Bajaj Statistics By Revenue And Insights on Performance (2026)

Updated · May 29, 2026

Table of Contents

Introduction

Bajaj Statistics: Bajaj Auto stepped into the 2025–2026 financial cycle with what looked like one of the best runs it has seen, powered by premium motorcycles, an even bigger push for electric vehicle growth, and export momentum that stayed pretty aggressive. Even with global inflation hanging around, supply chain volatility, and the fact that India’s two-wheeler arena is getting more crowded by the day, the company still logged record-type numbers for revenue, profitability, and volumes. It kept strengthening its grip in both internal combustion engine (ICE) and electric mobility, using brand muscle like Pulsar, Chetak, KTM, and Triumph.

Exports going through Latin America, Africa, and Southeast Asia essentially turned into a core growth motor. At the same time, domestic premium motorcycle demand started looking healthier, helped by GST rationalisation. This whole diversified approach across motorcycles, three-wheelers, EVs, and global markets is what let Bajaj outpace several industry peers during FY2026, more or less.

Editor’s Choice

- Bajaj Finance’s quarterly revenue from operations went up 31.8% YoY to ₹16,005.65 crore in Q4 FY26.

- Bajaj Finance’s quarterly PAT jumped 34% YoY to ₹2,746.13 crore in March 2026

- Annual Bajaj Finance revenue moved higher to ₹58,732.48 crore from ₹50,010.31 crore in FY25

- Annual Bajaj Finance PAT arrived at ₹9,824.66 crore, up from ₹8,151.42 crore last year

- Bajaj Auto’s automotive segment revenue rose 40.8% YoY to ₹17,213.55 crore in Q4 FY26

- Annual automotive revenue climbed to ₹60,530.43 crore from ₹49,982.13 crore in FY25

- The financing business’s quarterly revenue leapt more than 127% to ₹1,007.84 crore

- Financing segment profit climbed sharply to ₹287.38 crore from ₹88.32 crore YoY

- Consolidated Q4 FY26 segment revenue grew 41.8% YoY to ₹18,493.86 crore

- Total Q4 FY26 profit before tax surged 74.5% YoY to ₹4,336.06 crore

- Domestic two-wheeler sales increased 24% YoY to 6,21,912 units in Q4 FY26

- Total export volumes rose 21% YoY to 22,50,183 units during FY26.

- Bajaj Auto’s total FY26 vehicle volumes crossed 51.17 lakh units, up 10% annually.

- Bajaj approved a ₹5,633 crore share buyback at ₹12,000 per share plus a ₹150 dividend payout.

- Chetak EV cumulative sales crossed 7,27,779 units, while Bajaj captured nearly 23% of India’s electric two-wheeler market by May 2026.

Bajaj’s Stable Growth Momentum

(Source: bajajauto.com)

- Bajaj Finance reported a fairly strong financial performance for the quarter that ended March 2026, and it looks like there was steady momentum in both revenue and profitability.

- Revenue from operations moved up to ₹16,005.65 crore, from ₹12,147.97 crore in March 2025, so that’s about 31.8% growth, which is kinda impressive.

- If we add other income, total revenue rose to ₹16,426.66 crore, suggesting a solid business expansion, plus a good level of operational resilience too.

- Profit before tax (PBT) improved from ₹2,703.40 crore to ₹3,662.66 crore, roughly a 35.5% increase, and that seems to point toward better cost control and also stronger lending margins.

- Profit after tax (PAT) jumped to ₹2,746.13 crore, compared with ₹2,049.31 crore earlier, so the year-on-year increase is around 34%. Based on company filings and the annual financial statements, the bigger picture over the year stays just as robust, not only the quarter.

- On the annual front, revenue from operations came in at ₹58,732.48 crore, against ₹50,010.31 crore last year. Meanwhile, annual PAT climbed to ₹9,824.66 crore from ₹8,151.42 cror.

- Company annual reports and stock exchange disclosures also show that the firm is trying to keep a balance between expansion and earnings strength, which in turn helps investor confidence.

- In simple terms, Bajaj appears to be placed well within India’s fast-moving, fast-growing financial services space, and that positioning matters quite a bit.

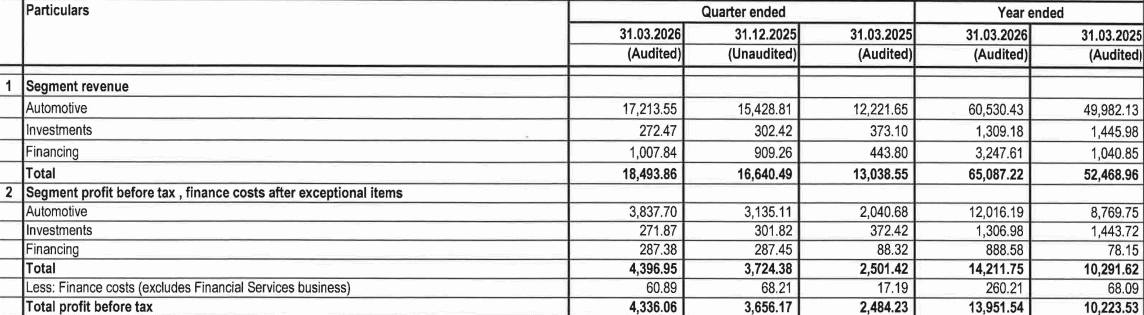

Bajaj’s Multi-Segment Growth

(Source: bajajauto.com)

- Bajaj Auto showed up with a pretty solid all-around financial outcome for the quarter and for the full year ended March 2026, and it kind of underlines how the firm manages to keep growth moving while also keeping profitability and day-to-day efficiency in check across several business lines.

- The automotive segment remained the largest engine of expansion. In the quarter, segment revenue climbed to ₹17,213.55 crore, up from ₹12,221.65 crore in March 2025, which works out to about 40.8% growth.

- In the company’s financial statements, full-year automotive revenue also moved higher to ₹60,530.43 crore versus ₹49,982.13 crore last year. That kind of shift suggests solid domestic demand, good export traction, and a better product blend in premium motorcycles plus electric vehicles, basically a nicer mix overall.

- Quarterly financing revenue went to ₹1,007.84 crore from ₹443.80 crore a year ago, and that’s more than 127% growth. Segment profit in financing rose sharply to ₹287.38 crore from ₹88.32 crore, pointing to stronger lending activity and also improving asset quality.

- Things seen in stock exchange updates and related disclosures indicate that higher consumer finance uptake has played a major role in Bajaj’s earnings expansion, even when conditions feel bumpy.

- On a consolidated basis, total segment revenue increased to ₹18,493.86 crore from ₹13,038.55 crore, roughly 41.8% year-on-year growth.

- Total profit before tax jumped to ₹4,336.06 crore compared to ₹2,484.23 crore, which is close to a 74.5% rise.

- For the annual view, profit before tax grew strongly as well, reaching ₹13,951.54 crore against ₹10,223.53 crore.

- Overall, Bajaj’s performance kinda mirrors a well-diversified set-up, where its auto strength, financial services growth, and cost discipline are moving along together in a pretty efficient way.

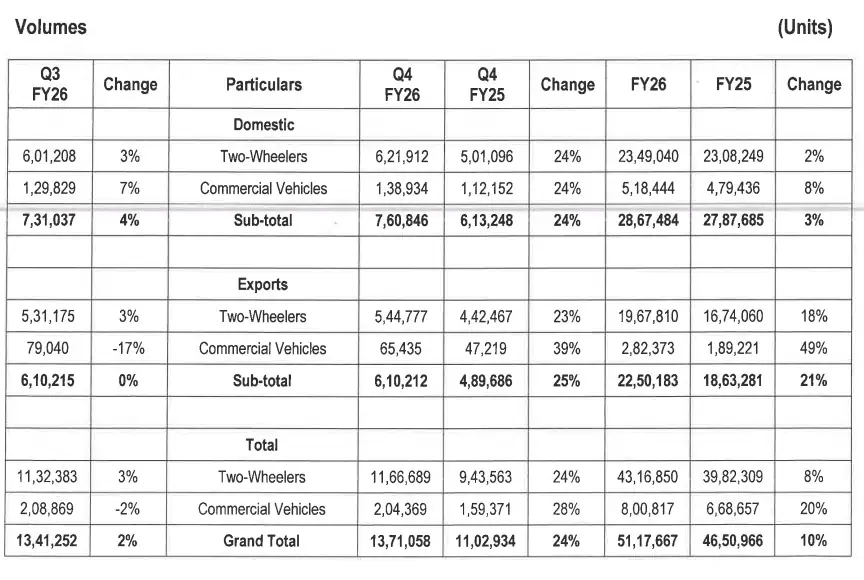

Bajaj Auto Deliveries

(Source: bajajauto.com)

- In FY26, Bajaj Auto delivered a solid, almost loud kind of run on vehicle volumes, with momentum visible in both home turf and outside markets.

- Based on the company’s sales figures and the investor presentations, domestic two-wheeler volumes in Q4 FY26 went up to 6,21,912 units from 5,01,096 units in Q4 FY25. That’s an impressive 24% year-on-year jump.

- Commercial vehicle sales were also up, by 24% to 1,38,934 units. So basically, total domestic volumes landed at 7,60,846 units for the quarter.

- On a full-year basis, annual domestic sales came in at 28,67,484 units, showing a steady 3% uptick compared to FY25.

- Export two-wheeler volumes rose 23% year-on-year in Q4 FY26 to 5,44,777 units, while export commercial vehicle volumes jumped 39% to 65,435 units.

- Inputs coming from annual reports and exchange filings suggest that the demand lift across Africa, Latin America, and several Asian markets helped this expansion.

- For FY26 overall, total export volumes grew sharply by 21% to 22,50,183 units, which signals a strong global stance for Bajaj.

- At the consolidated level, Bajaj reported total Q4 FY26 vehicle volumes of 13,71,058 units compared with 11,02,934 units in Q4 FY25, and it showed a robust growth of 24%.

- Meanwhile, full-year total volumes crossed 51.17 lakh units, up around 10% versus FY25 levels. Two-wheelers stayed the company’s backbone, contributing over 84% of annual total volumes, more or less.

- Overall, Bajaj’s volume performance is pointing to a healthy mix of domestic revival and export resilience.

- As per market analysts, along with company disclosures, this kind of balanced growth play strengthens Bajaj’s competitive edge and also helps it remain set for long-term expansion in the global mobility market.

- Bajaj Auto has delivered one of the strongest shareholder-return stories in India’s automotive sector for FY26, with a massive share buyback alongside a generous dividend, while at the same time investing heavily in electric vehicles and financial services. Sources: The Economic Times, Upstox, Bajaj Auto FY26 Results.

- Bajaj Auto’s board approved a ₹5,633 crore share buyback at ₹12,000 per share via the tender route, which lets the company repurchase almost 46.94 lakh shares, basically about 1.68% of total outstanding equity.

- The buyback price worked out to roughly a 14–16% premium over the stock’s pre-announcement trading levels, so long-term investors get rewarded more directly.

- On the same note, the company also announced a big ₹150 per share final dividend, which is equal to 1,500% of face value on a ₹10 stock.

- Together, the buyback and dividend come to around ₹9,825 crore, and effectively, it means distributing almost 100% of FY26 consolidated profit after tax back to shareholders. Sources: Economic Times Markets, Upstox Market Coverage.

- Importantly, Bajaj Auto is doing these payouts from a position of strength, not from a spot of weakness. FY26 was a record year, financially.

- Consolidated revenue climbed around 23% year-on-year to ₹62,900 crore, while profit after tax jumped roughly 47% to ₹10,744 crore.

- As per Autocar India and Vahan registration figures, the cumulative Chetak sales crossed 7,27,779 units from FY2021 through May 2026.

- FY26 alone is said to have added nearly 2,98,436 units, and that roughly matches about 25% annual growth, give or take.

- By mid-May 2026, Bajaj controlled around 23% of India’s electric two-wheeler market, so it sits as the second-largest EV player behind TVS Motor at about 25%.

- Bajaj’s 23% placing put it ahead of Ather Energy at around 17%, Hero Vida near 11%, and Ola Electric at roughly 8%.

- At the same time, Bajaj Auto is also shaping another kind of growth engine through Bajaj Auto Credit Ltd (BACL). This NBFC arm has been scaling with an almost aggressive speed since its all-India rollout started in 2024.

- Investor updates say BACL’s assets under management doubled year-on-year, reaching nearly ₹18,835 crore, and profit after tax has jumped more than 11 times to about ₹665 crore.

- Earlier disclosures, from Angel One, also pointed to Bajaj’s plan to pump in as much as ₹1,500 crore into this financing business during FY25–FY26, mainly to back expansion and regulatory capital requirements.

- Today, the company is rewarding investors pretty aggressively; at the same time, it is pushing money into tomorrow-type growth spaces— electric mobility, premium motorcycles via the KTM and Triumph tie-ups, and also vehicle financing.

- Together, all that kinda forms a strong story: a long-standing motorcycle giant is trying to become a broader mobility ecosystem, not by draining profitability, but while still protecting shareholder returns and all that.

Conclusion

Bajaj Auto started FY2026 with serious financial and operational momentum, backed up by premium motorcycles, export recovery, electric vehicle expansion, and financial services that keep widening. The firm managed record revenue, strong profitability, and higher vehicle volumes, and it did that while keeping margins healthy even with inflation and tough competition around. Their shareholder-return approach, with a big buyback plus dividend distribution, helped keep investor confidence solid.

Meanwhile, Bajaj also sped up long-term EV investment via Chetak, and deepened financing through Bajaj Auto Credit Ltd. With solid domestic traction, exports that are rising, and EV market share that’s climbing, Bajaj looks like one of India’s sturdier diversified mobility and automotive growth bets heading into 2026.

FAQ.

Bajaj Auto crossed 51.17 lakh in total vehicle volume in FY26, up about 10% year-on-year.

The company approved a ₹5,633 crore share buyback, at ₹12,000 per share.

Cumulative Chetak EV sales went past 7,27,779 units by May 2026.

Bajaj Finance posted 34% YoY growth in quarterly profit after tax, touching ₹2,746.13 crore.

Bajaj held nearly 23% of India’s electric two-wheeler market by mid-May 2026.

Pramod Pawar brings over a decade of SEO expertise to his role as the co-founder of 11Press and Prudour Market Research firm. A B.E. IT graduate from Shivaji University, Pramod has honed his skills in analyzing and writing about statistics pertinent to technology and science. His deep understanding of digital strategies enhances the impactful insights he provides through his work. Outside of his professional endeavors, Pramod enjoys playing cricket and delving into books across various genres, enriching his knowledge and staying inspired. His diverse experiences and interests fuel his innovative approach to statistical research and content creation.