Edge Data Center Statistics By Market Size, Country, Revenue, Innovations And Facts (2025)

Updated · Sep 16, 2025

Table of Contents

- Introduction

- Editor’s Choice

- Global Edge Data Center Market Size

- Edge Data Centre Market Revenue

- Major Investors of The Edge Data Center And Digital Solution Sectors

- Edge Data Centre Market By Region

- Data Center Market Revenue By Country

- Global Edge Data Center Market Size By Component Statistics

- Recent Developments

- Innovations And Changes In Edge Data Center Statistics

- Conclusion

Introduction

Edge Data Center Statistics: Edge data centers started in 2024 as a niche idea and have grown into an important part of the web’s infrastructure. These facilities are provided in smaller, distributed locations nearer to users and devices to enable less latency in running applications like video streaming or online gaming, AR/VR, and industrial IoT.

This article will present Edge Data Center statistics for the year 2024: market value and growth rates, splits by region, power and trends, innovations, and investment patterns.

Editor’s Choice

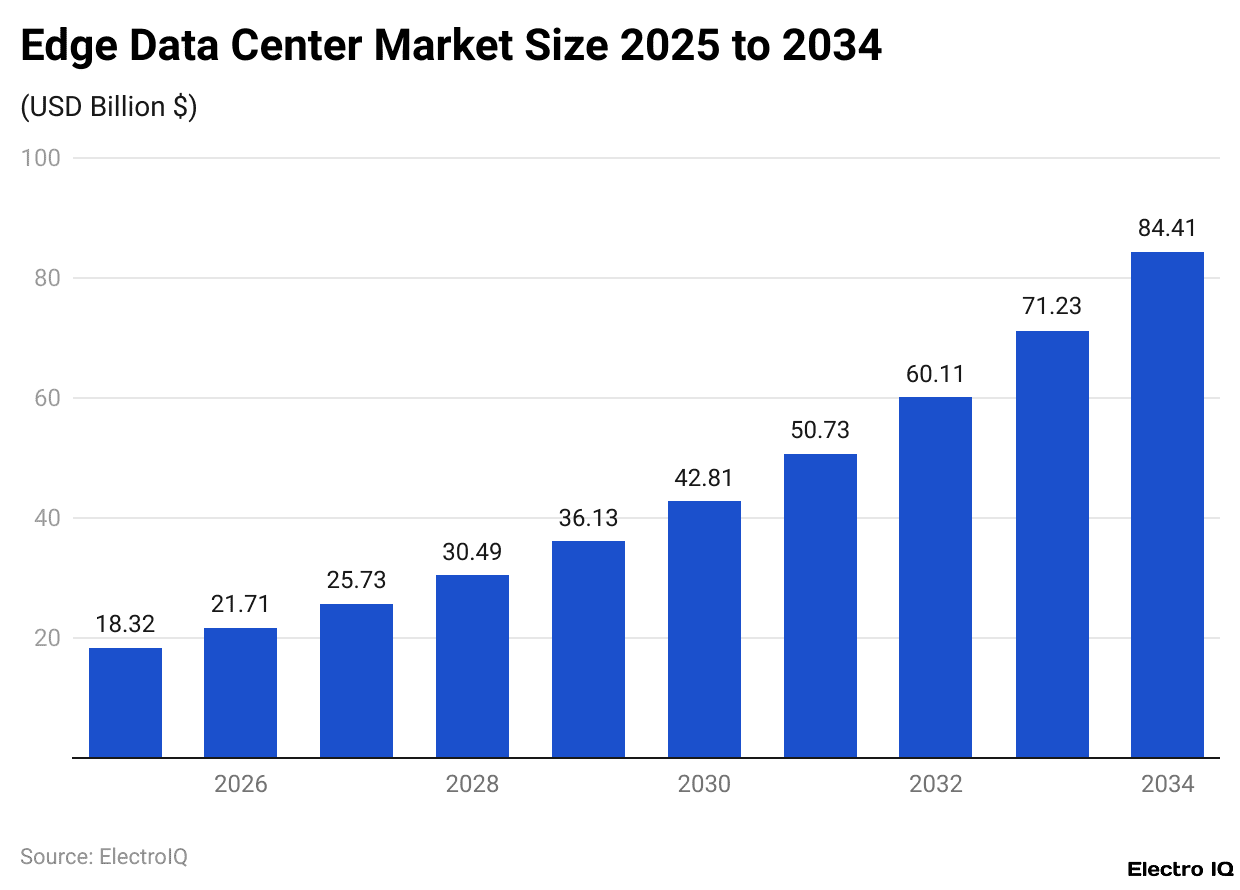

- In 2024, the world’s edge data center market was valued at US$15.46 billion and is expected to reach US$84.41 billion by 2034, growing at a CAGR of 18.5%.

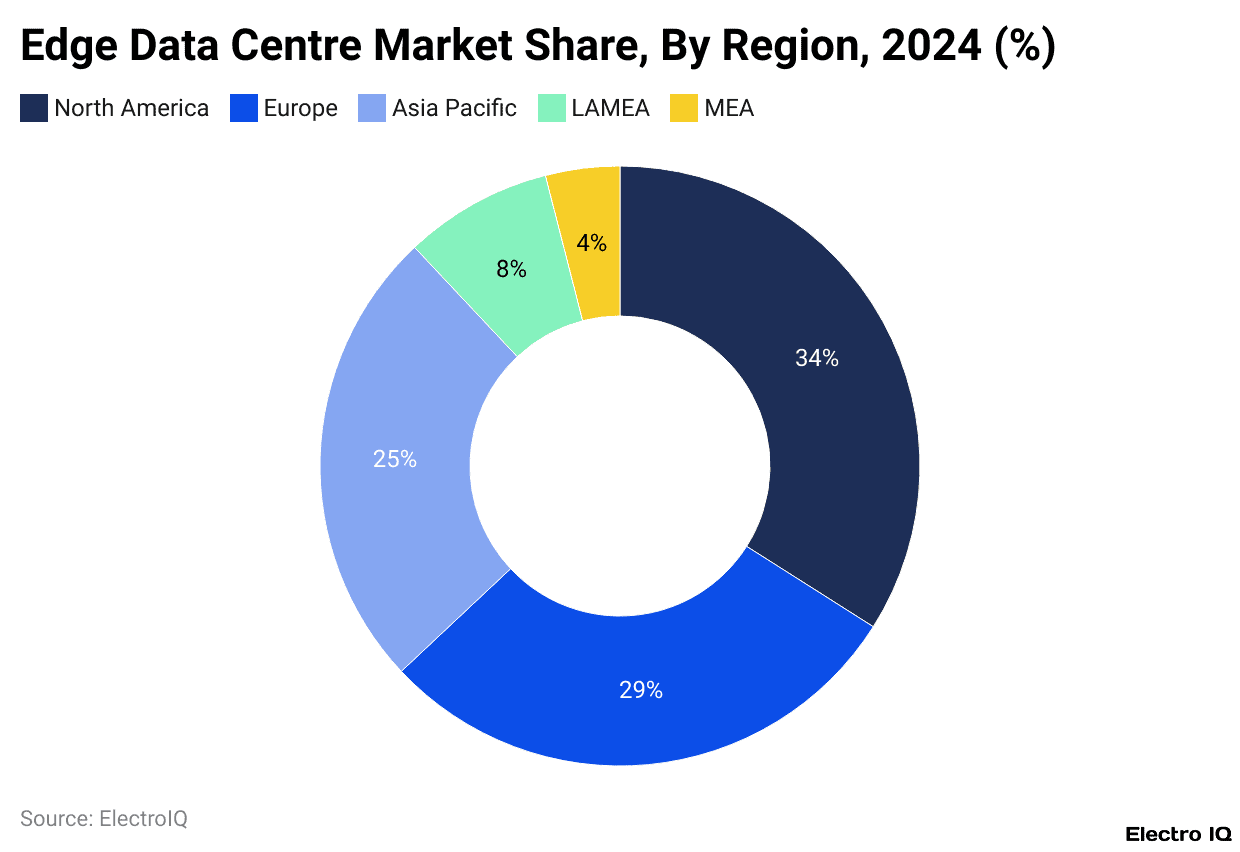

- North America accounts for the highest share at 34%, followed by Europe at 29%, Asia-Pacific at 25%, LAMEA at 8%, and MEA at 4%.

- In 2024, the United States generated the highest revenue in the data center industry at US$123.20 billion, followed by China at US$95.74 billion.

- By component, edge data center solutions and services are estimated to total US$60.2 billion by 2033, with solutions accounting for the bulk of growth.

- Major investors include Goldman Sachs (US$1.1B), Deutsche Bank (US$786M), Brookfield (US$775M), Natixis (US$773M), and Equinix (US$581M), suggesting a good financial backing for the sector.

- India plans to triple edge capacity to 200–210 MW by 2027, thereby increasing its share from 5% to 8% by 2028.

- In this period, a large-scale 190 MW contract was awarded between Calpine Corporation and CyrusOne in Texas, with expected operations to be facilitated in 2026.

Global Edge Data Center Market Size

(Reference: precedenceresearch.com)

- As per Precedence Research, Edge Data Center statistics show that in 2024, the global edge data center market was valued at around US$15.46 billion.

- It is expected to continue to experience considerable growth over the coming decade.

- By 2034, the market is projected to reach about US$84.41 billion, reflecting a growth at a compound annual growth rate (CAGR) of nearly 18.5% between the years 2025 and 2034.

- This strong growth goes to show how edge computing is gaining importance, with enterprises, telecom providers, and cloud companies pushing services closer to end users for lower latency and better performance.

- North America has been somewhat of an early adopter for edge services.

- Its edge data center market size was already around US$4.44 billion in 2023, showcasing the region’s strong adoption of delivery of next-generation digital services and infrastructure.

- This regional momentum, together with the global spread of the concept, further cements the expectation of front-run edge data centers as one of the fastest-growing sub-trains in the larger data-centre industry, with growth across the next decade.

Edge Data Centre Market Revenue

- From 2017 through 2029, the global data center industry saw a few fluctuations but was characterized by strong upward analysis of revenue.

- Data center revenues totalled around US$272.95 billion in 2017 and slowly rose to US$306.44 billion in 2018.

- A few years after coming with a slight set down at US$301.39 billion in 2019, the revenues dropped to US$298.30 billion in 2020.

- The market again bounced back to US$319.32 billion in 2021 before declining slightly to US$312.31 billion in 2022.

- Growth was heightened from 2023 onward. Revenues rose massively to US$372.79 billion in 2023 and held at US$416.10 billion in 2024.

- The growth momentum continued to US$452.48 billion in 2025 and to US$483.23 billion in 2026.

- US$572.01 billion in 2027, later levelling off a bit at US$575.29 billion in 2028 to rise once again to US$624.00 billion in 2029.

- In general, the trend signifies that the data center market is resilient and growing, supported by the escalating global need for data processing, cloud, and storage capacity.

Major Investors of The Edge Data Center And Digital Solution Sectors

- The major financial and technology institutions have made significant investments to strengthen the data center and digital solutions industry.

- Goldman Sachs takes the lead with investments totalling approximately US$1.1 billion across five companies, illustrating their fervent commitment to innovation in this space.

- Deutsche Bank follows next with an amount of US$786 million distributed amongst four companies, highlighting its strategic emphasis on data management.

- The Brookfield Corporation, on the other hand, has taken the more exclusive route by infusing US$775 million into only two companies, expressing a certain degree of confidence in its choices.

- Natixis, in turn, has invested US$773 million dispersed across three companies, suggesting that this sector is attractive to a broad spectrum of financial players.

- In relation to industry operators, Equinix has been very instrumental, with a US$581-million investment spread over three companies, considered to be direct interventions in shaping the data center landscape.

- Intel Capital took a broader approach by investing US$92 million in seven companies, essentially betting on an array of innovative opportunities.

- On the other hand, BPI France has shown support for growth companies by investing US$20 million in five companies.

- Startup-wise, Techstars has put in around US$480,000 into six companies, mostly focusing on the early-stage side of development.

- Instead, Telefonica put US$125,000 across four companies to give some support to the new entrants in the industry.

- Overall, this investment implies a blend of large-scale financial commitments and smaller, targeted ones, all feeding into the growing confidence in data centers and the digital infrastructure.

Edge Data Centre Market By Region

(Reference: precedenceresearch.com)

- The regional breakdown shows that North America leads the edge data center market with roughly 34% of the market share.

- This share stands as a testament to the region’s huge infrastructure base, relatively early adoption of digital services, and aggressive investments made by cloud providers and telecom operators.

- With 29%, Europe takes its place next, under strong data regulations, local data processing demands, and growing adoption across enterprises.

- The Asia-Pacific is a 25% holding, registering rapid expansions with 5G rollouts, urbanisation, and increasing applications of IoT and mobile services.

- LAMEA (Latin America, the Middle East, and Africa together) keeps the rest at 8%, the Middle East and Africa themselves maintaining a slice of 4%, hinting at a smaller yet steadily growing influence along the global edge data center map.

- Overall, this also points to developed regions making up for most of the concentration of market activities, while emerging ones start pitching in more steadily.

Data Center Market Revenue By Country

- In 2024, the global data center industry speaks loudly about American dominance, which has US$123.20 billion, upholding its position at the forefront of digital infrastructure and cloud services.

- Next comes China with US$95.74 billion, giving credit to China for its quick-paced developments in the market.

- Other countries contribute heavily, with amounts reported as US$20.60 billion for Japan and US$18.70 billion for Germany.

- The United Kingdom followed suit with revenues from the data center sector amounting to US$17.18 billion, while France contributed US$11.75 billion, thus constituting key markets in Europe.

- Emerging players also have their wings spread out. India pulled in revenues of US$8.65 billion, while Canada witnessed a revenue flow of US$8.08 billion.

- Italy came up with US$7.04 billion, followed by South Korea with US$6.79 billion.

- Auditor-based markets appeared well traversed by Australia with US$5.40 billion, Brazil with US$5.32 billion, and the Netherlands with US$5.25 billion.

- Still, smaller players such as Russia with US$4.84 billion and Spain with US$4.48 billion amount to meaningful parts of the world market.

- This demonstration offers clues to the widespread nature and importance of the data center industry as both established economies and emerging markets play key roles in catering to the ever-increasing world demand for data processing and storage.

Global Edge Data Center Market Size By Component Statistics

- The global edge data center market splits into two major components: solutions and services, and both operate with accolades in growth year after year.

- Solutions stood at approximately US$8.72 billion in 2023, while services posted US$1.88 billion, bringing the total to US$10.6 billion.

- The solutions rose to US$10.45 billion in 2024, with services reaching US$2.25 billion, and an upward trend continued in 2025 when solutions were at US$12.18 billion and services at US$2.62 billion.

- Ups and downs continued in 2026, with solutions further climbing to US$15.23 billion and services at US$3.27 billion.

- In the year 2027, solutions shot up to US$18.52 billion while the services lingered at US$3.98 billion and maintained the momentum in 2028 when the services reached revenue of US$4.67 billion, with the rise in solutions hitting US$21.73 billion.

- After 2029, the growth sees a spur. Solutions create US$24.28 billion with services at US$5.22 billion in 2029.

- When solutions claim US$29.05 billion in 2030 with services at US$6.25 billion, in 2031, solutions reach US$33.99 billion while services stay at US$7.31 billion.

- Solutions will be US$40.57 billion in 2032, while services will be US$8.73 billion, and shortly after, in 2033.

- They will hit their peak at US$49.54 billion for solutions and US$10.66 billion for services. Then, the total market size is anticipated to be around US$60.2 billion.

- This steadily growing trend shows how hardware and software solutions are being joined by managed services and support to become increasingly essential.

- The expansion shows how worldwide, edge data centres are increasingly relied upon to meet the growing demand for data processing that is faster and localised.

Recent Developments

- In July of 2025, India formulated key plans for the edge data centre sector to take capacity from about 60–70 MW at the present time and nearly triple it to 200–210 MW in 2027.

- It is expected that edge capacity, which presently comprises about 5% of the total in the country, will eventually rise to 8% after the onset of new technologies by 2028.

- In April 2025, RailTel Corporation of India partnered with the National Buildings Construction Corporation (NBCC) to build data centres within India and abroad.

- The collaboration formalized by a Memorandum of Understanding will see projects roll out over the next five years.

- A month later, in June 2025, NES Data Pvt Ltd. announced the rollout of new advanced edge and containerised data centers in India.

- These facilities are modular, sustainable, and customizable according to remote environment considerations, AI, and real-time applications, with operationalisation happening the following month after the announcement.

- In May 2025, Duos Edge AI, Inc., a subsidiary of Duos Technologies Group, revealed yet another project with the Region 3 Education Service Centre in Victoria, Texas.

- The efforts aim at supporting edge data centers in rural markets and bolstering the broader education sector as various steps within the company’s nationwide expansion strategy.

- A Nutanix May 2023 announcement about the launch of Nutanix Central as a cloud-delivered platform providing unified visibility, control, and monitoring of edge, hybrid, and public cloud infrastructures.

- NTT Ltd. followed suit in June 2023, unveiling its Chennai 2 hyperscale data center campus at Ambattur, India.

- The campus, spread across six acres with two buildings, is rated for 34.8 MW of IT load, with 17.4 MW being brought to the market immediately.

- Alongside this, NTT had also announced the launch of the MIST undersea cable system in Chennai, further boosting the connectivity and digital infrastructure of India.

- The tandem of deployments emphasises the fast-tracking of capacity in mature markets like the U.S. and India, paying huge attention globally toward modular, sustainable, and region-specific data center strategies.

Innovations And Changes In Edge Data Center Statistics

- In 2023 and beyond, edge computing is becoming a critical component of IT infrastructure amidst changes that are transforming how enterprises operate across industries.

- The major reason is the real-time processing of data closer to where it is created. This minimises delays, enhances reliability, and strengthens security.

- Implementing AI and machine learning farthest from the cloud is among the biggest challenges.

- This enables edge computing processes to analyse data and make instant decisions without having to return all of the data to a central server.

- With faster connections and less latency, the rollout of 5G is on its way to being the best opportunity for edge computing for IoT devices and other real-time applications.

- Edge data centers, being close to where data is generated, support a huge amount of information coming from connected devices and digital tools.

- These centers equip businesses to get useful insights much faster and respond more effectively.

- Meanwhile, many edge centers are focusing on sustainability through the usage of renewable energy sources and state-of-the-art cooling techniques to further reduce their carbon footprint.

- Overall, the next-gen edge computing is emerging very fast, with thoughts of rapid processing and smart technologies standing out for future concepts.

- This trend has been assisting companies in fulfilling the ever-increasing demands of digital transformation in a super-connected world.

Conclusion

Edge Data Center Statistics: The edge data center industry is rapidly changing the skyline of digital infrastructure. It has bridged the gap between a very niche concept and an everyday necessity. It is estimated that the industry will witness growth from US$15.46 billion in 2024 to US$84.41 billion by 2034. This shows that it has the capacity to support low-latency applications, 5G adoption, AI, and IoT.

North America, Europe, and the Asia-Pacific indubitably lead the charge in expansion, whereas countries like India and the U.S. are making gigantic strides in capacity expansion. With strong investor confidence, coupled with continuous sustainability and modularity innovation, the edge data centers shall continue to serve as a great source to channel sustainability and digital transformation across industries worldwide.

FAQ.

The global edge data center market is expected to increase from USD 15.46 billion in 2024 to USD 84.41 billion by 2034, which accounts for a growth rate of 18.5% CAGR, thus showcasing strong demand for faster and localised data processing.

With 34% of the global market share, North America is first, followed by Europe with 29% and Asia-Pacific with 25%. LAMEA accounts for 8%, while the Middle East and Africa contribute 4%.

The main financiers are Goldman Sachs (with US$1.1 billion), Deutsche Bank (US$786 million), Brookfield (US$775 million), Natixis (US$773 million), and Equinix (US$581 million), proving the commitment the financial space and operators have toward the industry.

India plans to triple edge capacity from 60-70 MW in 2025 to 200-210 MW by 2027, raising its share from 5% to 8% of the national market by 2028.

Edge data centers are upgraded with AI, machine learning, and 5G networks for faster real-time processing, with sustainability developments focusing on renewable energy usage and advanced cooling techniques.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.