FinTech Statistics By Blockchain, Artificial intelligence and Facts (2025)

Updated · Sep 13, 2025

Table of Contents

- Introduction

- Editor’s Choice

- General Facts

- Global Funding Activity In Fintech

- Market Capitalization of Fintech Companies

- Fitech Market Size

- Fintech Market Growth By Segments

- Fintech Adoption Rates

- Regional Difference of Fintech Adoption

- Fintech AI Integration

- Leading The Fast – Growing Fintech Categories

- Fintech Startups

- Fintech Investment

- Largest Fintech Companies Global

- eWallet Statistics

- Loan Lending Overview

- Mobile Banking Overview

- Fintech Blockchain Statistics

- Cybersecurity In Fintech

- Future of FinTech Statistics

- Conclusion

Introduction

FinTech Statistics: Throughout 2024, financial technology (fintech) shaped new digital avenues for the use, storage, borrowing, and investing of money. Even amidst elevated interest rates and geopolitical challenges, users adopted digital payments, real-time money transfers, and mobile-first banking in increasing numbers.

This article will discuss the important FinTech statistics in 2025—funding, payments, open banking, neobanks, remittances, and policy—assembled with plain language, precise percentages, and dollar amounts.

Editor’s Choice

- During the first half of 2025, investments in fintech worldwide diminished to US$44.7 billion.

- The large payment networks continue to dominate the fintech landscape, with Visa holding a market capitalisation of US$662.6 billion in 2025 (up from US$547 billion in 2024).

- Mastercard at US$346.3 billion in 2025 (down from US$389 billion in 2024).

- A staggering 96% of global users are familiar with at least one fintech product, and approximately 64% of consumers worldwide make use of these services, compared with 46% in the United States.

- By 2028, with a CAGR of 16.8%, the global fintech app market is estimated to grow to US$492 billion, reaffirming fintech as a lasting innovation in financial services.

- Digital payments globally foresee 5.48 billion users and US$14.78 trillion in transaction value by 2028. By 2027, neobanking transactions are expected to hit the US$9.2 trillion mark.

- AI in fintech is expected to enhance risk management and customer service and grow to US$70.1 billion by 2033.

- By 2030, open banking is expected to reach US$135.17 billion, and embedded finance has the potential to reach US$291.3 billion by 2033.

- InsurTech, which was valued at US$22.1 billion in 2023, is set to grow to US$306.5 billion in 2030, marking a CAGR of 45.6%.

- By 2034, BNPL services are set to explode to US$80.2 billion, growing from US$14.55 billion in 2024.

- The number of fintech startups is expected to reach 29,955 in 2025, an increase from 12,131 in 2018, while the U.S. is predicted to dominate with more than 13,100 startups.

- FinTech financings hit a US$229.6 billion all-time high by 2021, fueled in part by the COVID-19 pandemic, but their value dropped to US$106.2 billion in 2024 and is expected to decline further in 2025.

General Facts

- The small niche of startups around fintech has now transformed into a global ecosystem of multibillion-dollar companies.

- The number of firms in the fintech sector has increased tremendously, particularly in North America and Europe.

- Looking at 2024, the number of global fintech users has increased significantly, with over three billion people using digital payments. In 2024, the slowdown in investment activity that started in 2022, in the face of increasing user and company growth, has started to stabilise.

- There isn’t a single definition for fintech since it includes digital banking, payments, blockchain, insurtech, wealthtech, AI, and more.

- Artificial intelligence is being discussed for its uses in fraud detection, providing financial advice, and other efficiency improvements.

- Open finance has improved data sharing between financial institutions, and regulation has fostered its use in most jurisdictions.

- After fintech investments reached their highest point in 2021, they dropped severely. The drop, however, was reduced by 2024, which makes it appear that it might stabilise.

- Despite the general decline, increased investments were made in payments, wealthtech, and regtech in 2024.

- Due to central bank interest rate cuts, the reduction of M&A and venture capital activities has slowed down.

- The industry is no longer moving at a breakneck speed but is transitioning to more sustainable growth.

- Between 2025 and 2028, we expect open finance and AI to catalyse new fintech developments.

- Fintech is shifting global finances strategically, even though the early explosive growth phase is over.

- While advanced economies such as the EU, Brazil, and Australia have adopted comprehensive open finance frameworks, emerging countries are following more limited paths.

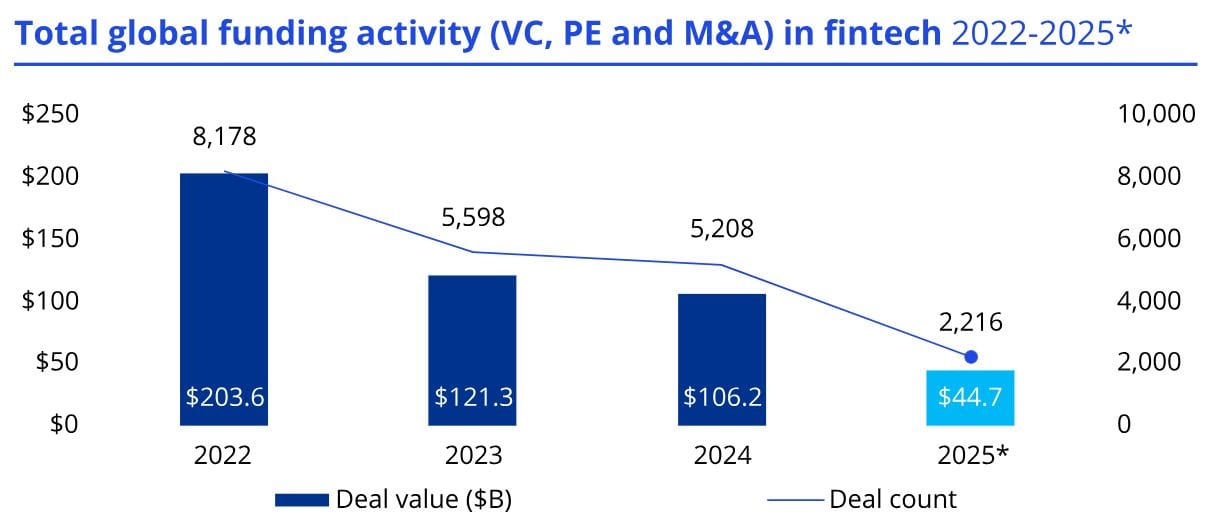

Global Funding Activity In Fintech

(Source: kpmg.com)

- As per the KPMG report, FinTech statistics state that the volume of investments secured by fintech companies reached a mere US$44.7 billion in the first half of 2025, recording the weakest six-month period since early 2020.

- The decline can be attributed, to a very large extent, to the higher interest rate regime in place.

- Higher interest rates not only increase the cost of borrowing but also compel investors to seek safer bets as opposed to the ‘spray and pray’ style of investing.

- While at the start of 2025, there appeared to be some guarded optimism, the mixture of fresh geopolitical strife compounded with changes in U.S. tariff and trade regulations led to a bigger cloud of uncertainty and dissent among investors on the willingness to commit sizable capital.

- The deceleration became particularly apparent in Q2, during which investment totalled just US$18.7 billion over 972 deals.

- The number of deals is the lowest we have witnessed since Q3 of 2017.

- This demonstrates the extent of the withdrawal from the market, with investors exhibiting a significantly more cautious and selective strategy.

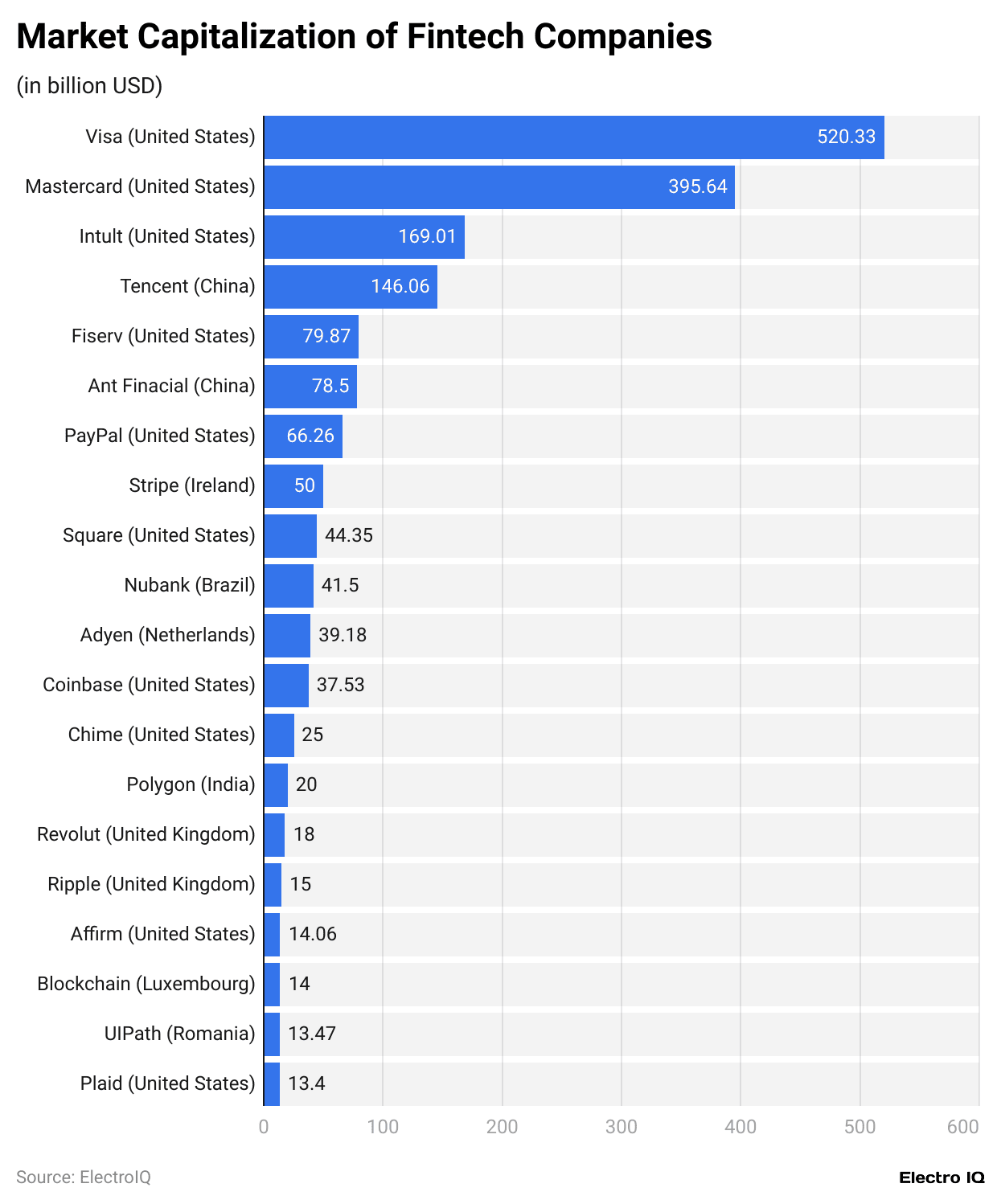

Market Capitalization of Fintech Companies

(Reference: nimbleappgenie.com)

- As per Nimbleappgenic, FinTech statistics show that in 2024, Visa dominated as the world’s largest fintech company, boasting a market cap of US$547 billion.

- Trailing behind was Mastercard in second place, with US$389 billion in market cap.

- The figures underline the ongoing dominance of payment networks within the fintech sector worldwide.

- Fintech usage on the consumer side has demonstrated marked growth globally. Approximately 64% of consumers worldwide utilise fintech, compared to 46% in the United States.

- In a Forbes survey, close to three in four respondents (74.4%) indicated willingness to use fintech products from big tech, implying that technology companies may have a competitive advantage over traditional lenders in meeting client expectations.

- Outside of Visa and Mastercard, there are more than 25 fintech companies valued at US$10 billion or more, known as “decacorns.”

- The United States leads the fintech sector, hosting half of the world’s top 20 fintech companies by market capitalisation.

- Nine of them are U.S. companies, which highlights the country’s clear leadership.

- In addition to the U.S., China makes a notable contribution to the fintech sector, with two companies ranked in the global top 20, taking the third and fifth places for market value.

- The United Kingdom also has two companies listed among the top fintech firms.

- Furthermore, countries such as Ireland, Brazil, the Netherlands, India, Israel, Singapore, and Luxembourg each have at least one fintech company ranked among the top 20.

- Collectively, this demonstrates that although the U.S. continues to dominate the fintech sector, other parts of the world are gradually establishing a stronger foothold, as fintech innovation and high-value companies exist on several continents.

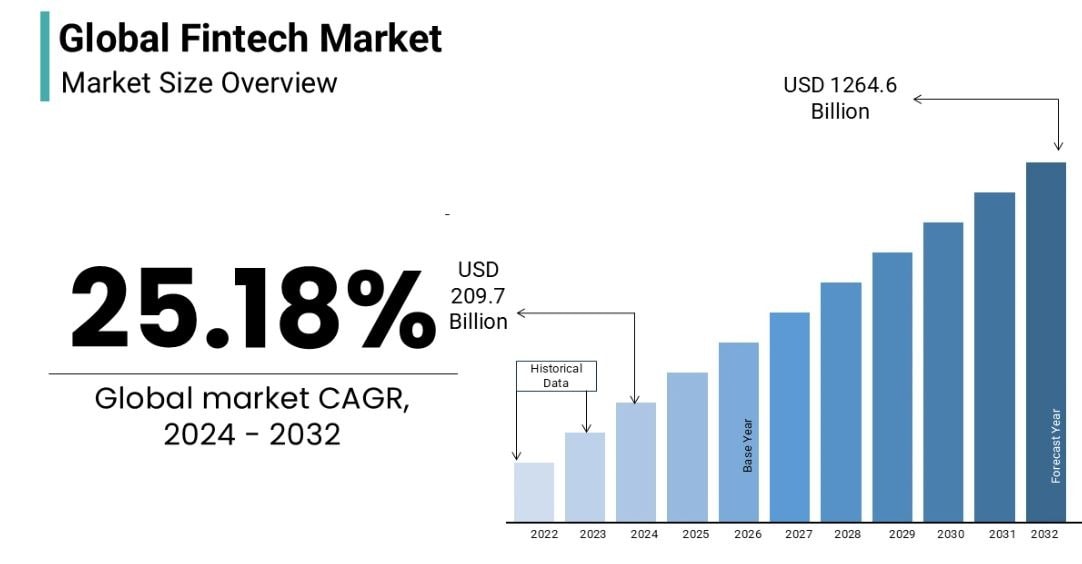

Fitech Market Size

(Source: nimbleappgenie.com)

- The fintech application market is changing rapidly and is set to dominate the future landscape of the global financial sector.

- According to a report, by 2028, the fintech market is expected to grow to US$492 billion, with a strong CAGR of 16.8%.

- This rate of growth demonstrates that fintech is not a short-term change but a fundamentally new approach to managing, transferring, and investing money.

- This expectation shows that the fintech market is set to gain an increasingly important role in global financial services in the future because of its ability to provide truly digital, swift, and user-friendly alternatives to the dated legacy systems.

Fintech Market Growth By Segments

(Source: nimbleappgenie.com)

- The global fintech sector has made double-digit progress in the last several years, as its revenue has more than doubled to reach US$190 billion in 2022, having stood at US$90.5 billion around 2017.

- Such remarkable growth demonstrates the success of fintech in redefining the financial ecosystem and becoming a vital part of the global economy.

- Neobanks operating fully digital banks without any physical branches are one of the fastest-growing sectors.

- By 2027, neobanking transactions are estimated to rise to US$9.2 trillion, illustrating a clear shift towards mobile and app-based banking.

- Digital payments mark the strongest impetus behind fintech adoption.

- With a projected transaction value of US$14.78 trillion by 2028, it is evident that people across the globe are looking for quicker, safer, and more efficient payment methods.

- With a US$179 billion mark, the overall fintech market is already well established and is on track to reach US$324 billion by 2028, as per Statista.

- This gradual increase accentuates fintech’s position as one of the most impactful and robust markets in the world.

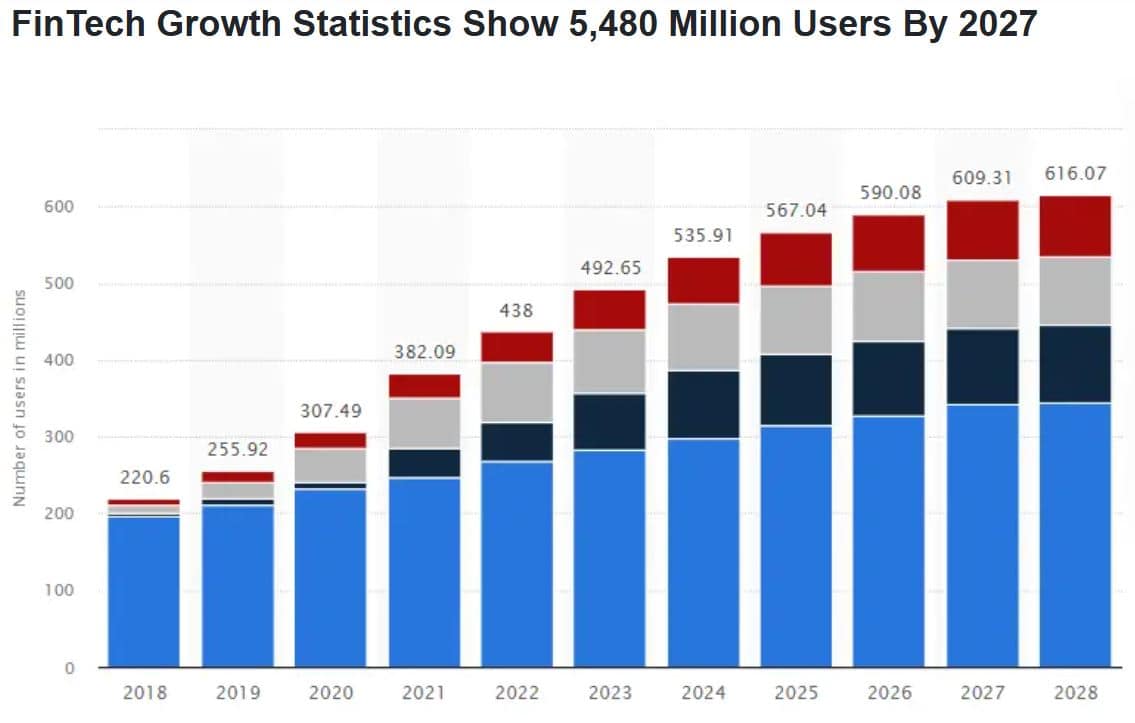

- By 2027, the number of individuals utilising digital payments globally is projected to hit 5.48 billion, highlighting the extent to which fintech is embraced.

- The data dispels any doubts: not only is fintech growing in monetary terms, it is integrating itself into the everyday routines of billions of people globally.

Fintech Adoption Rates

- Now, FinTech is everywhere, and the demand for quicker, more secure, and usually cheaper alternatives to traditional financial services has spawned their global adoption.

- Approximately 64% of the population now uses fintech services globally.

- Although the United States slightly falls behind with an adoption rate of 46%, nearly all Americans, 96%, are aware of at least one fintech service.

- When evaluating different service sectors, the foremost is payment and money transfer services, used by 75% of global customers.

- The adoption of insurance fintech products has also increased markedly, with 48% of customers using them.

- Moreover, small and medium-sized enterprises (SMEs) are increasingly seeking fintech assistance, with 25% of SMEs worldwide already employing fintech services.

- At 23%, the adoption rate among U.S. SMEs is lagging just behind the global average.

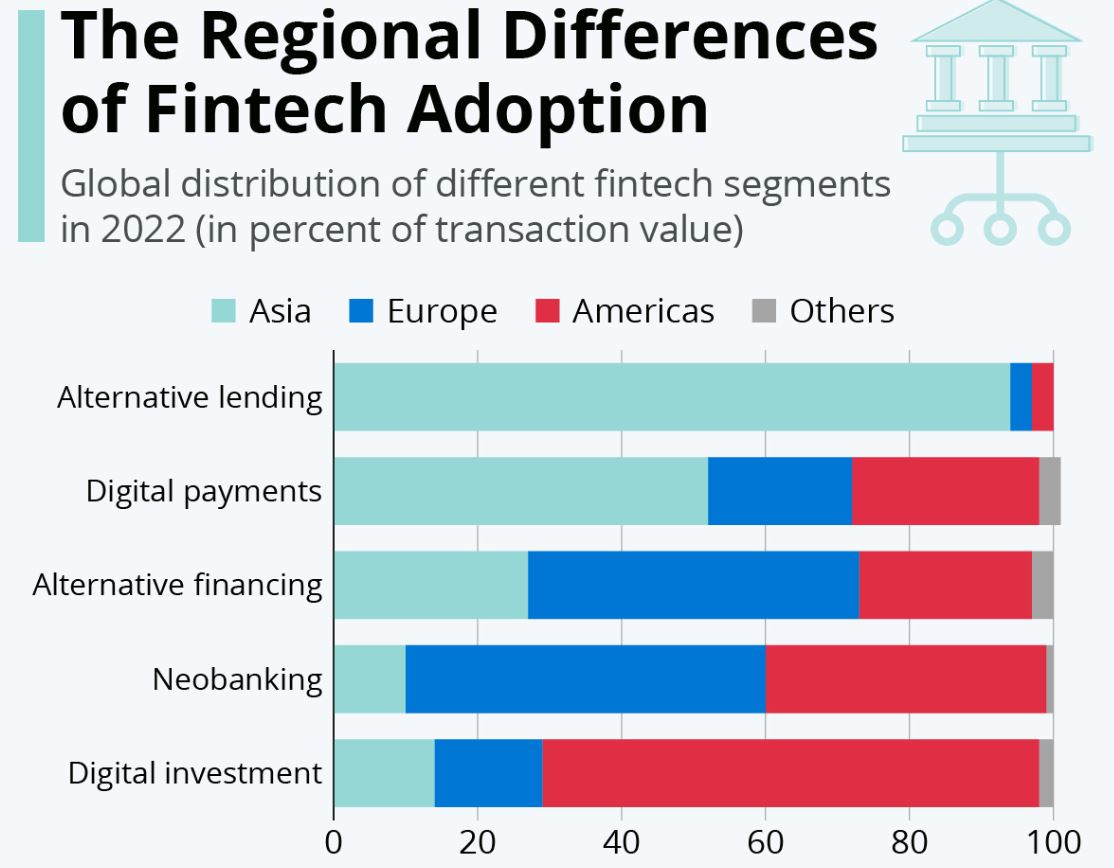

Regional Difference of Fintech Adoption

(Source: statista.com)

- Fintech is developing globally, but each region has its own style and focus.

- The information from Statista’s Digital Market Outlook illustrates the variability in the distribution of fintech globally.

- Asia stands out in digital payments and alternative lending.

- In fact, more than half of the digital payment transaction value worldwide in 2022 was from Asia.

- This underlines the region’s adoption of mobile payments, super apps, and real-time transfer systems.

- The region’s alternative lending segment is even more pronounced, accounting for 94% of the global transaction value.

- While this segment is booming, it does face criticism due to the potential risks associated with borrowing outside of traditional banks, especially when regulations are lax.

- In contrast, the rest of Europe becomes the focal point for advanced alternative financing such as crowdfunding and peer-to-peer financing.

- At the same time, the rest of the Americas, notably the United States, take the lead in digital investing.

- There, consumers and companies actively use online brokerage services, robo-advisors, and even app-based wealth management tools.

- The data emphasise that the specific use cases and success metrics of fintech firms in a particular region depend largely on the region’s specific needs, infrastructure, and regulatory landscape.

- Fintech firms in different parts of the world adopt their services for different purposes and are successful on different parameters.

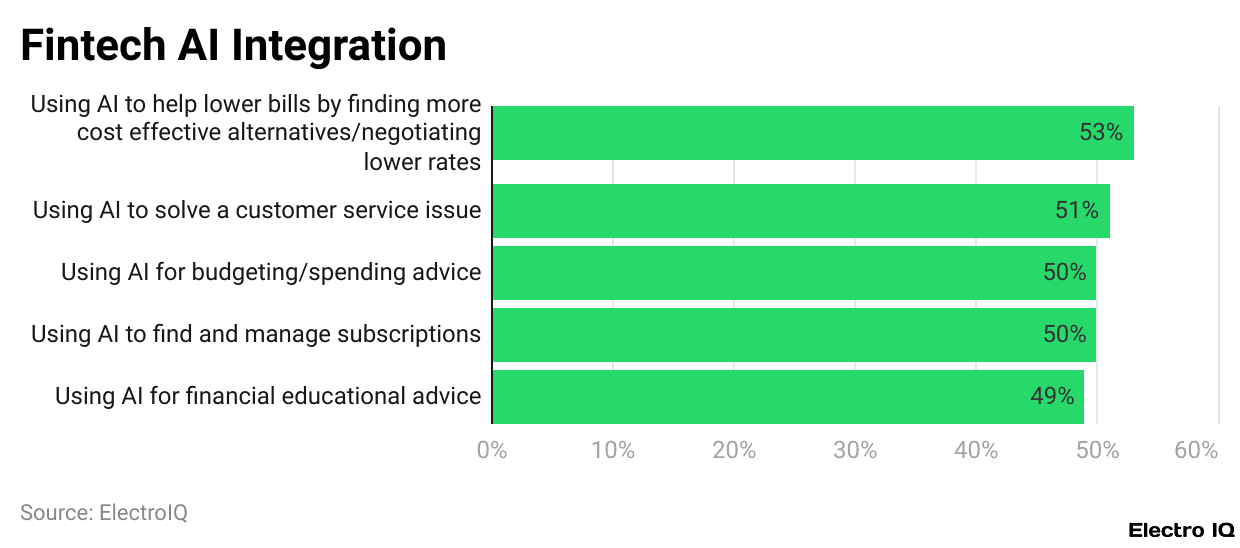

Fintech AI Integration

(Reference: omnius.so)

- Look at one of the biggest trends in fintech, and you will notice the fintech industry integrating artificial intelligence from risk management to personalised customer services.

- In the year 2024, AI in fintech was worth US$17 billion and is forecasted to reach US$70.1 billion by the end of 2033.

- Companies such as JPMorgan Chase, Goldman Sachs, and Nubank are not only keeping pace but setting the standards.

- In return, Zest AI has shown how potent this technology can be by improving customer experience as much as 70% in loan process acceleration.

- In addition to technology, consumers are now gravitating more towards companies implementing green initiatives, which is sustainability’s focal point.

- For instance, Aspiration has managed to gain more than a million customers by providing products that promote environmentally responsible spending and investing.

- Regulation, on the other hand, is critical since greater control in North America and Europe requires faster adaptation by fintech companies.

- The majority of fintech companies (80%) have increased their compliance budgets in 2024, with Revolut and N26 paying active attention to requirements intended to improve organisational resilience.

- At the same time, embedded finance is on the rise, enabling non-financial companies to embed financial services within their platforms, a US$7.2 billion revenue market by 2030, as stated by DashDevs.

- In addition, generative AI is supporting these changes by augmenting productivity in fintech-related programming, customer support, and digital marketing.

- Given their lean operational models, fintechs stand to gain the most benefits from these innovations as compared to traditional banks, and that, in the short term.

Leading The Fast – Growing Fintech Categories

Digital Banking and Neobanks

- The emergence of neobanks and digital banking marked an accelerated expansion in 2024.

- It is estimated that the user base of neobanks will rise to 386.30 million by 2028, with an average annual growth rate of 13.7% between 2021 and 2028.

- PayPal, Square, and Alipay are notable players in this sector, providing mobile-first, branchless banking solutions that resonate with the younger, tech-savvy demographic.

Artificial Intelligence (AI) and Machine Learning

- AI is now integrated in fintech to enhance risk and fraud management and provide tailored financial solutions.

- In 2024, the AI market in fintech was estimated to be worth US$17 billion and is expected to increase to US$70.1 billion by 2033, growing at a CAGR of 17%.

- Prominent firms such as JPMorgan Chase, Goldman Sachs, and Nubank have implemented AI to optimise their operations and customer experience.

Blockchain Technology

- The use of blockchain technology in fintech is spearheaded by cryptocurrency exchanges, cross border payments, and decentralised finance (DeFi) platforms.

- From 2024 to 2029, the fintech blockchain market will likely grow at an astounding CAGR of 46.92%, expanding to US$31.84 billion by 2029.

- Coinbase, Ripple, Binance, Kraken, and Gemini have cemented their positions as leaders in this field.

RegTech (Regulatory Technology)

- As compliance demands increase, regulatory technology has become a fast-growing fintech category.

- The RegTech market is expected to reach US$14.26 billion in 2024 and grow at a CAGR of 22.6% through 2032.

- Companies like ComplyAdvantage, Trunomi, ClauseMatch, Elliptic, and Behavox are pioneering the development of tools that simplify financial institutions’ compliance and regulatory risk management.

Embedded Finance

- Embedded finance—where non-financial platforms offer payments, lending, or insurance—is fundamentally reshaping the e-commerce and retail sectors.

- The global embedded finance market is expected to increase at a CAGR of 15.8%, from US$63.2 billion in 2023 to US$291.3 billion in 2033.

- Some of the leading companies in this industry are Apple, Amazon, Plaid, Shopify, and Stripe.

Open Banking

- Open banking enables consumers to grant third-party providers secure access to their financial data, and it is rapidly being adopted worldwide.

- From 2023 to 2030, the CAGR is estimated to be 27.2% and the global open banking market is expected to reach US$135.17 billion by 2030.

- Plaid, Revolut, HSBC, Barclays, and BBVA are notable ecosystem builders who make banking more integrated and competitive.

InsurTech

- The fastest-growing fintech category today is insurance technology, or InsurTech.

- The market is expected to grow with a CAGR of 45.6% from US$22.1 billion in 2023 to nearly US$306.5 billion in 2030.

- Startups such as Lemonade, Hippo, Root Insurance, Wefox, and Trov are revolutionising the outdated insurance sector with AI-powered claims management, customised pricing, and mobile-first solutions.

Buy Now, Pay Later (BNPL)

- The BNPL industry has evolved into a widely accepted payment method, offering shoppers flexible short-term credit at the point of sale.

- The worldwide BNPL industry is expected to be US$14.55 billion in 2024 and may grow to US$80.2 billion by 2034, with a CAGR of 21.8%.

- Leading providers include Klarna, Afterpay, Affirm, Zip, and Sezzle, who continue to attract millions of users worldwide.

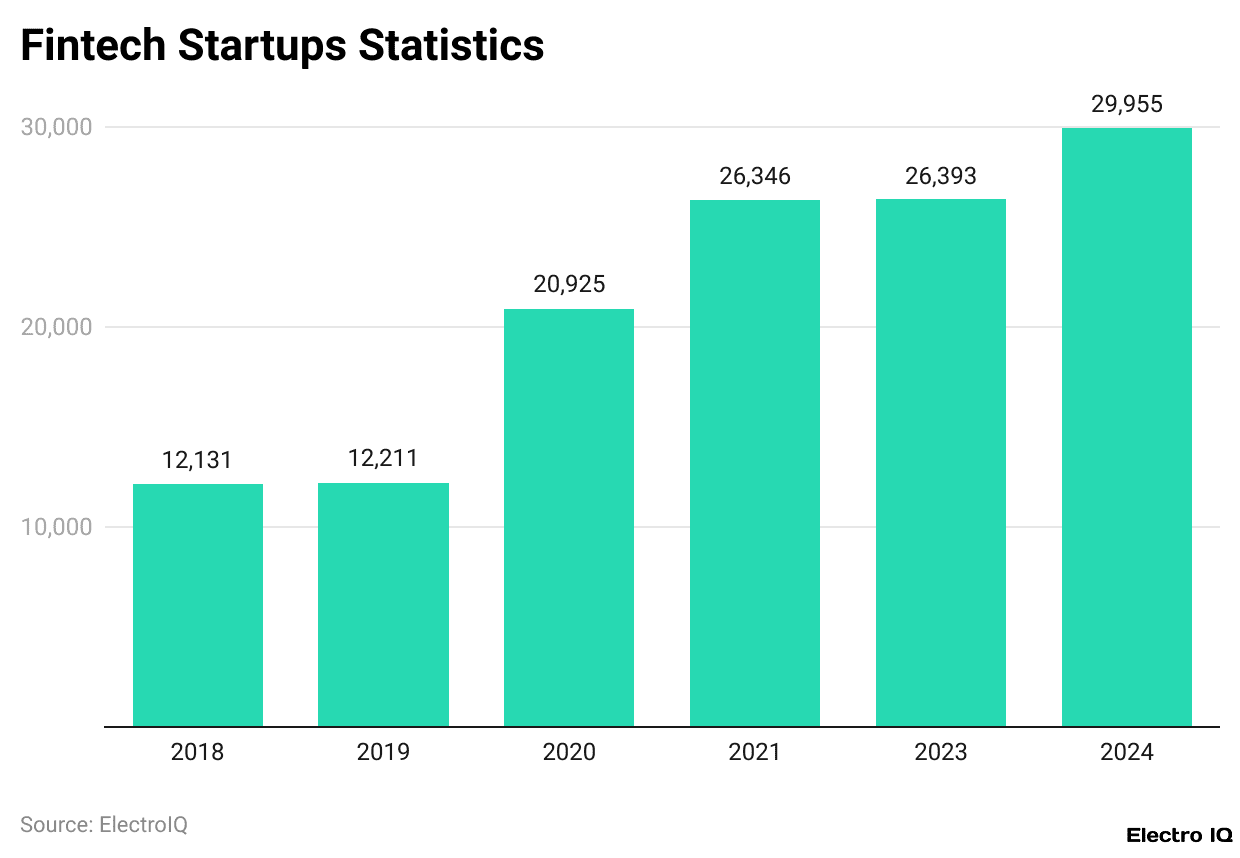

Fintech Startups

(Reference: demandsage.com)

- Looking at 2025, the total number of fintech startups will be upward of 29,955 worldwide, which further emphasises the growth of this sector in recent years.

- Today, there are more than double the number of fintech startups that existed in 2018, which has a record of 12,131.

- This number was almost unchanged in 2019 when it was recorded at 12,211.

- The number of startups leapt in 2020 when it was recorded at 20,925 and continued to grow to 26,346 in 2021.

- The number reached 26,393 in 2023 and further increased to nearly 29,955 in 2024.

- This clearly demonstrates how the fintech sector is among the most fast-paced sectors to grow globally.

- The rest of the world may have some catching up to do, but in the EMEA region (Europe, the Middle East, and Africa), there are already 10,696 fintech startups, demonstrating their strength.

- Europe alone has around 9,200 fintech companies, placing it as the second-largest hub after North America.

- Numbers indicate consistent improvement, with the EMEA region increasing from 3,581 startups in 2018 to 10,969 in 2024, while the APAC region increased from 2,864 in 2018 to 5,886 in 2024.

- This highlights the growth of fintech in Asia, especially in digital payments and alternative lending.

- More than 13,100 fintech startups in the United States alone mark North America as a major player in the industry.

- On an even broader scale, North America has over 12,000 fintech firms active.

- The U.S. figures provide clear evidence of rapid expansion: there were 5,686 startups in 2018, and the figure went up to 5,779 in 2019.

- In 2020, the number surged to 8,775, which then increased to 10,755 in 2021, and then to 11,651 in 2023, before settling at 13,100 in 2024.

- This type of growth shows that the U.S. maintains the targeted position of being the world’s leading source of fintech innovation, backed by strong capital deployment and early uptake of the newest technologies.

Fintech Investment

(Reference: demandsage.com)

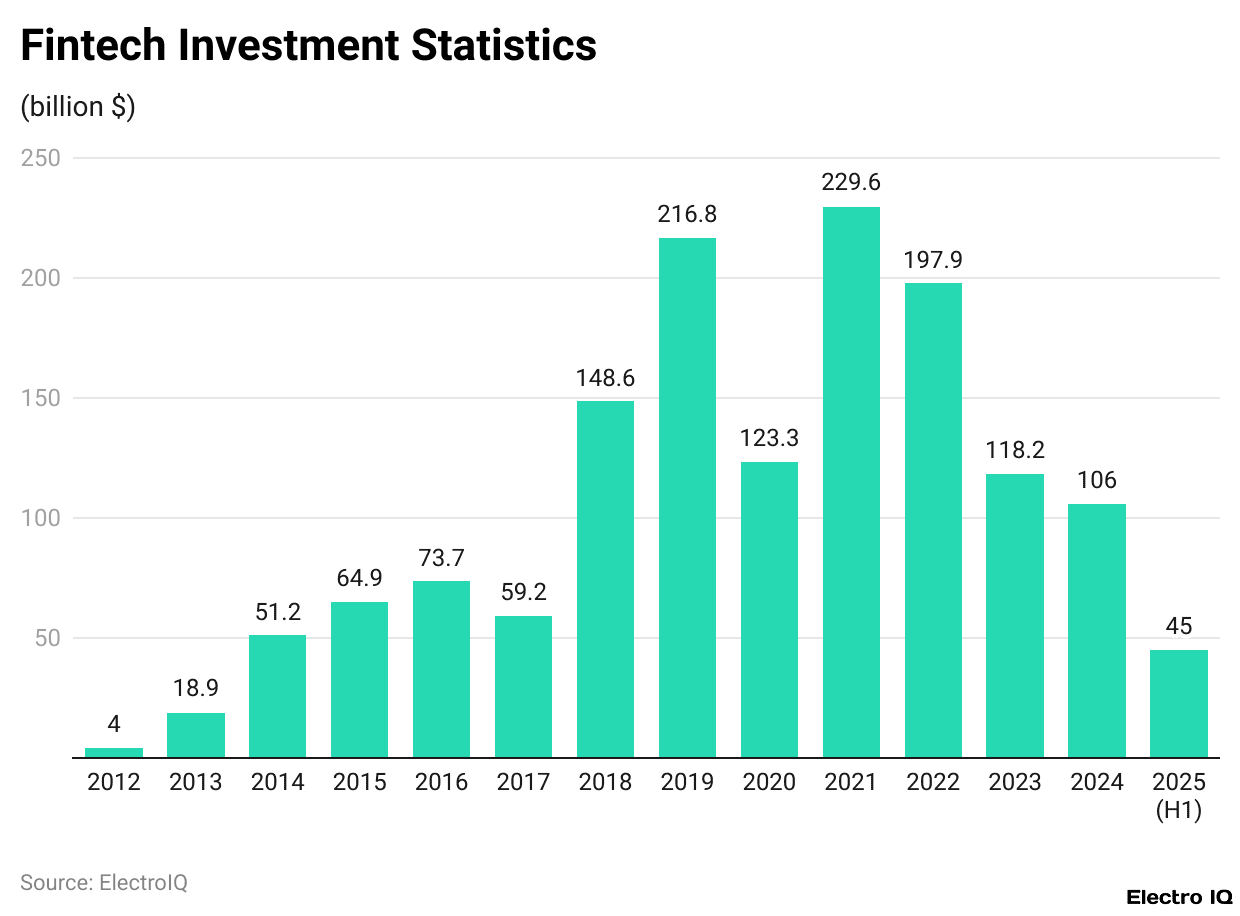

- As per Demandsage, FinTech statistics show that the Fintech investment trends over the last decade indicate episodes of fast growth followed by periods of decline, illustrating the changing dynamics of the industry.

- Fintech firms secured US$106.2 billion in investments in the year 2024.

- In the first half of 2025, the sector had already experienced investments of US$44.7 billion spread across 2,216 deals, being a sign of unwavering belief of investors even with the presence of global economic challenges.

- Needless to say, the obvious highlight was 2021, having the highest fintech investments of US$229.6 billion, thanks to the digital transformation during the pandemic and the spike in fintech services.

- In clear contrast, the lowest amount of fintech investments was recorded in 2012, with just US$4 billion, which further reinforces the amount the sector has grown in just over a decade.

- For example, with regard to funding, it started at US$18.9 billion in 2013, followed by US$64.9 billion in 2015, and further increased to US$73.7 billion in 2016.

- After falling to US$59.2 billion in 2017, it made a strong comeback with US$148.6 billion in 2018 and further increased to an all-time high of US$216.8 billion in 2019.

- Investment dropped to US$123.3 billion in 2020, then soared to the highest on record, at US$229.6 billion, the following year.

- After that, investment steadily declined, marked by US$197.9 billion in 2022, US$118.2 billion in 2023, and US$106.2 billion in 2024.

- Fintech investment in the United States stands out, reaching some US$69.1 billion in 2024, a significant portion of the global total, and making the country the largest market.

- Their dominance underlines the importance of the U.S. as a focal point of innovation and venture capital for the fintech sector.

- It is also where the most notable progressions in fintech technology and business model innovation take place.

Largest Fintech Companies Global

| Top Fintech Companies | Market Cap |

Type Of Company

|

| Visa | $662.6 billion | Paytech |

| Mastercard | $346.293 billion | Paytech |

| Tencent | $174.055 billion | Regtech |

| Ant Financial | $151 billion |

Open Banking

|

| Intuit | $115.509 billion |

Accounting

|

| PayPal | $85.181 billion | Paytech |

| Fiserv | $74.024 billion |

Open Banking

|

| Stripe | $74 billion | Paytech |

| Square | $48.011 billion | Paytech |

| Adyen | $45.161 billion | Paytech |

| Nubank | $41.500 billion |

Challenger Bank

|

| Checkout.com | $40 billion | Paytech |

| Revolut | $33 billion |

Challenger Bank

|

| Chime | $25 billion |

Challenger Bank

|

| Polygon | $20 billion |

Blockchain

|

(Source: demandsage.com)

- At the forefront of the fintech ecosystem, we find companies specialised in payment technologies, or paytech, as well as companies specialised in other fintech areas.

- We begin by analysing the data related to the leading global fintech companies, ordered primarily by their market capitalisation.

- First, Visa holds US$662.6 billion, followed by Mastercard with US$346.3 billion. Both firms lead in the paytech area, showing the dominance of digital payments in the fintech market.

- Additionally, there are other prominent companies in this area, such as PayPal with US$85.2 billion, Stripe with US$74 billion, Square with US$48 billion, and Adyen with US$45.2 billion.

- Furthermore, leadership in fintech spans additional sectors. Tencent (US$174.1 billion) stands for regtech, while Ant Financial (US$151 billion) and Fiserv (US$74 billion) mark strong competition in open banking.

- Intuit (US$115.5 billion) is a pioneer in accounting solutions, proving that the financial software sector is still very relevant.

- Challenger banks such as Nubank (US$41.5 billion), Revolut (US$33 billion), and Chime (US$25 billion) are also notable, underscoring the explosive growth in online-only banking.

- The list also includes companies from blockchain and cryptocurrency, like Polygon with US$20 billion, Ripple with US$15 billion, Coinbase at US$14.5 billion, Blockchain.com with US$14 billion, Opensea at US$13.3 billion, KuCoin with US$10 billion, Bullish with US$9 billion, and Fireblocks with US$8 billion.

- At the same time, companies like Plaid, at US$13.4 billion, improve open banking systems, and Robinhood at US$8.6 billion, excels in wealth tech with its trading-centric approach.

eWallet Statistics

- The eWallet sector is among the biggest and most rapidly advancing segments of fintech.

- Like a virtual wallet, eWallets enable sending and receiving money, bank account access, balance top-ups, and bill payments, all of which can be done effortlessly.

- According to market estimates, the global eWallet market is expected to reach US$3.5 trillion as of 2025, and by 2030, it could climb to a whopping US$489.3 billion.

- The Asia-Pacific region leads in this sector, with notable eWallet providers such as AliPay, PayPal, Apple Pay, and Google Pay.

- Another study forecasts that the number of mobile wallet users will increase from 2.7 billion to 4.8 billion in 2025, equivalent to almost half the global population.

Loan Lending Overview

- With the removal of classical and traditional lending systems, loan lending apps streamline borrowing through soft loans.

- It is further expected that the global loan lending market will grow to US$138 trillion by 2025, with the US alone capturing US$35 trillion, growing at 5% year on year.

- From US$3.5 billion in 2013, peer-to-peer (P2P) lending platforms are expected to reach US$1 trillion by 2025.

- In 2025, the use of loan-lending apps is expected to grow, with an average of 5.9%, while mortgage origination volumes increased from US$1.68 trillion to US$2.155 trillion.

- The US continues to be the largest lending market, proving its significance in global fintech.

Mobile Banking Overview

- Mobile banking apps have become the most widely adopted fintech solution and have reshaped the functioning of online banking to operate on a mobile phone.

- By 2025, the global mobile banking market is expected to reach US$3.6 trillion, with the Asia-Pacific region spearheading adoption, especially in China, India, and Southeast Asia.

- Checking account balances, paying bills, and transferring funds remain the most popular features and continue to grow user engagement.

- As mobile banking apps grow in popularity, the number of users is expected to reach 80 million by 2028.

- The growth in user numbers is a clear indicator of the rising influence of mobile banking in fintech.

Fintech Blockchain Statistics

- Blockchain has emerged as one of the pivotal elements of fintech, as it facilitates not only cryptocurrency transactions but also enhances security, transparency, and operational efficiency for large enterprises such as IBM, Microsoft, Intel, Goldman Sachs, and Walmart.

- In 2024, approximately 30% of the largest early-stage fintech transactions, in which the focus shifted once more to crypto and blockchain, involved companies dealing with digital assets.

- In that same year, the crypto, blockchain, and digital assets segment registered 91 expansion-stage transactions totalling almost US$1 billion.

- Given its relative efficiency and lighter compliance burden, financial institutions have been adopting blockchain more and more for stablecoin payments and cross-border remittances.

- The increase from US$17.9 billion in 2023 to US$19 billion in 2024 reflects a consistent rise in spending on blockchain solutions.

- Moreover, a compound annual growth rate (CAGR) of 48% is recorded for the market from 2018-2024.

- Additionally, investment in digital assets and currencies peaked at US$9.1 billion in 2024, up from US$8.7 billion in 2023.

- In the latter half of 2024, the Americas led the way in deal size, marked by Stripe’s US$1.1 billion acquisition of Bridge and Praxis’s US$525 million fundraising.

- Looking back at 2025, the Bitcoin network surpassed 518,000 transactions in a single day as more than 19 million Bitcoins were already in circulation.

Cybersecurity In Fintech

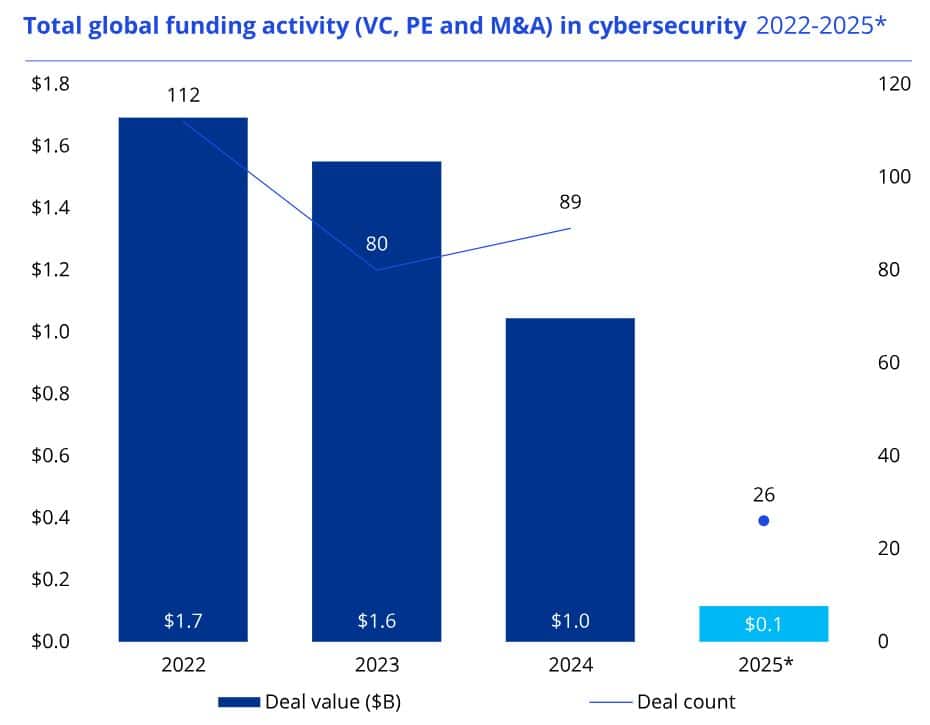

(Source: kpmg.com)

- When compared to the previous year, investment in cybersecurity-focused fintech companies in the first half of 2025 registered a sharp decline.

- Only US$120 million was raised across 26 deals, down from US$1 billion across 89 deals in 2024. Most of the funding activity took place in the seed and early stages rather than in later rounds.

- The US$50 million raised by Blockaid, an Israel-based blockchain security company, was the largest deal.

- Following that, there was US$8 million in seed funding for Cork, a U.S. startup that provides cyber warranties for small and mid-size businesses.

- Additionally, US$20m was invested towards Humanity Protocol, a Hong Kong company that’s working on decentralised identity solutions.

Future of FinTech Statistics

- The impact of artificial intelligence on industries is anticipated to further develop by 2035, as profitability increases by 39% across industries.

- This, coupled with the reshaping of the fintech sector, hints at a staggering US$14 trillion in global economic profits.

- More and more companies are integrating AI and machine learning with their services, especially in terms of improving user experience as well as security.

- As fintech services see greater uptake, there is a shift in the perception of money.

- In the US, 63% of the population states that it has become easier to talk about money with friends due to the availability of fintech services.

- In addition, there is a change in the focus of the industry.

- The B2B2X model, which spans from business-to-business to the end user, as well as the more conventional B2B model targeting small businesses, are becoming more prominent.

- Small and medium-sized enterprises (SMEs) endure the most acute consequences of this global US$5 trillion credit shortfall, and thus, the import of fintech becomes the most clear-cut.

- In terms of geography, the Asia Pacific will lead, accounting for 42% of revenue growth.

- Emerging countries like China, India, and Southeast Asia will be the focal points of financial accessibility through fintech.

- If we look at it now, fintech comprises only 2% of global financial revenue.

- However, concerning global banking values, it is anticipated that by the year 2030, fintech will witness a growth of US$1.5 trillion, translating to about 25% of the global banking value.

Conclusion

Today, the fintech sector has been recognised as an international driver of change; the sector has successfully repositioned finance and transformed digital banking, payments, and lending, as well as introduced AI, blockchain, and InsurTech. Even though investment activity has declined since its 2021 peak, higher adoption translates into billions of people using mobile payments, neobanks, and digital credit.

Developed nations such as the United States and those in Europe and the Asia-Pacific are at the forefront of innovation, while emerging economies continue to extend accessibility. Sustainable, long-term growth is suggested by the fast expansion of AI, BNPL, RegTech, and embedded finance. The impact of fintech is crystallised in the projection for 2030, when it is slated to make up 25% of global banking valuation, a metric that illustrates this sector’s impact on financial services.

FAQ.

In the first half of 2025, the funding raised by fintech companies amounted to US$44.7 billion, marking the slowest six-month stretch since early 2020. Investors turned cautious due to steep interest rates, geopolitical strife, and regulatory grey areas. Even so, fintech still commands the attention of venture capital, as evidenced by 2,216 transactions in the first half of 2025.

Fintech in 2025 will be dominated by payment companies, Visa and Mastercard, with a market valuation of US$662.6 billion and US$346.3 billion, respectively. They will be followed by PayPal, Stripe, Square, and Adyen. In open and digital banking, Ant Financial, Nubank, and Plaid will be the key players. Significant participants from blockchain and wealth technology will be Coinbase, Polygon, and Robinhood.

Neobanks, AI-based financial technologies, digital payments, RegTech, embedded financing, open banking, InsurTech, BNPL, and blockchain are some rapidly expanding areas. To illustrate, digital payments are projected to hit US$14.78 trillion by 2028, and InsurTech might increase from US$22.1 billion in 2023 to US$306.5 billion by 2030.

Fintech services are used by approximately 64% of consumers worldwide, including 46% in the U.S. The most utilised services are digital payments, money transfers, and insurance products. There is also a growing usage of fintech by SMEs, with 25% of them adopting such solutions globally. The adoption is heterogeneous in different areas, with Asia excelling in payments and alternative lending, Europe in crowdfunding, and the U.S. in digital investment.

According to current predictions, by 2035, the economic value generated by the use of AI will reach US$14 trillion. Moreover, by 2030, Fintech is expected to contribute US$1.5 trillion to the global banking and finance. Asia-Pacific will lead 42% of revenue growth. New business models, AI adoption, embedded finance, and the use of existing funds will continue to change the financing and management of money worldwide for businesses and individuals.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.