CFMoto Statistics By Market Share And Financial Performance (2026)

Updated · Jun 05, 2026

Table of Contents

Introduction

CFMoto Statistics: CFMoto has turned into one of the fastest-growing powersports manufacturers around, going from this more regional Chinese motorcycle builder into a real global player, for motorcycles, ATVs, side-by-sides (SSVs), and also high-end leisure vehicles. It was founded in 1989, and it sits in Hangzhou, China. Over time, the brand leaned hard into aggressive global rollout, technology alliances that feel very intentional, plus heavy R&D spending… all of that helped them land in more than 100 countries.

In 2025, CFMoto reported record sales, and that energy basically carried into the start of 2026. Now we are seeing double-digit revenue growth, better profitability, and a larger footprint in Europe, North America, Latin America, and Asia-Pacific. Their fast pace is usually linked to premium motorcycle platforms, strong ATV/UTV models, and ongoing tweaks in engine engineering.

Editor’s Choice

- In FY2025, CFMoto generated RMB 19.75 billion (USD 2.73 billion) revenue, which is a 31.3% year-over-year jump.

- Revenue is expected to climb from RMB 19.75 billion in FY25 to RMB 37.53 billion in FY28, which implies about 90% cumulative growth over the period.

- Net profit is forecast to rise from RMB 1.68 billion to RMB 3.66 billion between FY25 and FY28, nearly a 119% increase.

- Earnings per share (EPS) should more than double, moving from RMB 10.88 in FY25 to RMB 23.46 in FY28.

- Overseas revenue hit RMB 13.79 billion, so it made up 69.84% of total company revenue in FY2025.

- Motorcycle sales went up 40% in Europe, 48% in North America, and 42.9% across Latin America and ASEAN markets.

- CFMoto sold 197,000 ATV units in FY2025, giving 16.45% growth by volume, and bringing in RMB 9.61 billion in revenue.

- The company seemed to grab 74.01% of China’s overall ATV export value, so it really did reinforce its export leadership, sort of, in practice.

- CFMoto is sitting at about 25% ATV market share across Europe, and it ranks first in 17 European countries.

- When it acquired GOES Europe, it also opened up access to a dealer network, with more than 1,200 dealers spanning 17 countries… which is pretty broad.

- For ZEEHO, electric two-wheeler sales shot up by 420.2%, reaching 551,200 units, and at the same time, EV revenue jumped 381% to RMB 1.91 billion.

- Book value per share (BVPS) is forecast to climb from RMB 49.17 up to RMB 84.55 by FY28, that’s roughly 72% growth.

- Return on Equity (ROE) should improve from 15.03% in FY24 to above 27% in FY27–FY28, as overall profitability looks better on paper.

- In the U.S., tariff expenses rose 329% to RMB 978 million in FY2025, and that really weighed on profitability.

- In Q1 2026, revenue grew 26.07% to RMB 5.36 billion, but net profit rose only 1.81% to RMB 423 million, showing the margin situation is still tight.

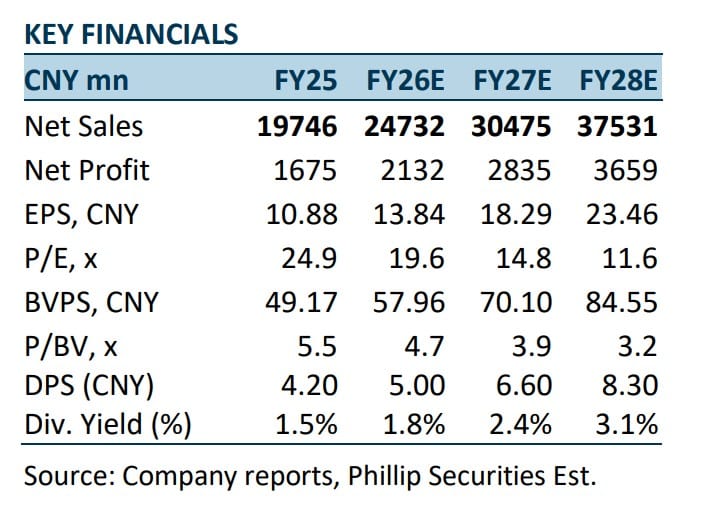

CFMoto Financial Outlook (FY25–FY28)

(Source: research.cyberquote.com.hk)

- CFMoto looks like it’s moving into a pretty powerful growth phase, with realized net sales of RMB 19.75 billion in FY25, and revenue projected at RMB 37.53 billion in FY28. That’s basically a cumulative climb of about 90% in only three years, which is hard to ignore.

- Revenue growth is also expected to stay steady and strong, going from RMB 24.73 billion in FY26 to RMB 30.48 billion in FY27, and then to RMB 37.53 billion in FY28. This seems to track the expanding worldwide appetite for CFMoto motorcycles, ATVs, side-by-sides, and also premium recreation vehicles.

- Profitability, meanwhile, is forecast to rise even faster than the top line, with net profit moving from RMB 1.68 billion in FY25 to RMB 3.66 billion in FY28, a very striking increase of nearly 119%.

- The implication there is improving operating leverage and a more favorable product mix, kind of the whole package.

- On a per-share basis, earnings per share (EPS) are projected to grow from RMB 10.88 in FY25 to RMB 23.46 in FY28.

- One of the more interesting signals is valuation compression. Specifically, the price-to-earnings (P/E) ratio is expected to slide from 24.9x in FY25 down to 11.6x in FY28, implying that earnings should expand far quicker than the share price is appreciating.

- Even the balance sheet keeps strengthening, since book value per share (BVPS) is forecast to move up from RMB 49.17 to RMB 84.55, roughly a 72% rise.

- And for shareholders, returns are anticipated to get better too. Dividends per share (DPS) are projected to increase from RMB 4.20 to RMB 8.30, while dividend yield improves from 1.5% to 3.1% by FY28.

- Overall, the forecasts portray CFMoto as a rapidly expanding global powersports manufacturer combining double-digit revenue growth, accelerating profitability, stronger book value, and rising dividends, positioning the company.

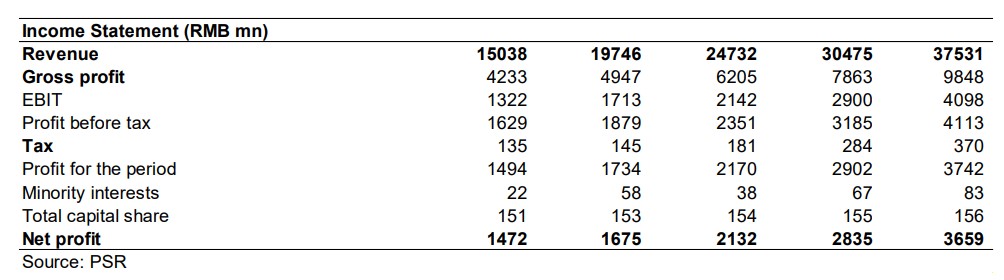

CFMoto Financial Performance and Earnings Outlook

(Source: research.cyberquote.com.hk)

- CFMoto seems to be walking into a phase of pretty robust expansion, with revenue expected to move from RMB 15.04 billion in FY24 up to RMB 37.53 billion in FY28.

- The strong 149.6% jump over four years, and it basically points to the company’s growing worldwide footprint across motorcycles, ATVs, and powersports vehicles—yeah, not just “local” anymore.

- On the numbers side, revenue is projected to climb in a fairly steady way, starting at RMB 19.75 billion in FY25 and then rising to RMB 24.73 billion in FY26, RMB 30.48 billion in FY27, and finally RMB 37.53 billion in FY28.

- Gross profit is also looking notably stronger, almost doubling, from RMB 4.95 billion in FY25 to RMB 9.85 billion by FY28. So it’s not only that more units are being shifted, but CFMoto is also generating more value per unit sold, which matters.

- Operating performance keeps improving too, with EBIT forecast to grow from RMB 1.71 billion in FY25 to RMB 4.10 billion in FY28. That’s roughly a 139% increase, and it indicates better operational efficiency, plus the benefit of economies of scale kicking in over time.

- Profit before tax is expected to rise from RMB 1.88 billion in FY25 to RMB 4.11 billion in FY28, while tax expenses stay relatively controlled. In other words, earnings growth looks healthy, without too much drag from taxes.

- Net profit is anticipated to surge from RMB 1.68 billion in FY25 to RMB 3.66 billion by FY28, which comes out to nearly 118% growth. And interestingly, it grows faster than revenue, so margin improvement is likely doing some of the heavy lifting there.

- From a shareholder value perspective, it’s also pretty clear. Total capital shares are basically flat, only nudging from 153 million to 156 million, which suggests most of the earnings growth is driven by how the business performs rather than dilution.

- Overall, these projections make it seem like CFMoto is shifting from being a quick-growing regional manufacturer into a globally competitive powersports brand, backed by strong revenue

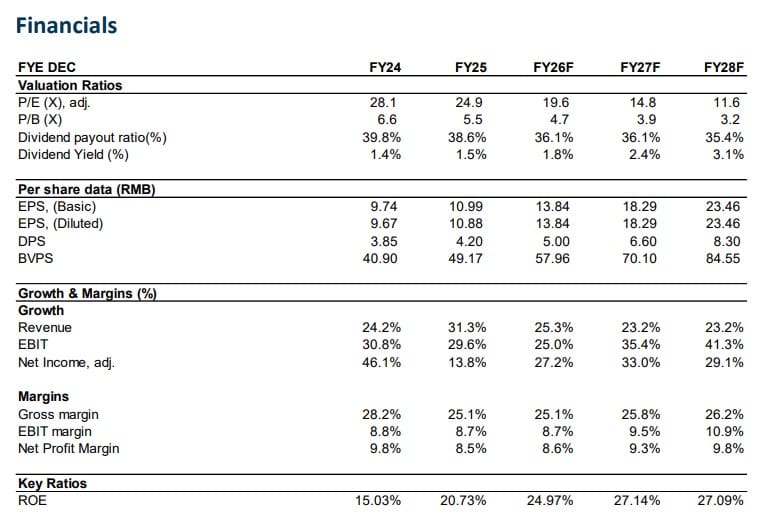

CFMoto Strong Growth Engine with Expanding Profitability

(Source: research.cyberquote.com.hk)

- CFMoto’s valuation looks pretty much more compelling every quarter, with the adjusted P/E ratio expected to slip from 28.1x in FY24 down to 11.6x by FY28F—so earnings should outpace the share price growth, which feels like a good tailwind for long-term investors, even if it takes time.

- The earnings momentum is still quite strong, with basic EPS forecast to move from RMB 9.74 in FY24 to RMB 23.46 by FY28F, basically a cumulative jump of around 141%, and that underlines the company’s ability to turn revenue into profit.

- On the top line, revenue growth is projected to stay punchy at 31.3% in FY25, then hold in a healthy 23–25% band through FY28F. This suggests sustained appetite for CFMoto’s motorcycles, ATVs, and powersports products.

- Profitability also seems to be tightening up steadily, since EBIT is expected to grow 29.6% in FY25, then speed up to 41.3% by FY28F. That pattern points to better operating leverage, plus improved effectiveness across the business.

- Adjusted net income growth stays convincing too, forecast at 27.2% in FY26F, 33.0% in FY27F, and 29.1% in FY28F, so expansion continues even after already-high growth levels.

- Shareholder returns are getting better alongside those fundamentals. DPS is projected to rise from RMB 3.85 to RMB 8.30 between FY24 and FY28F, meaning it more than doubles over the forecast stretch.

- Dividend yield should also move up, from 1.4% in FY24 to 3.1% by FY28F, so the stock may become more interesting to investors who want both growth and some income, not only one side.

- Finally, book value per share is expected to increase from RMB 40.90 to RMB 84.55, which reflects balance-sheet strengthening and a higher level of shareholder equity overall.

- Return on Equity is one of the more standout metrics, moving up from 15.03% in FY24 to over 27% by FY27F–FY28F, so it looks like management is pulling in meaningfully more profit from each yuan of shareholder capital.

- Meanwhile, gross margins are expected to stay broadly steady near 25–26%, but the EBIT margin is projected to rise from 8.8% to 10.9%, which usually hints at tighter cost control and better operating efficiency, kinda like a more efficient engine room.

- Net profit margin is forecast to bounce back from 8.5% in FY25 to 9.8% in FY28F, and that supports the view of sustainable profitability progress even while new investments keep rolling in.

- Overall, CFMoto is combining strong double-digit revenue growth, margin expansion, a higher ROE, growing dividends, and a notably lower valuation multiple, creating a fairly compelling mix of growth and value that frames the company as a potentially attractive participant in the global powersports industry

(Source: CFMoto 2025 Annual Report and FY26–FY28F estimates to the Phillip Securities April 30, 2026, Equity Research Report.)

- During FY2025, CFMoto delivered one of the better growth narratives in the global powersports space, with total revenue hitting RMB 19.75 billion (USD 2.73 billion).

- 3% year-on-year uplift, and it outpaced the broader industry’s projected growth rate by quite a bit.

- Export markets have turned into the backbone of the business, with overseas revenue rising to RMB 13.79 billion, or 69.84% of total revenue.

- So basically, nearly 7 out of every 10 yuan earned by CFMoto comes from outside China, not from domestic sales.

- Domestic revenue was still quite substantial, around RMB 5.96 billion, with demand that keeps expanding for the company’s NK, MT, SR, and ZEEHO product families in China.

- At the same time, CFMoto’s wider global footprint grew across several regions, not just one place, and motorcycle sales went up 40% in Europe, 48% in North America, and 42.9% in both Latin America and ASEAN.

- North America continues to be one of the bigger growth engines, and CFMoto now runs through a network of more than 700 dealerships.

- For profitability, the ATV and side-by-side segment is still the most robust growth pillar. In FY2025, the company sold 197,000 ATV units, which is up 16.45% year-over-year, and those sales generated RMB 9.61 billion in revenue. That’s a remarkable 33.26% rise, frankly, in a pretty short stretch.

- Also, the company’s ATV export position is unusual, in a good way: it captured 74.01% of China’s total ATV export value, so effectively CFMoto is the major driver behind the country’s global ATV exports.

- Europe remains the strongest international ATV market too, where CFMoto holds about 25% market share, and it is number-one in 17 European countries, including Germany, Austria, Spain, Sweden, Portugal, Estonia, and the Czech Republic.

- The acquisition of GOES Europe kinda strengthened this position… by giving access to a distribution network of more than 1,200 dealers spread across 17 European countries.

- Electrification is also turning into another big growth catalyst, with the ZEEHO EV brand selling 551,200 electric two-wheelers in FY2025.

- An extraordinary 420.2% jump, while revenue climbed 381% to RMB 1.91 billion. So in practice, it now sits among the fastest-growing EV two-wheeler brands globally.

- Even after the end of its long-standing European distribution partnership with Pierer Mobility in 2025, CFMoto managed to shift toward dedicated distribution channels.

- Looking ahead, CFMoto seems exceptionally well placed to benefit from the expanding global ATV market, which is projected to grow from USD 5.88 billion in 2025 to USD 13.09 billion by 2035.

- With export strength, ATV leadership, dealer expansion, and EV growth working together, there is a solid base for continued global market-share gains.

- CFMoto delivered yet another year of impressive expansion in FY2025, but under that strong revenue momentum, there’s this quieter tale of cost pressures mounting, which then slows how well profit is converted… really, it shows the gap between growth and actual profitability.

- Revenue rose 31.3% year-over-year to RMB 19.746 billion, meaning CFMoto keeps taking market share quicker than the broader global powersports industry, and that wider sector is expected to grow at a much slower pace in the years ahead.

- The most obvious profitability headache came from U.S. trade tariffs. Additional tariff expenses jumped to RMB 978 million in FY2025, which is up 329% from RMB 228 million in FY2024, so yeah, it’s not a small bump.

- Gross margin fell by 3.12 percentage points to 26.94% from roughly 30.06% a year earlier, and that also trimmed the likely gross profit by an estimated RMB 616 million.

- On top of that, currency moves added friction. The Chinese Renminbi strengthened about 4.3% versus the U.S. dollar during 2025, which lowers the translated value of overseas earnings when they are brought back into RMB.

- This FX drag matters a lot because overseas revenue was RMB 13.79 billion and made up 69.84% of total company revenue, so exchange rate fluctuations effectively become a major profitability driver.

- Despite the challenges, CFMoto kinda showed resilience in Q1 2026, with revenue landing at RMB 5.359 billion, up 26.07% year over year.

- Meanwhile, net profit attributable to shareholders rose only 1.81% to RMB 423 million.

- That gap between 26.07% revenue growth and just 1.81% profit growth really makes it pretty clear that tariffs and currency pressures are still diluting the earnings momentum, even with sales doing well.

- If you compare CFMoto against global makers like Honda, Yamaha, and BMW, all of whom have also mentioned tariff-linked earnings strain, it suggests CFMoto has maintained decent operational discipline in a tough international trade setting.

- The GOES Europe acquisition brings some extra strategic wiggle room for potential European assembly work later on, which could, in turn, reduce tariff exposure and help strengthen long-term competitiveness in global markets.

- CFMoto is still a high-growth powersports leader, but FY2025 and Q1 2026 together suggest future earnings will depend on more than just sales growth.

Conclusion

CFMoto, kind of like it has positioned itself as one of the faster-growing powersports manufacturers worldwide, with a mix of solid overseas expansion, improving profitability, and gains in market share… more and more. In FY2025, the company seemed to show serious momentum, mostly lifted by export growth, ATV leadership, and the quick rise of its ZEEHO electric mobility business. Looking forward through FY2028 forecasts suggest it keeps that double-digit revenue growth vibe, earnings should keep climbing, shareholder returns get stronger, and operational efficiency improves too.

Still, there are headwinds—higher tariff costs and foreign-exchange pressures, which are basically the main issues that can soften profit expansion a bit. Taken all together, CFMoto’s global diversification, product innovation, electrification push, and export strength it leaves the company well placed for steady long-term growth.

FAQ.

CFMoto generated RMB 19.75 billion (USUSD 2.73 billion) in revenue during FY2025.

Overseas revenue made up 69.84% of total revenue, which equals RMB 13.79 billion in FY2025.

CFMoto sold around 197,000 ATV units, up 16.45% year-over-year.

ZEEHO electric two-wheelers sales rose 420.2% to 551,200 units, while EV revenue increased 381% to RMB 1.91 billion.

Expected revenue to land near RMB 37.53 billion by FY2028, basically close to double the FY2025 levels.

Joseph D'Souza founded ElectroIQ in 2010 as a personal project to share his insights and experiences with tech gadgets. Over time, it has grown into a well-regarded tech blog, known for its in-depth technology trends, smartphone reviews and app-related statistics.