Gaming Industry Statistics By Revenue And Facts (2026)

Updated · May 11, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Gaming Industry Revenue By Segments

- Gaming Industry Revenue By Country

- Annual Investment Volume In Video Gaming Companies

- Global Game Developer Sentiment Toward Blockchain, NFTs, And Web3

- Major Video Game Releases By Platform

- Video Game Industry Players

- Major Gaming Acquisitions

- IPO Momentum In The Video Gaming Industry Worldwide

- Global Gaming Penetration Q2 2025, By Age And Gender

- The Rise Of AI And Generative Tools In Game Development

- Esports And Live Streaming Viewership Metrics

- Mobile Gaming – The Uncontested Revenue Engine

- Conclusion

Introduction

Gaming Industry Statistics: The year 2025 created an important turning point, which established the global gaming industry as one of the largest and most enduring entertainment sectors that exists worldwide. The 2025 data shows an industry that operates at peak capacity while maintaining its ability to introduce fresh developments through its various business operations, demographic shifts, and rising customer interest, record-breaking income growth, and changing methods of making money. The gaming industry continued to thrive against all economic challenges and market competition because it maintained its importance to both cultural and economic sectors more than traditional media industries, such as film and music.

This article will highlight the gaming Industry statistics, which include revenue data and player demographic information, platform usage patterns, and new technology developments, and research insights showing the current state of the gaming industry and its future development path.

Editor’s Choice

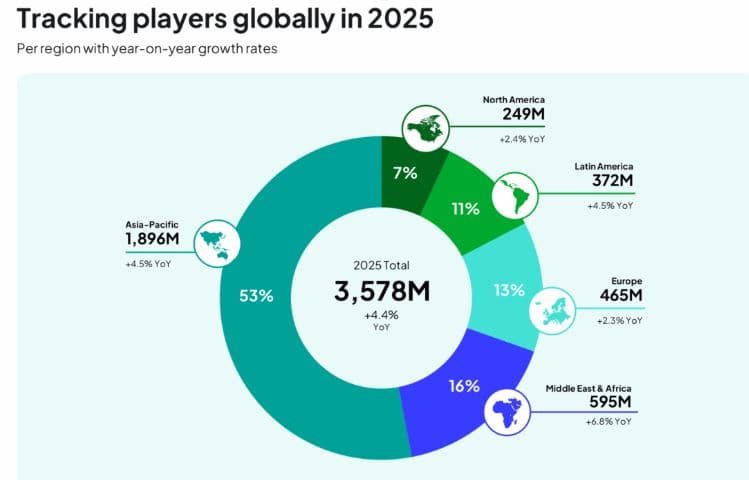

- The Gaming Industry reached 3.58 billion players worldwide in 2025, which represents a 4.4% yearly growth rate and a user base that exceeds 60% of all internet users.

- Mobile platforms lead user activity because 83% of gamers prefer to play on their smartphones.

- Global gaming revenue reached USD 282.3 billion in 2024, and it is expected to reach USD 363.2 billion by 2027.

- China earned USD 45.8 billion through 744.1 million players, while the United States generated USD 45.0 billion from 209.8 million users, which indicates that American users spend more money per person.

- The Asia-Pacific region has 1.9 billion players, which represents 53% of the total worldwide gaming population.

- The total of 190 gaming investments that occurred during 2025 YTD represents an 8.2% decline from the previous quarter, while the total amount reached USD 4.44 billion.

- 77% of developers show no interest in blockchain technology, while only 2% of developers use it for their projects.

- The PC platform leads with 156 upcoming game releases, followed by PS5, which has 115 upcoming games, and Xbox Series X/S, which has 113 upcoming games.

- The gaming community encompasses more than 82% of all internet users, according to data from Q2 2025.

- Among ages 16–24, 93% of males and 91.5% of females play video games.

- Twitch recorded 4.64B gaming hours watched in Q2 2025, holding 54% market share.

- Mobile gaming generated USD 92B in 2024, surpassing USD 100B in 2025, representing ~55% of total revenue.

- Generative AI could reduce development cycle times by 20–40% and cut routine asset creation time by 30–50%, improving production efficiency across the Gaming Industry.

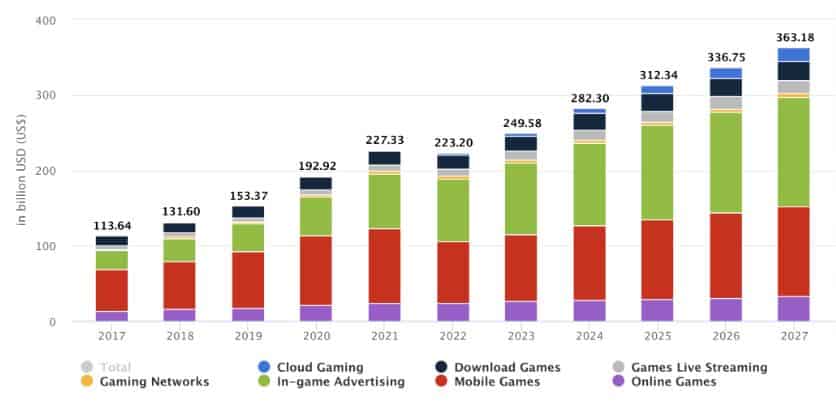

Gaming Industry Revenue By Segments

(Source: ustimes.biz)

- According to Statista, the gaming industry stands as the most powerful sector that drives worldwide entertainment industry revenue growth.

- By 2025, the global gamer population is expected to surpass 3.58 billion users, with 83% playing on mobile devices, underscoring mobile’s structural dominance in user acquisition and engagement.

- Revenue metrics further validate this leadership position. Global gaming revenues exceeded USD 282.3 billion in 2024, outpacing the combined revenues of the film and music industries.

- The financial momentum displays continuous growth because the projected 8.76% compound annual growth rate (CAGR) between 2024 and 2027 indicates extended development, which will not end until 2027.

- The market volume will reach USD 363.2 billion by 2027 because digital distribution and live-service monetization models, and the worldwide player base continue to expand.

- The console and PC market segments maintain their importance while mobile gaming serves as the main driver for market growth.

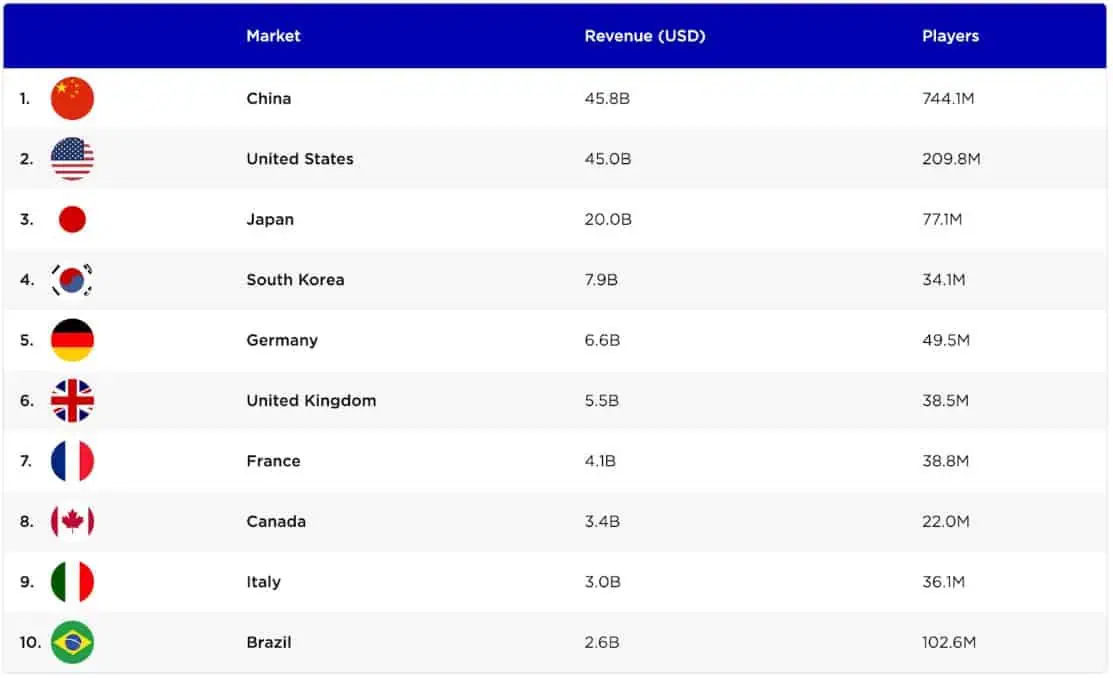

Gaming Industry Revenue By Country

(Source: helplama.com)

- According to Newzoo.com, the global gaming industry demonstrates a fascinating balance between revenue concentration and player distribution.

- China leads the market with revenue of USD 45.8B and an exceptional 744.1M players, which demonstrates its unparalleled size and mobile-first market supremacy.

- The United States follows closely at USD 45.0B, but with a significantly smaller player base of 209.8M, which results in much higher average revenue per user ARPU.

- Japan ranks third with USD 20.0B from 77.1M players, which demonstrates its ability to generate revenue through console and mobile gaming.

- The mid-tier revenue cluster between USD 5B and USD 8B consists of South Korea, Germany, and the United Kingdom, which operate as established markets.

- Brazil shows 102.6M players who produce USD 2.6B in revenue, which indicates strong user activity, but users spend less money on average.

- The Gaming Industry demonstrates distinct revenue generation patterns, which result from developed markets achieving higher ARPU while populous countries create large-scale operations.

- The regional economic conditions, together with platform user preferences and digital system development, create the current changes that are happening in the global gaming industry.

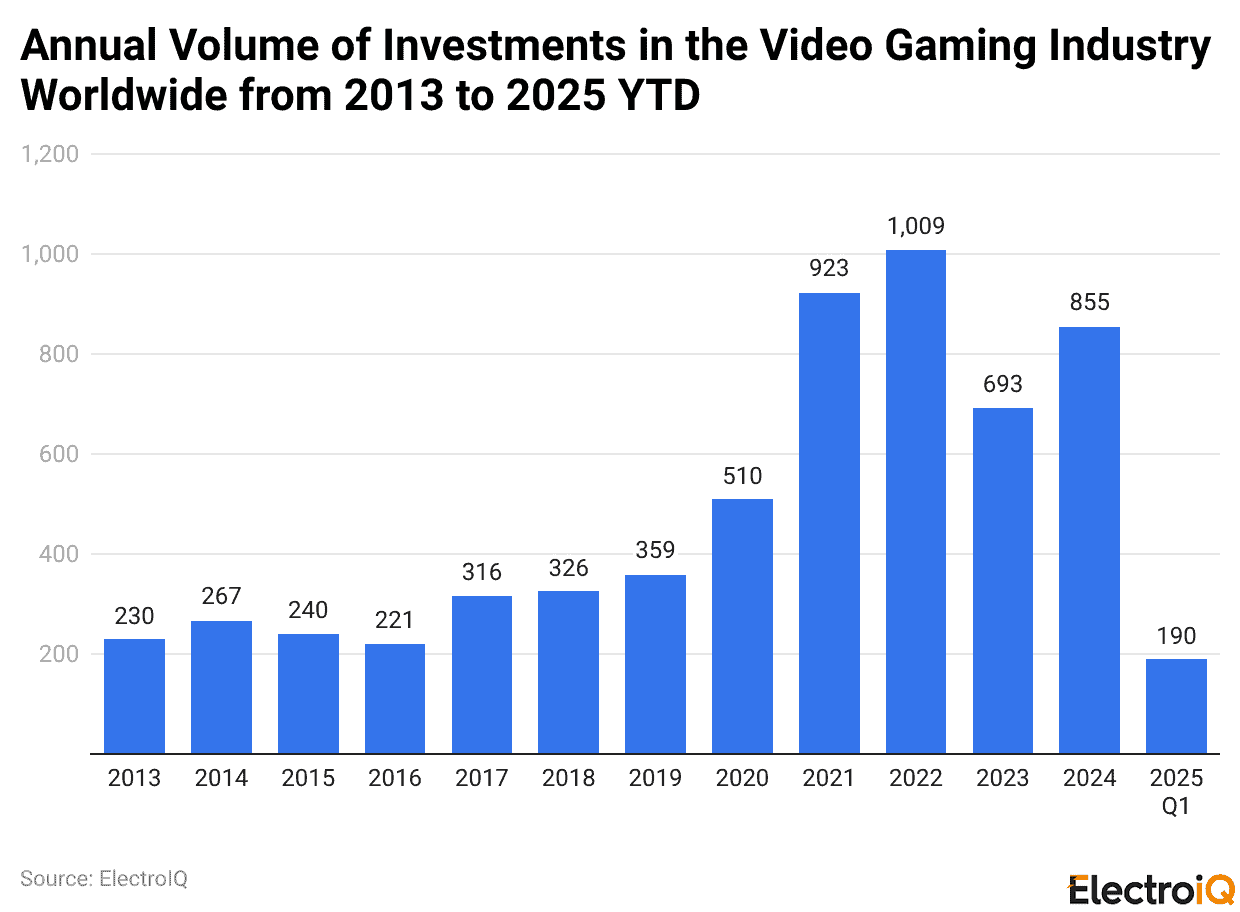

Annual Investment Volume In Video Gaming Companies

(Reference: statista.com)

- 2025 YTD data shows a controlled decrease in deal activity, which affects the entire Gaming Industry.

- The total number of disclosed investments reached 190, which represents a 8.2% decrease from the 207 transactions that occurred during the previous quarter.

- The total investment for 2025 Q1 reached USD 4.44 billion despite the market experiencing a decrease in deal activity.

- Investors now choose their investments more carefully because they want to invest in studios that can grow their operations through live-service models and IP-based development.

- The gaming industry currently moves from its period of rapid growth toward a phase where it controls its spending to achieve permanent business success through sustainable financial returns.

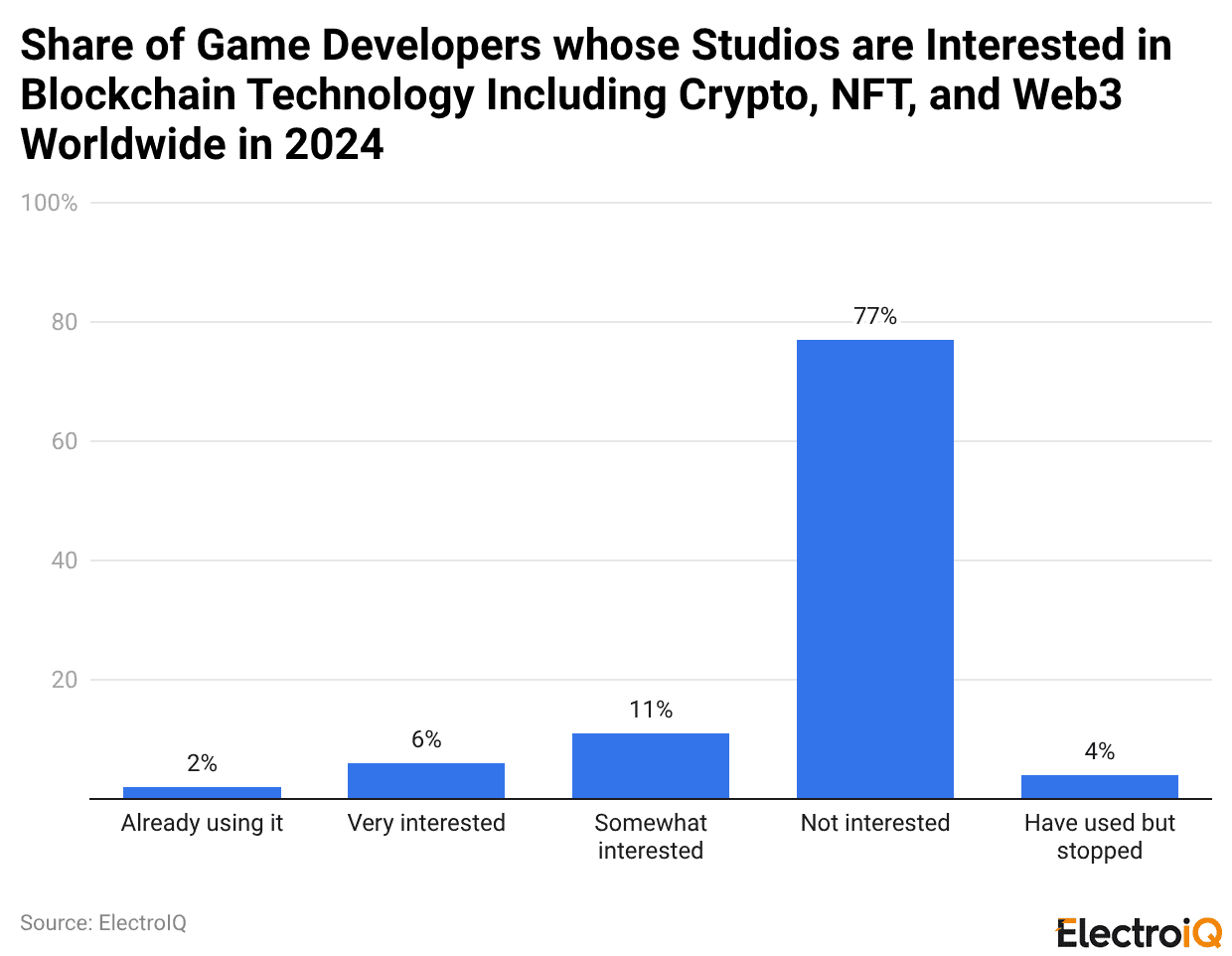

Global Game Developer Sentiment Toward Blockchain, NFTs, And Web3

(Reference: statista.com)

- The gaming industry in 2024 showed calculated doubt about blockchain integration through its existing systems.

- A striking 77% of developers show no interest in crypto, NFTs, or Web3, which shows their resistance to new technologies despite initial excitement.

- The industry shows limited commitment to blockchain technology because only 2% of companies use it, while 6% of companies plan to implement blockchain, and 11% of companies show interest in testing it.

- The gaming industry lost 4% of its players who tried blockchain technology but found it unhelpful. The combination of increasing development expenses, unclear regulatory frameworks, and fluctuating cryptocurrency markets causes a decrease in risk-taking behavior.

- The gaming industry focuses on established growth drivers, which include live services, cloud gaming, and cross-platform ecosystems instead of pursuing unproven decentralized development methods.

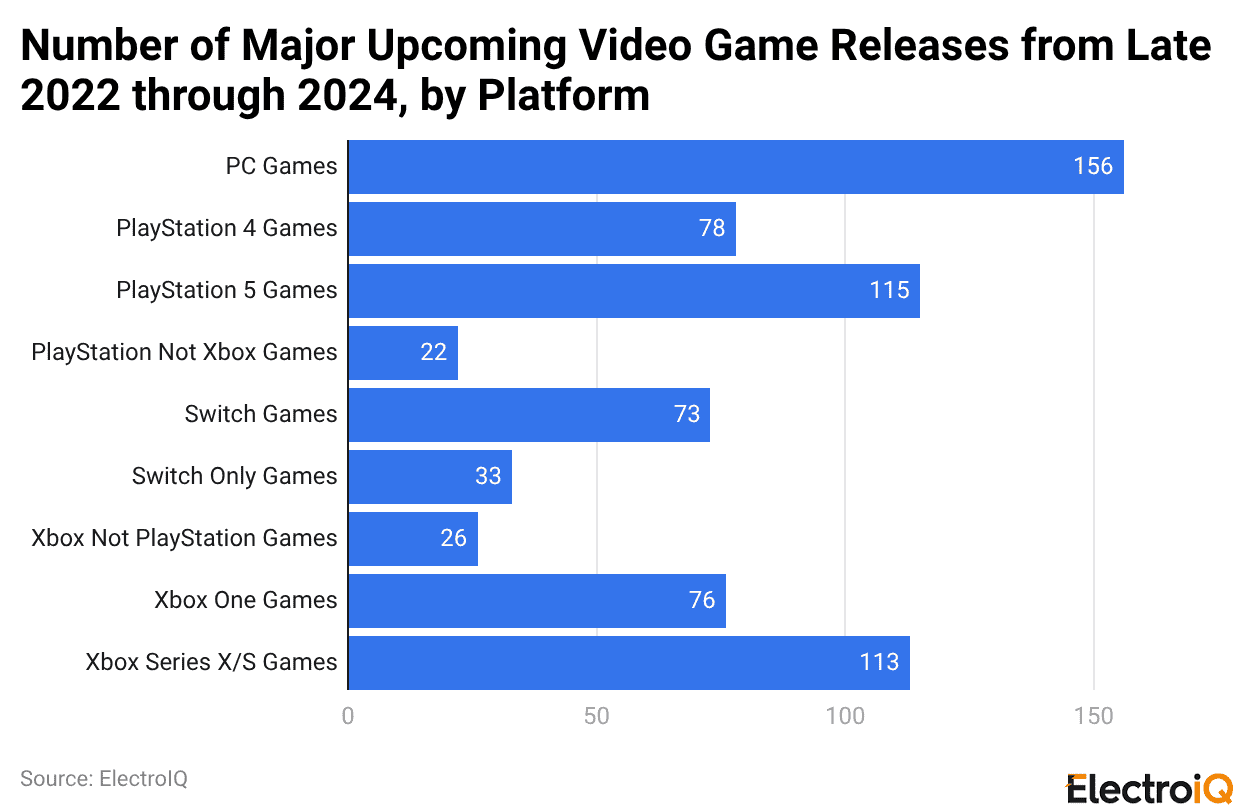

Major Video Game Releases By Platform

(Reference: statista.com)

- The gaming industry is clearly shifting toward platform diversification rather than rigid exclusivity.

- Between late 2022 and 2024, PC leads with 156 planned releases, showing its dominance as the most accessible and scalable ecosystem.

- The console market competes intensely because 115 games are developed for PlayStation 5, while 113 games are developed for Xbox Series X/S, which shows that both systems receive almost equal support from third-party developers.

- The industry maintains exclusive strategies through 22 PlayStation-only games and 26 Xbox-only games, which constitute only a small fraction of total game releases.

- The gaming industry now focuses on distributing games through multiple platforms because this approach helps studios reach more players while generating multiple revenue sources and maintaining player interest over time.

Video Game Industry Players

(Source: newzoo.com)

- The gaming industry is entering a maturity phase, which no longer depends on acquiring new users for its growth.

- PC gaming has 936 million players who make up 26% of the total market, while console gaming has 645 million users who represent 18% of the market, which indicates that traditional gaming segments have reached their stable point.

- The Asia-Pacific region has 1.9 billion players who represent 53% of the global gaming population, while the Middle East and Africa region experiences its fastest growth at 6.8% annual rate because of mobile-first technology adoption.

- As the gaming industry penetration reaches its highest point, the industry must shift its focus to retention metrics, cross-device ecosystems, and long-tail monetization strategies.

- Future growth will depend less on scale and more on deep engagement, particularly as Generation Alpha embraces multi-platform gaming experiences.

Major Gaming Acquisitions

| Acquiree – Acquirer (date) | Segment | Upfront EV in mUSD |

Total EV (incl. earn-out) in mUSD

|

| Keyword Studios acquired by EQT (Oct 2024) | Outsourcing | 2,800 | 2,800 |

| Easybrain acquired by Miniclip (Nov 2024) | Mobile | 1,200 | 1,200 |

| Jagex acquired by CVC Capital (Feb 2024) | PC & Console | 1,100 | 1,100 |

| SuperPlay acquired by Playtika (Nov 2024) | Mobile | 700 | 2,000 |

| Plarium acquired by MTG (Nov 2024) | Mobile | 620 | 820 |

| Gearbox acquired by Take-Two Interactive (Jun 2024) | PC & Console | 460 | 460 |

| Landvault acquired by Infinite Reality (Jul 2024) | Tech | 450 | 450 |

| Saber acquired by Beacon Interactive (Mar 2024) | PC & Console | 247 | 341 |

| Data.ai acquired by Sensor Tower (Mar 2024) | Tech | n/d | n/d |

| Chartboost acquired by LoopMe (Dec 2024) | Tech | n/d | n/d |

(Source: statista.com)

- The gaming industry will undergo a major transformation because 2024 introduces a new period for its merger and acquisition activities.

- The industry now prefers to execute organized development work through its consolidation activities instead of pursuing major corporate buyouts.

- The EQT acquisition of Keywords Studios for USD 2.8 billion in October 2024 serves as evidence of investor trust in expanding business operations, which provide development support, localization, quality assurance, and live operations.

- The company now chooses to invest in operational backbone assets instead of acquiring complete content ownership.

- The total value of deals during 2024 remains far below the previous record established in 2022 when Take-Two purchased Zynga, and Microsoft made its historic USD 69 billion acquisition of Activision Blizzard, which remains the biggest deal in the history of gaming.

- The previous period experienced rapid growth because of low interest rates and intense competition among platforms.

- The industry now focuses on achieving operational efficiency through automated processes while maintaining profit margins because this approach represents its current development phase.

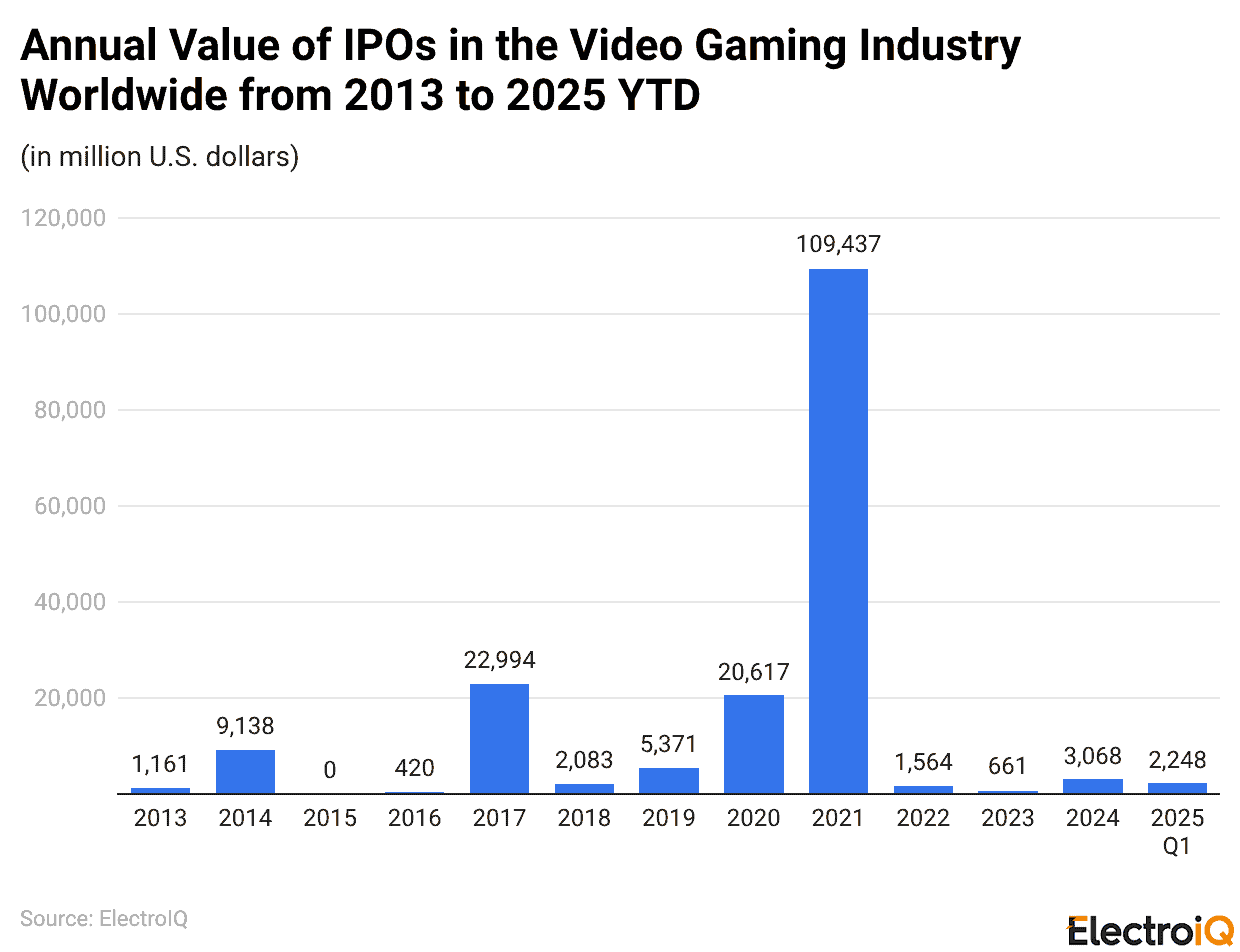

IPO Momentum In The Video Gaming Industry Worldwide

(Reference: statista.com)

- The period from 2013 to 2019 saw IPO proceeds that moved between USD 1 billion and USD 9 billion as investors showed caution about the gaming industry, which functioned as a small public market segment.

- The year 2017 marked a significant change because the total IPO value reached almost USD 23 billion, which resulted from the growth of mobile gaming and the initial excitement about esports. The year 2020 saw IPO proceeds reach USD 20.6 billion, while 2021 brought an all-time high of USD 109.4 billion, which resulted from the combination of lockdown demand, extremely low interest rates, and the rising popularity of digital entertainment.

- The monetary policy changes led to a new cycle because IPO value dropped to USD 1.56 billion in 2022 and USD 661 million in 2023.

- The year 2024 saw activity reach USD 3.1 billion, while the first quarter of 2025 produced USD 2.25 billion, which indicates that the gaming industry is slowly starting to open its capital markets, but it will not go back to its past periods of high-risk investment.

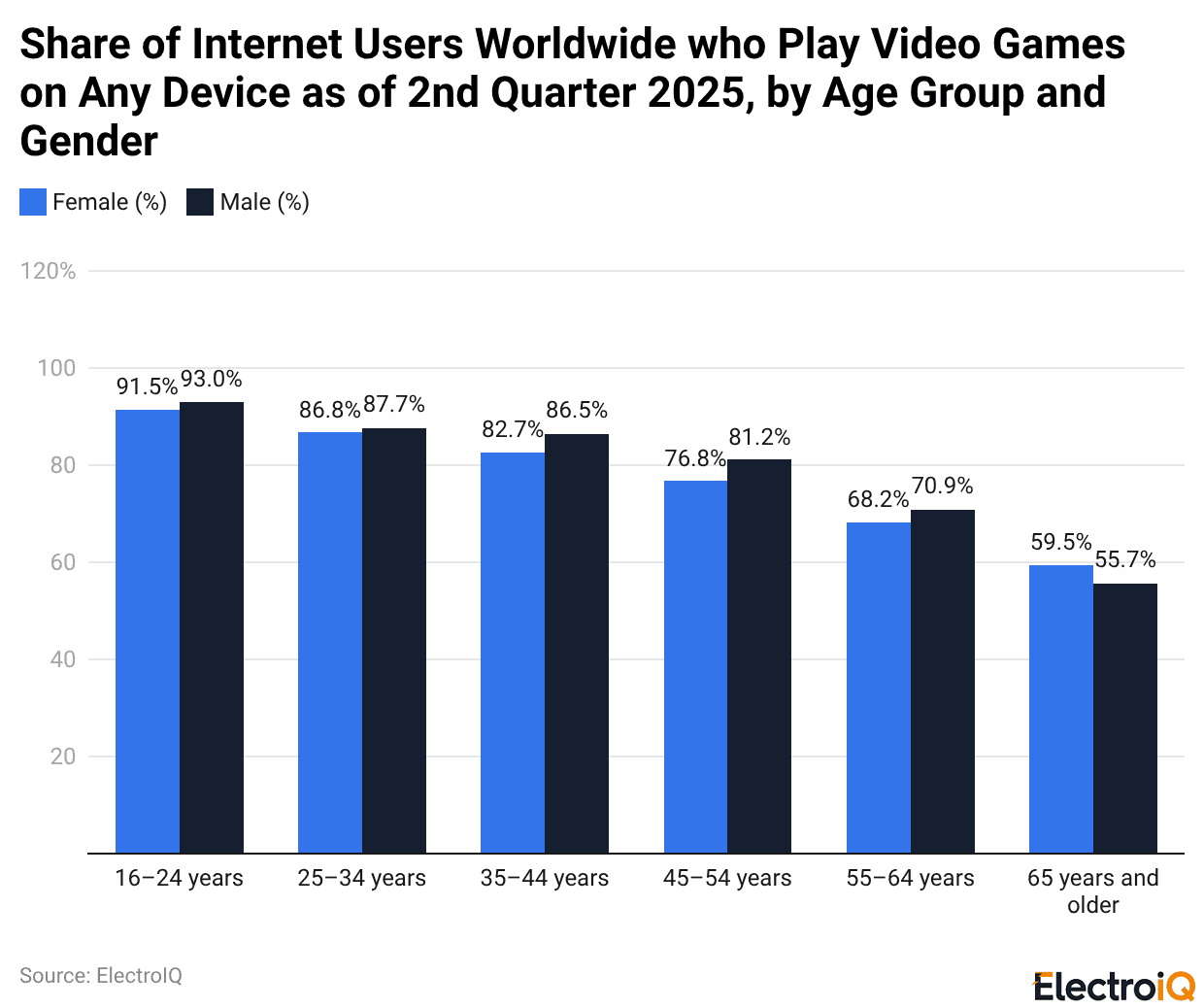

Global Gaming Penetration Q2 2025, By Age And Gender

(Reference: statista.com)

- Q2 2025 penetration data demonstrates that the Gaming Industry achieves exceptional market reach among younger age groups.

- Over 82% of internet users worldwide now identify as gamers, which shows that gaming has become a popular activity.

- Gen Z shows high engagement levels because 93% of male users and 91.5% of female users aged 16-24 play video games on any device.

- The gender gap of 1.5 %age points demonstrates that people now participate in activities with more equal access.

- The gaming industry benefits from youth adoption, establishes permanent revenue streams, shows strong demand across platforms, and demonstrates deep cultural ties to digital entertainment.

The Rise Of AI And Generative Tools In Game Development

| Cost and workflow dimension | Traditional development costs (indicative AAA pattern) | AI‑assisted development costs (indicative impact) | Representative insights |

| Asset creation (concept art, 2D/3D props, background variants) | The organization executes its operations through its three main art departments while engaging external developers who handle 15 to 30% of its total budget for projects that require substantial content development. | The BCG report shows that studios that implement generative AI technologies can achieve time savings between 30 to 50% when they develop routine assets, while their costs decrease because they can produce more affordable iterations of their work. | BCG, Unity ecosystem commentary. |

| Coding and tools engineering | The team needs to spend multiple hours on basic coding tasks while they develop scripts and maintain their internal tools, which creates problems because they cannot use previous work, and their testing process takes too much time, particularly when working on large live-service projects. | Deloitte reports that organizations that implement gen-AI coding tools achieve tangible productivity improvements because these tools enable them to automate major sections of their standard coding components and testing frameworks, which leads to decreased coding duration and allows their engineering teams to operate with reduced staff or flexible roles. | Deloitte AI and software quality. |

| Quality assurance and playtesting | The big projects need manual QA teams together with external vendors who use 20 to 30% of their engineering and QA budgets, which results in testing cycles that last several weeks or several months, together with inefficient balancing processes. | The Google Cloud games survey reports that 47% of developers currently implement AI for their playtesting and balancing processes, while Deloitte software data shows that AI-driven test generation reduces QA cycle time by double digits and maintains testing coverage when used with reliable validation methods. | Google Cloud–Harris Poll, Deloitte. |

| Localization and narrative variants | The organization incurs expensive translation costs together with narrative editing expenses, because it needs to translate its content into multiple languages. | According to Google Cloud, 45% of developers use AI for localization and translation, which provides significant cost savings and faster project completion times for each language project while enabling multiple product releases and extended A/B testing of both narrative elements and marketing materials. | Google Cloud–Harris Poll. |

| Overall production schedule and budget | The development of AAA titles requires studios to spend 3 to 6 years together with an 80 to 200 million dollar budget, which creates substantial risks. | Bain and McKinsey estimate that generative AI will eventually take over more than 50% of development work while reducing development cycles by 20% to 40%, which will result in savings of millions of dollars for each project and create additional funds for marketing innovation and live-operations assistance. | Bain & Company, McKinsey. |

Esports And Live Streaming Viewership Metrics

| Platform | Total hours watched (gaming/esports, 2025 snapshot) | Year‑over‑year growth (hours watched) |

| Twitch | The total number of gaming hours watched in Q2 2025 reached 4.64 billion, which represented 54 % of the worldwide gaming livestreaming market for that quarter. | The decline of hours watched reached −4.6% because the platform reached its peak usage and faced stronger competition from its competitors. |

| YouTube Gaming | The Q2 2025 gaming livestreaming market showed approximately 2.2 billion hours of gaming content, which made up 24% of the total market during that time. | YouTube Gaming achieved its fastest growth rate because its hours watched increased by 25% between 2024 and 2025. |

| Kick (and other emerging platforms) | Kick streaming platform had more than 1 billion hours of content viewed during Q2 to Q3 2025, while Facebook Gaming and other regional platforms contributed approximately 1.26 billion additional viewing hours. | Kick achieved triple-digit annual growth because its yearly growth rate reached approximately 112% while new platform entrants expanded niche markets, which resulted in overall positive growth. |

Mobile Gaming – The Uncontested Revenue Engine

| Revenue dimension | 2024–2025 snapshot (approximate) | Key takeaways |

| Mobile vs. total games revenue | Mobile games generated about USD 92 billion in 2024, which represented 49% of the USD 187 billion global games market, and mobile gaming surpassed USD 100 billion in 2025 while accounting for 55% of total games revenue. | Mobile is the single largest and fastest‑growing segment, out‑earning console and PC combined in many years. |

| IAP vs. ad revenue in mobile | Mobile games generated IAP revenue of USD 81 to 82 billion during 2024, showing a 4% Yearly growth, while in-app advertising revenue increased approximately 4% Yearly and experienced rapid growth in hybrid-casual and casual games. | IAP still dominates, but ad monetization is growing faster, and hybrid models are increasingly standard. |

| APAC share of mobile revenue | The Asia-Pacific region generated approximately 49 to 50 % of worldwide mobile gaming revenue during 2025, which included USD 72.9 billion of 2024 APAC mobile revenue and USD 27.5 billion (45% share) YTD by September 2025. | APAC is the epicenter of mobile gaming spend, with China, Japan, South Korea, and India driving both volume and revenue growth. |

| Global mobile gamer demographics | More than 50% of smartphone users engage in mobile gaming activity, while female players make up 45 to 50% of the gaming population, and users aged 18 to 34 show the highest gaming activity, although players aged 35 and older also participate heavily. | Mobile has the broadest, most demographically balanced audience in gaming, making it a prime channel for mass‑market and brand advertisers. |

Conclusion

The gaming industry achieved its greatest record-breaking performance in 2025, which demonstrated its capacity to endure and change while maintaining its significance throughout modern culture. The industry achieved success through its three operational sectors, which included mobile, console, and PC platforms, while introducing fresh methods to earn revenue and new ways to use platforms, demonstrating its dedication to developing new solutions. The gaming industry will develop new abilities for social connections through artificial intelligence content creation and advanced technologies, which include cloud gaming, augmented reality, and virtual reality systems.

The multitude of problems related to supply and monetization methods and investment conditions has not stopped the gaming industry from establishing itself as a major worldwide force, which will determine how digital content and interactive experiences, storytelling, and entertainment will progress into the future.

Sources

FAQ.

The Gaming Industry had 3.58 billion players throughout the world in 2025, and 82 % of internet users played games, while 83 % of users played games on mobile devices.

The Gaming Industry is expected to reach more than USD 300 billion in revenue for 2025, according to projections, which show that mobile will generate more than USD 100 billion.

The global gaming revenue reached USD 282.3 billion in 2024, which surpassed the combined earnings of the film and music industries.

The industry experiences an 8.76 % annual growth rate from 2024 to 2027, which shows that it develops steadily instead of facing brief periods of growth.

Joseph D'Souza founded ElectroIQ in 2010 as a personal project to share his insights and experiences with tech gadgets. Over time, it has grown into a well-regarded tech blog, known for its in-depth technology trends, smartphone reviews and app-related statistics.