Small Business Insurance Statistics By Market And Facts (2025)

Updated · Jul 23, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Small Business Insurance Market

- Small Business Health Insurance

- U.S. Small Businesses’ Most Important Problem

- Small Business Cyber Insurance Statistics

- Small Business Insurance Average Cost

- Commercial Insurance And Fire – Related Losses

- Small Business Insurance Claim

- Small Business Index

- Reasons Small Business Owners Want To Update Insurance Coverage

- Insurance Status of Small Business Owners

- Conclusion

Introduction

Small Business Insurance Statistics: Small businesses form the foundation of the global economy, with all kinds of perils they suffer property damage, liability claims, data breaches, and employee injuries, among others. Insurance stands as an essential tool to protect small businesses against these financial risks. For that reason, the demand for small business insurance is ever-growing in 2024, as owners come to terms with the legal and operational risks that surround these enterprises.

This article will show the latest small business insurance statistics, and analyse industry insights and cost data alongside some key trends influencing this crucial sector in 2025.

Editor’s Choice

- 56% of small employers provide health insurance coverage, whereas 89% of businesses with over 30 employees provide coverage, while only 39% of microbusinesses (1-9 employees) provide coverage.

- Cost of providing insurance is the leading barrier, as claimed by 65% of small employers, with 88% of those with more than 30 employees citing it, and 70% among those with 10-29 employees.

- 94% of small businesses say it’s hard to manage insurance costs, and 98% among those providing insurance currently fear its long-term affordability.

- 31% of SMBs say they have cyber insurance, contrasted with 57% that have had a breach.

- Cyber insurance premiums are forecasted to increase by 25–30% per year, with a peak in 2025.

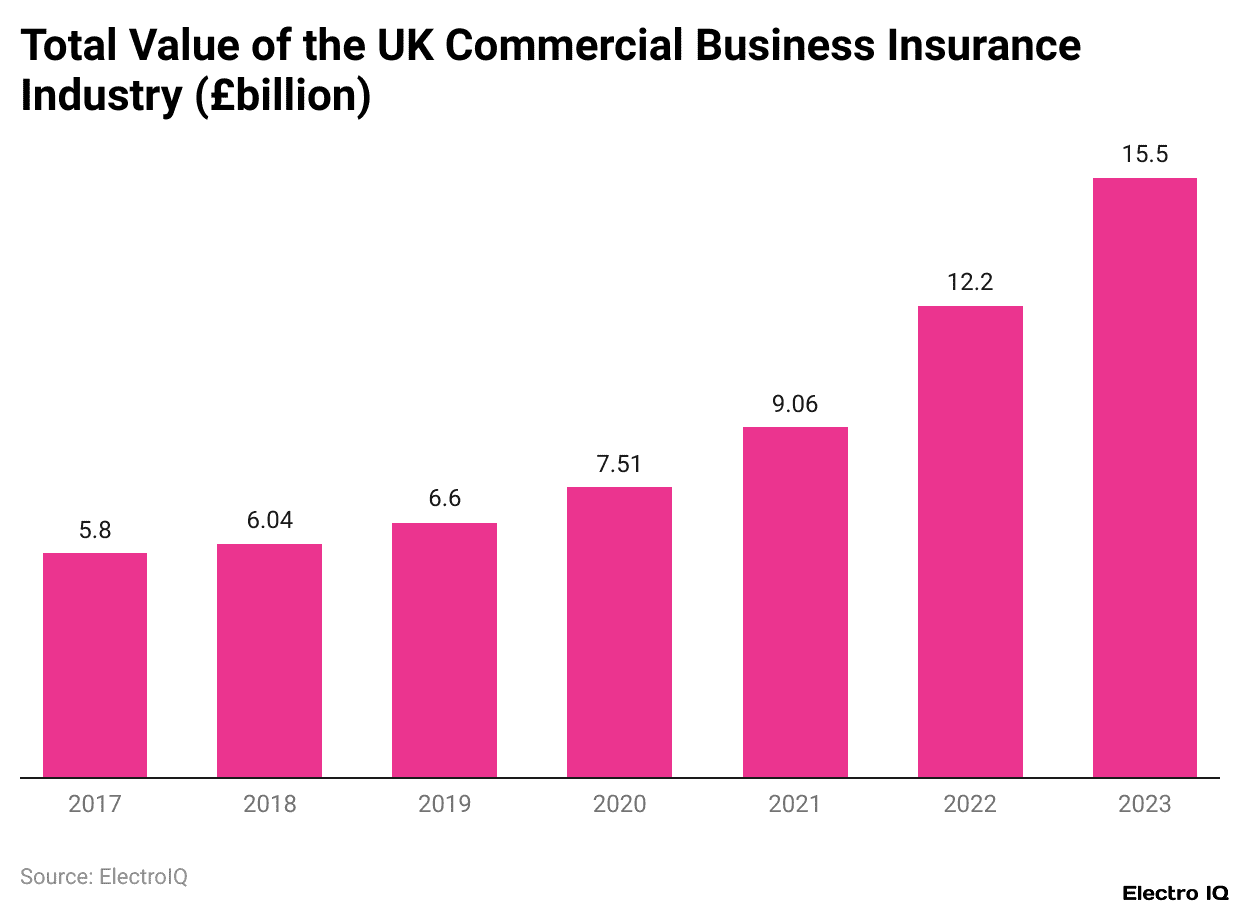

- Between 2020 and 2023, the UK business insurance market grew by 106%, having crossed £15.5 billion in valuation.

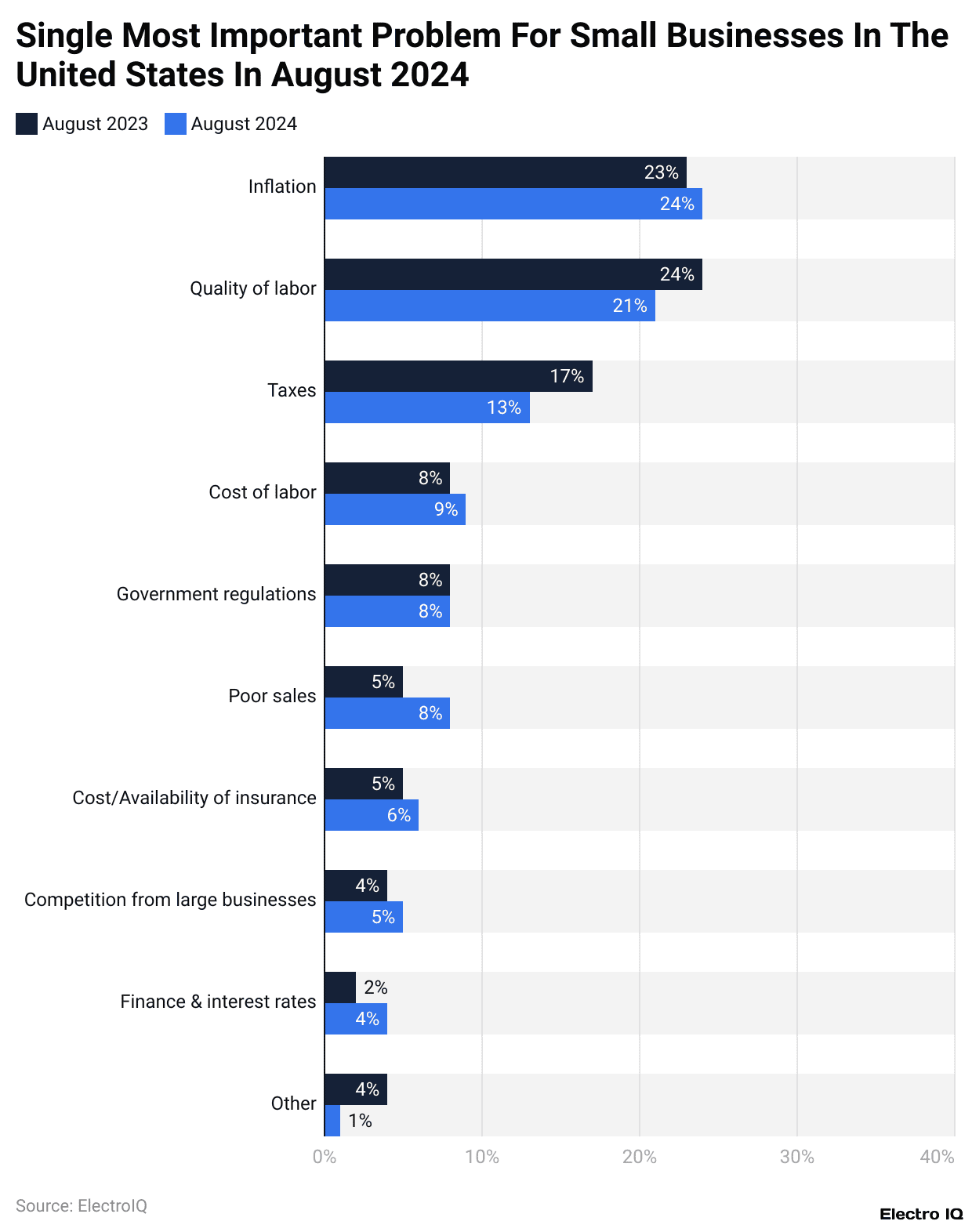

- Labor quality was one of the main concerns expressed by 21% of U.S. small business owners in 2024, while 24% were of the opinion that inflation was the top problem.

- Generally, small business insurance costs US$341 per month and US$4,090 per year, at US$30 per month for general liability and US$124 per month for cyber liability.

- Fire has historically been the most expensive kind of commercial claim, happening once every 64 seconds in the United States, while major large-loss incidents use millions in claim payments.

- In 2023, ransomware situations saw small businesses coughing up ransom worth US$16,000 on average; 50% of those who paid did not get their data restored, and 27% were subjected to attacks again.

- By Q2 2024, 61% of small businesses declared themselves to be in a healthy state, as opposed to 25% at the end of 2020.

- 36.9% of small business owners want to update their insurance to reflect their current needs, and 32.7% want to add coverage they hadn’t realised they needed.

Small Business Insurance Market

(Reference: money.co.uk)

- As per Money.co.uk, small business insurance statistics show that the UK business insurance market has seen significant growth in recent years. In 2023, it was valued at over £15.5 billion, marking a 71.8% increase since 2021, when the market was worth £9.1 billion.

- Looking further back, the market has more than doubled in size since 2020, rising from £7.51 billion to £15.5 billion, which represents a 106% growth over just three years.

- This upward trend began to accelerate around 2017, at which point the market was valued at under £6 billion.

- It experienced steady yearly increases of about 3% to 4%, followed by a more notable 9.4% rise between 2019 and 2020.

- Over the entire six-year period from 2017 to 2023, the UK business insurance industry expanded by approximately 167%, achieving an impressive average annual growth rate of 27.8%.

- These figures reflect a rapidly strengthening sector, driven by rising awareness of risk, increased demand for coverage, and inflationary pressures affecting premiums.

Small Business Health Insurance

- 2024 found a complex and costly issue in the realm of small business health insurance, which still remains.

- An estimated 56% of small employers presently provide health insurance coverage for their employees.

- However, there is a strong dependence on the size of the business in deciding whether or not to offer coverage.

- For example, 89% of companies with thirty or more employees offer health insurance, while only 39% of those with one to nine employees do. Cost continues to be the main barrier for those who don’t offer health insurance.

- 65% of small employers cite high expenses as the reason they don’t provide coverage.

- 88% of businesses with 30 or more employees, 70% of those with 10–29 employees, and 63% of microbusinesses (1–9 employees) all say cost is the primary reason for not offering health benefits.

- Looking ahead, nearly half of small employers that do not currently offer health insurance have no plans to provide it in the future.

- Nevertheless, this recognition remains: 63% of all employers believe that offering health coverage is vital for attracting and retaining employees.

- Here is a wider concern for costs: 94% of small employers say that insurance is a major financial burden.

- Among those who now provide coverage, 98% are worried that in the next five to 10 years, costs might become unsustainable.

- So the picture is clear: Small businesses understand the worth of health insurance, but affordability is a major barrier.

U.S. Small Businesses’ Most Important Problem

(Reference: statista.com)

- According to the survey conducted in the U.S. in August 2024, 21% of small business owners ranked labor quality among the most pressing issues they face. This again points to concerns regarding the ability to find skilled and reliable workers.

- The other principal concern has remained inflation, with 24% of respondents saying that was the biggest problem for their businesses.

- This shows a marginal uptick from August 2023, when 23% of small businesses felt inflation was the biggest concern.

- So, these data point to labor quality and rising costs as prime issues for small businesses nationwide.

Small Business Cyber Insurance Statistics

- According to a Forbes report, small business insurance statistics indicate that this era has brought and is bringing a greater threat to cyberspace, and only 31% of SMBs have taken cyber insurance to mitigate their threats.

- Yet, 57% of SMEs have gone through at least a cybersecurity breach, thus emphasising the lack of coverage.

- Between 2017 and 2021, the claims on average amounted to US$345,000 for cyber insurance claims paid out against SMEs, showing the magnitude of the cost attached to such insurances.

- From 2016 to 2020, almost 99% of the claims filed were against SMEs, indicating they are the major victims of cyber-attacks.

- With risks rising, it is expected that premiums for cyber insurance paid annually will begin to rise by 25-30% through 2025, which will in turn make cyber insurance even more expensive and yet more necessary for an entity to purchase.

Small Business Insurance Average Cost

| Type of Policy | Average Monthly Cost |

Average Annual Cost

|

| General Liability Insurance | $30 | $360 |

| Commercial Property Insurance | $63 | $756 |

| Inland Marine Insurance | $14 | $169 |

| Cyber Liability Insurance | $124 | $1,485 |

| Business Interruption Insurance | $40 | $480 |

| Workers Compensation | $70 | $840 |

| Total Average Cost of Small Business Insurance | $341 | $4,090 |

(Source: forbes.com)

- As per a Forbes survey, small business insurance statistics show that insurance for small businesses varies by the type of insurance needed. Indemnity insurance, for instance, averages US$30 monthly or US$360 annually, making it one of the cheapest.

- Commercial property insurance, however, is more expensive, as it offers coverage for buildings and physical properties, costing about US$63 per month or US$756 per year.

- Underwater marine insurance, which protects goods being transported or some special items, costs about US$14 a month, or US$169 a year.

- Unlike this, with the increasing cyber threats, cyber liability insurance is far more expensive, costing around US$124 a month or US$1,485 a year.

- Interruption insurance averages at US$40 a month or US$480 a year, which helps cover lost income during disruptions.

- Workers’ compensation, of course, bases its premium upon the payroll of a company, which means the weight of this insurance depends on its size and payroll, approximately costing US$70 a month, amounting to about US$840 a year.

- Together, these policies average a total of US$341 monthly, or US$4,090 yearly, depending, of course, on the size of the business, location, and industry.

Commercial Insurance And Fire – Related Losses

- Commercial insurance is integral to the protection of a business so that business interruptions may be indemnified for financial loss, even to the loss of property due to fire.

- In 2022, commercial insurance incurred losses estimated at US$202.7 million for the first time since 2018. While this is a sizeable amount, it is relatively minuscule when compared to the US$394.8 billion in net premiums written for commercial lines insurance for the very year.

- Fire damage remains among the costliest and most common claims under commercial property insurance.

- These policies enable businesses to repair or replace properties that have been damaged by such events.

- On average, commercial property insurance runs about US$63 per month or US$756 annually, making it a critical yet manageable investment for a considerable number of small businesses.

- Fire is still a major danger and very frequent. It takes the fourth position in business insurance claims.

- There is a structure fire every 64 seconds, according to data from the Insurance Information Institute.

- Fire losses, in 2021 alone, amounted to US$44.2 million, with the average loss per individual going up to US$133.26.

- In 2020, the top three costliest large-loss fires occurred in California, with eight of the ten most expensive large-loss fire events in American history recorded in the same state, and damages from these events are estimated to exceed US$32.25 million.

- Historically, nine of the top 10 deadliest fires in U.S. history occurred in the 1800s and 1900s.

- The only recent epidemiological one was the World Trade Centre terrorist attack, which saw the tragic loss of 2,976 lives.

- These statistics highlight the need for commercial property insurance and highlight its role in mitigating devastating economic consequences from hot and other perils.

Small Business Insurance Claim

- 56.4% of injuries and illnesses from 2021 to 2022 were from service, transportation, and production occupations.

- 79% of deaths at work originated from falls and transportation incidents.

- US$678 million in losses came out of five of the top-ten large-loss fires for 2021 alone; US$100 million of that loss from a single fire, the Marshall Fire.

- The number of fires has declined by 54% since 1980, but on a cost basis, inflation-adjusted property losses in 2023 were 3% higher than in 1980.

- 2023 saw 3,205 compromises in cyberattacks reported in the U.S.

- From the US$16.6 billion global cyber insurance premiums, the U.S. cyber insurance market wrote US$9.84 billion, or 59% of the world total, in 2023.

- There were a total of 30,000-plus cybercrime incidents in the world from November 2022 up to October 2023, with 900 cases reported by small businesses.

- The insurance claims for business email compromise amounted to US$2.9 billion in 2023.

- 59% of companies have cybersecurity awareness training.

- In 2023, ransomware payments were US$16,000 on average for small businesses.

- Of those who paid, 50% lost their data.

- 27% were attacked again.

- 27% were asked to pay more ransom.

- 41% of small businesses were hit with a cyberattack last year.

- 53% of small businesses now carry cyber insurance.

- Overall, cyberattacks are averagely cheaper, dropping from US$10,000 to US$8,300.

- In 2023, software supply chain attacks were twice as many as those in the past three years combined, costing the U.S. US$45.8 billion.

- Natural disasters caused underwriting losses of US$34 billion for insurers during the first half of 2023, with most losses coming from convective storms rather than hurricanes.

- Fatal workplace injuries decreased 8.4% to 5,283 in 2023 relative to 2022.

- In 2022, there were deaths every 99 minutes; in 2023, these changed to deaths happening every 96 minutes.

Small Business Index

(Reference: statista.com)

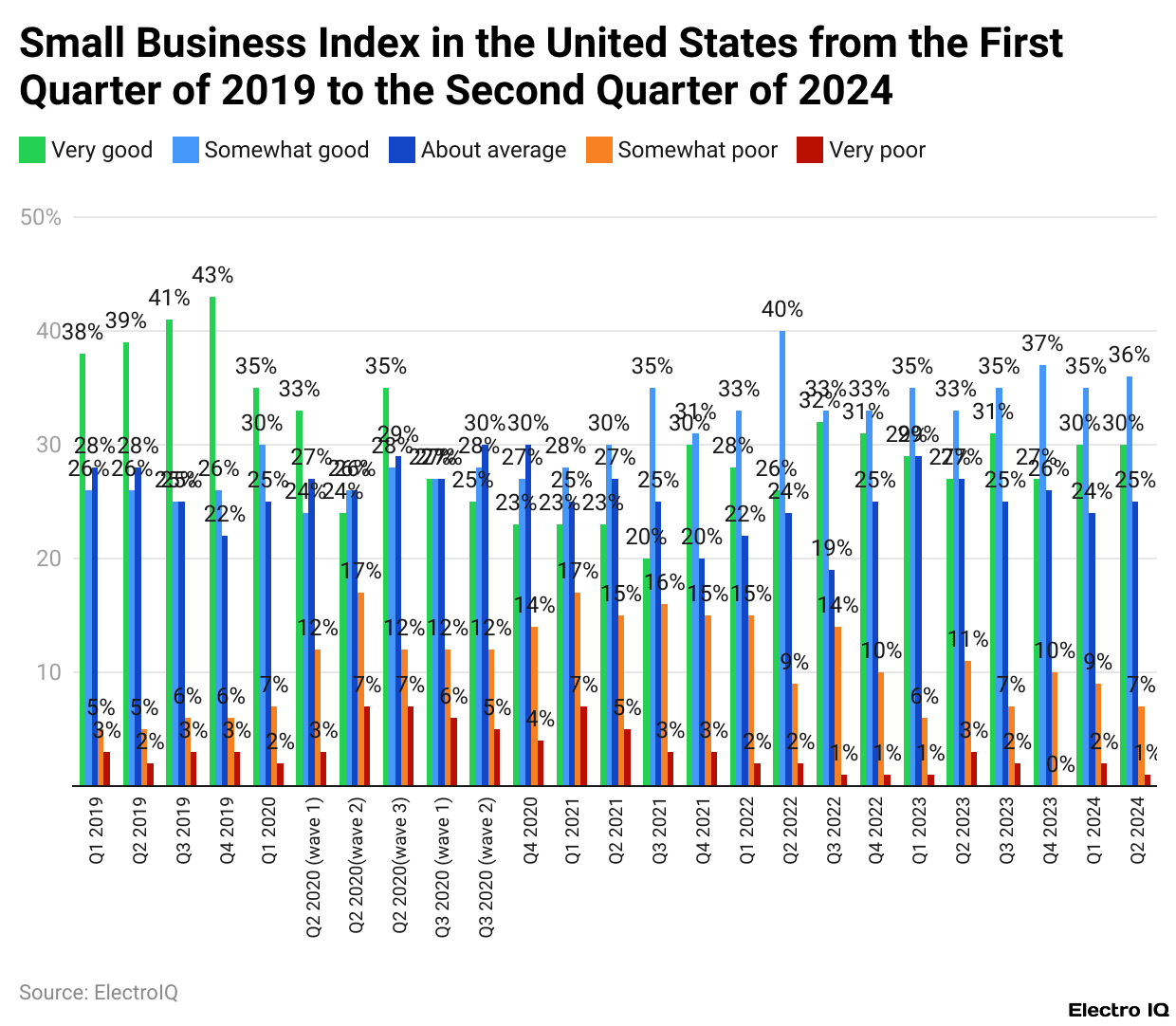

- Small business owners stating their business was in good health in the second quarter of 2024 totalled 61%.

- Another 24% said their business was in average condition.

- Looking from behind, at the end of 2019, the percentage of small businesses in “very good” health peaked at 43%.

- However, by the pandemic’s end in 2020, this number witnessed a sharp drop to 25%.

- Thus, this data showcases an improving trend of recovery, with conditions in 2024 showing improvement from 2020.

Reasons Small Business Owners Want To Update Insurance Coverage

- As per Businessdasher, small business insurance statistics state that what % of business owners in some kind of insurance mindset would like to take advantage of updated insurance coverage to better fit their present requirements–somewhere around 36.9%.

- And another 32.7% want to update their coverage so that they can add protection they never thought they might need before.

- Meanwhile, a quarter of the owners aim to update their policies to cover out “danger” scenarios where they find themselves uncovered.

- To save on insurance costs is the motivation for 18.4% of the respondents.

- Another small percentage, just a mere 0.8%, picked “Others” as their reason for wanting to make changes to their insurance coverage.

Insurance Status of Small Business Owners

- About 30% of small-business proprietors have private insurance coverage outside of any kind of employer or government program.

- An additional 25% are uninsured altogether.

- Some 21% get insurance as dependents, mostly through the employer of their spouse.

- About 19% are insured either by their own small business or business, while the remaining 6% are insured through some form of government program, such as Medicaid or Medicare.

- This distribution, therefore, highlights the diverse and often precarious forms of insurance coverage faced by small-business proprietors.

Conclusion

In 2024, insurance becomes a must-have for small businesses. Changes in risk come with digital evolution, climate change, and regulatory changes, so the right type of insurance becomes the assurance for a business to stay running, comply, and have a serene mind. With a rise in threats of cybercrime, natural disasters, and liability claims comes a higher consciousness among small businesses to protect themselves adequately.

The smarter, faster, and user-friendly character that small business insurance thus has is because of its increasing accessibility over online portals that also allow flexibility in plans.

FAQ.

Many small businesses see the cost of health insurance as the principal obstacle to providing it. In 2024, 65% of small employers said that cost was the number-one cause for not providing health coverage. The problem is more pronounced in the larger small businesses: 88% of businesses with 30 or more employees and 70% of businesses with 10 to 29 employees report that insurance is too costly.

Looking at averages, small business insurance costs between $341 monthly and $4,090 annually. These costs fluctuate with the nature, size, and location of the business. General liability insurance is among the cheapest at US$30/month, whereas cyber liability charges about US$124/month due to mounting digital threats.

Only about 31% of SMBs have cyber insurance at present, although 57% have been breached. This glaring gap should have several red flags to worry about, given its exorbitant cost-an average claim is around US$345,000, and premium rates are expected to rise 25% to 30% annually through 2025. Small businesses paid an average of US$16,000 ransom in 2023, yet 50% were not able to recover their data.

Burglary and theft top the list of most common small business insurance claims, followed by fire and water damage. Fire, meanwhile, remains the most expensive: Every 64 seconds, there is a structure fire in the U.S.; in 2021 alone, losses that occurred due to fire reached US$44.2 million.

In 2024, 36.9% of small business owners wanted to update the insurance policies to better fit present needs, and 32.7% aimed to include coverage they had never considered before. Another 25% wanted to make sure they were not uninsured in some occurrences, and 18.4% were mere cost-cutters.

Joseph D'Souza founded ElectroIQ in 2010 as a personal project to share his insights and experiences with tech gadgets. Over time, it has grown into a well-regarded tech blog, known for its in-depth technology trends, smartphone reviews and app-related statistics.