Neobank Statistics and Facts By Market Size, Growth, Revenue, User Demographics, Trends and insights (2025

Updated · Oct 27, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Neobank Market Size

- By Region

- Global Growth And Market Size By Users

- Neobank Revenue And Profitability

- Leader of US Neobanking And Payments

- User Demographics

- Average Transaction Value Per User

- Account Type Insights

- App Download Insights

- Fraud In Neobanking

- Neobanking Market Segmentation

- Key Companies and Insights

- Technological Innovations

- Neobanking Brand Shares

- New Developments

- Conclusion

Introduction

Neobank Statistics: Neobanks are banks operating mainly through applications and websites, and they have grown at a fast pace. Neobanks earned approximately USD 33.5 billion in revenue globally in 2023. The largest neobank by user count, Nubank, had about 93 million customers that same year. Revolut reached 40 million users by March 2024. Another leading U.S. competitor, Chime, had roughly 20 million accounts in 2022. Global transaction volume for neobanks was estimated at about USD 4.96 trillion in 2023.

In 2025, they are leveraging AI more than ever before. AI comes in handy in fraud detection, customer service, credit scoring, and personal financial advice. This article tries to give a clear picture of Neobank statistics on how AI is transforming neobanks in 2025.

Editor’s Choice

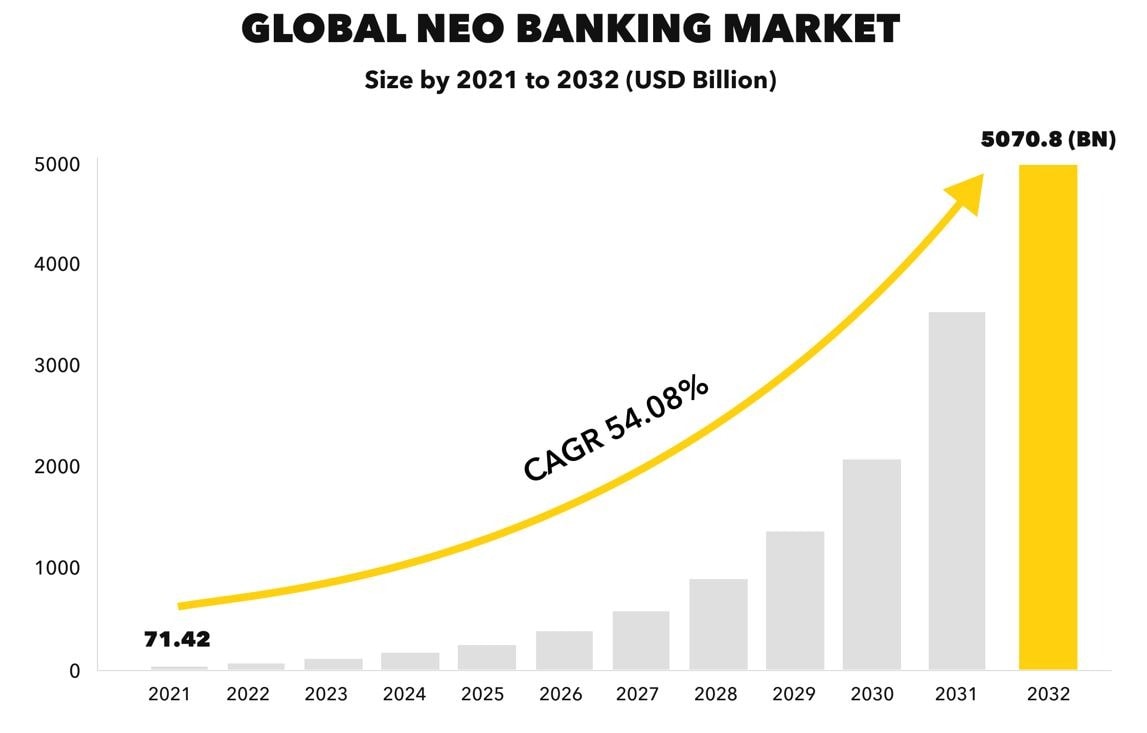

- The global neobanking market is expected to reach US$3.3 trillion by 2032, growing at the fastest CAGR of 54.09% since the inception of the financial sector.

- In 202the 3, the valuation of neobanks crossed the US$100 billion mark, with Europe in the lead with more than 80 million users accounting for 40% of the global customer base.

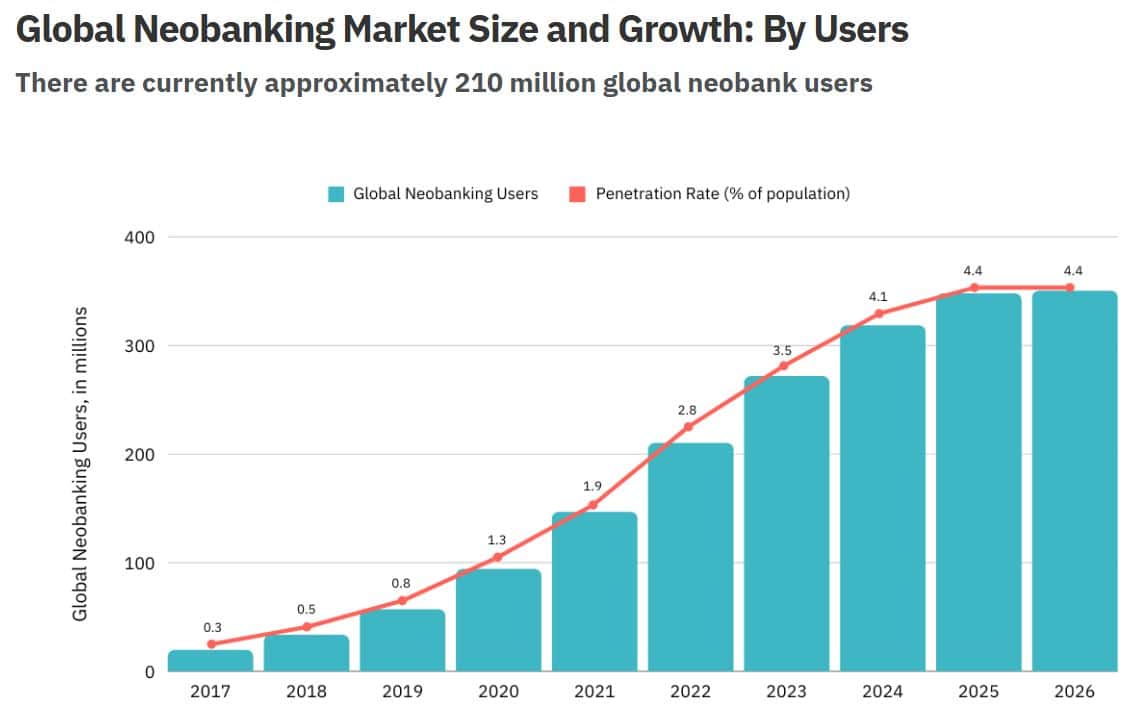

- Worldwide, neobank users grew from 146 million in 2021 to 210 million in 2022 and are expected to hit 350 million in 2026.

- In 2023, neobanks earned revenues of US$40 billion; however, almost 80% of them are still not profitable, and only 15% are expected to reach profitability by 2025.

- In the U.S., CashApp has kept a lead market share of 45%, and Chime has remained the top neobank with 10%, with a transaction value that went up 30% to US$1.43 trillion in 2023 from 2022.

- This adoption is mainly driven by younger generations, with 10.6% of digital bank users between 18-24 years of age and 10.5% in the 25-34 years age group.

- About an average user transacting US$1,200 per month, SMEs transact US$15,000 monthly, while international remittances are US$1,000 per transfer.

- In a breakdown of neobank services, 65% are for basic savings accounts; meanwhile, crypto-linked accounts rose 50% and teen banking gained 35%.

- Last year saw an unprecedented explosion of neobank app downloads, reaching 1.2 billion, with a pellet 85% of users saying it is highly intuitive, while average daily usage stands at 25 minutes.

- With twice the fraud incidents of credit cards and thrice those of debit cards, fintechs face the dilemma of keeping fraud at bay.

- In Latin America, Nubank leads with 32%, Revolut is famous across Europe with a user base of 30 million-plus, and Chime leads with 40% market share in the USA.

Neobank Market Size

(Source: dashdevs.com)

- As per Dashdevs, Neobank statistics show that the world of neobanks moves very quickly because of digital innovation.

- By 2023, the global market for neobanks had climbed to a very considerable size, reflecting the population since app-based banking became a household phrase.

- Analysts project that by the year 2032, the global neobanking market will be many times bigger than it is today, sustained by a CAGR of 54.09%.

- This would assert a market growing at an average pace of over 50% per annum, which is very rarely granted to any industry with normal growth rates.

- These numbers affirm the confidence that analysts and investors place in the seemingly endless growth of digital-first banks.

By Region

| Region | Growth/Users in 2023 |

Notable Insights

|

| Europe | 80 million users (40%) |

Highest penetration globally

|

| Asia-Pacific | 38% growth in 2023 |

Driven by India, China, and Indonesia

|

| North America | 34.6% CAGR through 2026 |

Tech-savvy millennials driving growth

|

| Latin America | 54% YOY growth |

Nubank leads with 85 million users

|

| Neobank share |

15% of global retail banking customers

|

(Source: coinlaw.io)

- As per Couinlaw statistics, Neobank statistics show that this banking has been a fairly fast-growing sector over the last few years, with global valuation crossing US$100 billion in 2023, a figure that is more than double from the US$47 billion recorded in 2020.

- Europe remains the leader, housing over 80 million users and forming 40% of the global neobank customer base.

- Growing has also been phenomenal in the Asia Pacific region, with a 38% surge from 2023, principally driven by increasing adoption in countries like India, China, and Indonesia.

- The focus for North America is to see strong growth continuing into the neobank market with a compound annual growth rate of 34.% till 2026, fueled primarily by millennials who are highly comfortable with digital financial solutions.

- Latin America has also seen great momentum, with neobank adoption increasing 54% year on year, led by Brazil’s Nubank, which had 85 million customers in 2023.

- As such, as digital banks scale up, the gap with traditional banks is narrowing, currently serving greater than 15% of the world’s retail banking clientele.

- Moving forward, about 40% of banks globally are forecasted to partner with neobanks to upscale their digital services and capabilities by the year 2024.

Global Growth And Market Size By Users

(Source: unit21.ai)

- In the year 2021, it was calculated that around 146.42 million neobanks spanned the globe.

- The number stepped to 210.02 million in 2022 and was expected to hit 350.12 million by 2026.

- Meanwhile, the penetration rate had been a mere 2.8% in 2022, but it is forecasted to reach as high as 4.4% by 2026, further signifying the increasing importance of neobanks in supporting the everyday financial transactions of a larger population.

- Also, in the U.S., the number of digital-only bank account holders is jumping, forecasted to grow from 29.8 million in 2021 to 53.7 million in 2025.

- The steady upward movement of these two, the user number and penetration rate, shows the extent of adoption and trust placed upon neobanks.

- Growing at an average rate of 35% each year over the past five years, it is clear that neobanks have become the top choice for the modern, tech-savvy population.

- People are not just experimenting with digital banking; the drifts are showing the outright exit from conventional banks, choosing neobanks for primary financial services.

- This goes to portray the ever-growing demand for digitally oriented financial services with customers’ eagerness for convenient, innovative, and user-friendly banking.

Neobank Revenue And Profitability

| Metric |

Value/Description

|

| Global revenue (2023) | $40 billion |

| US revenue (Chime and Varo) | $3.5 billion |

| Revolut revenue (2023) | $1 billion |

| Unprofitable neobanks (2023) | 80% |

| Revenue from transaction fees | 60% |

| Interest on deposits contribution | 25% |

| Venture funding (2023) | $15 billion |

(Source: coinlaw.io)

- The year 2023 witnessed neobanks across the globe reaching revenues of over US$40 billion while riding a current momentum of a further 32% CAGR achieved since 2019.

- In America, Chime and Varo together registered close to US$3.5 billion, while in Europe, Revolut hit an actual milestone by crossing the US$1 billion mark of annual revenue for the first time.

- However, notwithstanding the achievement of this height of growth, most neobanks are still far away from profitability.

- Around 80% of these keep losing money, primarily due to continuously high customer acquisition costs.

- In the composition of their revenue streams, some 60% came from transaction fees, with another 25% coming from earning interest on customer deposits in 2023.

- Profitability continues to be a barrier, and analysts predict that only 15% of neobanks will be profitable by 2025.

- Despite these financial challenges, interest from the investing sector remains strong.

- In 2023 alone, neobanks raised US$15 billion internationally in venture funding, so there remains strong interest in their potential to transform the future of banking.

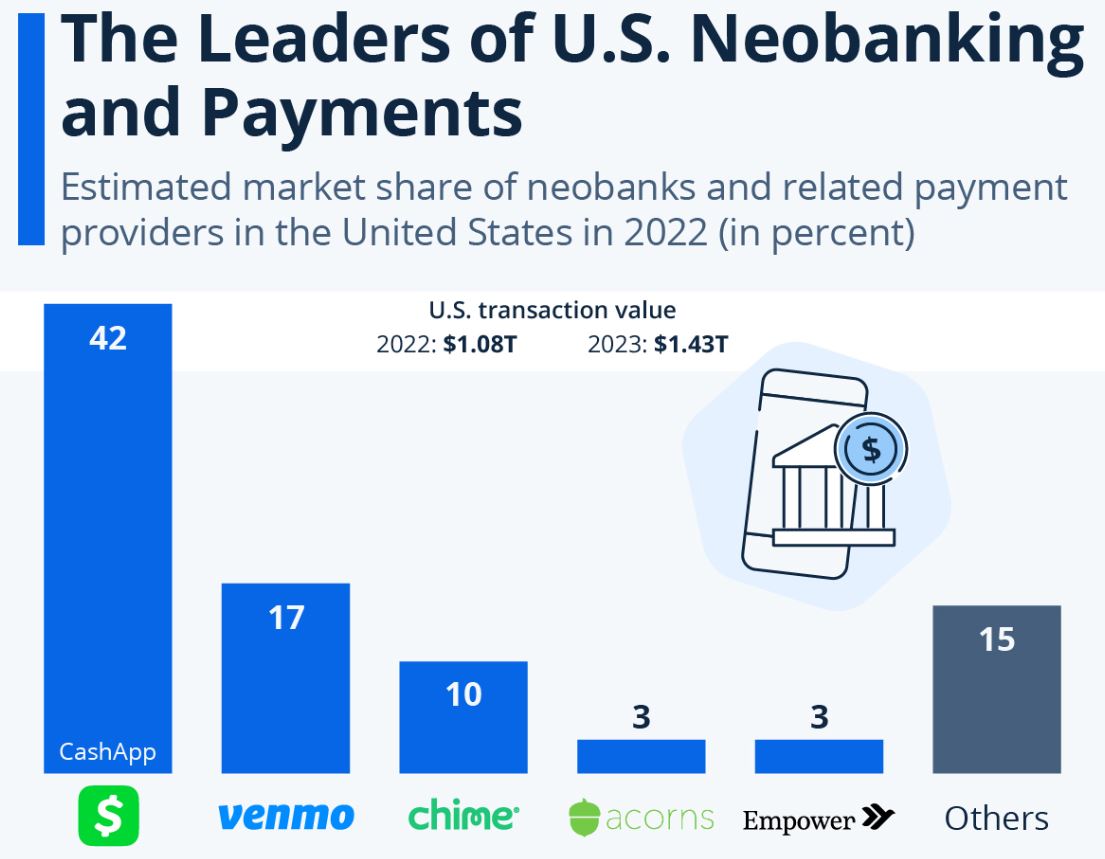

Leader of US Neobanking And Payments

(Source: statista.com)

- Neobanks are developing fast globally, but payment providers led digital banking in the U.S.

- According to Statista Market Insights, among the analysis of pure digital and independent services, CashApp commands about 45% of the market share, far outdistancing Venmo.

- While they mostly started as payment systems, CashApp and Venmo are keenly pushing other financial products to their customers, hence narrowing the gap between them and neobanks.

- Chime is the first true neobank on the market, but it is a distant third with a market share of 10%.

- Behind it are Acorns and Empower, each with only 3% of the market, as of 2022.

- The overall digital banking & payment space in the United States maintains rapid growth. With a transaction value of US$1.43 trillion, it grew over 30% from its 2022 value in 2023.

- This points to payment providers continuing to dominate America’s digital finance ecosystem, while traditional neobanks are still trying to build their presence.

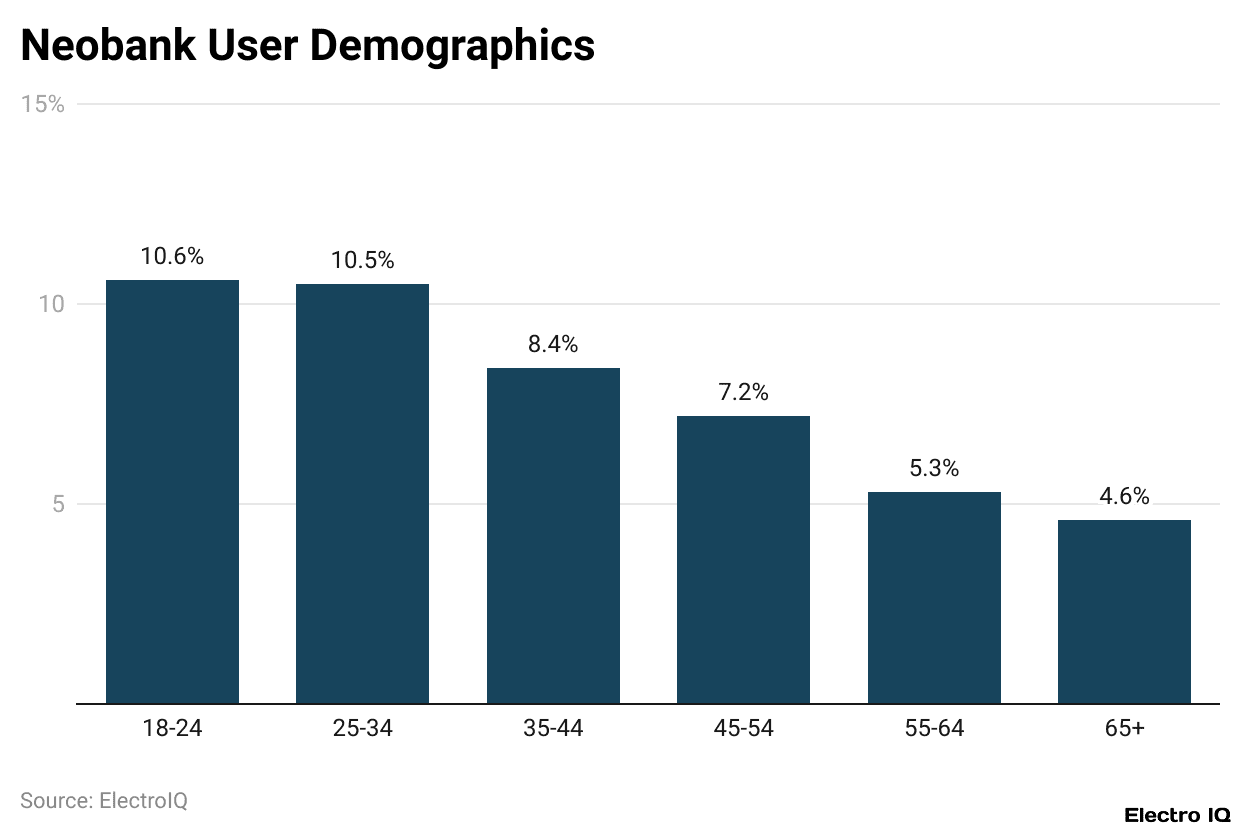

User Demographics

(Reference: unit21.ai)

- It is in the younger age groups that digital banks are most popular in the United States.

- Nearly 10.6% of people aged between 18 and 24 have an active account with digital banks, 10.5% of those in the 25-34 age group, grabbing a close second position.

- The above figures reveal that the younger generations of tech-savvy customers are the prime driving force in the growth of digital banking.

- About 9.6% of men in America utilise neobanks as opposed to only 5.5% of women.

- However, while this gap is slightly more visible in the U.S., the global trend indicates that men are slightly more inclined towards digital banks than their female counterparts.

- These figures shed light on how age and gender influence the trajectory in which digital banking is adopted.

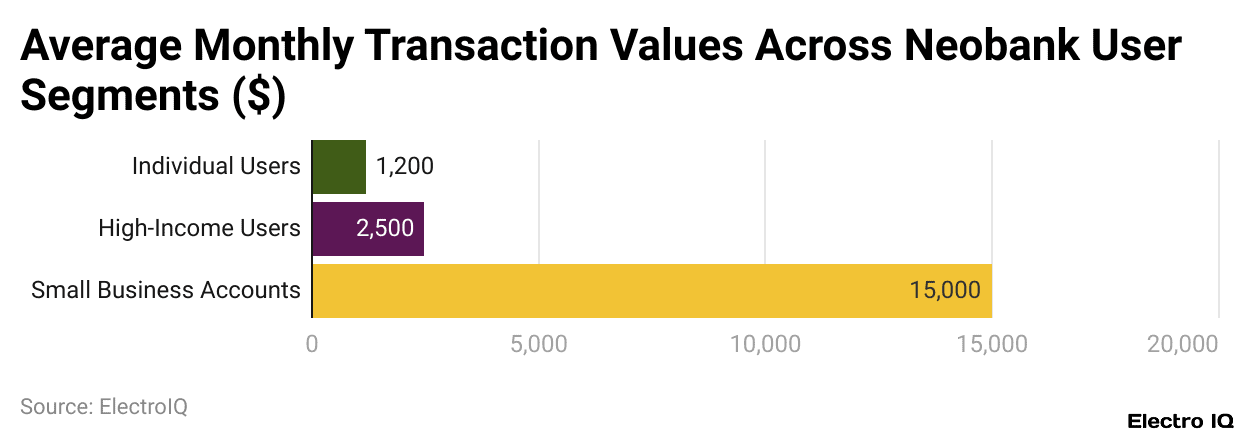

Average Transaction Value Per User

- Average monthly transaction value per neobanker increased to US$1,200 in 2023, up from US$950 in 2022.

- High net worth consumers were the biggest contributors to the transaction volume, forming almost 25% of the transaction value, with an average monthly transaction value of US$2,500.

- Likewise, neobanks saw an influx of interest from smaller corporates, as the latter’s business accounted for around US$15,000 each month on average, indicating an increasing class of SMEs turning to digital banks.

- Around 43% of surveyed users responded that they mainly use their neobank bill for e-commerce, with the average size of a transaction being almost US$180.

- Peer-to-peer transfers also increased, by 22%, to an average of US$300 per transaction in 2023.

- Especially Gen Z users showed fantastic growth, with their monthly transaction values rising 15% year-on-year to US$950.

- Moreover, international remittances through neobanks were up by 30%, averaging US$1,000 per transfer, emphasizing how these banks are fast turning into the preferred choice for cross-border payment.

Account Type Insights

- In 2023, there was a major focus on savings accounts by neobanks, with basic savings making up 65% of all accounts.

- Other lines have been growing at 40%, such as small business and freelancer accounts, supported by features such as invoicing and tax tools.

- Salary-linked accounts rose by 30%, especially in cities where digital salary payments are common. Premium-tier accounts maupfor 20% of the total accounts and offer perks such as cashback and travel rewards.

- Cryptocurrency-linked accounts surged by almost 50% on the back of digital asset trading and storage interest.

- Teen banking grew by 35%, although more parents are now opting for supervised accounts to grant their little ones more financial literacy.

- Joint accounts saw an 18% increase, showing that families are increasingly using digital platforms for shared money management.

App Download Insights

- Neobanking app downloads surged at a rate of 40% in 2023 and hit 1.2 billion worldwide.

- The users have described these apps as well-designed and fast, with 85% agreeing that they were “highly intuitive,” considering smooth navigation and quick check numbering amongst the few attributes.

- Biometric authentication became common as 90% of neobanks adopted either facial recognition or fingerprint scanning.

- These days, digital-money-app users see a rising need to track transactions in real time, with 75% of them doing it to track their spending.

- Some 30% of these neobanks have put in-app tools in place to educate customers financially, hoping to improve their customers’ financial literacy.

- Mobile-first design strategies increase the number of daily app users by 25%, and these apps see an average user spend time of 25 minutes per day.

- Third-party integration options such as PayPal and Stripe increased by 28%, offering users more convenience and flexibility.

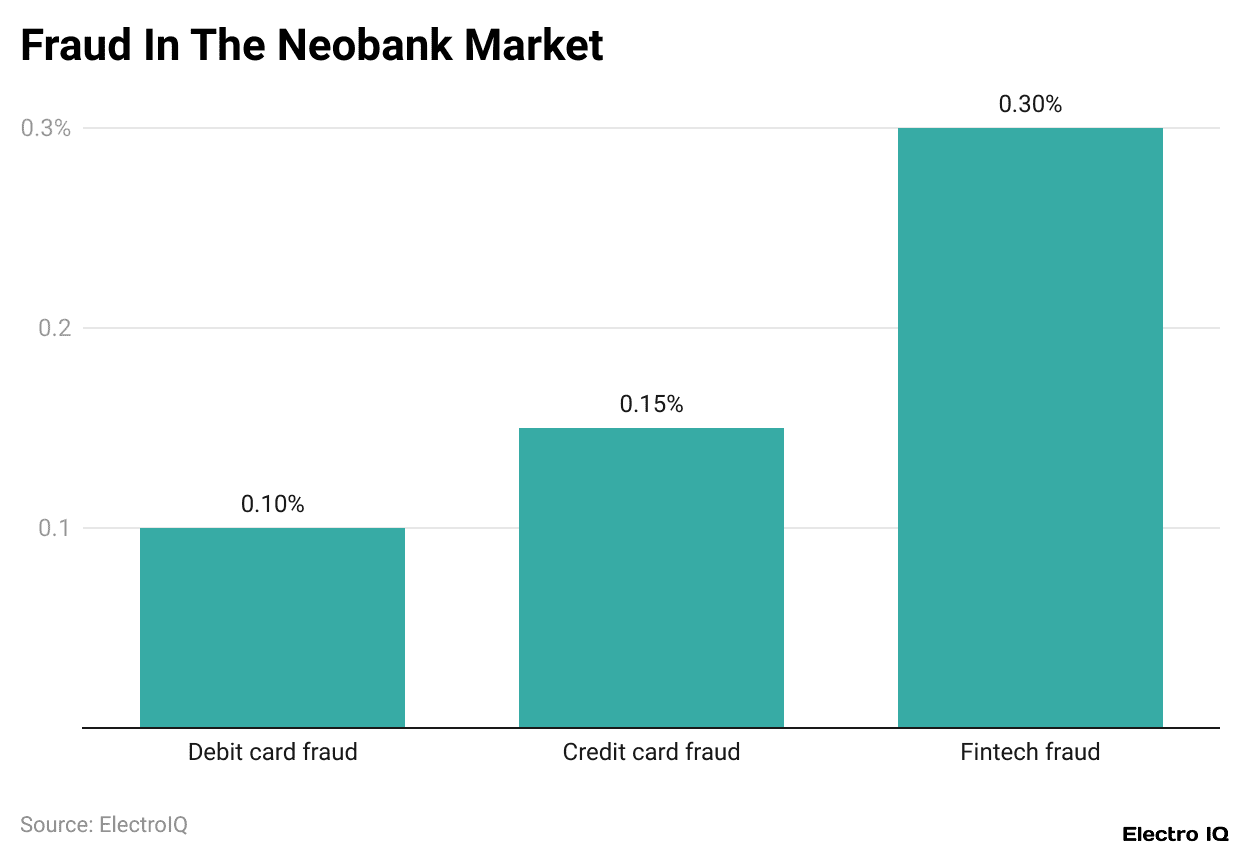

Fraud In Neobanking

(Reference: unit21.ai)

- Fintech companies suffer from a higher fraud rate than traditional banks.

- On average, at a 0.30% fraud rate, the incidence of fraud among fintechs stands almost twofold the rate of credit card fraud rate incidence, which is between 0.15% and 0.20%, and thrice as much as that of debit cards, at 0.10%, as claimed by AiteNovarica.

- The dawn of 2022 saw PayPal admitting that 4.5 million accounts on its platform were fraudulent, pointing to the deficiencies in its customer acquisition process.

- Before that, back in 2000, PayPal was losing to fraud across the world to the tune of US$6 million, which means every hour was stealing away US$1,900 from PayPal.

- While these percentages may appear very small, when multiplied by millions of users and large transaction volumes, the impact is massive.

- Fraud levels at challenger and neo banks tend to be higher relative to conventional banks, with different opportunities in the customer journey, from account opening to transactions.

- Much in the way PayPal struggled to keep pace with fraudsters in the early 2000s, neobanks today find themselves straining to achieve the same level.

- Fraudsters have now grown accustomed to the increased attention and cash poured into the sector; hence, the biggest negative is fraud prevention.

Neobanking Market Segmentation

- In 2023, the neobanking industry displayed well-established patterns concerning market segmentation, leading companies, and technologies shaping the industry.

- Retail banking held the largest share, generating a percentage of the overall revenue.

- Small and medium businesses made up about a quarter of neobank users, thanks to tools for loans and payroll that need to be simple.

- 10% of these users were cryptocurrency holders who relied on neobanks for their trading and storage needs, whereas 20% of the new account openings were for freelancers in the gig economy.

- Adoption was strongest in urban areas, accounting for 70% of users, but the rural areas flourished equally with an increase of 35% in 2023.

- Younger generations, primarily millennials and Gen Z, comprised the core customer group and accounted for 75% of global users.

- There was also an emergence of niche neobanks in the market, such as those serving eco-conscious customers or crypto traders, which grew by 20%.

Key Companies and Insights

- Focusing on leading companies, Nubank cemented its position at the very top around the world with a 32% share of Latin America.

- Revolut strengthened its hold across Europe, with revenues rising 5% and surpassing 30 million users.

- Chime led the first-wave digital banking market with an estimated 40% share in the U.S., while Monzo boasted a 45% increase in its user base, concentrating on budgeting tools in the U.K.

- Starling Bank, on the other hand, grew 22%, targeting SMEs..

- Fi managed to win a 15% share of the local markets in India by appealing to younger users, whereas N26 hit 9 million active accounts and expanded in the U.S. and Brazil.

Technological Innovations

- Artificial intelligence, for instance, became central to the technology scheme, with 70% of neobanks providing predictive financial insights on their apps.

- Blockchain adoption rose by 18%, bringing greater transaction security to crypto accounts. Voice-activated banking found itself rather popular, with 30% adoption among tech-savvy users.

- Half of the neobanks were using Open Banking APIs to integrate with third-party platforms for easy data sharing.

- Cloud migration gained pace with 65% of the neobanks running completely on cloud infrastructure, maximising their efficiency.

- Machine learning raised the accuracy of fraud detection by 40% and fostered user retention by 25% through association personalisation tools.

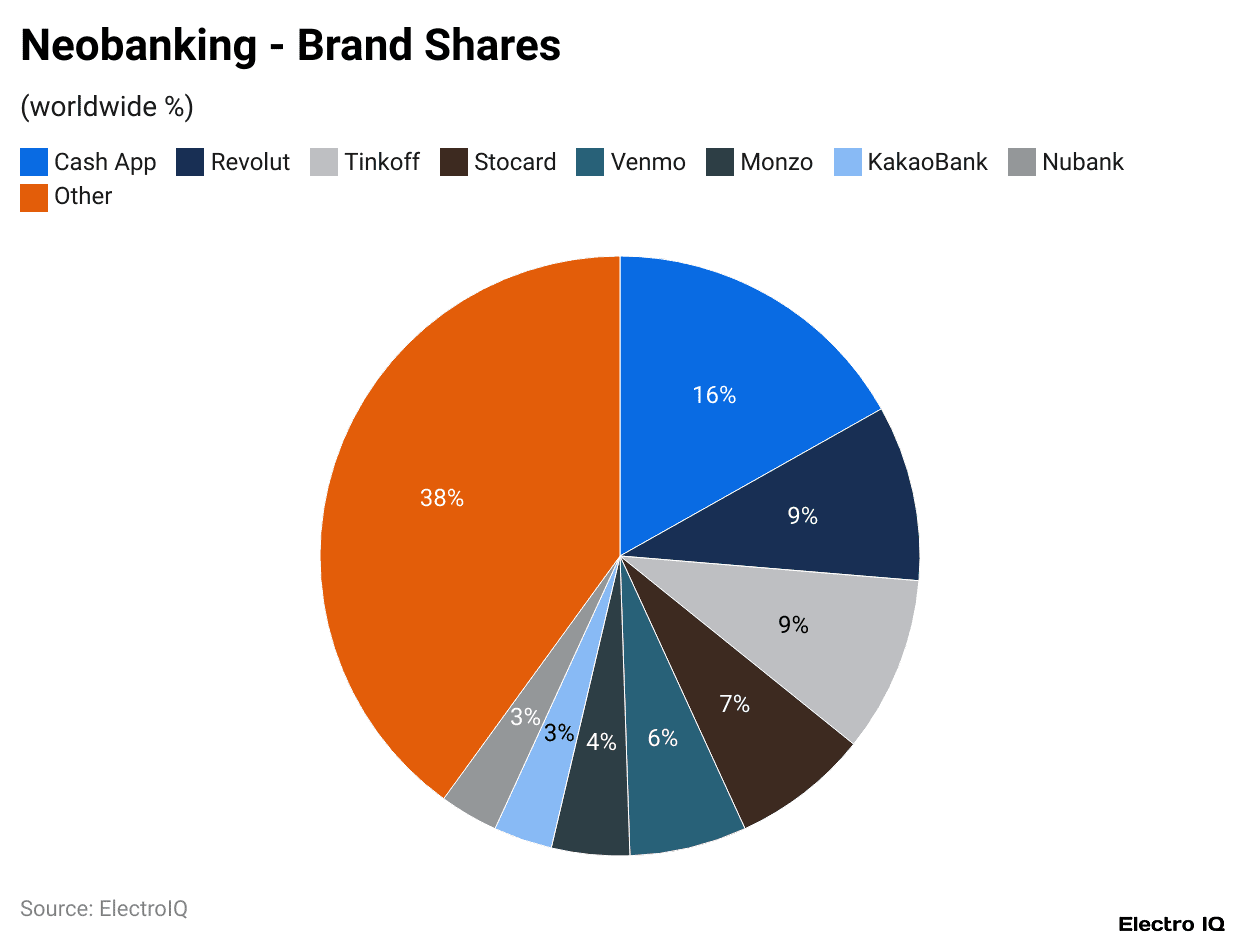

(Reference: stax.com)

- The chart shows how market share was distributed across the leading neobanking brands.

- Of individual brands, Cash App leads with a 16% market share, followed by Revolut and Tinkoff with 9% each. Stocard has 7% market share, while Venmo has 6%.

- Holding a 4% share, Monzo, according to the CIS, is followed by 3% shares each by Nubank and KakaoBank.

- This would show that well-known names still have substantial footprints, but the market is distributed; in fact, it is still the plethora of smaller entities that accounts for the largest share.

New Developments

- The global neobanking market is expected to enter a high growth phase, projected at US$3.3 trillion by 2032.

- A major chunk of this growth comes from neobanks more intensely targeting small and medium businesses, where they are filling niches left vacant by conventional banks with more customised financial solutions.

- Another visible trend is the convergence of fintech and banking, where many fintech companies are moving toward becoming full-fledged neobanks to offer a wider range of services and keep customers engaged for a longer time.

- In addition, a heavy reliance is being placed by neobanks on newer technologies, such as AI and blockchain, in making operations more efficient, security measures stronger, and providing better customer experience.

- Another big trend is geographical expansion, as neobanks typically move into emerging markets where a huge chunk of the population is left unbanked by conventional banking systems.

- The strategy not only allows them to grow their clientele but also promotes financial inclusion across the globe.

Conclusion

Neobank Statistics: Neobanks are setting the stage for modernisation in global banking by bringing forth digital-first, AI-enabled financial services that cater to tech-savvy individuals, small businesses, and marginalised consumer groups. Though dominated by a few players recording surges in user base, market size, and revenues, most neobanks have yet to make profits due to high acquisition costs and an inherent risk of fraud.

Innovations in AI, blockchain, and open banking APIs now provide a boost to their power bases. With user penetration expected to witness an upswing and more traditional banks coming in partnership with digital players, neobanks have a firm footing for expansion on a global level. Their focus on personalised experience, ease of use, and financial inclusion in the present gives them the strength to be a big future player in banking.

Sources

FAQ.

Neobanks are thriving because they give fast, mobile-first banking solutions with fewer fees and more accessibility than traditional banks. The younger generation, small businesses, and international users who need digital convenience are creating demand for adoption.

The neobank market is projected to rise to the value of US$3.3 trillion by 2032, at a CAGR of 54.09%. This makes it one of the fastest-growing financial sectors worldwide, hence indicating great investor and consumer faith.

Most neobanks are still not profitable. About 80% of them are operating at a loss, primarily due to the high costs of customer acquisition. Revenues, on the other hand, are growing rapidly; in 2023, a staggering figure of US$40 billion is expected to be generated globally, and is expected that around 15% of neobanks will be at a break-even point by 2025.

Europe stands on top in global respect, with about 80+ million users, while Nubank dominates Latin America. In the US, neobank Chime leads, but CashApp has the largest digital finance share. Revolut stays strong in Europe, while Monzo and Starling flourish in the UK.

Neobanks have the harder task of dealing with fraud, which occurs at a much higher rate than in traditional banking, alongside keeping operational and acquisition costs high. Profitability, growth, security enhancement, and regulatory compliance remain the principal hurdles for long-term viability.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.