Fathom Statistics By Revenue, Users and Facts (2025)

Updated · Nov 10, 2025

Table of Contents

Introduction

Fathom Statistics: Fathom made a big entrance as a small, privacy-centric web analytics application, but by 2025, it’s a small but really strong player in the analytics world. It provides very simple but accurate site statistics, no cookies for most of the users, and a tracking script that is so small it does not affect the speed of the pages. With a sharp focus on transparency, speed, and simplicity, it’s redefining how data and property insights coexist.

The company’s bold acquisition of My Home Group has propelled its revenue and agent growth, while its commitment to lean operations is steering it closer to profitability. In this article, we will present to you the top Fathom statistics for 2025.

Editor’s Choice

- The company’s total revenue for Q2 2025 was US$121.4 million, representing a notable 36.1% year-over-year increase, largely driven by the acquisition of My Home Group.

- Fathom Realty’s agent count has grown by 21%; the company had 14,300 agents at the end of 2024, 2,200 of them coming from the My Home Group acquisition.

- The loss of net income was US$21.6 million for Fathom in 2024, which included US$6.2 million of the loss in Q4, yet the revenue for that quarter increased by 24% to US$91.7 million.

- Operational metrics improved in the second quarter of 2025, with a 34.4% reduction in the operating loss compared to the previous year. Now it stands at US$2.38 million, and the total losses within the six months have decreased by 26.7% to US$6.80 million.

- Fathom’s Adjusted EBITDA for the second quarter of 2025 was just US$29,000, which is very close to the break-even point.

- The six-month adjusted EBITDA loss was US$1.45 million, reflecting good progress toward profitability.

- Fathom Analytics serves 15,584 companies, primarily small businesses with 1-10 employees and annual revenues of US$1-10 million.

- The platform has about 0.1% market share in the web analytics market, which reinforces its privacy-oriented niche positioning.

- The customer base consists of 67% of companies with less than 50 employees, 38% which are from the U.S., and 11% are from the U.K.

History of Fathom

- 2018 → Fathom Analytics was established as a privacy-first web analytics project, launched first as an open-source “Fathom Lite” before a paid hosted product was introduced. Early public releases appeared on GitHub in late 2018.

- 2019 → Version 2 launched in October with a new dashboard, event tracking, live visitor details, weekly email reports, dashboard sharing, and 7-day trials. In November–December, an affiliate program and a WordPress plugin were released.

- 2020 → Weekly and monthly email reports expanded in January; uptime monitoring was added in May; major ingestion and aggregation refactors improved scale and speed through mid-year; a DDoS incident in November prompted additional security hardening and spam protection.

- 2021 → Version 3 entered early access in April after a multi-month analytics database migration completed in March, bringing faster queries and scalability; an “All Sites” view was added in May; EU Isolation and dedicated CDN endpoints were rolled out in October–November to improve performance and compliance.

- 2022 → A surge of interest followed the Austrian DPA decision that Google Analytics violated EU law, highlighting Fathom’s EU Isolation approach; a UTM builder and a large codebase refactor shipped in March; event filters arrived in November and LIKE filters plus trial changes in December; a dashboard rewrite was completed in July.

- 2023 → A Google Analytics importer launched in May; performance and UX upgrades continued through the year; Version 3.5 in November added date-range comparisons and grouped charts; further dashboard, API, and rate-limiting improvements were delivered.

- 2024 → A new marketing site and a refreshed public changelog went live in January; email reports were rebuilt in February; traffic-source classification and other attribution improvements were added early 2024.

- 2025 → The company confirmed leadership transition with Paul’s retirement and Jack taking the reins; advanced filters, city and region data, OS reporting, dashboard notifications, and chart milestones were introduced between January and August to enhance analysis and data quality.

Fun Facts About Fathom

- 2018 marked the establishment of Fathom Analytics as a privacy-first web analytics company, created to offer a simple alternative to invasive tracking.

- The company was co-founded by Paul Jarvis and Jack Ellis; Jarvis later retired from day-to-day operations while Ellis continues to lead product and engineering.

- The platform processes billions of pageviews and serves thousands of paying customers, reflecting sustained, profitable growth without selling personal data.

- A core product decision is to avoid collecting personal data and to operate cookie-free, which removes the need for consent banners in many jurisdictions.

- Compliance coverage includes GDPR, CCPA, ePrivacy, and PECR, while still providing key traffic insights for site owners.

- In late 2021, the team built “EU Isolation” so that EU visitor data is processed only within the EU and does not touch US-owned servers.

- EU Isolation routes EU traffic to infrastructure in Germany and Finland using Hetzner data centers, supporting strict regional data separation.

- The EU Isolation feature is enabled for all plans with no extra setup, ensuring automatic geographic data handling for customers worldwide.

Fathom Analytics - The service is positioned as a Google Analytics alternative that prioritizes simplicity and lawful data processing rather than ad-tech profiling.

- The product originated as a privacy-focused project that evolved into a hosted SaaS offering, emphasizing sustainable growth and customer-driven development.

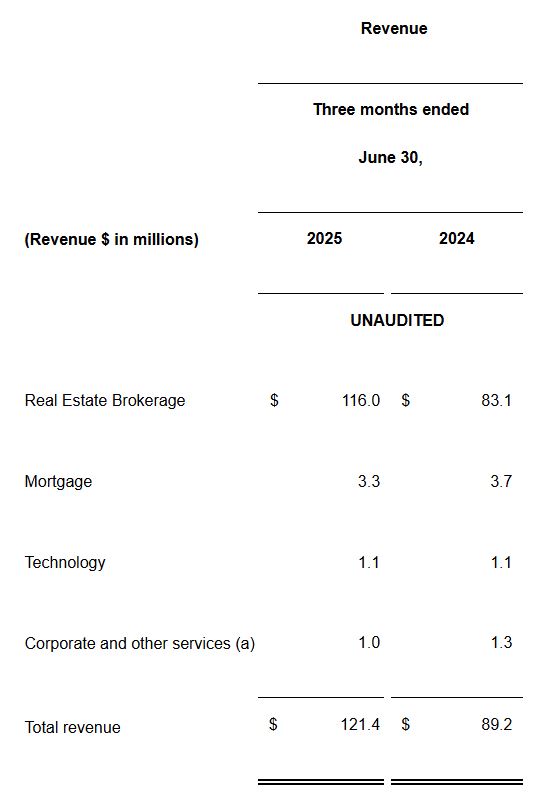

Fathom Revenue

(Source: ir.fathominc.com)

- The second quarter of 2025 demonstrated a notable improvement in Fathom’s overall performance compared to the same quarter in 2024.

- The company’s total revenue increased from US$89.2 million in Q2 2024 to US$121.4 million in Q2 2025, representing a 36.1% year-over-year increase.

- The primary driver of this growth was the acquisition of My Home Group, which was completed in November 2024, leading to a significant increase in Fathom’s real estate operations.

- The real estate brokerage division, which represents Fathom’s most significant business unit, was the primary beneficiary of the overall revenue growth.

- Revenue from this segment increased sharply from US$83.1 million in 2024 to US$116.0 million in 2025, thereby recording a high 39.6% increase.

- This augmentation is in line with the increased real estate transactions reported, which rose by approximately 25.4% year-over-year, reaching 12,710 transactions for the period.

- The addition of My Home Group’s business was a significant factor in this surge in transaction volume and brokerage revenue.

- Conversely, the mortgage segment experienced a minor decline, with revenue decreasing from US$3.7 million to US$3.3 million, representing a 10.8% decrease. This could be interpreted as a reflection of either less mortgage origination activity or harsher housing finance conditions during the period.

- The tech segment showed the same performance as last year at US$1.1 million, with no change in revenue, implying consistent performance but meagre growth.

- On the other hand, revenue from corporate and other services declined slightly from US$1.3 million to US$1.0 million, representing a 23.1% decrease, likely due to internal restructuring or reduced auxiliary service activity.

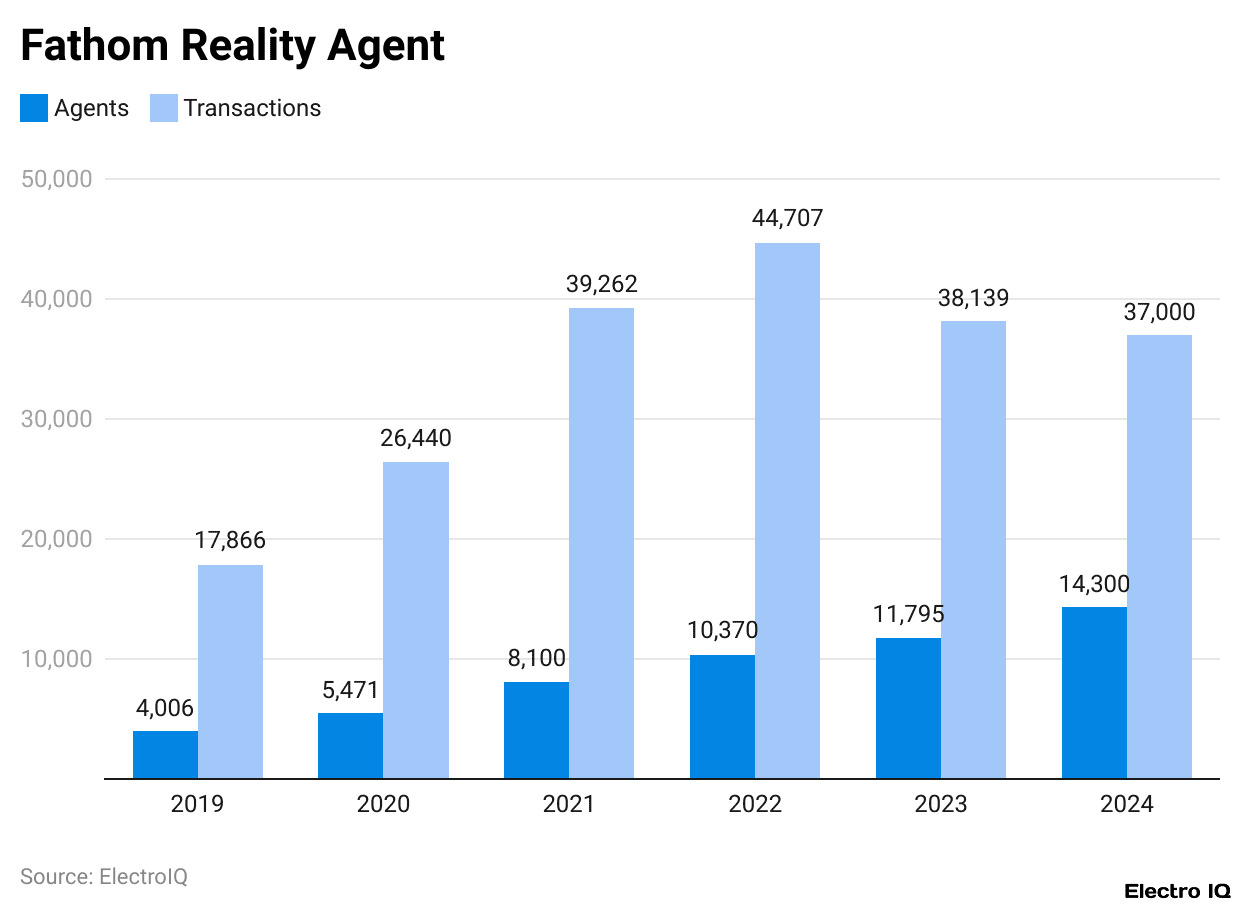

Fathom Reality Agent

(Reference: inman.com)

- Fathom Realty ended the year 2024 as one of the few real estate firms to record growth in a hard housing market.

- The company’s original flat-fee and revenue-sharing commission models, together with its purchase of Arizona’s My Home Group, accounted for a whopping 21% increase in agent count, even though there were fewer transactions, and the company faced larger losses.

- Fathom Holdings, which is based in Cary, North Carolina, announced a net loss of US$21.6 million for the year, which included a US$6.2 million loss in the last quarter.

- However, revenue for the quarter increased by 24% compared to the previous year, reaching US$91.7 million.

- The acquisition of My Home Group in November 2024, which was the third-largest brokerage in the state, added 2,200 agents immediately and further expanded Fathom’s national reach.

- The company had 14,300 agents at the end of the year, which was an increase of 2,505 agents from the year 2023, showing that the company still had a strong recruitment drive in the market, which was not very favourable.

- The wider U.S. real estate market had its hardest year in terms of existing-home sales since 1995, and Fathom’s transactions dropped by 3% to 37,000.

- Marco Fregenal, the CEO, recognised the difficulties but was still optimistic for 2025, mentioning the possibility of two new sources of revenue, a reduction of annual costs by US$2 million, and integration synergies that would lead to positive EBITDA by Q2 2025.

- While the management didn’t provide specific Q1 guidance, Fregenal hinted that the forecasts could be reinstated later in the year as conditions become more stable.

- Fathom has seen a rapid growth of agents in the last five years, with 48% of their agents in 2021 alone being the main factor of success.

- The flexible, agent-friendly commission structure is the major push behind its success. The agents pay US$700 as an annual fee, and they can choose either to pay US$465 as a transaction fee (capped at US$9,000) or to share commissions at a rate of 12% (with a ceiling of US$12,000).

- Once they reach the cap, agents only pay US$165 per transaction, thus ensuring expenses are known.

- The commission split is both a trap and a hook for the agents since they can earn more with it, and the company has the loyalty of the agents and even gets new ones.

- In 2024, the real estate brokerage revenue was 94% of Fathom’s US$335 million total revenue, which is a clear indication of the company focusing on its right area.

- The mortgage business expanded from US$7.2 million to US$10.9 million, which is a 51% increase, while the sale of Dagley Insurance for US$15 million helped the company make its better focus on real estate and lending.

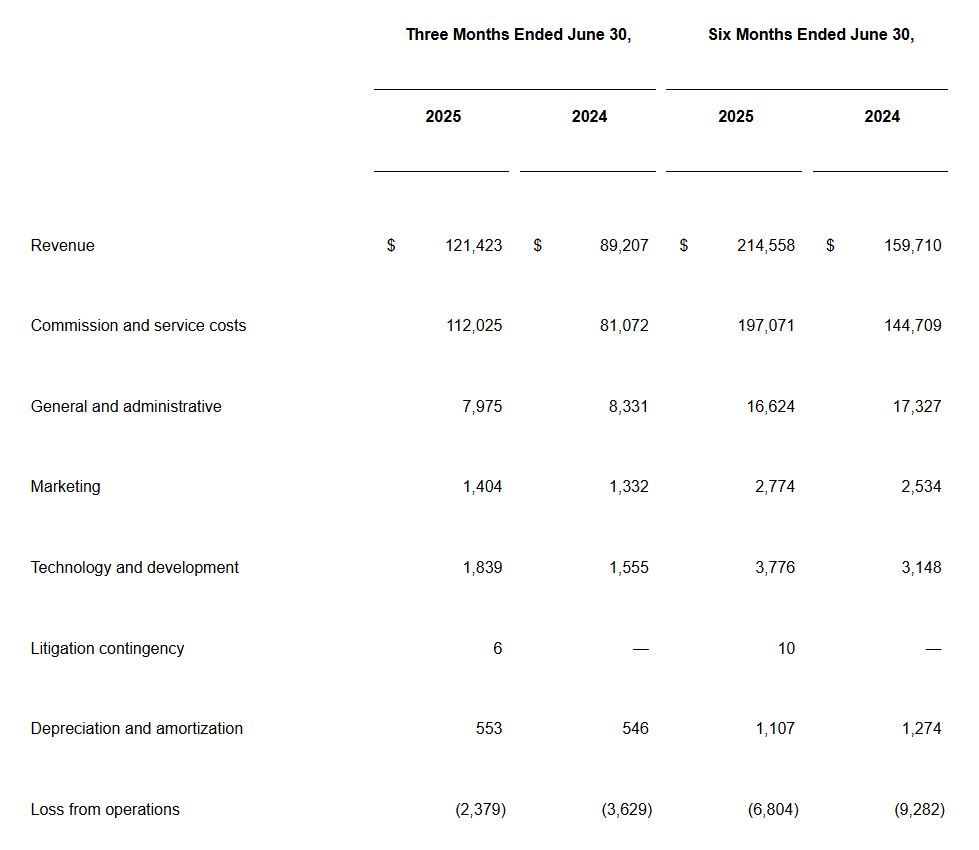

Fathom Loss From Operations

(Source: ir.fathominc.com)

- Fathom’s financial results for Q2 2025 show a significant improvement compared to the same period in 2024, even though the company is still losing money from its operations.

- Total revenue for the three months ended June 30, 2025, was US$121.4 million, compared to US$89.2 million reported in 2024.

- That accounts for an increase of 36.1% compared to the same quarter last year.

- The strong growth was mainly a result of increased real estate transactions and the incorporation of My Home Group, which not only added to the company’s agents but also increased its area of influence.

- The total commission and service costs increased in parallel with revenue growth from US$81.1 million to US$112.0 million, a 38.2% hike compared to the previous year.

- This shows that the increased activity in transactions resulted in higher payouts to agents, which goes hand in hand with Fathom’s commission-based model.

- On the other hand, general and administrative expenses shrank slightly from US$8.3 million to US$8.0 million, a 4.3% drop that signifies the company’s victory in terms of cost management and operational efficiency.

- A 5.4% increase in marketing costs, from US$1.33 million to US$1.40 million, indicates that the company is still maintaining a systematic approach in its investments toward agent recruitment and brand visibility.

- The technology and development expenditure went up from US$1.56 million to US$1.84 million, which is an 18.3% hike that denotes continued investment in digital infrastructure and platform enhancements.

- There was a minor litigation reserve of US$6,000 in 20;5 no such reserves were there in 2024.

- The depreciation and amortisation charges were almost the same at US$553,000 in 2025 and US$546,000 in 2024, which indicates a little increase of 1.3% only.

- In total, the firm registered an operating loss of US$2.38 million during the second quarter of 2025, whereas in the second quarter of 2024, it was US$3.63 million loss – a year-on-year improvement of approximately 34.4%.

- The reduction in losses is a clear indication of a stronger revenue increase and much more effective expense management in the quarter.

- During the six-month period that ended on June 30, 2025, Fathom posted revenue worth US$214.6 million, which was a 34.3% growth from US$159.7 million in the first half of 2024.

- Commission and service costs went up by 36.2% to US$197.1 million, while general and administrative expenses went down by 4.1% to US$16.6 million.

- The marketing and technology costs increased by 9.5% and 19.9% respectively, causing steady investments in growth and product innovation.

- The loss incurred during the six months was reduced from US$9.28 million in 2024 to US$6.80 million in 2025, resulting in a net decrease of 26.7%.

- It appears that the operating costs of Fathom Company are gradually decreasing to zero, as revenues are increasing, despite the challenges of disciplined cost management and market difficulties.

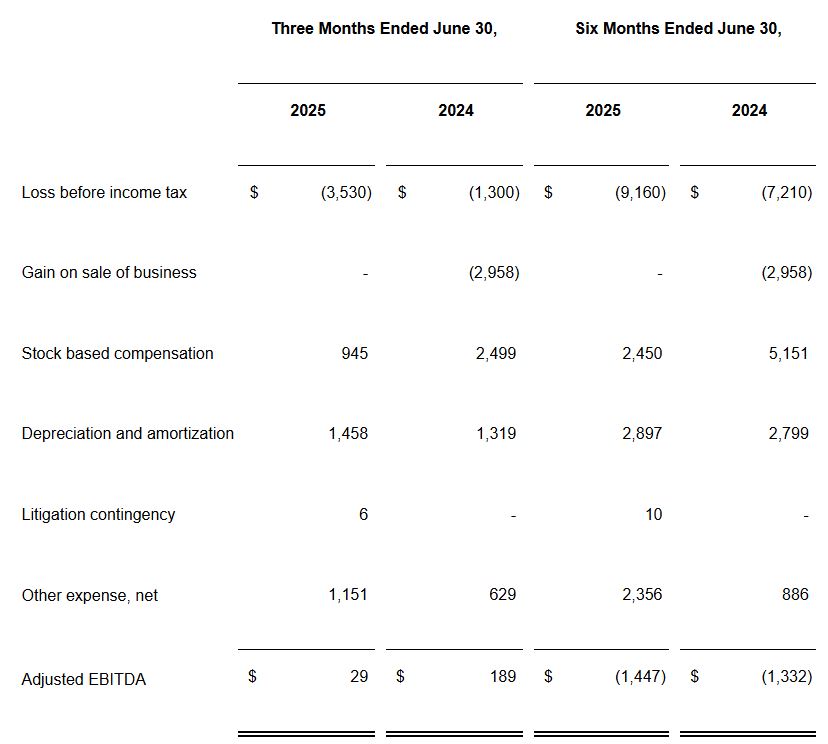

Fathom Adjusted EBITDA

(Source: ir.fathominc.com)

- Adjusted EBITDA of Fathom company for the year 2025 was still under pressure for profitability but showed a relative stabilisation compared to 2024, especially after adjustment for one-off items.

- Fathom recorded a loss of US$3.53 million before tax for the three months that ended on June 30, 2025, while the loss for the same period of the previous year was US$1.3 million— a decline of about 171% year-on-year.

- But the 2024 loss was attributed, at least in part, to a US$2.96 million gain on the sale of a business, which was not repeated in 2025. If one excludes that gain, the yearly comparison is more equitable.

- The stock-related compensation costs were reduced substantially, from US$2.5 million in Q2 2024 to US$945,000 in Q2 2025, which is a 62% cut and thus reflects the company’s commitment to controlling costs associated with equity.

- Depreciation and amortisation costs rose slightly by 10.5%, from US$1.32 million to US$1.46 million, indicating a slight increase in fixed assets or investment in capitalised technology.

- A minor litigation contingency amounting to US$6,000 was recognised in 2025, which had not been recognised in the previous year, whereas other expenses escalated from US$629,000 to US$1.15 million, accounting for an 83% rise, presumably as a result of higher financing or miscellaneous operational costs.

- For the half-year period up to June 30, 2025, the firm incurred a pre-tax loss of US$9.16 million, which is greater than the US$7.21 million loss in the first half of 2024 by 27%.

- The prior year again had the business sale gain of US$2.96 million, which affected the comparison to some extent.

- Authorities’ fees decreased by 52% from 5.15 million dollars to 2.45 million dollars, while the amount spent on the buildings increased by 3.5% up to 2.9 million dollars.

- The six-month period included litigation contingencies of US$10,000, and other expenses skyrocketed from US$886,000 to US$2.36 million, a 166% rise, which means the company has incurred higher interest or non-operating costs.

- When these items are adjusted, adjusted EBITDA for the first six months of 2025 was a loss of US$1.45 million, in contrast to the US$1.33 million loss in the first half of 2024.

Fathom Analytics’ User Base And Market Presence

- According to Enlyft, Fathom Analytics is currently being utilised by 15,584 companies.

- The platform serves a major part of very small businesses, with most users consisting of 1 to 10 employees and their annual earnings ranging from US$1 million to US$10 million.

- The data collected by Enlyft on usage spans a five-year period, demonstrating a steady adoption trend throughout.

- This indicates that, despite Fathom’s small install base, it remains significant within the segment of small businesses it targets, rather than large enterprises.

- Fathom has an approximate 0.1% (~0.09%) share of the worldwide web analytics market in terms of market share. This figure is based on the scanning of billions of public documents and the monitoring of more than 15,000 tech products.

- Geographically speaking, the platform has the most extensive usage in the U.S., with 38%, followed by the U.K., with 11%, and the rest is divided among other countries, with 51%. This identifies the U.S. as Fathom’s main market, together with a substantial secondary market in the U.K.

- When analysing customer size by the number of employees, it turns out that 67% of Fathom’s customers have less than 50 employees, 20% fall into the medium-sized category (most probably 50-1,000 employees), and just 12% are those who have more than 1,000 employees.

- Such data reveal a strong preference for the tool among smaller entities and little usage by larger companies.

- The strategy of targeting small businesses aligns with Fathom’s simpler feature set and highlights its branding as a privacy-compliant, lightweight analytics solution for small to medium-sized enterprises.

Conclusion

Fathom Statistics: By 2025, Fathom has confirmed its position as a tough competitor in both real estate and web analytics. The company’s acquisition of My Home Group, establishment of flat-fee and revenue-sharing models, and rigorous cost control made the revenue upsurge possible. While still a challenged firm in terms of profitability, the improvement of adjusted EBITDA, along with efficiency in operations are sign of a company moving towards the sustainable performance path.

In web analytics, Fathom’s solution is catching up with small businesses that are privacy-conscious and looking for a lightweight tool; hence, one can infer that niche, quality-driven strategies can produce steady adoption and pave the way for future growth.

FAQ.

The total revenue of Fathom for the second quarter of 2025 was US$121.4 million, which is 36.1% higher than Q2 2024’s US$89.2 million. The main factor for this growth was the purchase of My Home Group, which not only increased the real estate operations but also the transaction volumes.

At the end of 2024, Fathom Realty was home to 14,300 agents, which was a 21% increase from the previous year. The merger with My Home Group brought in an additional 2,200 agents, which was a clear sign of strong recruitment even though the housing market was tough.

Fathom’s operating loss was US$2.38 million in Q2 2025, which is less than the previous year’s loss of US$3.63 million by 34.4%. This is due to the higher turnover and effective expense management.

There are 15,584 companies that use Fathom Analytics, and most of them are small businesses consisting of 1-10 employees and having an annual revenue of US$1-10 million. The platform has a market share of about 0.1% and is liked for its privacy, subtlety, and easy-to-use features.

Fathom’s strategy for profitability consists of agent recruitment, maintaining cost discipline, and making strategic acquisitions. The operational efficiencies, the integration of new revenue channels, and the controlled investments in technology and marketing are the ways that Fathom will achieve positive adjusted EBITDA and sustainable growth in 2025.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.