Credit Score Statistics By Country and Age Group (2025)

Updated · Sep 18, 2025

Table of Contents

Introduction

Credit Score Statistics: Credit scores come into play when one is going for a credit card, mortgage, or loan. Lenders weigh the score to see if begging the person for money would be just another investment or would be a doubt in the firm’s credibility. They determine whether you can get a loan, interest rate, even if some jobs will accept an application to rent, and credit cards you would qualify for. Since credit scores have a heavy say in a lot of approvals, it does make sense to track yours and/or compare it with that of others to see where you stand.

This article will present the Credit Score Statistics, with average scores that are historically very high, and more people fall in the top tiers. The real problems are levels of debt and an unequal credit system.

Editor’s Choice

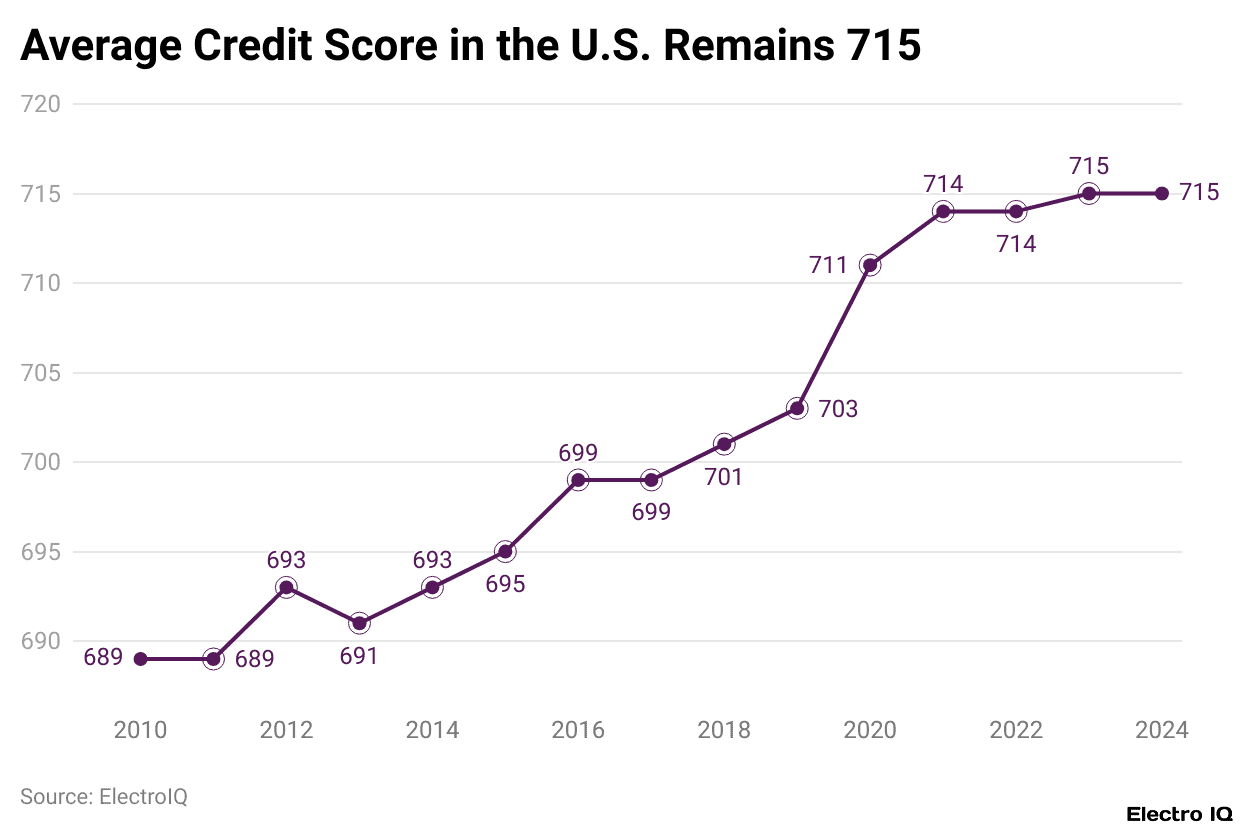

- The Average US FICO® Score remained steady at 715 in 2024.

- (300–549), Fair (550–649), Good (650–749), Very Good (750–799), Excellent (800–900).

- Silent Generation ~760, Boomers 745, Gen X 709, Millennials 690, Gen Z 680.

- None-most states saw any changes, some small ones: -1 in Arizona, Arkansas, Delaware, Florida.

- Credit utilisation ratio: steady at 29% for 2023 and 2024.

- Credit cards-2.40%, Mortgages-2.24% (1.88% in 2023), Auto loans–3.68%, Personal loans–3.86%.

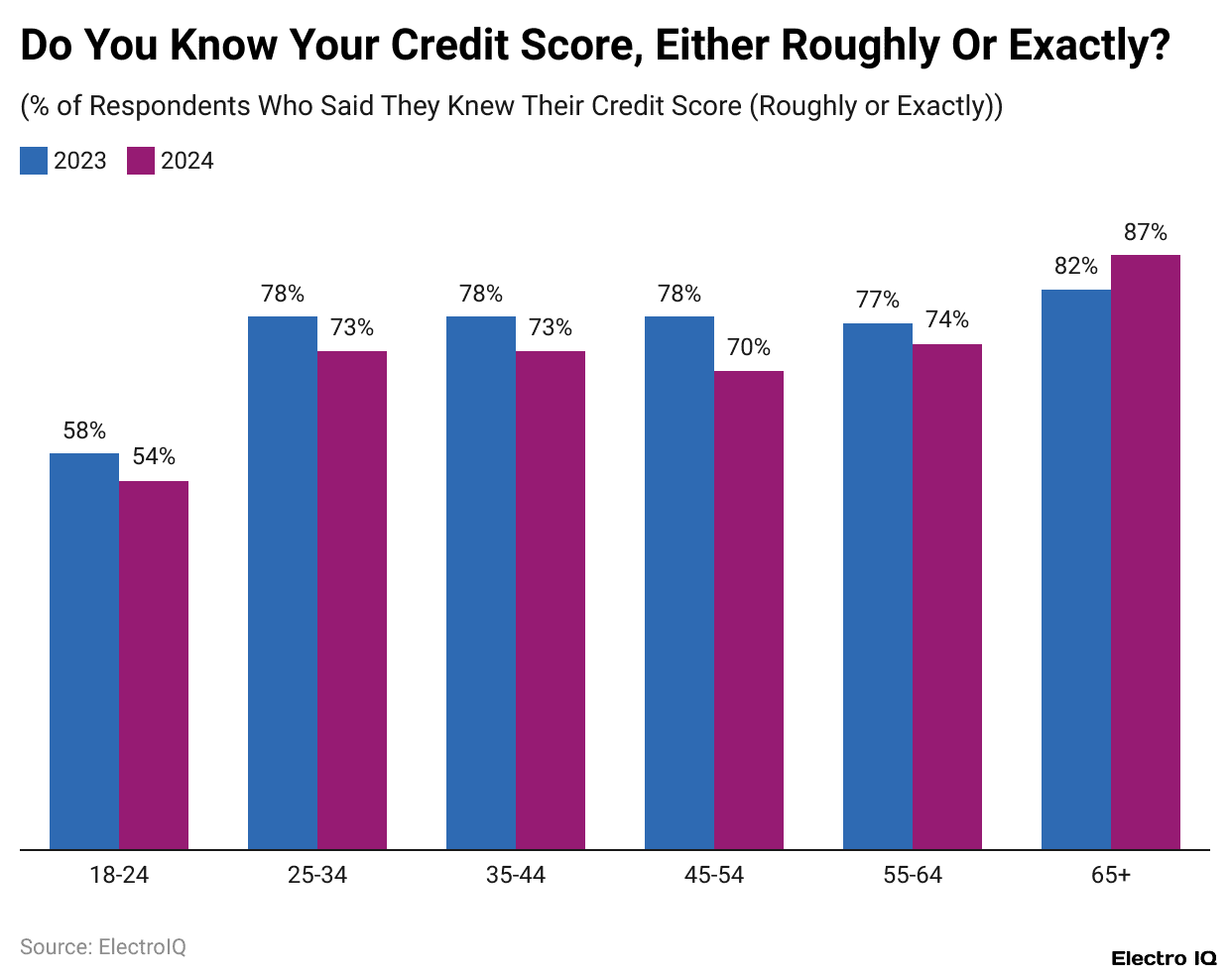

- 72% of consumers knew their score by 2024, down from 78% in 2023, with awareness the lowest among Gen Z and young adults.

Credit Score Ranges

(Source: godigit.com)

- Credit scores are those three-digit numbers that indicate how trustworthy you are in borrowing and repaying money.

- If a score falls between 300 and 549, it depicts a financially haunted history, which may include missed payments, defaults, or too much credit usage.

- Lenders will consider you the highest risk and therefore largely deny loan approvals or credit.

- A score of 550-649 is deemed Fair, meaning you could have had late payments or too many credit checks.

- In the eyes of lenders, you might still be risky, and while some may grant you the loan, others will have you pay higher interest or require bigger down payments.

- Between working with 650 and 749 is known as good credit. It means you have shown decent repayment behaviour and are thought of as less risky by lenders; almost all lenders will approve your loans, but you won’t always be offered the best loan deals.

- On the very good level at 750 to 799, you have proven yourself over a long time to make payments on time and borrow responsibly.

- Lending institutions will treat you as a low-risk client and may even offer you discounted loan deals. 800 to 900 is the highest range, an excellent score with superb fiscal discipline.

- Banks and other financial creditors would trust you to the utmost and would give you the best interest and terms.

Average Credit Score In The U.S

(Reference: experian.com)

- According to Experian, credit score statistics show that the average FICO® Score was 715 in the U.S. for the 12 months ending September 2024.

- While credit scores had remained steady, the surrounding economy had changed.

- In 2024, late in the year, the Federal Reserve sliced one percentage point off the interest rate in three stepwise cuts; this made borrowing a bit easier.

- Meanwhile, unemployment had remained low, while inflation slowed to reverse in a couple of cases; this meant living costs were steady, and many workers had enough pocket money to see their monthly spending alongside their present monthly debt costs.

Credit Score By Age Group

| Age Group |

Average Credit Score

|

| Generation Z (18-25) | 680 |

| Millennials (26-41) | 690 |

| Generation X (42-57) | 709 |

| Baby Boomers (58-76) | 745 |

| Silent Generation (77+) | 760 |

(Source: badcredit.org)

- Scores have generally been on the rise for the adult population, but older folks still attain higher scores than younger ones.

- Those 77 and older, categorised under the Silent Generation, hold the highest average score of about 760.

- Next are the Baby Boomers, aged 58 to 76 years, who average 745, followed by Generation X, aged 42 to 57 years, who average 709. Millennials, from 26 to 41 years old, average 690, and Generation Z is at the bottom, with an average score of 680.

- Generally speaking, younger consumers have lower scores since their credit histories have been comparatively much shorter than those of an older population that has had years of building a long record of borrowing and repaying.

- Creditors generally consider the age of a credit report to be an important aspect of credit scoring; thus, younger consumers will be put at a disadvantage if their creditworthiness is perfect.

Average Credit Scores By State

| State | 2023 | 2024 |

Change (Points)

|

| Alabama | 692 | 692 | 0 |

| Alaska | 722 | 722 | 0 |

| Arizona | 713 | 712 | -1 |

| Arkansas | 696 | 695 | -1 |

| California | 722 | 722 | 0 |

| Colorado | 731 | 731 | 0 |

| Connecticut | 726 | 726 | 0 |

| Delaware | 715 | 714 | -1 |

| District of Columbia | 715 | 715 | 0 |

| Florida | 708 | 707 | -1 |

| Georgia | 695 | 695 | 0 |

| Hawaii | 732 | 732 | 0 |

(Source: experian.com)

- Throughout the past year, average FICO® scores across most states remained basically constant from year to year, with vanishingly small fluctuations at most.

- States like Alabama, Alaska, California, Colorado, Connecticut, Georgia, Hawaii, and Washington, D.C., remained absolutely stalwart in that the average scores were exactly as they were in 2023.

- Other states, including Arizona, Arkansas, Delaware, and Florida, had negligible one-point drops in their average scores.

- This, overall, showed that the credit health of the states remained steady throughout the year with no greater improvement or decline.

Key Components of Credit Score

- Payment History (35%): This has the greatest bearing on your score. Timely bill payments develop good credit, whereas one late payment can cause major harm.

- Amounts Owed (30%): This factor shows the amount of credit used compared to the limits. Credit scores get hit if more than 30% of available credit is used, especially on credit cards.

- Length of Credit History (15%): The longer the credit accounts have been active, the better. Lenders will consider the age of your oldest account, the newest account, and the average age of your accounts in evaluating your credit history.

- Credit Mix (10%): Having different types of credit, such as credit cards, car loans, or mortgages, may work in favour of your score if you manage these accounts properly.

- New Credit (10%): New credit inquiries will have a temporary downward effect on your credit score.

The Average Credit Usage

- One such major factor affecting a person’s credit rating is how much credit an individual uses, particularly on credit cards.

- Low balances compared to credit limits will increase the scores.

- Both in 2023 and 2024, the average credit card utilisation ratio stood at 29%. This rate remained steady in 2024 because even though credit card balances went up a little, so did credit limits; hence, the ratio remained the same.

- Once credit utilisation goes above 30%, it goes onto the downgrade list and may actually impact future offers for credit cards, mortgages, car loans, and so on.

- Generally speaking, the less credit you use relative to what’s available, the better for your score.

Delinquency Rates By Account Type 2024

- As per the data, delinquency rates—accounts or payments considered late for 30 or more days—changed mildly between 2023 and 2024.

- Credit card delinquencies saw a minuscule drop from 2.45% down to 2.40%, whereas personal and auto loans practically did not change, standing at 3.86% and 3.68%, respectively.

- On the contrary, mortgage delinquencies saw a significant rise, climbing from 1.88% in 2023 to 2.24% in 2024.

- That has been attributed to the expiration of relief programs initiated during the pandemic that temporarily kept delinquency rates down.

- While delinquencies on mortgages are up, they remain somewhat lower than the pre-pandemic rate of 2.48% in 2019.

- In general, the data suggests that most debt types seem to have stabilised, with only mortgages showing a definite increasing trend in delinquency.

Credit Score By Age

(Reference: experian.com)

- As per Experian, Credit Score Statistics state that in December 2024, Experian polled over 1,000 consumers and found fewer of them knew their credit scores than the year before.

- About 72% of the respondents said they had at least a rough idea of their score, down from 78% in 2023. This decline took place among nearly all age groups except for those older than 65.

- Most adults between 25 and 64 still keep tabs on their scores, whereas younger consumers tend to be less aware, most likely because they have not entered into credit products such as credit cards or auto loans.

- Despite this drop-off, experts agree that there has been a generation of increased money consciousness and discipline onshore over the last 10 years, partially owing to credit education and financial awareness.

Track Your Credit Scores

There are a few tips to maintain and/or improve your health:

Pay Your Bills On Time

- The most important factor in determining FICO® Score is your payment history.

- When a payment is missed, late for at least 30 days, the reporting of such late payments usually starts, and the score can be tremendously hurt.

- Setting up reminders or autopay can help ensure that all bills are paid on time.

Keep Balances Low

- Credit utilisation is a large factor in credit scoring.

- Experts advise utilisation below 30%.

- The highest scores, at 740 and above, generally keep balances at some small number of units.

Limit New Credit Applications

- Applying for too many new accounts in a short period tends to lower your credit score.

- While its percentage contribution to other variables is relatively smaller, the long-term high stability of using credit cautiously is a benefit.

Conclusion

Credit Score Statistics: Credit scores still remain the most important variable in determining financial health and the existence of credit, loan terms, even housing, or job opportunities. The average FICO® Score held constant at 715 in 2024, while the older parents and some states maintained an average higher than 715. Mortgage delinquencies did climb slightly, while those of credit utilisation and delinquencies generally stayed flat with the expiry of pandemic relief programs.

Credit-score awareness took a slight dip at the same time, especially amongst younger adults, emphasising the need for adequate financial education. Correcting these scores will deliver long-term stability and benefits to consumers who pay on time, keep balances low, and limit unnecessary applications for credit.

FAQ.

A good credit score falls between 650 and 749. This range depicts patterns of repayment behaviour that make the lenders, in turn, view you as a relatively low risk. Scores above 750 indicate very good ones, and scores above 800 are excellent, leading you to qualify for the best interest rates and terms on loans.

Payment history comes first with 35%, then percentages owed, 30%. Length of credit history, credit mix, and new credit queries then come into play but paying on time and maintaining low balances will practically guarantee maintaining or increasing your score.

Generally, the older generations have more awareness and higher scores. For instance, the Silent Generation scores very high, in the range of about 760, whereas Baby Boomers score just a tiny bit lower at 745. Younger adults, especially those who make up Generation Z, come up at 680 and sometimes lower, since knowledge is minimal, and their credit histories are even shorter, with very little experience in actual borrowing.

No, the national average remained at 715 as in 2023. There were, however, some small state-level fluctuations: Arizona, Arkansas, Delaware, and Florida experienced drops of one point each. Consequently, credit health remained stable, supported by low unemployment rates and slowing inflation.

Three methods to improve a credit score are viability: making on-time payments, maintaining a credit utilisation rate below 30% (preferably below 10), and rarely applying for new credit. As much as these three can sometimes protect your credit score, they will also help you qualify for better loans and offers over time.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.