Ibotta Statistics By Revenue, Demographics And Facts (2025)

Updated · Jul 18, 2025

Table of Contents

Introduction

Ibotta Statistics: Ibotta, an eminent mobile tech company native to the United States, has changed the way in which consumers earn cash back on everyday purchases. Since 2011, it has paid out billions, amounting to US$1.5 billion in cash rewards to its users. In 2024, the company registered tremendous growth with increased user engagement, more partnerships, and strong financial results.

This article will show the critical milestones and Ibotta statistics that have marked a charted pathway of success in 2025.

Editor’s Choice

- In 2024, Ibotta became a US$367.3 million company, growing 15% year over year. If excluding a one-time breakage benefit of US$13.5 million recognised in 2023, the company’s non-GAAP revenue growth hit 20%.

- Redemption revenue comprised the bulk of this, at US$308.8 million, a 27% increase over the prior year. Without the breakage D2C redemption revenue benefit, non-GAAP redemption revenue growth was 34%.

- In 2024, Incentive Promotion Network (IPN) grew to an average population of 14.7 million redeemers from 8.2 million in 2023, a 78% increase.

- Another rise happened in redemptions as well, with 344.1 million in 2024 compared with 256.2 million in 2023, marking a 34% year-over-year increase in redemptions.

- Net income stood at US$68.7 million or 19% of total revenue, while adjusted net income amounted to US$89.0 million or 24% of revenue.

- EBITDA was adjusted to a whopping US$112.2 million, providing an adjusted EBITDA margin of 31%.

- The company also created US$115.9 million in cash flows from operating activities and US$105.7 million in free cash flow in the year.

- The company bought back 0.5 million shares for US$31.2 million, with a net average purchase price of US$60.23 per share, excluding negligible broker commissions.

Ibotta Revenue

(Source: investors.ibotta.com)

- As per company reports, Ibotta statistics show that revenue generation for Ibotta in 2024 was US$367.3 million, a 15% rise from the US$320 million generated in 2023.

- The company claims to have two major streams of revenue: one from direct consumers and the other from third-party publishers.

- On the direct-to-consumer revenue side, which generally contributes to most of the revenue, a major drop was witnessed.

- Redemption revenue was down 21%, from US$163.7 million in 2023 to US$128.6 million in 2024.

- Ad and other revenue were down 23%, slipping from US$76.2 million to US$58.4 million. Thus, total direct-to-consumer revenue declined 22% year over year, from US$239.8 million to US$187 million.

- Meanwhile, there was a strong growth in revenues from the third-party publishers. Redemption revenue category increased by 125%, from US$80.2 million in 2023 to US$180.3 million in 2024.

- The redemption revenues after combining the two channels went up by 27%, from US$243.9 million to US$308.8 million.

- Conversely, ad revenues and others overall saw a downward trend of 23%, from US$76.2 million to US$58.4 million.

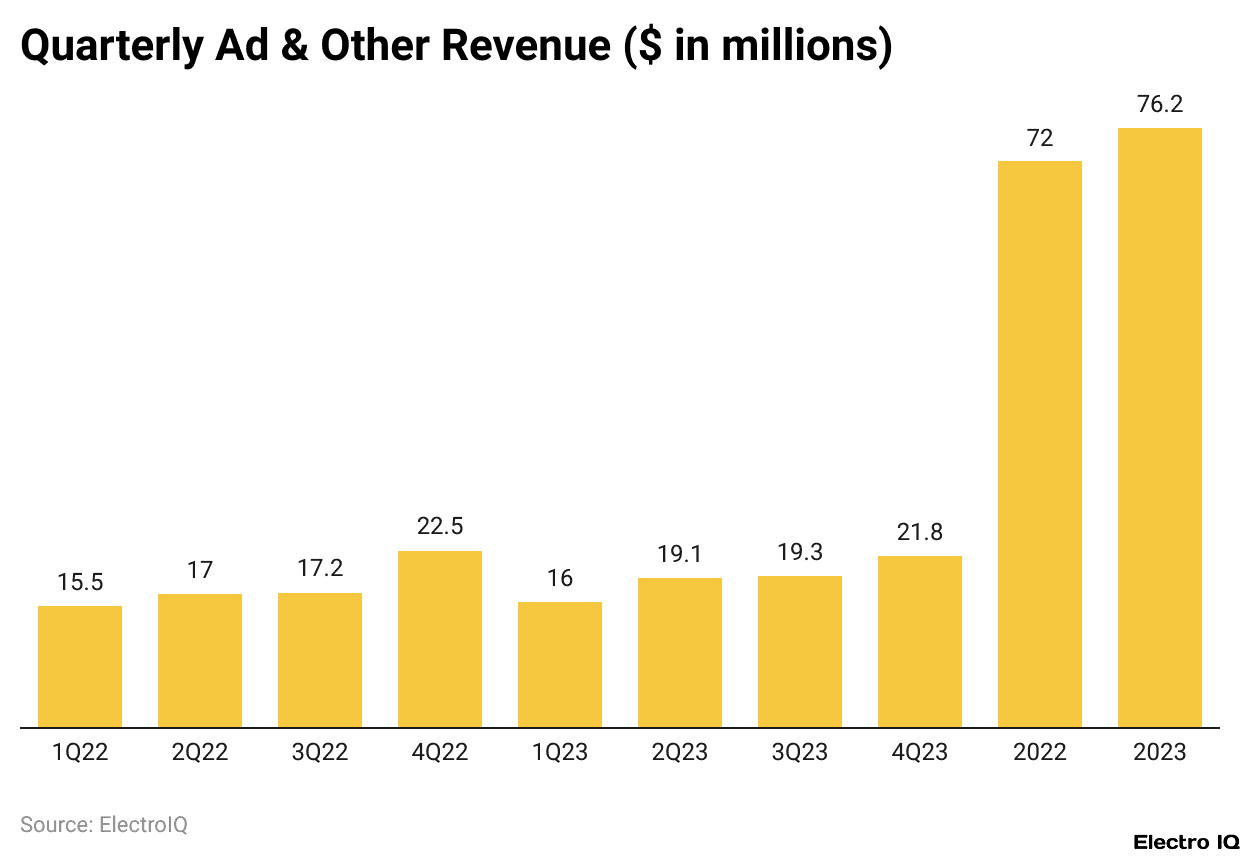

- The quarterly data (for the period ending December 31) gives a mixed picture as well. In Q4 2024, total revenue was US$98.4 million, down by 1% as compared to US$99.7 million in Q4 2023.

- It comprised a 6% increase in redemption revenue (from US$77.9 million to US$82.4 million), but a 27% decrease was noticed in ad and other revenue (from US$21.8 million to US$16 million).

- Overall, while revenues from direct-to-consumer declined considerably in the year 2024, the mushrooming redemption revenues of third-party publishers fuelled the overall revenue growth of the company.

Ibotta Stock-Based Expense

(Source: investors.ibotta.com)

- Ibotta experienced a large increase in stock-based compensation expenses amounting to US$76.2 million, as opposed to US$20.2 million in 2023. This witnessed a 278% rise year over year.

- By function, cost of revenue had US$1.5 million in stock-based compensation in 2024, up from US$659,000 in 2023.

- Sales and marketing, on the other hand, experienced the biggest share, shooting from US$15.4 million in 2023 to US$39.1 million in 2024. This in itself makes up for over half of the company’s total stock-based compensation for the year.

- R&D stock-based-compensation-related expenses increased to US$9.3 million in 2024 from US$2.1 million in 2023.

- Similar may not be so, of course, general & administrative stock-based compensation jumped from US$2 million to US$26.3 million, signifying the great growth of equity-based incentives given to leadership or administration areas.

- When it comes to the fourth quarter of 2024, the total stock-based compensation was US$12.9 million, almost 2.5 times the US$5.8 million recorded for the same quarter in 2023.

- The single biggest general & admin expense in Q4 was US$5.8 million, with expenses of US$4.3 million in sales & marketing, US$2.3 million in R&D, and US$485,000 in cost of revenue.

- The sharp increase in stock compensation across all departments suggests that Ibotta issued substantial equity grants in 2024 for talent retention, performance rewards, or its IPO and transition as a public company.

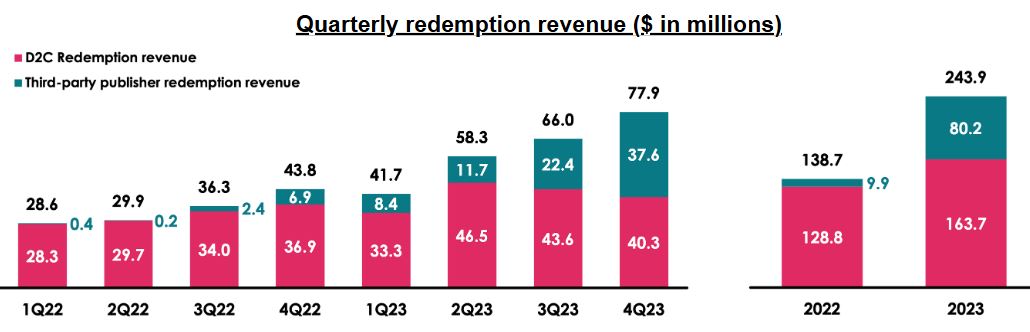

Ibotta Quarterly Redemption Revenue

(Source: sec.gov)

- Most of Ibotta’s gross revenue in 2023 was from redemptions, which made up roughly 76% of total revenue.

- The redemptions are said to take place when consumers use offers through Ibotta’s Incentive Promotion Network (IPN). Redemption revenue in 2023 was about US$243.9 million, which was significantly higher than US$138.7 million in 2022.

- From this, one may infer that there has been a solid growth year over year in the usage of cashback and reward-based promotions across the platform, thus keeping redemptions as a core dynamic of Ibotta’s business model.

Ibotta Ad And Other Revenue

(Reference: sec.gov)

- Besides its core revenues from redemptions, a good share is also earned via advertising and other data-driven service routes.

- This segment accounted for about 24% of total company revenues in 2023, or US$76.2 million, a slight increase from US$72.0 million recorded in 2022. This steady track of growth represents the increasing demand by consumer packaged goods (CPG) brands for more targeted and data-rich promotional tools.

- Ibotta sells advertising opportunities on its D2C platforms directly for brands to advertise their campaigns to very engaged users. These digital ads are mostly implemented alongside offer redemption campaigns and can either take the entire course of the campaign or just part of it.

- In essence, a client is charged by Ibotta a fixed dollar amount for the ads, thus bringing predictability in the pricing structure for the brands.

- The Ibotta platform also processes vast amounts of consumer data, which the company monetises via services in media, audience targeting, and data licensing.

- Brands can purchase consumer behaviour data about location and purchasing trends to optimise their promotional strategies. This helps Ibotta to give its partners good insights for decision-making regarding marketing activities, while it also earns licensing revenue from selling the use of its data assets.

- So, while redemption alone remains at the core of Ibotta’s business model, its advertising and data monetisation fronts have been gaining more weight on the revenue side, constituting scalable growth opportunities and further cementing brand partnerships.

Ibotta Adjusted EBITDA

(Source: investors.ibotta.com)

- According to Ibotta, net income for 2024 stood at US$68.7 million compared with US$38.1 million in 2023, thus showing strong growth in the bottom line.

- In the fourth quarter alone, net income came in at US$76.2 million, a huge bump from US$18.6 million recorded in the same quarter of 2023.

- The biggest adjustment came from stock-based compensation, at US$76.2 million for the year, which reflected a marked increase from US$20.2 million in 2023.

- In Q4 alone, stock-based compensation amounted to US$12.9 million, more than twice that of US$5.8 million in Q4 2023.

- Other adjustments consist of depreciation and amortisation of US$8.1 million in 2024 and US$6.7 million in 2023, which also includes the loss on debt extinguishment of US$9.7 million from 2024, which was absent in the year prior.

- Ibotta also recorded a US$3.1 million change in fair value of a derivative compared with US$5 million in 2023. Interest income of US$9.4 million in 2024 contrasted with interest expenses of US$6.9 million in 2023.

- There was a reversal of income tax benefit from US$44.2 million in 2024 to an income tax provision of US$5.9 million in 2023.

- Adjusted EBITDA for Q4 2024 was US$27.8 million, slightly less than US$33 million in Q4 2023; however, net income margin on a revenue basis for 2024 was 19%, up from 12% in 2023, depicting improved profitability.

- The adjusted EBITDA margin inched higher, moving from 26% in 2023 to 31% in 2024, a stellar indication of efficiency and revenues being well-earned, despite adverse expenses like stock-based compensation.

Ibotta Customers

(Source: businessdasher.com)

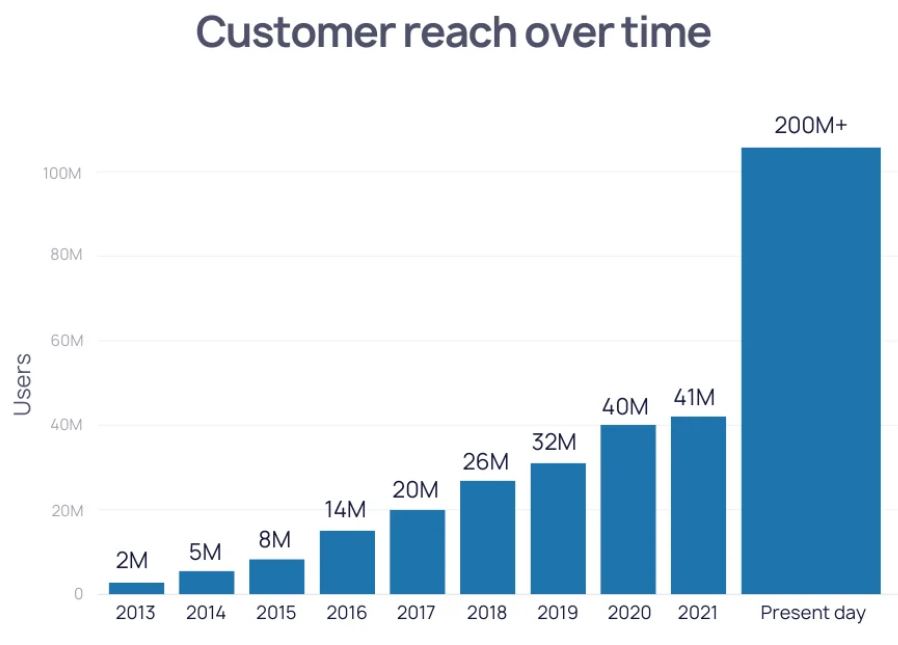

- As per Businessdasher, Ibotta statistics indicate that while counting active users currently using the platform, it stands tall at 50 million active users. More than 200 million consumers have interacted in some way with Ibotta over its lifetime, conveying a measure of broad appeal and reach.

- The platform has been connected with 91% of U.S. houses, ranked as one of the nation’s largest and favourite American shopping applications. User engagement has been significant, with each person opening the Ibotta app roughly 7 times a week and recording 25 to 30 sessions a month.

- The frequency goes on to speak volumes about how Ibotta has attached itself to the shopping and savings routine of almost all its users.

- Financially, Ibotta registered US$320.04 million in revenue in 2023, achieving 51.89% growth on a year-to-year basis, assurance of operational success, and growing demand in the market.

- On a very substantial level, the platform aids in massive savings for consumers, with payouts of close to US$2,500 every day going to users.

- Over the past seven years, Ibotta has returned US$1.8 billion-plus in cashback rewards to consumers, thus building a reputation as a major tool to assist budget-conscious consumers.

Ibotta Age Demographics

(Reference: businessdasher.com)

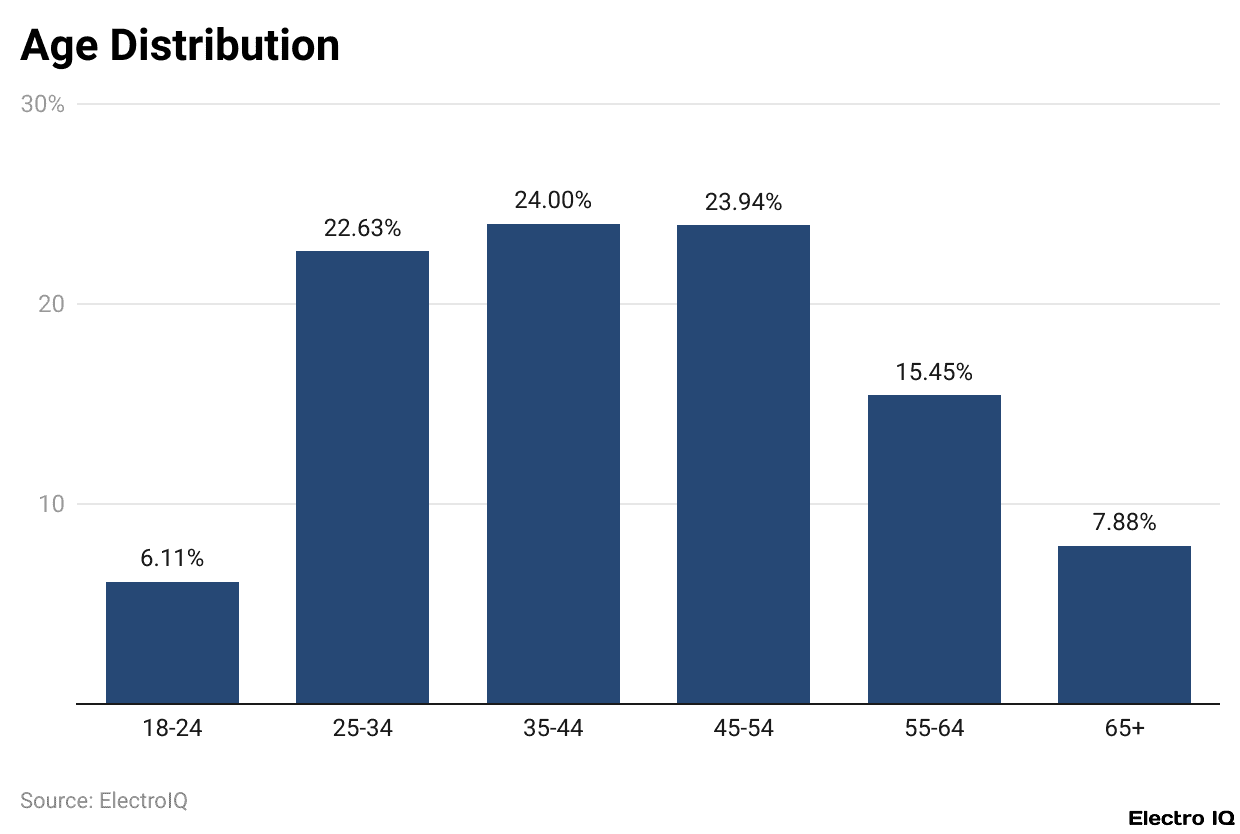

- As per Businessdasher, Ibotta facts state that the app is mainly used by women, who make up 72.38% of all users, while men make up the remainder, which is 27.61%.

- Adults aged between 25 and 54 years constitute 56% of the total user base. Users below 25, on the other hand, account for 44%, the mark of a somewhat older demographic leaning toward working adults and parents.

- Women also lead in savings: 70% of the top savers on the platform are female. This indicates quite a few budget-conscious women who actively use Ibotta to squeeze the best cashback and promotional offers.

Ibotta Stock Price Statistics

- Ibotta has seen its stock price drop by 47.91% over the last year, signaling either a sharp decline in investor confidence or market volatility affecting the company.

- The 50-day moving average, at present, stands at US$44.82.

- On the contrary, the 200-day moving average is higher at US$57.34, thus indicating a downward trend in prices along with bearish sentiments of the market.

- The Relative Strength Index (RSI) stands at 34.70, which is pretty close to the oversold territory of 30; with this, indications are that the stock is nearing undervaluation and might grab investor attention with strong fundamentals.

- The average daily volume in the past 20 days has seen around 371,809 shares being traded, reflecting a moderate level of activity.

- Without a 5-year beta figure, it is somewhat difficult to ascertain how volatile it may have been over time against market benchmarks.

Ibotta Dividends and Yield

- Ibotta does not presently pay dividends to shareholders, so there is no reported data about dividend per share, dividend yield, dividend growth, or payout ratio. This suggests that the company is likely to be reinvesting earnings back into the business as opposed to distributing profits to shareholders.

- Ibotta’s share buyback yield, however, is 7.28%, showing the company is actively repurchasing its own shares, a good way of giving value back to shareholders by reducing the number of shares outstanding and thereby potentially improving earnings per share.

- The shareholder yield is thus 7.28%, combining dividends and buybacks, but entirely dependent on buybacks.

- The earnings yield of the company stands at 5.74%, indicating how profitable the company is relative to its price.

- Finally, an FCF yield of 10.89% suggests a high generation level of cash and a great deal of financial flexibility, even if it chooses not to pay out dividends.

Conclusion

The performance of Ibotta in 2024 reflects a very strong business model and the ability to tune into consumer needs. With massive revenue growth, increasing user numbers, and strategic partnerships, the company has inked itself into the digital promotions corridor.

As value-conscious consumers make their shopping choices, Ibotta’s fresh take on cash-back rewards positions it for longer-term success.

Sources

FAQ.

In 2024, Ibotta generated revenues of US$367.3 million, up by 15% on a year-over-year basis. The non-GAAP revenue thus grew 20% when excluding a one-time breakage benefit in 2023. Direct-to-consumer revenues actually fell by 22%, though this was countered by a whopping 125% growth in third-party publisher redemption revenue, the latter having thus turned into a major growth driver.

The active user base has reached 50 million, and since its inception, Ibotta has reached over 200 million consumers. About 72.38% of the users are women, whereas about 56% are in the 25-54 age range. This is reflective of sizeable adoption among working-class and family-age adults. App usage is frequent: Users open the app seven times per week, and total 25-30 sessions per month.

Ibotta generated US$68.7 million in net income at a 19% net margin rate in 2024, compared with adjusted net income of US$89 million (24%). Adjusted EBITDA was reported to be US$112 million, which corresponds to a margin of about 31%. Therefore, a net operating cash flow of US$115.9 million and free cash flow of US$105.7 million would have meant a strong financial performance and liquidity for the company.

Currently, Ibotta does not pay any dividends, preferring to reinvest these funds to strengthen its growth. However, it has returned value through executing share repurchases, with a buyback yield of 7.28%. Its shareholder yield is thus entirely due to buybacks at 7.28%. The earnings yield stands at 5.74%, whereas free cash flow yield is 10.89%, underlining strong profitability and cash generation capacity.

Stock-based compensation went from US$20.2 million in 2023 to US$76.2 million in 2024, up sharply by 278%. Significant portions were allocated to sales and marketing (US$39.1 million) and general and administrative (US$26.3 million). This increase is likely reflective of talent retention efforts and support for the team in the IPO.

Tajammul Pangarkar is the co-founder of a PR firm and the Chief Technology Officer at Prudour Research Firm. With a Bachelor of Engineering in Information Technology from Shivaji University, Tajammul brings over ten years of expertise in digital marketing to his roles. He excels at gathering and analyzing data, producing detailed statistics on various trending topics that help shape industry perspectives. Tajammul's deep-seated experience in mobile technology and industry research often shines through in his insightful analyses. He is keen on decoding tech trends, examining mobile applications, and enhancing general tech awareness. His writings frequently appear in numerous industry-specific magazines and forums, where he shares his knowledge and insights. When he's not immersed in technology, Tajammul enjoys playing table tennis. This hobby provides him with a refreshing break and allows him to engage in something he loves outside of his professional life. Whether he's analyzing data or serving a fast ball, Tajammul demonstrates dedication and passion in every endeavor.