Isuzu Statistics By Market Share And Revenue (2026)

Updated · Apr 06, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Isuzu Motors Global Sales and Regional Growth

- Isuzu Motors Market Share Expansion

- Isuzu Motors Industrial Engine Shipments Outlook

- Isuzu Financial Performance Breakdown

- Isuzu After-Sales Revenue Growth

- Isuzu Inventory Outlook on Wholesale, Retail, and Dealer Trends

- Isuzu’s “Innovation Canvas” and Electrification Strategy (2026–2030)

- Joint Venture Analysis – UD Trucks Synergy Post-Acquisition

- Conclusion

Introduction

Isuzu Statistics: Isuzu Motors Limited has demonstrated resilience during the 2025–2026 period despite global supply chain disruptions, rising input costs, and currency fluctuations. Isuzu’s FY2025 revenue was down slightly due to Thai pickup market weakness, but FY2026 (ended March 2026) saw a recovery in the CV segment. The company maintains its long-term growth potential through its ongoing investments in emerging markets and its electrification and logistics solution development projects.

Isuzu has established itself as a major force in the automotive and mobility industries because its worldwide operations, export capabilities, and steady demand for light commercial vehicles provide essential support for its business.

Editor’s Choice

- Asia sales showed consistent progress, with sales increasing from 75K units to 76K units during FY2026.

- Fleet demand caused Japan volumes to grow from 77K units to 82K units.

- North America experienced a steep decline, which brought numbers down from 27K to 19K units because freight cycles showed weakness.

- Central & South America experienced growth from 27K to 31K units, marking a recovery.

- The African region experienced a demand surge, which brought volumes up from 19K to 26K units because of infrastructure requirements.

- The heavy-duty truck market share experienced an increase in its total from 40.1% to 41.6% of the market.

- Light-duty market share jumped from 43.5% to 51.5% despite lower volumes.

- Engine shipments will increase from 108K units to 120K units, which represents an 11.1% growth.

- The operating profit for FY2025 decreased from ¥196.8B to ¥172.5B.

- The foreign exchange (FX) impact resulted in a significant profit reduction of ¥23.0B.

- The company lost ¥15.5B in profits because of increased raw material expenses.

- The company expects after-sales revenue to reach ¥600B in 600B after growth of approximately 3.8% from the current total of ¥578B.

- The service department maintains strong service margins, which range between 15% and 20%.

- Dealer inventory decreased from 23K to 13K units, which led to better operational performance.

- The total amount of electrification investment reached ¥1 trillion from the beginning of the fiscal year until its end in FY2031.

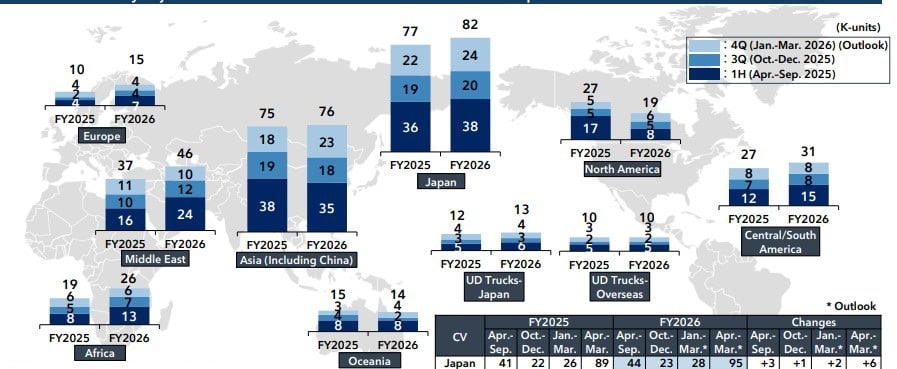

Isuzu Motors Global Sales and Regional Growth

(Source: isuzu.co.jp)

- Isuzu Motors demonstrates a balanced global growth trajectory heading into FY2026. The company achieves this growth through its geographical expansion, which maintains constant demand for commercial vehicles.

- The worldwide volume metrics display a slight increase, which different markets deliver through their essential yet strategic contributions.

- The Asian market, which includes China, functions as the primary growth engine. Its sales volume rose from 75K units in FY2025 to 76K units in FY2026 because infrastructure projects and logistics networks need expansion.

- The Japanese market, which serves as the principal domestic market, shows an increase from 77K to 82K units because replacement cycles remain stable while fleet requirements accelerate.

- North America experiences a market decrease, which declines from 27K to 19K units because the market shows weakness.

- High interest rates and cyclical freight declines have emerged as the main factors that decrease the company’s profit margins.

- The Central and South American markets experience growth from 27K to 31K units because emerging markets develop and economic conditions show improvement.

- The Middle East and African region experiences significant market expansion, especially in Africa, which increases from 19K to 26K units.

- The growth results from rising construction and mining operations in the area, which serve as a positive aspect of the situation shown for the three main search terms. regional diversification, emerging markets growth, commercial vehicle demand, and cyclical recovery.

- Additionally, UD Trucks (Japan & Overseas) maintains stable volumes (~10–13K units), indicating consistent performance in niche heavy-duty segments.

- Isuzu Motors is leveraging geographical balance and sectoral demand to offset regional volatility, positioning itself for sustainable long-term growth in global commercial vehicle markets.

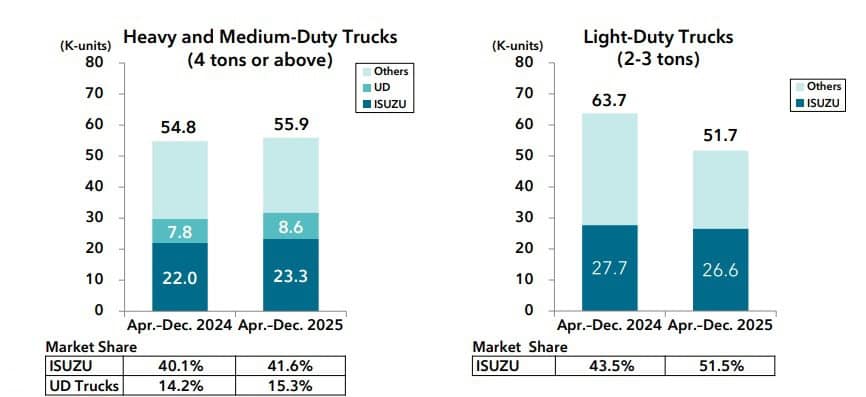

(Source: isuzu.co.jp)

- Isuzu Motors shows strong competitive advantages and market share growth in both heavy-duty and light-duty truck markets from April 2024 until December 2025.

- The heavy and medium-duty truck market experienced volume growth from 22000 units to 23300 units because ongoing infrastructure development and fleet replacement requirements drove demand.

- Isuzu increased its market share from 40.1% to 41.6%, which established its position as industry leader. UD Trucks also showed momentum, with share increasing from 14.2% to 15.3%, indicating healthy intra-group performance and segment competitiveness.

- The light-duty truck segment presents an even stronger narrative. Isuzu achieved a significant market share increase from 43.5% to 51.5%, although volumes decreased from 27.7K to 26.6K units, which shows how the market consolidated behind their brand.

- The analysis shows that Isuzu expanded its market position while competitors lost their market share, which reveals that the company maintains market dominance despite volume pressure.

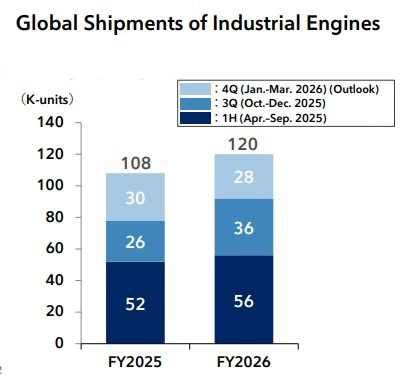

Isuzu Motors Industrial Engine Shipments Outlook

(Source: isuzu.co.jp)

- The industrial engine segment of Isuzu Motors shows continuous growth because the company maintains stable order levels that meet a variety of market needs.

- The company projects that global shipments will increase from 108K units in FY2025 to 120K units in FY2026, which represents an 11.1 % year-on-year growth that serves as a strong market recovery indication, together with rising equipment requirements.

- The shipment breakdown for 1H (Apr–Sep 2025) shows that 52K units in FY2025 increased to 56K units in FY2026 because of ongoing customer needs.

- The 3Q (Oct–Dec) volumes will increase from 26K to 36K units because of seasonal growth and supply chain improvements.

- The 4Q (Jan–Mar) outlook shows stability between 30K and 28K units, which demonstrates forecast certainty because no major changes will happen.

- Isuzu Motors develops its growth strategy through two main industry forces, which include rising industrial activity and increasing infrastructure development, to build its foundation in non-automotive powertrain markets.

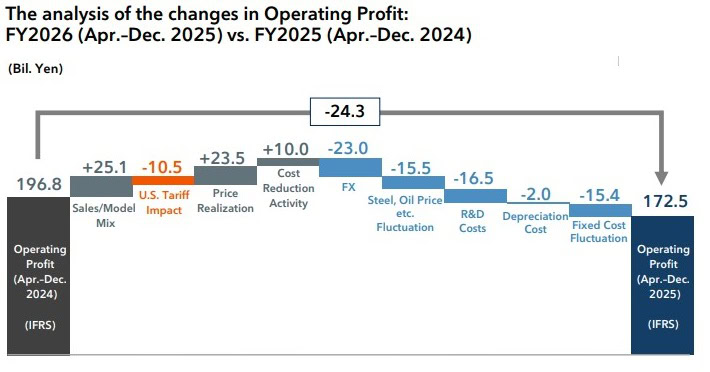

Isuzu Financial Performance Breakdown

(Source: isuzu.co.jp)

- Isuzu’s current financial report shows that operating profit has decreased by ¥24.3 billion from ¥196.8 billion in fiscal year 2024 to ¥172.5 billion in fiscal year 2025. This performance demonstrates how revenue growth factors interact with the financial difficulties presented by increasing costs.

- The positive aspect of the situation showed that sales volume and sales mix improvements brought in additional revenues of +¥25.1 billion, while companies achieved price realization gains, which brought in another +¥23.5 billion because their key markets experienced strong demand and their pricing power remained intact.

- The company achieved cost reductions through its efficiency programs, which produced savings of +10.0 billion.

- The U.S. tariff impact alone reduced profits by ¥10.5 billion, underscoring ongoing trade policy risks.

- The foreign exchange (FX) effect brought about a huge ¥23.0 billion drop, which occurred because of negative currency exchange rate movements.

- The company faced additional financial difficulties when raw material prices became unstable because of both steel and oil price hikes.

- The company experienced a financial loss of ¥15.5 billion from rising costs of steel and oil prices, while spending on research and development reached ¥16.5 billion to support its plans for future automotive development.

- The company faced extra financial challenges from both -₹15.4 billion in fixed expenses and -₹2.0 billion in asset depreciation expenses.

- Isuzu’s results demonstrate how the company attempts to achieve growth while facing economic obstacles.

- The company needs to control its expenses and manage international trade relationships and foreign exchange risks to maintain its ability to make a profit.

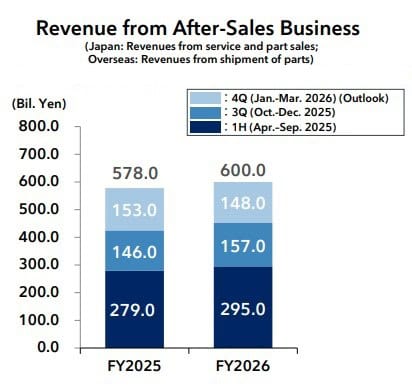

Isuzu After-Sales Revenue Growth

(Source: isuzu.co.jp)

- Isuzu’s after-sales business revenue shows continuous growth, which proves its status as a major profitable revenue source that benefits the entire automotive sector.

- Total revenue will grow from ¥578.0 billion in FY2025 to ¥600.0 billion in FY2026, according to analyst estimates, which show a yearly growth rate of about 3.8 %.

- H1 FY2026 financial results show a contribution of ¥295.0 billion, which exceeds the previous year, FY2025 total of ¥279.0 billion, because service demand and parts replacement cycles drove a 5.7 % growth.

- The Q3 FY2026 results show an increase to ¥157.0 billion, which exceeds the previous figure of ¥146.0 billion, thus demonstrating ongoing revenue growth through each quarter.

- The Q4 projections estimate a revenue decrease to ¥148.0 billion, which follows a previous projection of ¥153.0 billion, thus showing that market analysts have become more cautious about their forecasts because of supply chain changes and declining demand.

- The after-sales division generates higher operating margins, which range from 15 to 20 %, thus becoming an essential factor that drives business profitability.

- The business performance of Isuzu demonstrates that the company operates a balanced business model, which combines recurring revenue streams with customer retention efforts and lifecycle value maximization to achieve financial stability and business expansion.

Isuzu Inventory Outlook on Wholesale, Retail, and Dealer Trends

(Source: isuzu.co.jp)

- The inventory and sales pattern of Isuzu exhibits a detailed adjustment that affects wholesale operations, retail activities, and dealer stock levels.

- The company experienced a wholesale volume increase, which went from 34K units in FY2023 to 44K units in FY2024, showing a 29% annual growth rate before the volume dropped to 27K units in FY2025, which represented a 39% decrease that indicated the market reached equilibrium between supply and demand.

- The FY2026 forecast at 19K units demonstrates companies are taking a cautious approach to channel inventory, while the FY2027 projection of 30 to 35K units shows the market is entering a recovery period.

- The retail sales performance displays stable results because it increased from 26K units in FY2023 to 32K units in FY2024 with a 23% growth rate before decreasing to 29K units in FY2025 with a 9% drop.

- The market projects a recovery to 30–35K units for the FY2027 cycle because customers maintain strong demand for products, and market conditions keep improving.

- The dealers maintain inventory at controlled levels by decreasing their stock from 23K units in FY2024 to 20K units in FY2025, which represents a 13% reduction, before reaching an optimal level of 13K units in FY2026.

- The organization achieves better operational efficiency through improved inventory turnover ratios, which help decrease holding risk.

- Isuzu’s strategy enables the company to establish a sustainable recovery process through demand-supply synchronization and inventory control, along with future growth prospects.

Isuzu’s “Innovation Canvas” and Electrification Strategy (2026–2030)

- Isuzu Motors is undergoing a fundamental strategic transformation, which requires the company to change its business model from being an original equipment manufacturer to becoming a provider of commercial mobility solutions.

- The company has established its ISUZU Transformation (IX) mid-term plan, which requires all vehicle models to include carbon-neutral options by 2030. This marks a shift towards electrification, sustainable practices, and software-defined operational solutions.

- The scale of investment demonstrates that the company takes this transition process to the highest level of priority.

- Isuzu has allocated ¥1 trillion (≈ USD 6.6–7 billion) through FY2031, with ¥430 billion dedicated to R&D and decarbonization technologies, ¥350 billion to autonomous driving and connected services, and ¥180 billion to next-generation vehicles.

- The N-Series EV (Elf EV / NRR EV) serves as the main product for the company’s strategy because it provides a solution for urban logistics and last-mile delivery needs.

- The modular battery architecture provides battery configurations that range from 60 kWh to 180 kWh. This enables the system to deliver operational ranges between 66 km and 378 km, which matches fleet operators’ actual driving requirements.

- The platform achieves its maximum efficiency through the 150 kW power output, which creates a system that operates at 350V while delivering maximum efficiency, operational flexibility, and minimum payload capacity.

- The system provides fast-charging capabilities that reach 80 kW DC while offering charging windows that last between 1.2 and 1.8 hours; this feature improves the operational efficiency of fleet vehicles.

- The main element that sets Isuzu’s electrification program apart from other companies is its EVision Cycle Concept, which establishes batteries as equipment that can serve multiple purposes.

- The batteries provide more than their primary function because they serve as emergency power sources and renewable energy storage, and grid storage units in this innovative system, which combines energy systems with transportation solutions.

- Thailand serves as the main growth centre in ASEAN because Isuzu plans to invest THB 240 billion (~USD 6.6 billion) in this country.

- The EV system in Thailand contains 3720 charging stations, which will increase to 12000 stations by 2030, showing that the country can expand its electric vehicle infrastructure.

- Isuzu considers Thailand to be one of its primary markets because the country has 39 % of the ASEAN electric vehicle market and 40 % annual EV sales growth.

- Isuzu formed a battery-swapping partnership with Mitsubishi Corporation, which provides a low-cost solution that requires minimal infrastructure while solving essential problems that prevent people from adopting electric vehicles, including range anxiety, expensive initial costs, and charging problems.

- The CJPT-Asia alliance supports this project, which plans to expand its operations to Southeast Asia, including Indonesia, where the EV infrastructure is expanding fast, with charger growth at 157 %.

- Isuzu uses Australia as one of its target markets, which depends on urban fleet electrification because of ESG requirements and new regulations.

- Isuzu uses its multi-pathway strategy, which includes BEVs, FCEVs, and hybrids and hydrogen, to establish itself as a distinct player in the worldwide commercial vehicle industry.

- The company develops a practical electric vehicle system, which will grow as they tie total expenses of ownership to diesel costs in the upcoming decade.

Joint Venture Analysis – UD Trucks Synergy Post-Acquisition

|

Synergy Dimension |

Mechanism | Quantified Impact (where available) |

| Acquisition Enterprise Value | Isuzu acquires 100% of UD Trucks from the Volvo Group, cash and debt-free |

JPY 243 billion (~USD 2.2 billion)volvogroup+2 |

|

Alliance Duration |

20-year Strategic Alliance Framework with Volvo Group, overseen by Joint Alliance Board | Joint Alliance Office in Japan and Sweden; minimum 20 yearsvolvogroup+2 |

| Joint HD Common Platform | Single shared platform for GIGA + Quon HD trucks, using Volvo Group technology |

Completion 2028 per IX plan |

|

First Jointly Developed Products |

New GIGA + Quon tractor heads, launched for sale in April 2024 | First co-engineered HD trucks since the acquisition |

| Annual Synergy Value (FY2024) | Combined supply chain, R&D, manufacturing, and service efficiencies |

14 billion yen forecast in FY2024 |

|

Common Parts Purchasing & Joint Transport |

Shared logistics and purchasing across both brands’ procurement pipelines | Cost reductions underway from 2022isuzu+1 |

| I-MACS Modular Architecture | Shared component combination rules across Isuzu + UD vehicle programmes |

Enables quick/flexible spec setting; reduces unique tooling costs |

|

Combined Service Network (Japan) |

Co-located service and sales locations for both brands | Over 400 locations |

| UD Trucks 2020 Revenue | Pre-acquisition baseline |

JPY 261 billion (~SEK 23 billion)volvogroup+1 |

|

Powertrain Technology Access |

Volvo Group engine and driveline IP licensed to Isuzu/UD for fuel efficiency improvements | Real-world low/mid-load efficiency gains confirmed |

| Cummins Co-Developed MD Engines | Tochigi plant-manufactured engines for the Isuzu medium-duty range |

Incorporated in the current IX plan |

|

Earnout (performance-based) |

Additional payment to Volvo Group, subject to UD Trucks’ performance 2021–2023 |

Up to JPY 15 billion |

Conclusion

Isuzu Motors shows financial strength through its effective business operations, which succeed despite worldwide economic challenges. The company achieved growth through its diverse business operations in different regions and its increasing earnings from after-sales services, although foreign exchange price fluctuations, tariff costs, and higher input expenses affected its profitability.

The company demonstrates its competitive power through its market share increases in both heavy-duty and light-duty markets, although it experienced changes in product demand. The company established a long-term business foundation through its capital expenditures of ¥1 trillion, which support its electrification efforts, autonomous technology development, and carbon-neutrality objectives.

The organization achieved better operational efficiency through its inventory management improvements and its service-based profit enhancements. Isuzu maintains a sustainable growth path through its lifecycle value system, which targets emerging markets and its multiple electrification methods until the year 2030.

Sources

FAQ.

Sales show mixed growth, with strong gains in Asia, Japan, and Africa, offset by declines in North America.

Isuzu plans to invest ¥1 trillion (~USD 6.6–7 billion) through FY2031.

Profit fell due to FX losses (¥23B), tariffs, and rising raw material costs.

It generates high margins (15–20%) and is expected to reach ¥600B in FY2026.

Isuzu leads with 41.6% in heavy-duty and 51.5% in light-duty truck segments.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.