Drone Insurance Statistics By Segments, Market Capitalization And Revenue

Updated · Oct 16, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Revenue of Annuity Insurance

- Number of Employees in The Casualty Insurance Industry

- Gross Premiums of The Insurance Industry Worldwide

- Expense Insurance Ratio in Europe

- Global Insurance By Segments

- The Total Direct premiums written in the Life Insurance Industry Worldwide.

- Largest Insurance Companies in France

- Leading Insurance Companies in The United States and Worldwide

- Largest Insurance Companies Worldwide By Market Capitalization

- Largest Insurance Companies Worldwide By Revenue

- Top Insurance as the London Stock Exchange (UK) By Market Capitalization

- Health Spending Per Enrollee in The United States

- Pilots Owning Drone Insurance

- Global General Liability Insurance Market Forecast

- Drone Insurance overview

- Conclusion

Introduction

Drone Insurance Statistics: Drone insurance refers to financial coverage that is based on accidents involving drones. Primarily, it relates to mandated financial information about aviation devices. With the rise of drone sales, there is an increase in the chances of property damage involving drones. Likewise, local authorities have issued guidelines regarding these commercial aviation devices.

By going through the Drone Insurance Statistics, one can attain essential information. One can gain critical information about this financial model that protects drone-based financial coverage.

Editor’s Choice

- Revenue of annuity insurance increased from $776.7 billion in 2009 to $1041.1 billion by 2023.

- The number of employees in the casualty insurance industry grew from 652.1k in 2005 to 680.5k by 2023.

- Gross premiums of the global insurance industry rose from $2.51 trillion in 2000 to $6.06 trillion by 2022.

- In Europe, Cyprus has the highest expense ratio for non-life insurance, at 0.49.

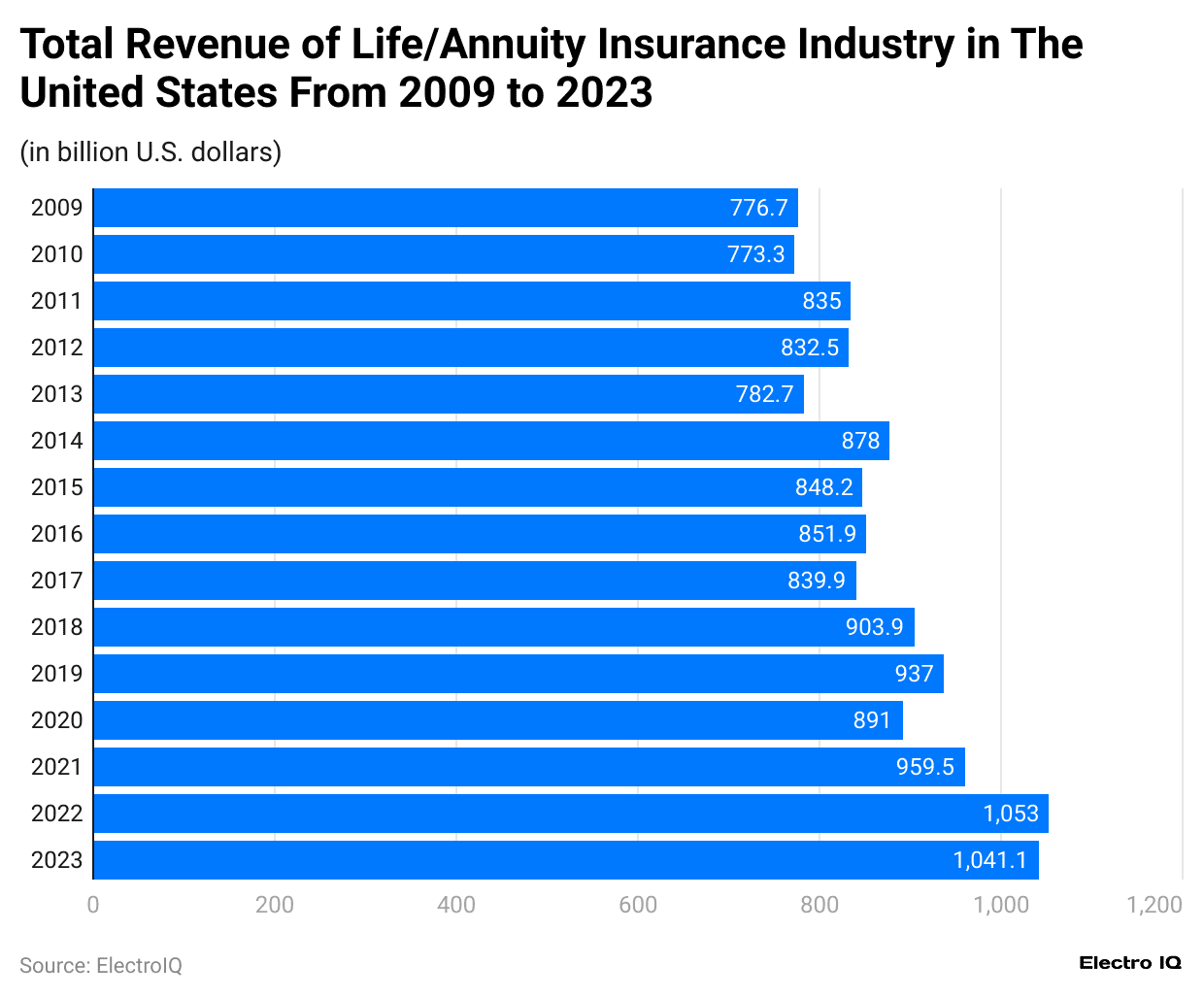

Revenue of Annuity Insurance

(Reference: statista.com)

- Drone Insurance Statistics showcases the increase in the revenue of annuity insurance over the years.

- While in 2009, the revenue was $776.7 billion, it had increased to $1041.1 billion by the end of 2023.

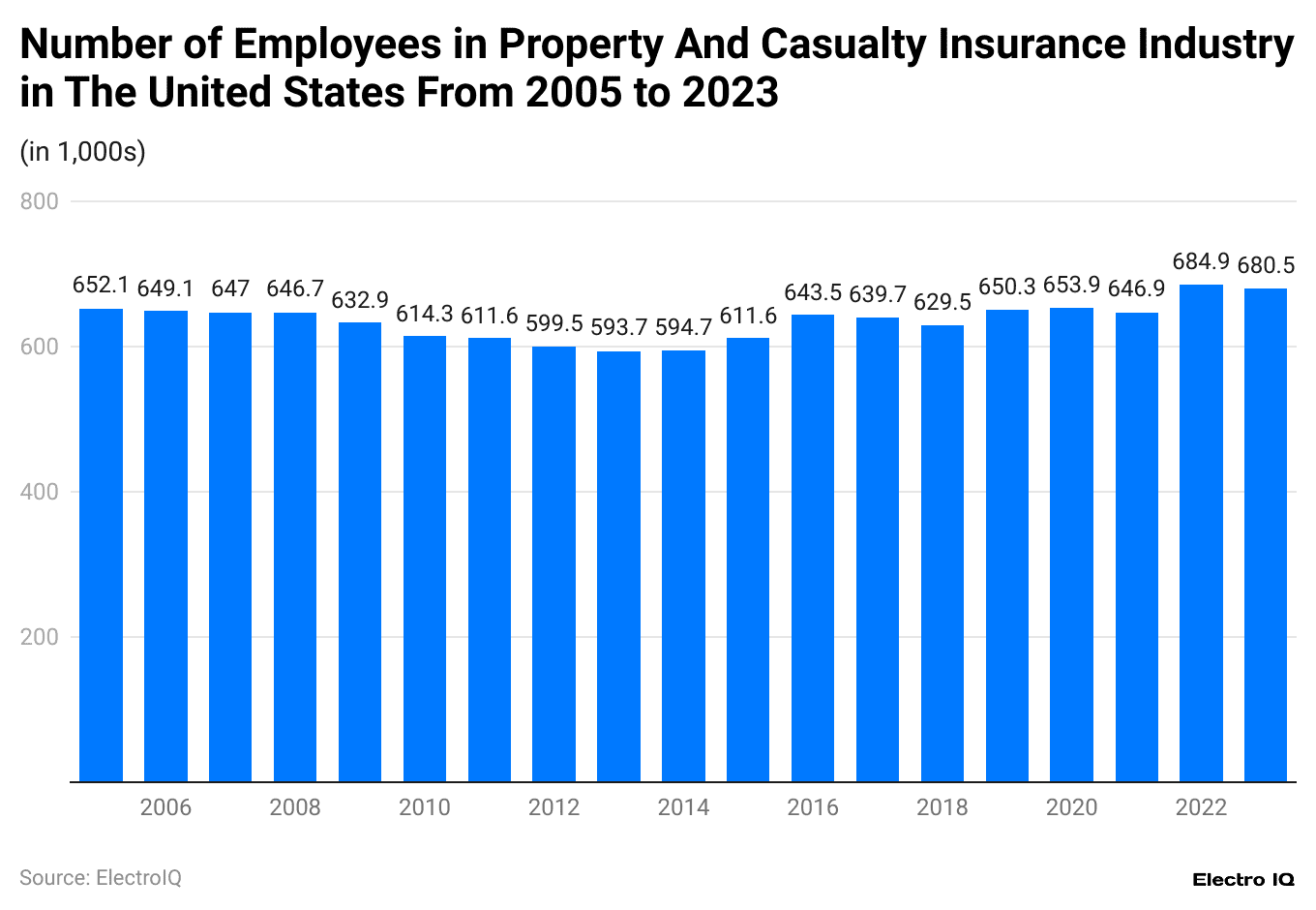

Number of Employees in The Casualty Insurance Industry

(Reference: statista.com)

- Drone Insurance Statistics showcases consistency regarding the number of employees in the insurance industry.

- In 2005, the number of employees was 652.1k, while by the end of 2023, there were 680.5k employees.

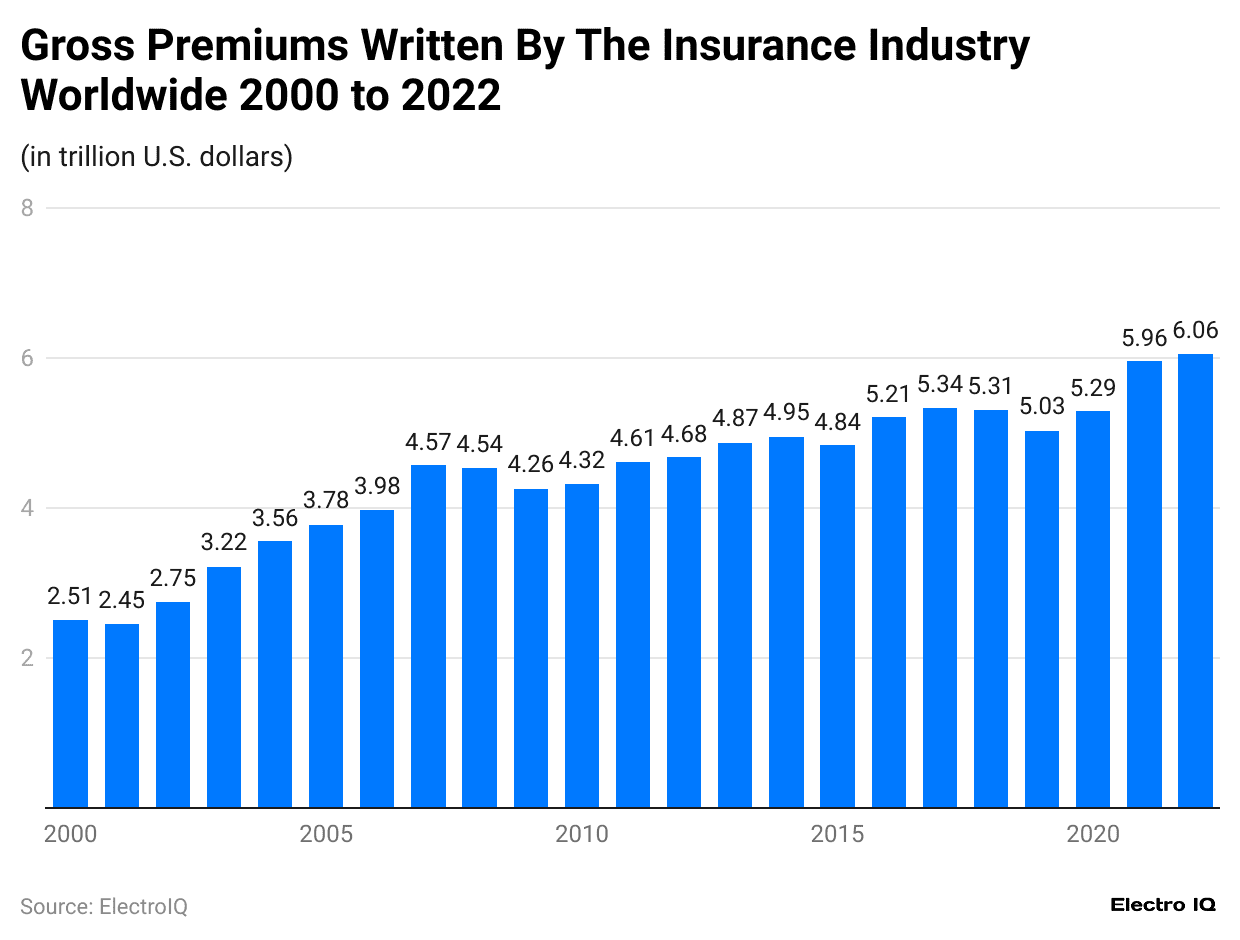

Gross Premiums of The Insurance Industry Worldwide

(Reference: statista.com)

- The Drone Insurance Statistics showcase that gross premiums written by the financial industry have increased over time.

- While in 2000, the premium was $2.51 trillion, it had increased to $6.06 trillion by the end of 2022.

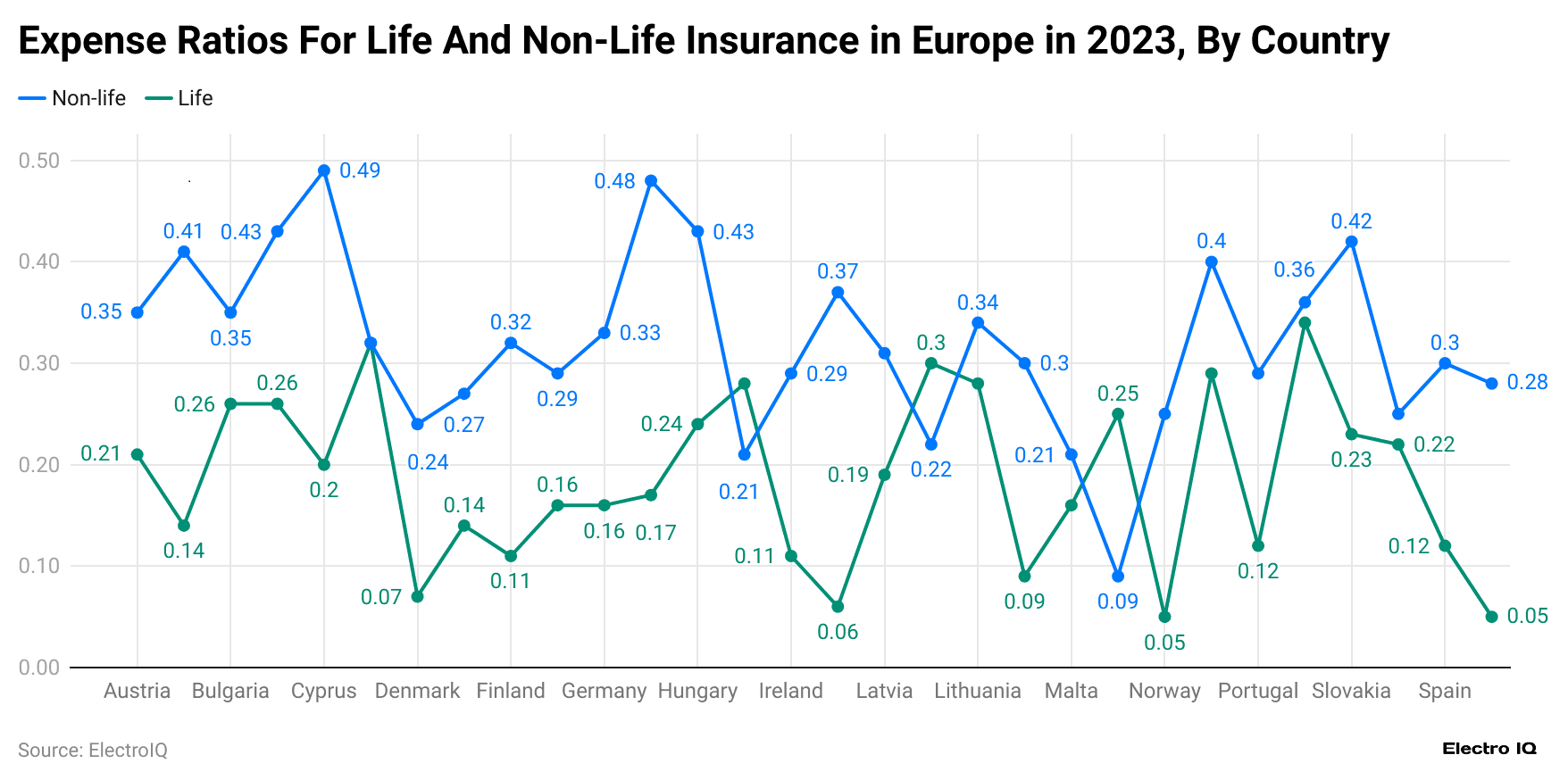

Expense Insurance Ratio in Europe

(Reference: statista.com)

- Drone Insurance Statistics showcase that Cyprus has the highest expense ratio for non-life insurance at 49, indicating higher operational costs in the country.

- Accordingly, Greece and Croatia display similar expense ratios for both insurance categories, with non-life insurance at around 0.43 and life insurance at around 26.

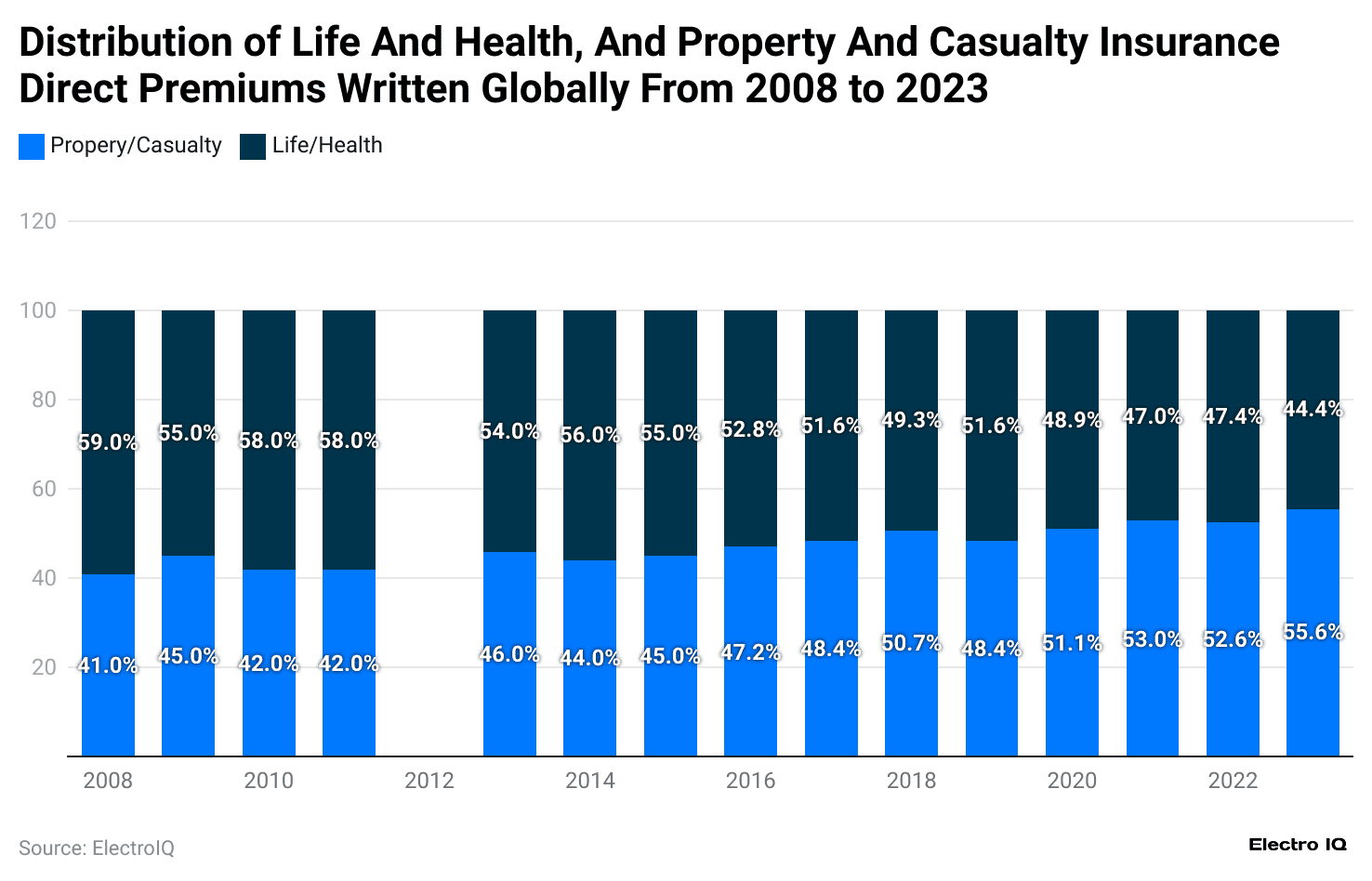

Global Insurance By Segments

(Reference: statista.com)

- Drone insurance statistics reveal that property/casualty and life/health insurance are two segments of global insurance.

- In 2023, Property has a 55.6% share of all insurance; in comparison, 44.4% has life/health insurance.

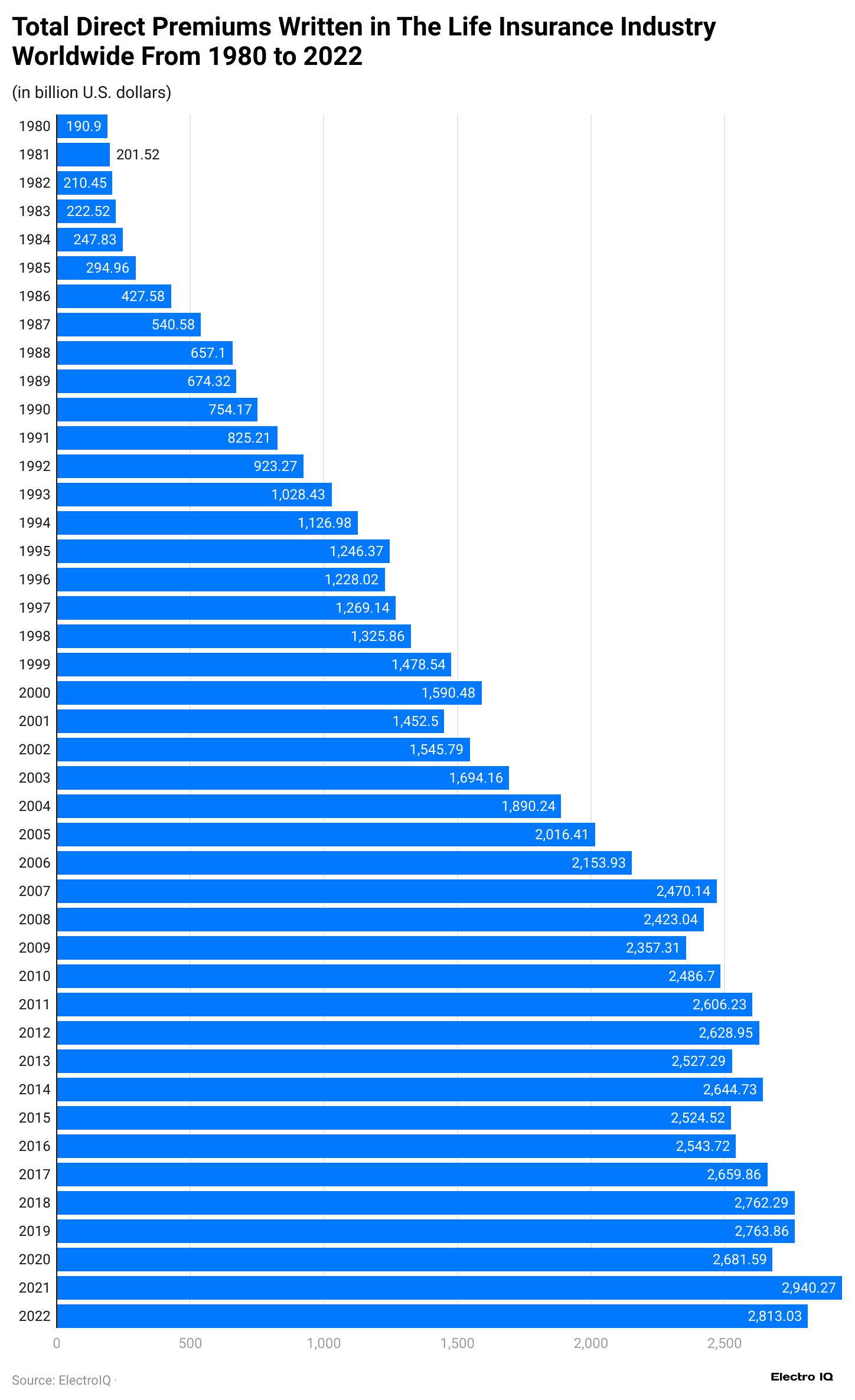

(Reference: statista.com)

- Drone Insurance Statistics showcase that direct insurance premiums have decreased significantly in the past four decades.

- 1980, the direct premium was $190.9 billion, but it had significantly increased to $2,813.03 billion by the end of 2022.

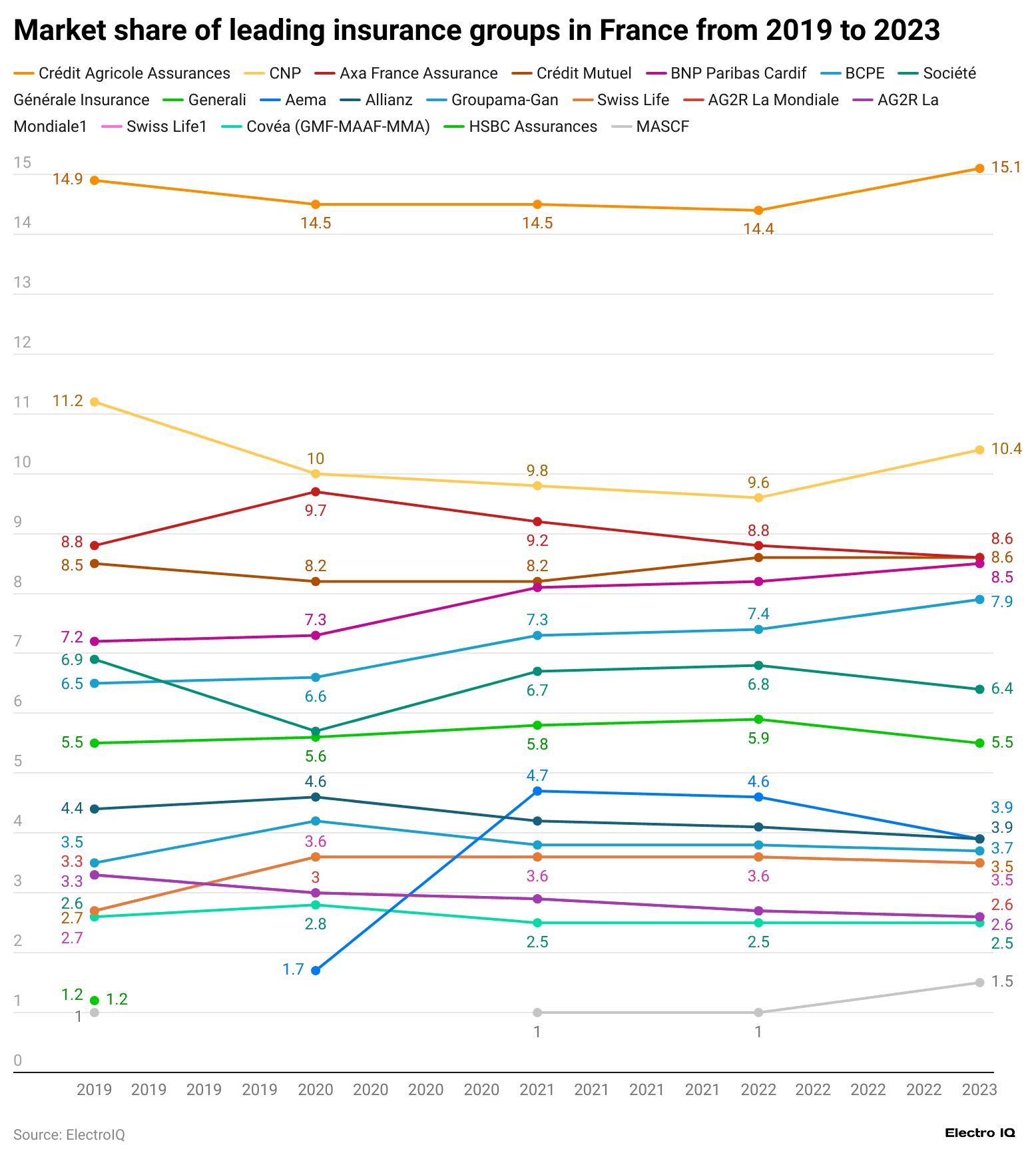

Largest Insurance Companies in France

(Reference: statista.com)

- CNP, La Mondiale AG2R, Humanis Malakoff, Axa France Assurance, Covéa (GMF-MAAF-MMA), BCPE, MASCF, Crédit Agricole Assurances, Generali, Allianz, BNP Paribas Cardif, Crédit Mutuel, Groupama-Gan, Société Générale Insurance, Aema, Swiss Life, HSBC Assurances rank among the largest insurance companies in France.

- Drone Insurance Statistics show that Crédit Agricole Assurances has consistently led the market, maintaining its top position. Its market share slightly increased from 14.9% in 2019 to 15.1% in 2023, indicating steady growth.

- Aema, which entered the market in 2020, showed rapid growth, reaching 3.9% by 2023. This indicates its ability to capture market share quickly, likely through aggressive marketing strategies, mergers, or acquisitions. Its growth trajectory is notable compared to that of more established players.

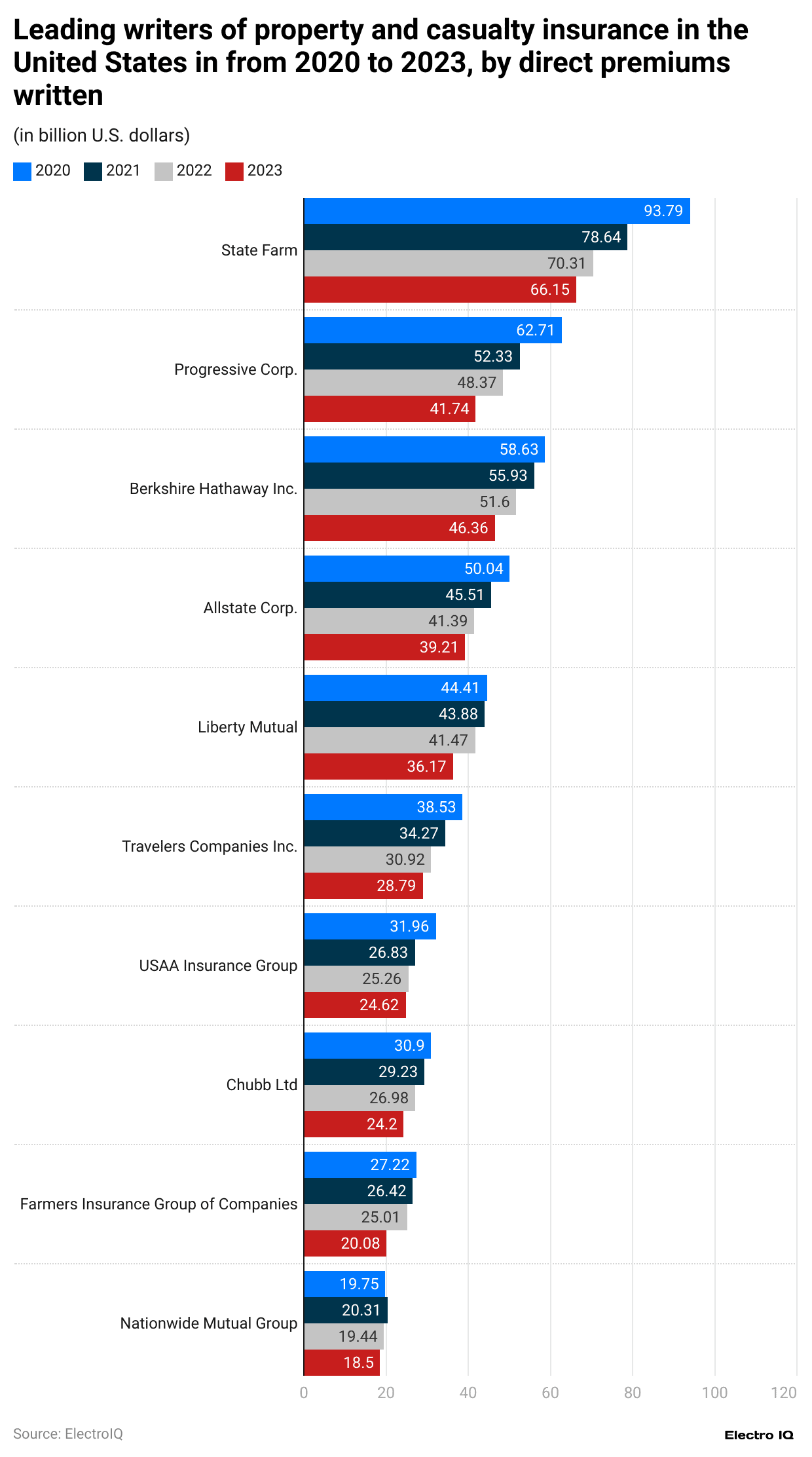

Leading Insurance Companies in The United States and Worldwide

(Reference: statista.com)

- Drone Insurance Statistics showcase that Hathaway Inc., Berkshire, Progressive Corp., Group Insurance USAA, Corp., Allstate, Group Nationwide Mutual, Mutual Liberty, Chubb Ltd., Farm State, Travelers Companies Inc., Group of Companies Farmers Insurance are the top insurance writers of property and casualty insurance.

- State Farm has consistently been the leading property writer with market share from 2020 to 2023: 2020 with $66.15 billion, 2021 with $70.31 billion, 2022 with $78.64 billion, and 2023 with $93.79 billion written.

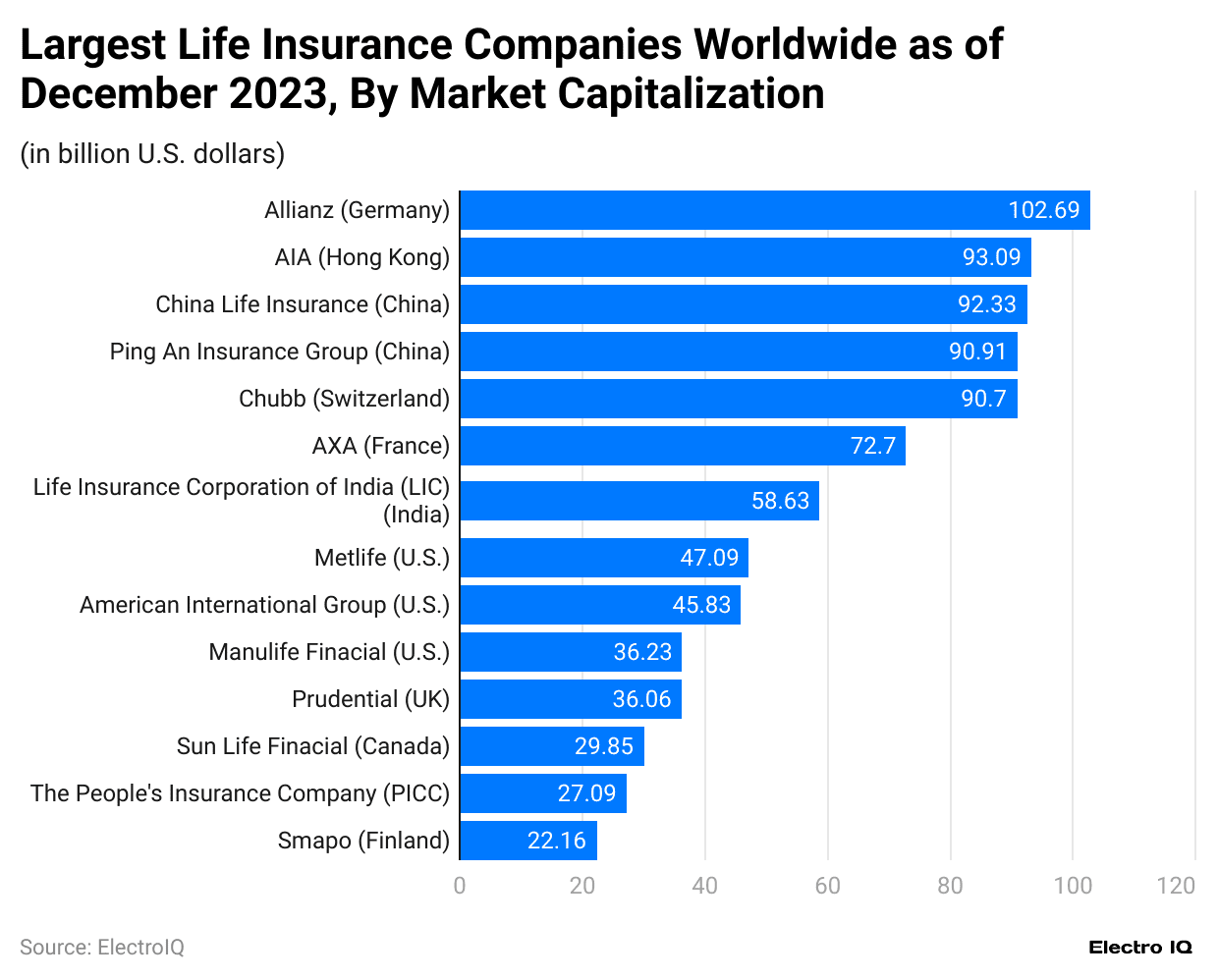

Largest Insurance Companies Worldwide By Market Capitalization

(Reference: statista.com)

- Drone Insurance Statistics showcase that Manulife Financial from Canada, Sun Life Financial from Canada, China Life Insurance from China, Prudential Financial from the U.S., Sampo from Finland, Metlife from the U.S., Ping An Insurance Group from China, AIA from Hong Kong, Chubb from Switzerland, AXA from France, American International Group from the U.S., Life Insurance Corporation of India (LIC) from India, The People’s Insurance Company (PICC) from China, Allianz from Germany, Prudential from the UK rank among largest life insurance companies worldwide.

- Allianz has the highest market cap with $102.69 billion, followed by AIA with $93.09 billion market capitalization, China Life Insurance with $92.33 billion, Ping An Insurance Group with $90.91 billion, Chubb with $90.7 billion, AXA with $72.7 billion, Life Insurance Corporation of India (LIC) with $58.63 billion, Metlife with $47.09 billion, American International Group with $45.83 billion, Manulife Financial with $36.23 billion, Prudential Financial with $36.06 billion, Prudential (UK) with $30.93 billion, Sun Life Financial with $29.85 billion, The People’s Insurance Company (PICC) with $27.09 billion, Sampo with $22.16 billion.

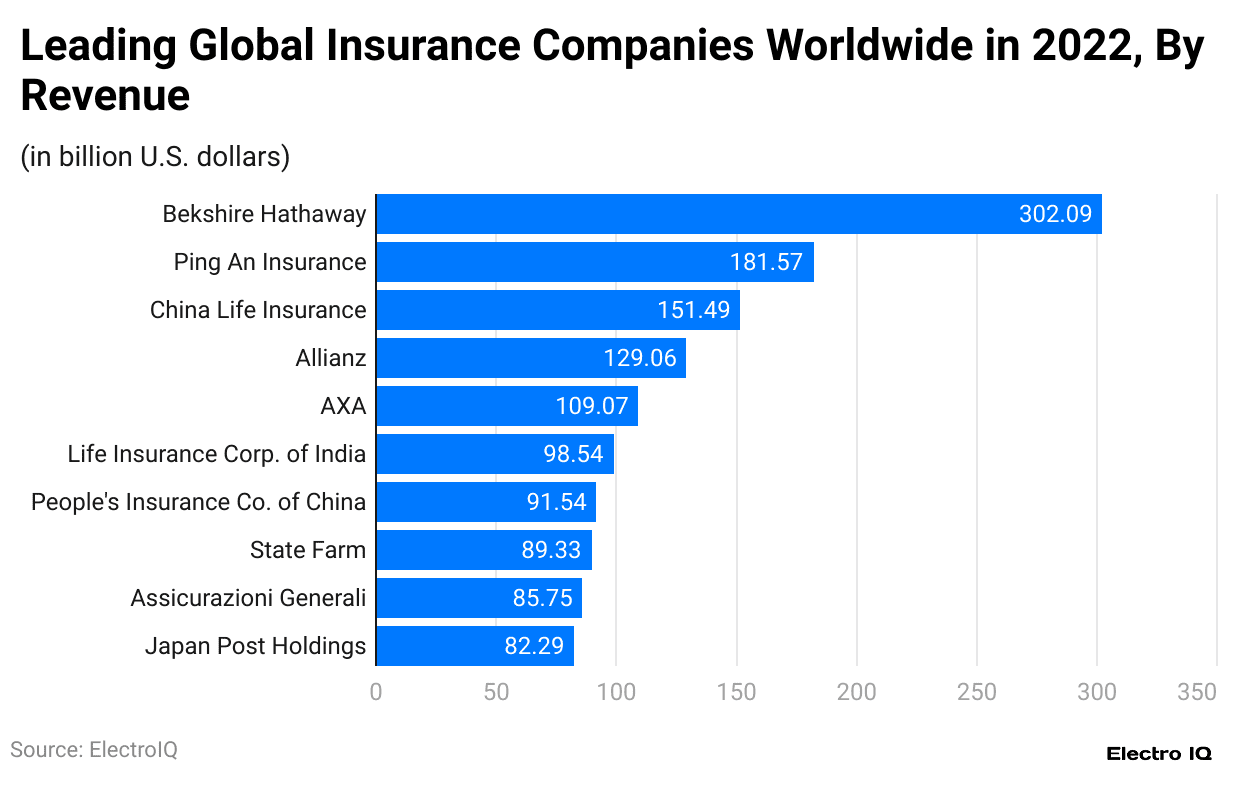

Largest Insurance Companies Worldwide By Revenue

(Reference: statista.com)

- Drone Insurance Statistics showcase Ping An Insurance, Assicurazioni Generali, AXA, People’s Insurance Co. of China, Life Insurance Corp. of India, Allianz, Japan Post Holdings, Berkshire Hathaway, China Life Insurance, and State Farm are leading insurance companies worldwide.

- Berkshire Hathaway has the highest revenue among insurance companies, with $302.09 billion, Ping An Insurance with $181.57 billion revenue, China Life Insurance with $151.49 billion revenue, Allianz with $129.06 billion revenue, AXA with $109.07 billion revenue, Life Insurance Corp. of India with $98.54 billion revenue, People’s Insurance Co. of China with $91.54 billion revenue, State Farm with $89.33 billion revenue, Assicurazioni Generali with $85.75 billion revenue, Japan Post Holdings with $82.29 billion revenue.

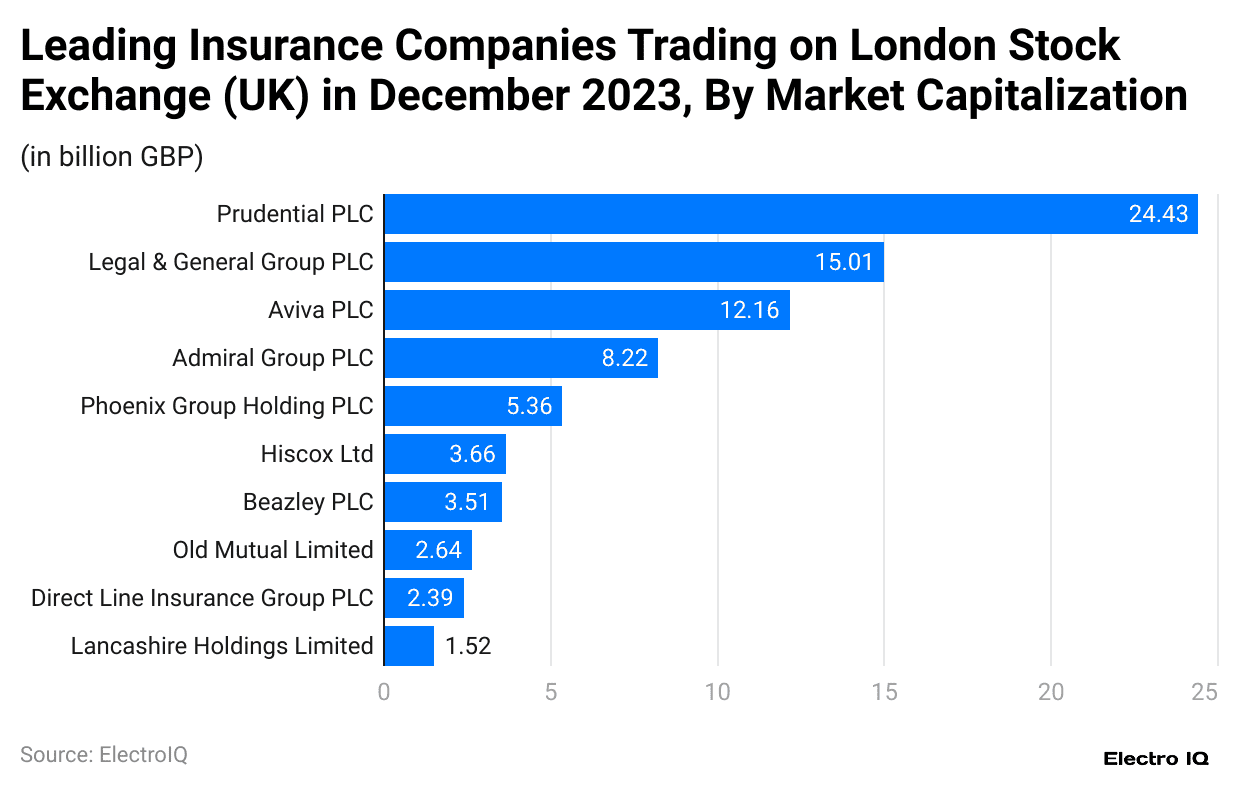

Top Insurance as the London Stock Exchange (UK) By Market Capitalization

(Reference: statista.com)

- Drone Insurance Statistics showcase that Old Mutual Limited, Admiral Group PLC, Phoenix Group Holdings PLC, Aviva PLC, Direct Line Insurance Group PLC, Lancashire Holdings Limited, Hiscox Ltd, Legal & General Group PLC, Beazley PLC, and Prudential PLC are leading insurance companies.

- Prudential PLC has highest market cap with 24.43 billion pounds, followed by Legal & General Group PLC with 15.01 billion pounds market capitalization, Aviva PLC with 12.16 billion pounds market capitalization, Admiral Group PLC with 8.22 billion pounds market capitalization, Phoenix Group Holdings PLC with 5.36 billion pounds market capitalization, Hiscox Ltd with 3.66 billion pounds market capitalization, Beazley PLC with 3.51 billion pounds market capitalization, Old Mutual Limited with 2.64 billion pounds market capitalization, Direct Line Insurance Group PLC with 2.39 billion pounds market capitalization, Lancashire Holdings Limited with 1.52 billion pounds market capitalization.

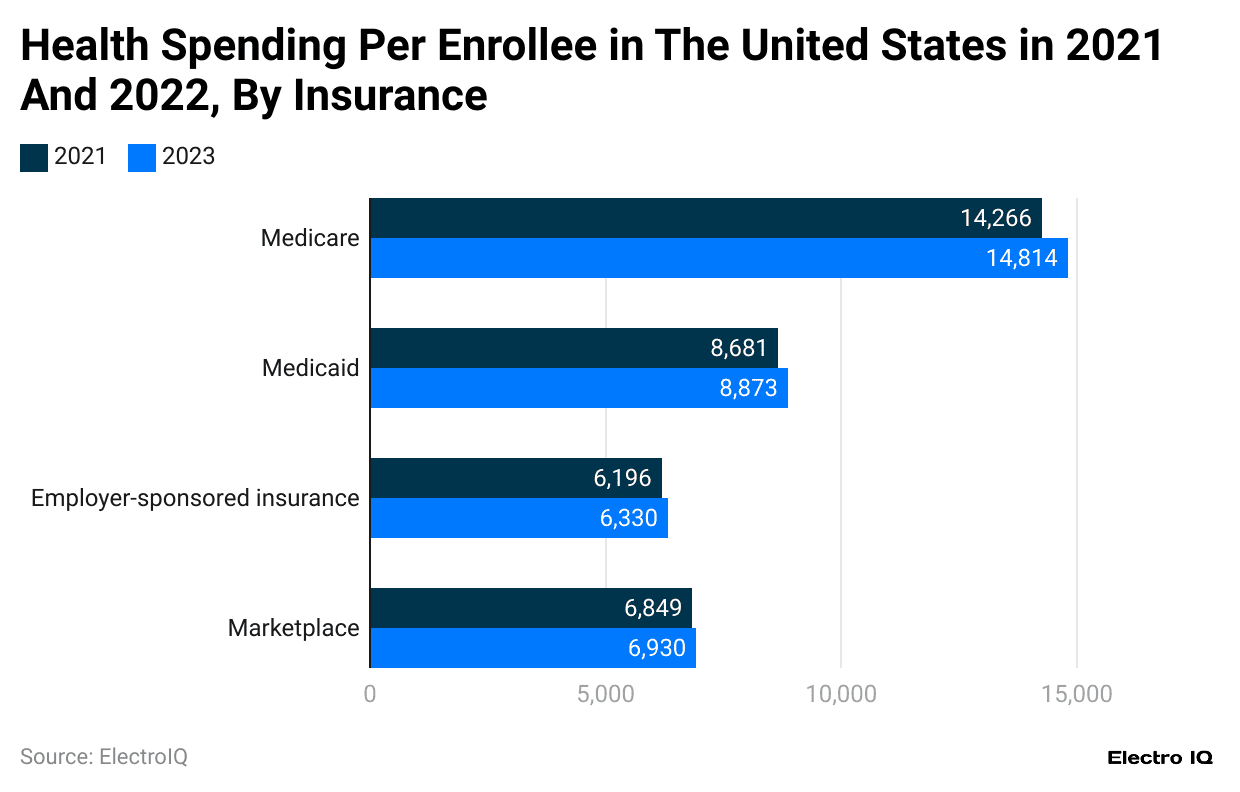

Health Spending Per Enrollee in The United States

(Reference: statista.com)

- Drone Insurance Statistics showcase that health spending per enrollee can be categorized into the following: Marketplace, Medicaid, Employer-sponsored insurance, and Medicare.

- Medicare has the highest spending per enrollee, at $14,814 billion in 2023.

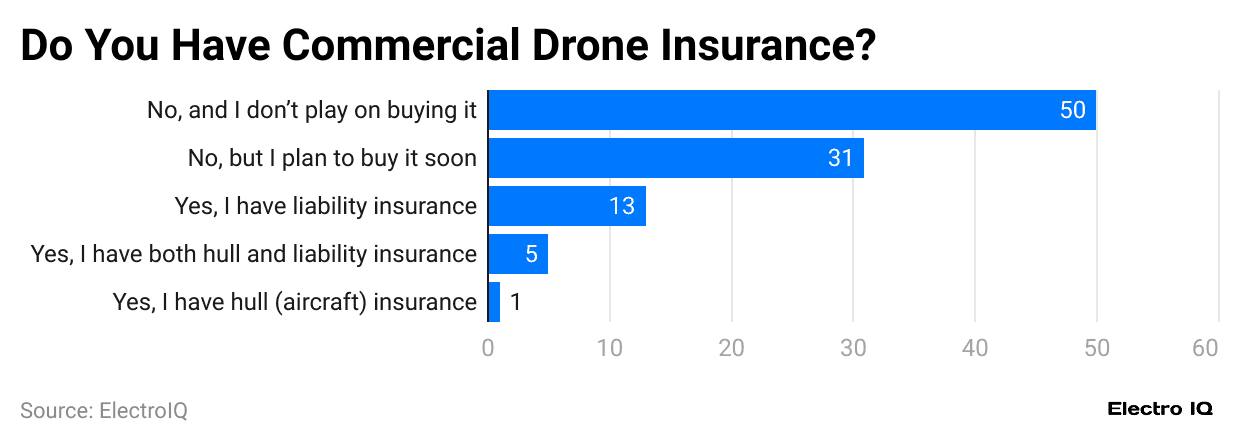

Pilots Owning Drone Insurance

(Reference: statista.com)

- Drone Insurance Statistics show that the likelihood of commercial drone insurance is mostly negative among 50% of respondents.

- Only 1% of respondents have aircraft insurance.

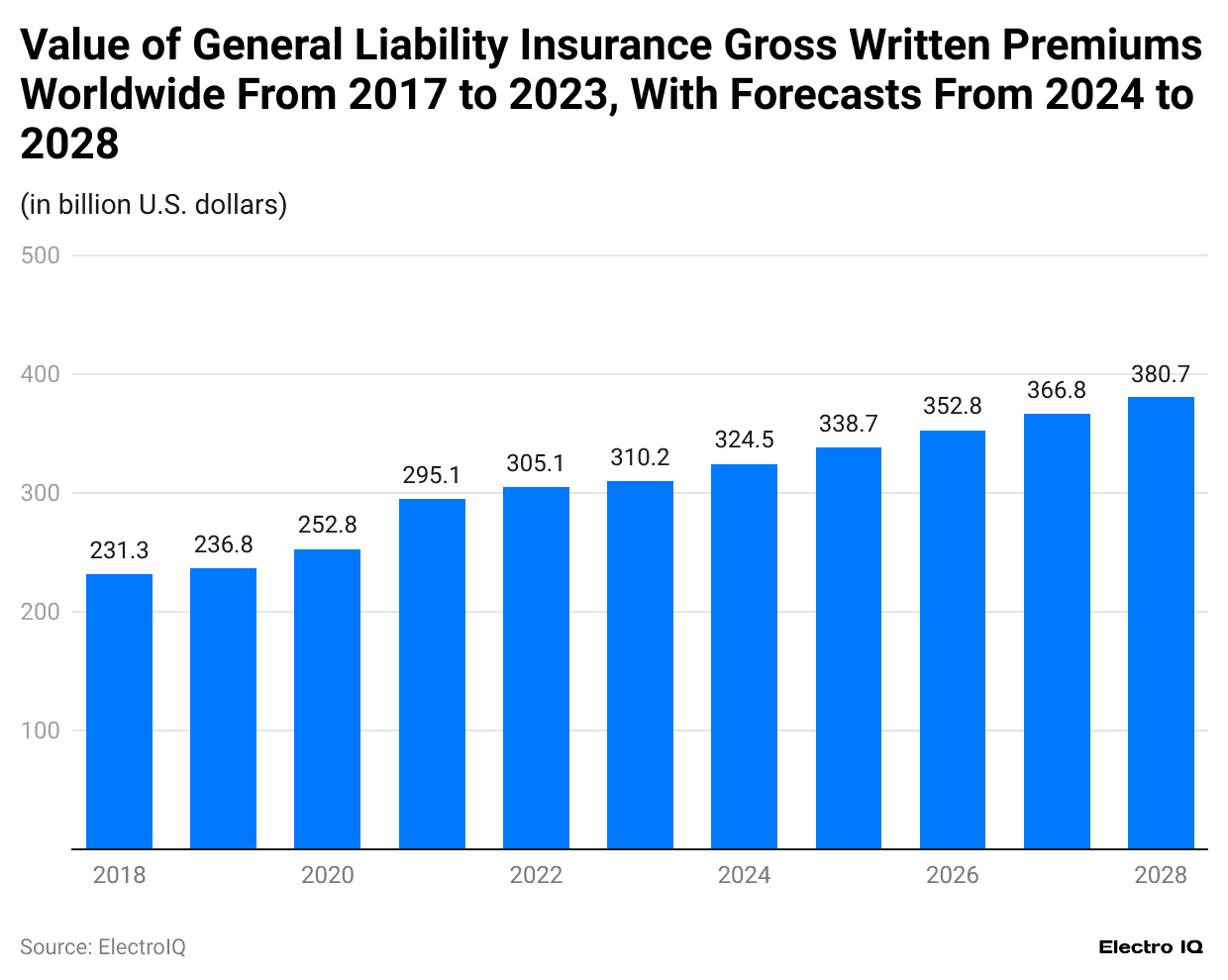

Global General Liability Insurance Market Forecast

(Reference: statista.com)

- Drone Insurance Statistics showcase that the general insurance liability has increased over time.

- In 2017, the general liability insurance value was $214.5 billion, but it had increased to $310.2 billion by the end of 2023.

- By the end of 2028, the general liability insurance value is estimated at $380.7 billion.

Drone Insurance overview

Drone insurance is becoming increasingly important as the use of drones continues to rise across industries such as agriculture, construction, and media. With the advancement of drone technology, businesses and individuals need to protect their investments, driving the growth of the drone insurance market. As of 2023, the drone insurance market is valued at approximately US$1.2 billion. This figure is expected to grow substantially over the coming years, with a projected value of US$1.9 billion by 2024.

#1. Why is Drone Insurance Important?

Drone insurance covers various risks that drone operators face, such as damage to the drone itself, third-party liability, and loss of equipment. It is essential for both commercial and recreational drone users. With drones being used for more professional applications, such as aerial photography, surveying, and delivery services, the need for comprehensive insurance coverage has grown significantly.

In 2023, around 60% of drone insurance policies were purchased by commercial operators, while the remaining 40% were for personal or recreational use. This trend indicates that businesses increasingly see drones as vital tools and want to protect their assets with proper insurance. The rise in drone-related accidents has also led to a surge in demand for insurance policies. Reports show that drone-related incidents increased by about 15% from 2022 to 2023.

#2. Types of Drone Insurance Coverage

Drone insurance typically includes two primary forms of coverage: hull insurance and liability insurance. Hull insurance covers the physical damage to the drone itself, while liability insurance protects operators from claims arising from damages or injuries caused by the drone.

In 2023, liability insurance accounted for around 65% of the total drone insurance market. This is because many drone operators are primarily concerned about the risks of injuring someone or damaging property during operations. On the other hand, hull insurance made up 35% of the market as operators seek to protect their expensive drone equipment from crashes or malfunctions.

As we move into 2024, the market share of these insurance types is expected to remain consistent, with liability insurance still leading the way. This highlights the growing awareness among operators about the potential legal and financial risks of drone operations.

#3. Drone Insurance Premiums in 2023 and 2024

The cost of drone insurance premiums varies based on factors like the type of drone, its value, and the level of risk involved in its operation. In 2023, the average premium for drone insurance ranged between $500 and $1,500 US dollars annually, depending on the drone’s coverage type and size. For more advanced commercial drones used in industries like construction or logistics, premiums could exceed $2,000 per year.

By 2024, these premiums are expected to rise by approximately 10% as the number of drones in operation continues to increase and as regulatory requirements for drone insurance become stricter. Additionally, as drone technology becomes more sophisticated and expensive, insurance companies will adjust their premiums to cover the increased risk.

#4. Market Growth Drivers

Several factors are driving the growth of the drone insurance market. One of the main factors is the increasing use of drones across various industries. For example, agriculture uses drones for crop monitoring, while the construction industry employs them for site inspections. In 2023, the agriculture sector accounted for about 25% of all commercial drone insurance policies, making it one of the largest sectors requiring drone coverage. The media and entertainment industry followed closely behind, with around 20% of the policies being issued for drones used in film and photography.

Another factor contributing to market growth is the rising number of drone regulations. Governments worldwide are implementing stricter rules for drone usage, including mandatory insurance requirements for commercial operators. This is expected to further boost demand for drone insurance in 2024. In fact, by the end of 2024, it is estimated that over 75% of commercial drone operators will have some form of drone insurance, up from 68% in 2023.

#5. Challenges in the Drone Insurance Market

Despite its growth, the drone insurance market faces particular challenges. One of the primary issues is the need for standardized regulations across different countries. While some nations, like the United States and the United Kingdom, have well-defined drone operations and insurance rules, others still develop their frameworks. This creates uncertainty for drone operators and insurance providers, potentially slowing market growth in regions with unclear regulations.

Additionally, the high cost of drone insurance premiums can be a barrier for small businesses or individual operators who may need help to afford the coverage they need. As more affordable insurance options become available in 2024, this could help to mitigate the problem and allow more operators to obtain the necessary coverage.

#6. Future Trends in Drone Insurance Statistics

Looking ahead, the future of drone insurance statistics points to continued growth and expansion. By 2024, the drone insurance market is expected to increase by over 20%, driven by new drone applications in logistics and delivery services. With companies like Amazon and UPS testing drone delivery systems, the demand for high-value insurance policies will rise significantly.

Furthermore, technological advancements in drones, such as improved sensors and navigation systems, will likely reduce accident rates in the long term. This could lead to lower premiums as insurers adjust their pricing models to account for reduced risk. However, in the short term, the rising number of drones in operation means that premiums will likely continue to increase.

Conclusion

Drone insurance is rapidly becoming a crucial component of the broader insurance industry, driven by the increasing use of drones across various sectors. Drone Insurance Statistics reveal that the market was valued at $1.2 billion, with projections indicating growth to $1.9 billion by 2024.

Looking ahead, technological advancements in drone capabilities may lead to reduced accident rates and potentially lower premiums in the long term. Integrating drones into new sectors, such as logistics and delivery services, is expected to drive market growth further.

FAQ.

Drone insurance is financial coverage for drone accidents, primarily related to property damage and liability.

It protects investments and covers risks such as damage to the drone, third-party liability, and loss of equipment.

The two primary forms are hull insurance (covering physical damage to the drone) and liability insurance (protecting against claims from damages or injuries caused by the drone).

Saisuman is a skilled content writer with a passion for mobile technology, law, and science. She creates featured articles for websites and newsletters and conducts thorough research for medical professionals and researchers. Fluent in five languages, Saisuman's love for reading and languages sparked her writing career. She holds a Master's degree in Business Administration with a focus on Human Resources and has experience working in a Human Resources firm. Saisuman has also worked with a French international company. In her spare time, she enjoys traveling and singing classical songs. Now at Smartphone Thoughts, Saisuman specializes in reviewing smartphones and analyzing app statistics, making complex information easy to understand for readers.