microfinance.

- By doing this, the company took a step towards gaining more ground in the rural areas of India, while it would also prove to be a great help in reaching the unserved populations.

- In the same fashion, Bandhan Bank in late 2022 made a US$3 billion purchase of Gruh Finance that not only widened its microfinance basket but also gave it a better position in housing finance, thus expanding its potential clientele.

- One more aspect that kept pushing the sector ahead was the innovation of products. A digital loan platform that drastically cut down the application and disbursement time was launched by SKS Microfinance in the middle of 2023.

- The funding activities have played an important role in the industry’s enlargement. Accion Microfinance pulled off a successful US$100 million fundraising in 2023, which it planned to use for the expansion of its operations and for the creation of innovative financial products, targeted at the underserved markets.

- The Grameen Foundation also benefited when the Bill & Melinda Gates Foundation awarded it a US$50 million grant in late 2023 towards the realisation of its vision of financial inclusion and poverty elimination through microfinance projects.

- The RBI (Reserve Bank of India) put forward a new set of regulations for MFIs in 2023 that were meant to enhance transparency and governance in the sector.

- Among other things, the new measures, such as interest rate caps and stringent reporting requirements, were introduced to ensure fair lending practices and thus the protection of the borrowers through greater monitoring.

- On the other hand, African nations have been taking steps to facilitate financial inclusion by creating new policies, giving financial assistance, and supporting microfinance institutions so that they can reach the remote and neglected areas of their populations.

Conclusion

Microfinance Statistics: Microfinance is still a powerful long-term force in the world and the key to financial inclusion, liberating millions of poor people, mainly women and young people, to establish their livelihoods. The steady growth of the sector, which is expected to exceed US$310 billion by 2025, is an indicator of its increasing role in poverty alleviation and entrepreneur creation. With a very high 96% repayment rate and soaring digital penetration, microfinance institutions show both strong performance and resilience.

On the other hand, they still face a combination of problems such as over-indebtedness, regulations, and climate change. At the same time, technology, AI, and blockchain are transforming the industry the attention is still on the same point: the balance between social impact and financial sustainability will be an important factor in the future economic empowerment and inclusive growth globally.

Sources

FAQ.

Microfinance stands for access to small loans, savings accounts, and insurance coverage for the unbanked. People can then start small businesses, finance their education, and cover their financial risks with the help of microfinance, which thus plays a vital role in poverty alleviation.

At the onset of 2024, the global microfinance market is coming to about US$279.22 billion and will continue to be a trendsetter by touching US$310.10 billion in 2025. Market studies predict that the mobile-based lending, digital innovation, and increased penetration into previously underserved communities will all lead to almost US$797 billion by 2034. This profound global demand scaling sees more than 11% annual growth in total.

Women’s role in the microfinance sector is significant as they account for approximately 70–80% of all clients. The use of microloans enables women to be entrepreneurs, assist their families, or attain financial independence. According to the research, enterprises led by women backed by MFIs grow 12% quicker than their male counterparts.

MFIs are confronted with high operating costs, borrower over-indebtedness, regulatory pressures, and climate-related risks that negatively affect repayment rates among the challenges they face. Also, the process of digital transformation is accompanied by concerns over cybersecurity and data privacy issues.

The microfinance industry is transforming with technology through digital lending, AI-driven credit scoring, and blockchain-based transparency. It is estimated that now around 25% of the loans are being digitally disbursed, thereby enhancing the efficiency and accessibility for clients residing in remote locations.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.