MSME Statistics And Facts (2025), By Shares, Region, Financing Gap, Challenges, Development, Trends & Insights

Updated · Sep 30, 2025

Table of Contents

Introduction

MSME Statistics: Micro, small, and medium-sized enterprises are tiny pieces of the world’s engines. They combine a huge number of businesses and feed hundreds of millions of mouths, create jobs, and, oftentimes, are also the spark for innovation. The Micro, Small, and Medium Enterprises (MSMEs) are at the core of global economic growth, decent work, and social justice. They employ most of the labour force across the world and have a rich contribution to community development.

However, there are a number of constraints that stand in the way of realising their full potential. In this article, we will find the MSME statistics and their status around the globe.

Editor’s Choice

- MSMEs account for around 90% of businesses all across the globe today, provide more than 70% of the total employment, and contribute roughly 50% of the global GDP.

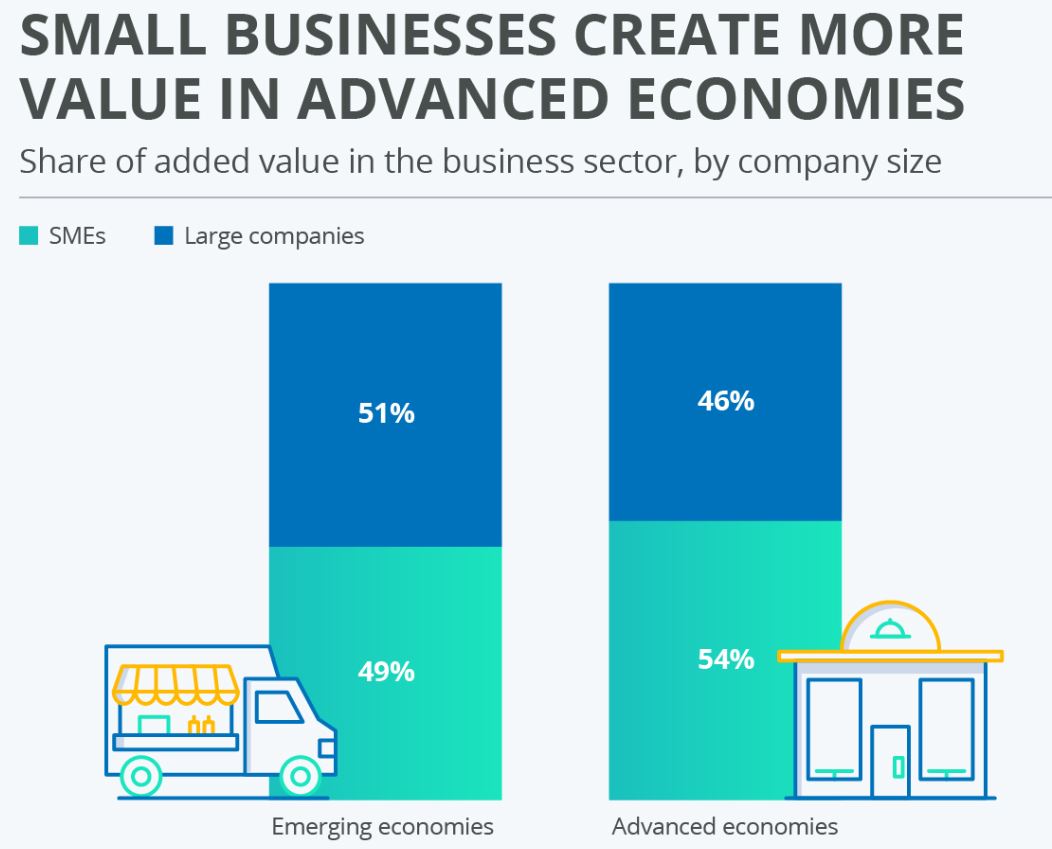

- In emerging economies, small businesses produce about 51% of the value in the business sector, and large firms produce about 46%; in advanced economies, SMEs produce 49%, and large firms produce 54%.

- In developing countries, 65 million MSMEs face an annual financing gap of US$5.2 trillion, with East Asia and the Pacific region alone accounting for 46% of the global gap.

- Since MSMEs employ around 70% of the global labor force, there lies a large percentage–estimated at 80%–operating in informal economies, and productivity, in their case, stands at less than one-third compared to that in large firms.

- There are between 57 and 64.4 million registered MSMEs in India, employing between 241-267.7 million, followed by a contribution of about 30% to the GDP and more than 45% to exports.

- Support from the government in India included public procurement amounting to US$4.5 billion from micro and small enterprises during FY 2024–25.

- In the United States, small businesses amounting to 34.8 million make up 99.9% of all U.S. businesses, employing 59 million people and contributing 43.5% to the GDP.

- 82% of small businesses in the U.S. are sole proprietorships, while family-owned businesses account for 27.3% of them.

- AI adoption among U.S. small businesses remains high, wherein 99% of small businesses use at least one type of AI platform, and active usage of AI is recorded by about 40%, nearly twice as much as was measured a year ago.

- From Lebanon’s US$30 million iSME project to India’s US$500 million SIDBI credit line, Jordan’s US$70 million credit line, and the Moroccan credit guarantee scheme supporting US$3.28 billion in loans.

- Leasing programs in Ethiopia and Guinea have disbursed US$147 million and US$25 million, respectively, to over 7,200 and 31 MSMEs.

- In Europe, SMEs constitute 99.8% of enterprises, employ 65.1% of the labor force, and produce 53.6% of value added.

- Total employment within SME increased 1.1% in 2024, forecast to grow 1% in 2025; digital SMEs are now leading employment growth at 2.4% and value-added growth at 2.2% in 2024.

(Source: statista.com)

- Small enterprises greatly contribute to value creation worldwide.

- Roughly 51% of value created within the business sector goes to small businesses in emerging economies, while around 46% is created by big companies.

- In contrast, in advanced economies, SMEs contribute about 49% of value creation, while big corporations take the lead with 54%.

- Thus, that means almost half of all economic value is actually generated by SMEs in both settings.

- Since they form an employment platform for more than half of the world’s population, their role becomes a very crucial one.

- Going further, they serve to stimulate innovation and develop avenues for local communities while ensuring the resilience of the economy.

- Be it in developed or developing regions, balanced and sustained growth will boil down to how well SMEs perform.

The Global SME Financing Gap

- Small and medium-sized enterprises (SMEs) are confronted with a far greater challenge while obtaining bank loans compared to large companies.

- Many SMEs work from their own savings or with help from friends and family for starting or sustaining their businesses instead of acquiring formal credit.

- According to the International Finance Corporation (IFC), about 65 million firms or 40% of MSMEs in developing countries are supposed to meet a financing need estimated at a total of US$5.2 trillion every year.

- That financing shortfall is 1.4 times the current MSME lending across the globe, which gives you an idea of how big this problem is.

- The funding gap is not evenly shared among regions of the world. East Asia and the Pacific hold the lion’s share at 46% of the global total, with Latin America and the Caribbean following at 23% and then Europe and Central Asia at 15%.

- Some areas are hit much harder when the gap is compared with potential demand: in Latin America and the Caribbean and in the Middle East and North Africa, the gap is as much as 87%-88% of probable SME financing demand.

- For roughly 50% of formal SMEs, access to credit remains a critical issue, and this restriction stretches far when micro and informal enterprises are included in the mix.

- This persistent funding gap restricts the capacity of SMEs to grow, hire, and contribute more forcefully toward economic development.

The Global Role And Challenges of MSMEs

(Source: ilo.org)

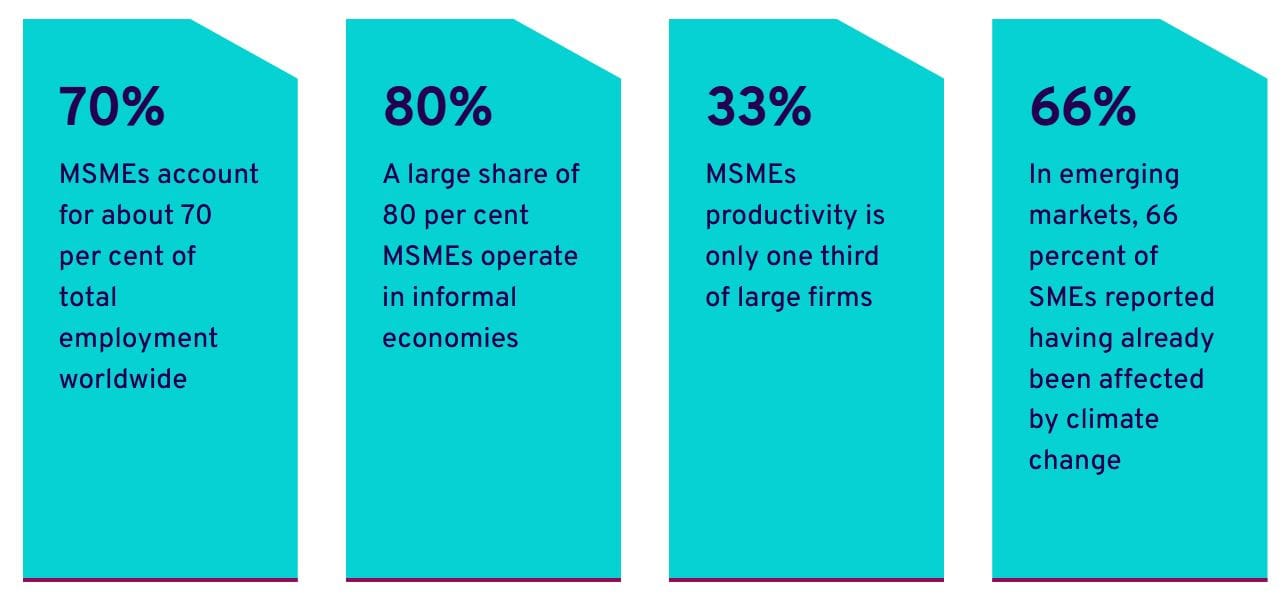

- Worldwide, MSMEs account for approximately 70% of total job creation, emphasising their importance in big job creation and sustaining livelihoods.

- However, a major 80% of MSMEs are in the informal economy, which renders them susceptible to unstable working conditions, lack of protection, limited access to finance, or social benefits.

- Productivity is among these, another concern; on average, MSME productivity is just one-third of that of large firms, blatantly underlining a very wide gulf in efficiency and competitiveness.

- Moreover, this also posits another layer of difficulty with the environmental challenges.

- In emerging markets, about 66%of SMEs are directly impacted by climate change, which poses a threat to their stability and long-term growth.

- Taking up the ILO work with governments, employers, and workers’ organisations to improve conditions for the MSMEs in striving for better market access, entrepreneurship promotion, productivity, decent work, as well as green and resilient growth models.

- The intent is to galvanise MSMEs toward economic and social development in a sustainable manner.

Global MSME Financing And Development Initiatives

The data provide insight into various international projects for the improvement of access to finance and support for the growth of MSMEs. Here is a breakdown of the statistics with explanations.

#1. Innovative Small And Medium Enterprises (iSME) Project – Lebanon

- The iSME project, conceptually supported with a US$30-million grant, is channelled towards supporting innovative young firms.

- Its equity co-investment fund has been able to disburse US$10.23 million in total, over 22 investments, which in turn has successfully leveraged an amount of US$25.47 million in private co-financing.

- Among the 174 grantees, 60 managed to raise US$13.1 million from other sources, almost giving the project a leverage ratio of 5.3 times.

- This is proof of the project’s success at attracting private capital and expanding opportunities for early-stage equity financing in Lebanon.

#2. MSME Growth, Innovation, And Inclusive Finance Project – India

- India’s initiative has given a whopping US$500 million credit line to SIDBI, along with US$3.7 million worth of technical assistance.

- This project has disbursed loans worth US$265 million to underserved MSMEs while bringing in digital innovations such as a contactless lending platform, which recently attracted US$1.9 billion in private financing.

- In addition, the Fund of Funds for Startups is placed for US$1.5 billion in disbursements by 2025, showing India’s commitment towards funding startup growth and innovation for the long term.

#3. Lines of Credit – Jordan

- The financing strategy of Jordan envisaged two main lines of credit. The first targeted an amount of US$70 million to fund MSMEs throughout the Kingdom.

- 58% of the MSMEs were located outside the Amman area, and 73% were owned by women.

- About 22% of the funds went to startups that assisted in the financing of 8,149 MSMEs and in the creation of 7,682 jobs: 79% for the youth and 423% for women.

- Following this was another tranche of US$50 million (where US$45.2 million was disbursed) to 3,345 MSMEs, 77% of whom were women and 48% were youth, while 65% of the beneficiaries were outside Amman.

- This concretely shows Jordan’s strong gender and youth inclusion agenda in MSME financing.

#4. Development Finance Project – Nigeria

- In Nigeria, the Development Bank of Nigeria (DBN) serves as a midpoint in elevating MSME access to finance.

- As of May 2019, the DBN had disbursed about US$243.7 million of credit through 7 banks and 10 microfinance banks to almost 50,000 end borrowers.

- A commendable 70% of the beneficiaries were female, clearly indicating a strong gender-inclusion focus in financial assistance.

#5. Partial Credit Guarantees – Morocco

- Under the MSME Development project, credit guarantees were placed to overcome the financing obstacles for MSMEs.

- Since 2011, there has been an 88% increase in the number of MSME loans and an 18% increase in the volume of loans.

- During the life of the project, loans of a total guaranteed amount of US$3.28 billion passed through the system, enabling the MSMEs to build their credit histories and to more easily obtain financing.

#6. Supporting Women-Owned SMEs – Ethiopia (WEDP)

- The Women Entrepreneurship Development Project in Ethiopia tackled the financing gap for women entrepreneurs directly.

- Loans reached more than 14,000 women entrepreneurs, while training covered over 20,000.

- Significantly, 66% of these women were first-time borrowers, indicating that the project was able to reach hitherto excluded groups.

- The program lifted the average loan size by 870% to US$11,500 while reducing collateral requirements from 200% to 125%.

- MFIs also contributed US$30.2 million of their own funds. On the positive side, women entrepreneurs experienced a 40% increase in annual profits, and employment increased by 56%.

#7. Supporting Women-Owned SMEs – Bangladesh

- The phenomenal US$2.8 billion gap impedes sufficiency in the credit requirements of women-owned SMEs; incarceration is typical of collateral obstructions.

- There are almost 10 million SMEs in Bangladesh that produce 23% of GDP, contribute to 80% of jobs in the industrial sector, and offer employment to about 25% of the population.

- The first-ever SME Policy in Bangladesh in 2019 attempted to develop a systemic plan for tackling financing challenges and improving the environment for women-owned enterprises.

#8. Leasing-Ethiopia And Guinea

- About leasing in Ethiopia, a US$200 million credit facility worked toward restructuring leasing by supporting 7 leasing institutions and introducing 4 new products (hire purchase, finance lease, microleasing, and agrileasing).

- By June 2019, a total of 7,186 MSMEs had been granted access to financing worth US$147 million.

- In Guinea, reforms, including the adoption of a national leasing act, assisted in the employment of 3 companies that commenced leasing operations, providing leases to the value of US$25 million to 31 medium enterprises.

- Thus, the two countries have reinforced alternative financing avenues for small-scale enterprises.

MSME Statistics By Region

Europe SME Employment

(Source: webgate.ec.europa.eu)

- In Europe, most companies remain small, with micro-enterprises representing the majority.

- There are approximately 24.5 million micro-enterprises, or 93.6% of all registered enterprises.

- Despite their numerical superiority, they employ only about 41.5 million persons, constituting a mere 30.1% of employment, and generate approximately €1,816.4 billion, or 20.1% of the total value added.

- Small enterprises, comprising those with 10-49 employees, consist of 1.4 million establishments (5.4% of all establishments).

- They exist to employ 26.9 million people (or 19.5% of the labour force), while value added generated by small enterprises amounts to €1,504.4 billion, representing 16.6% of the total.

- Medium-sized enterprises are still few, with their number being around 214,000 (0.8% of the total), but have a total employment of 21.3 million people–15.5% of total employment–with €1,527.5 billion value added, or 16.9%.

- Together, SMEs (micro, small, and medium-sized enterprises) account for almost all businesses in Europe—99.8% of the total.

- SMEs employ about 89.8 million people, which is 65.1% of total employment, and create €4,848.3 billion, or 53.6% of total value added.

- On the contrary, there are only a handful of large companies: 44,358 in total, representing 0.2% of all firms.

- They do, however, employ 48 million workers, making up 34.9% of the total workforce, and produced value added equal to €4,204.4 billion, or 46.4% of the total.

- The outcomes for SMEs in the EU in 2024 were mixed as far as different indicators are concerned.

- Employment grew by 1.1%, after a 1.7% increase in 2023, signifying that SMEs did continue to generate jobs.

- Yet, on the other hand, inflation-adjusted value added declined slightly by -0.2%, after a mild increase of +0.8% in 2023.

- Micro-enterprises showed the best performance among the groups by enjoying a 1.6% employment growth and 1.9% value-added growth, being thus the only group to experience real value-added growth, whereas other SME size classes suffered declines.

- In the long run, 2025 is foreseen to be a good year for SMEs. Employment growth is predicted to be approximately 1.0%, while inflation-adjusted value-added is anticipated to rebound at a rate of 1.6%.

- Except for Mining and quarrying, where employment is forecasted to decrease by -1.5%, most sectors (NACE sections) are expected to see growth in both employment and value added.

- The industry of Electricity, gas, steam, and air conditioning supply is projected for 3.4% growth in employment and value added.

- Beyond the ecosystems, the digital ranked first in 2024 with the highest SME employment growth of 2.4% and value added of 2.2%, being the only ecosystem to surpass the 2% threshold.

- Prospects for 2025 are still encouraging, with digital SMEs forecasted to grow by 2.1% and value added clocking 2.9%, thus maintaining their top position.

- SME employment has been on an upward trajectory since 2021, but at a decelerating rate: from 2.3% in 2022 to 0.9% in 2023 and 2024, with a further slowdown to 0.6% expected in 2025.

- Simultaneously, value added shrank by -0.5% in 2023 and deepened its slump to -1.5% in 2024, but is expected to bounce back in 2025 with a growth rate of 1.2%.

India MSME Status

- It can safely be said that India harbors the world’s largest single-country MSME system, housing somewhere between 57 and 64.4 million registered MSMEs as of mid-2025.

- Employing an estimated population of 241 to 267.7 million people, these enterprises only go to show how important they are to job creation.

- They contribute enormously to the economy, accounting for almost 30% of India’s GDP as well as providing more than 45% of trade from the country, thus being the strongest driver of both internal growth and international affairs.

- The distorting policies act in their favour as well. During 2024–25, procurement from public agencies of markets under micro and small enterprises reached approximately ₹37,190.02 crore (about US$4.5 billion).

- With this, the government is making active efforts to create at least some stable demand for their produce through procurement policies for MSMEs, providing them with better opportunities to grow and compete.

U.S. MSME Statistics

(Source: sellerscommerce.com)

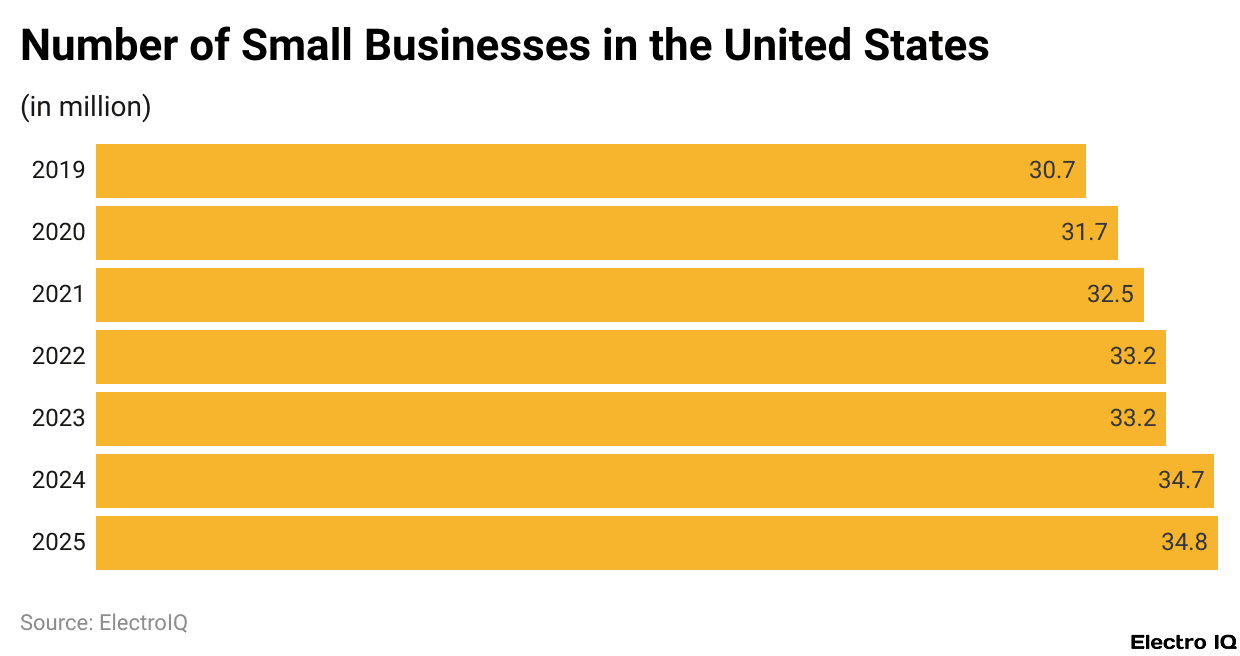

- As of 2025, the United States has nearly 34.8 million small businesses, accounting for 99.9% of all businesses in the country.

- They employ almost 59 million people, thus accounting for 45.9% of private-sector employment.

- As an interesting fact, 82% of small businesses do not operate with any employees; thus, the United States is full of solo ventures.

- The average small business employs around 11 people, while small businesses typically less than two years old have about six employees, and those over 20 years tend to employ about 58 people.

- It has been estimated that small businesses contribute almost 43.5% to the GDP of the country, thus playing a great role in the U.S. economy.

- However, these businesses confront several challenges, such as inflation, quality of labor, taxes, and government regulations.

- Also, 90% of businesses oppose lawsuits at some stage in their lifetime, wherein small businesses bear a hundredfold share of tort costs.

- Regarding ownership demographics, White people own 85% of small businesses, Asian Americans own 11%, Hispanic Americans own 7%, and Black or African American persons own 3%.

- Approximately 27.3% of small businesses are family-owned businesses with an average of 14 employees.

- Almost 99% of small businesses use some form of AI platform, with 40% really using AI, followed by a rise of almost 2 times from last year.

- Also, 91% of the businesses using AI believe it is going to remain a growth platform into the future, and 81% intend to increase their use of technology platforms.

- Starting a new business in the United States costs approximately US$40,000, but this figure varies based on industry and location.

Conclusion

Micro, small, and medium enterprises (MSMEs) keep the world economy going as they provide jobs, innovations, and economic value. There are approximately 90% businesses worldwide that have a workforce of more than 70% and contribute nearly 50% to the global GDP. Though all seem very important, MSMEs have faced several challenges, ranging from a lack of access to finance, low productivity, and vulnerabilities arising from economic and climate shocks.

Thus, using targeted interventions such as credit lines, equity funds, leasing programs, or government procurement has been shown to empower MSMEs, especially those operated by women and youth. Hence, strengthening MSMEs remains imperative on the path of inclusive, resilient, and equitable economic growth in the world.

FAQ.

In total global employment, MSMEs create at least 70% of opportunities, which are very important in livelihood creation and support.

About 65 million formal MSMEs in developing countries are confronted with an unmet financing need of US$5.2 trillion every year, thereby restricting them from growing and contributing to economic activity.

Countries such as India, Lebanon, Jordan, Morocco, Ethiopia, and Bangladesh have in place credit lines, equity funds, and leasing programs to empower MSMEs and women entrepreneurs.

In Europe, SMEs provide 53.6% of value added and employ 65.1% of the workforce; in the U.S., small businesses provide 45.9% of private-sector employment and 43.5% of GDP.

In the U.S., 99% of small businesses use at least one AI platform, with 40% actively leveraging AI for growth and operational efficiency.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.