Cloud Computing Statistics: Market Size, Adoption & ROI (2025)

Updated · Nov 04, 2025

Table of Contents

- Introduction

- Editor’s Choice

- General Facts

- Market Share of Cloud Infrastructure

- Cloud Computing Revenue Drives From Microsoft

- Cloud Computing Market Size

- Cloud Computing Value

- Global Cloud Computing Data By Region

- Cloud Storage And Usage

- Cloud Computing Cost

- Cloud Computing’s Role In Business

- Cloud Adoption Statistics

- Conclusion

Introduction

Cloud Computing Statistics: In 2024, the impact of cloud computing was felt more broadly within business and technology. Organisations increasingly relocated their data and workloads from on-premises systems to public, private, and hybrid clouds. Generative AI’s emergence, the development of new networks, and budget-aware FinOps elevated cloud expenses.

This article summarises 2024’s cloud computing statistics — covering market size, growth, provider shares, adoption, spending, and infrastructure scale.

Editor’s Choice

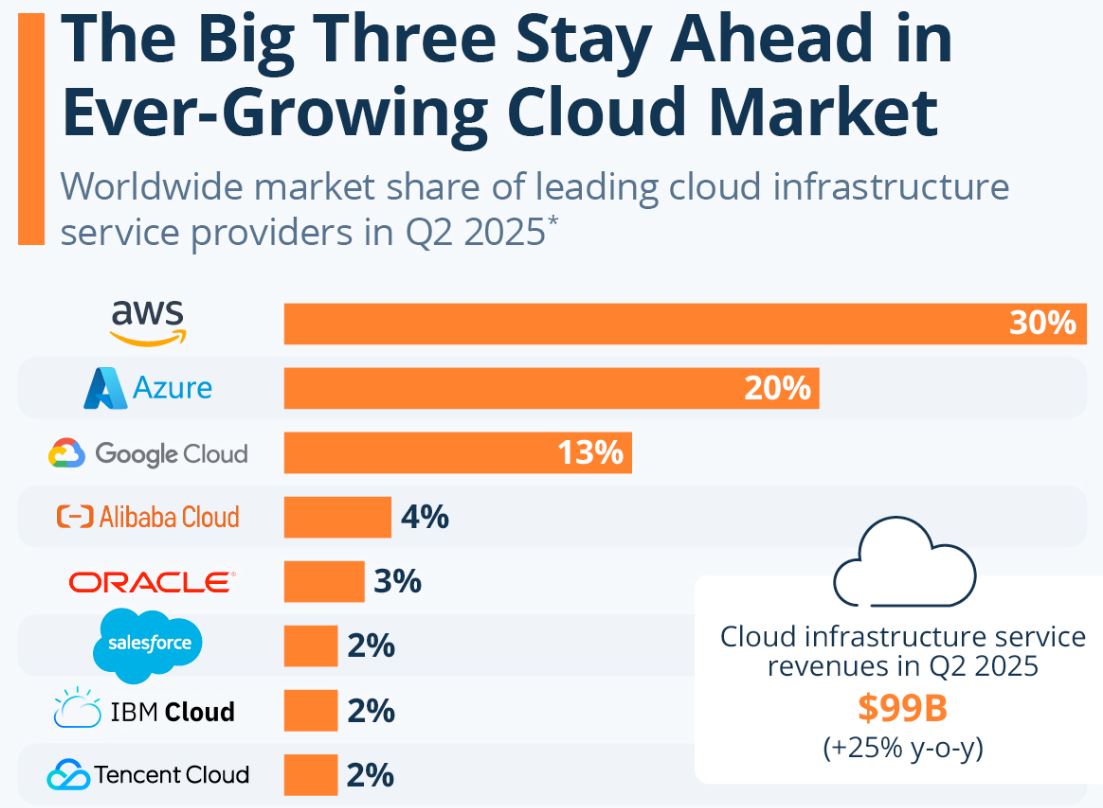

- AWS has about 30% of the global cloud infrastructure market, Azure 20%, and Google Cloud 13%, giving them over 60% in total.

- Cloud infrastructure spending reached US$99 billion in Q2 2025, which is 25% higher than the previous year, and it is expected to exceed US$400 billion yearly.

- The growth of AI-specific cloud services in Q2 2025 was 140–180%, which in turn boosted the growth of the overall market.

- In late 2023, Microsoft’s cloud revenue made up 55% of its total revenue, which was 41% in 2021.

- The global cloud market was worth US$500 billion in 2023 and is estimated to be US$1.6 trillion by 2030.

- The major advantage cloud offers is faster innovation and product delivery, which 24% of Fortune 1000 tech leaders agree to.

- Currently, 94% of companies use cloud technology, but only 44% of them are small businesses.

- In 2025, we are looking at a global cloud expenditure of US$1.3 trillion, where the average ROI is US$3.86 for every US$1 invested.

- An estimated 98% of companies use some type of cloud technology, out of which 89% use multi-cloud strategies.

- It was estimated that in 2024, companies would allocate 80% of their IT budgets to the cloud.

General Facts

- Today, in addition to storing data, companies are able to manage and process it through cloud computing, which uses remote servers via the internet.

- In 2023, it generated over US$500 billion in revenue and is still expanding.

- Cloud computing offers a number of advantages, including lower costs, reduced technical obstacles, and access to sophisticated technologies.

- It can offer infrastructure, platform, or software services and can be deployed privately, publicly, or in a hybrid manner.

- The biggest category is Software as a Service (SaaS). It eliminates the need for users to maintain their own infrastructure, instead allowing access to software offered as a service.

- CRM, analytics, and AI-driven applications are common use cases for SaaS. Notable vendors are Salesforce, Microsoft, Adobe, and SAP.

- Following next is Platform as a Service (PaaS), which provides tools for the creation of applications, including operating systems, databases, and programming languages.

- Notable vendors are Microsoft Azure, AWS, Google Cloud, and IBM Cloud. Although it is the fastest-growing cloud segment, it remains the smallest.

- The IaaS (Infrastructure as a Service) model offers storage, servers, networking, and virtual machine services as remotely managed solutions.

- It is smaller than the SaaS market but is expanding due to a slowdown in traditional IT infrastructure.

- Amazon dominates the market with close to 50% of the global share, followed by Microsoft and then Alibaba.

(Source: statista.com)

- As per Statista, cloud computing statistics show that cloud infrastructure is highly competitive, but Amazon Web Services (AWS) maintains its lead, capturing roughly 30% of the global market in the second quarter of 2025.

- Following is Microsoft’s Azure with a 20% share, and Google Cloud with 13%.

- These three, in unison, cover over 60% of the market, leaving the rest of the competitors to fight over an insignificant single-digit share.

- The quarter ending in the second quarter of 2025 witnessed a rapid increase in cloud infrastructure spending, as it climbed to US$99 billion, marking a 25% increase or more than US$20 billion increase over the same period in 2024.

- For the entire year of 2025, it is anticipated that revenues from these services will exceed the US$400 billion mark, illustrating the stiff competition for what is becoming an incredibly lucrative market.

- The cloud market is enormous, and there is still a lot of room for expansion. In fact, growth has picked up in the last few quarters, primarily fueled by the rise in artificial intelligence and the intense computing power it demands.

- In the second quarter of 2025, AI-focused cloud services expanded twofold. This not only intensified the growth of such services but also further expanded the range of cloud services offered.

Cloud Computing Revenue Drives From Microsoft

(Reference: statista.com)

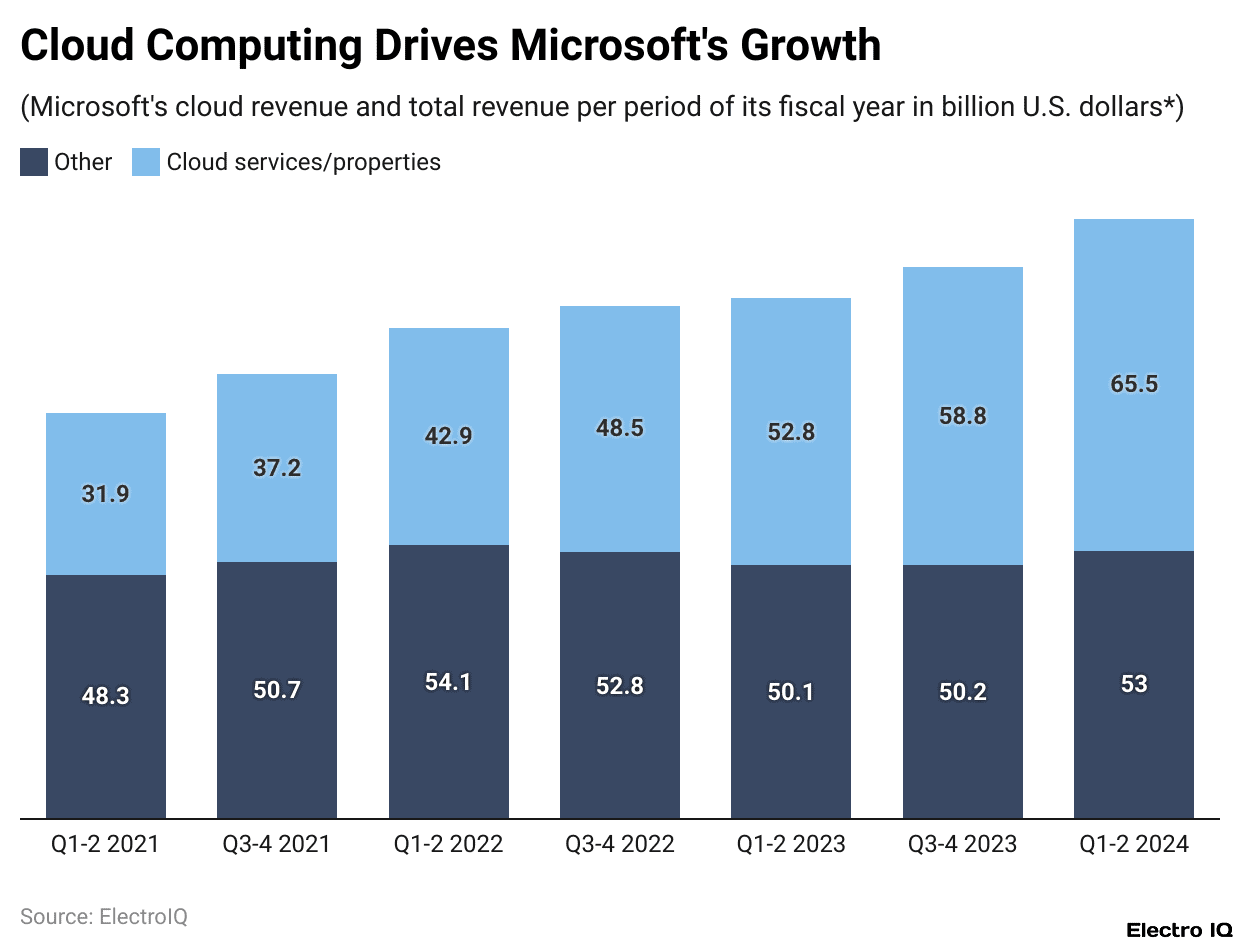

- Though Microsoft’s most popular consumer product remains Microsoft 365, the company has vigorously pursued growth with its cloud services.

- In the second half of 2023, Microsoft secured US$118.5 billion in revenue. From that, US$65.5 billion, or 55%, stemmed from cloud services.

- That percentage has been on the rise: it stood at 41% in the same period in 2021, rose to 46% in 2022, and surpassed 50% in 2023.

- This marks the increasing abandonment of old, on-site systems for cloud ones.

- Between fiscal years 2021 and 2024, Microsoft’s cloud revenue more than doubled thanks to customer demand and its partnership with OpenAI.

- With the goal of implementing OpenAI’s sophisticated AI model GPT-4 into its products, Microsoft further invested US$13 billion in OpenAI in January 2023.

- As of now, Windows 11, Microsoft 365 for Enterprise, GitHub, and Bing — each leveraging Azure cloud infrastructure — have integrated AI features and are utilizing OpenAI’s services.

- This approach implies that Microsoft’s cloud division is anticipated to be pivotal for the company’s future achievements.

- Gartner report on cloud computing statistics claims that the spending of end users on public cloud services is projected to be close to US$679 billion in the year 2024, with Google Cloud, Amazon’s AWS, and Microsoft being the leading vendors.

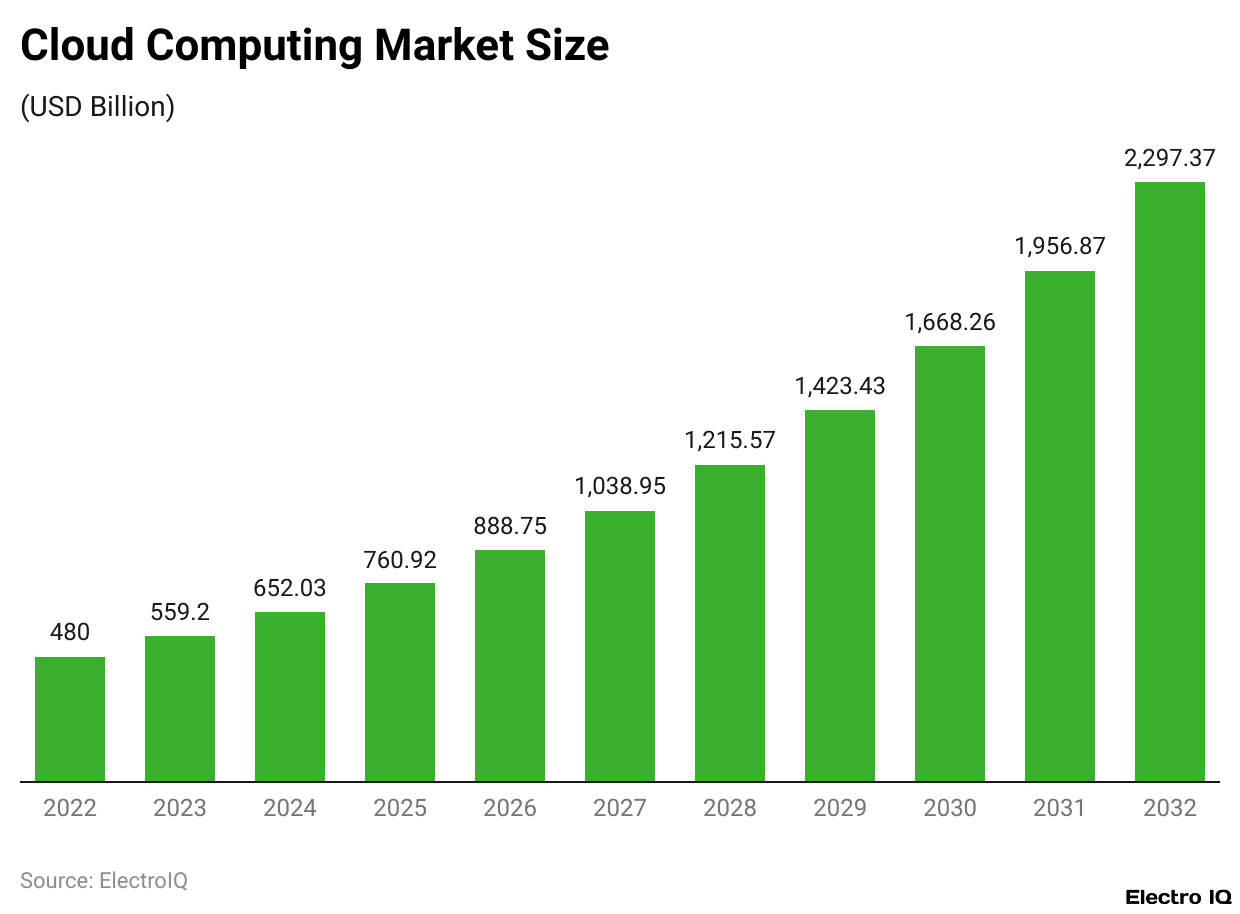

Cloud Computing Market Size

(Reference: edgedelta.com)

- The worldwide cloud computing market has been growing swiftly. It was worth US$446.51 billion in 2022 and increased to US$500 billion in 2023.

- Predictions indicate that it will continue to rise, surpassing US$1 trillion in 2028 and hitting approximately US$1.6 trillion in 2030.

- Researchers project it will keep a solid pace with a compound annual growth rate of 17.43% until the year 2032.

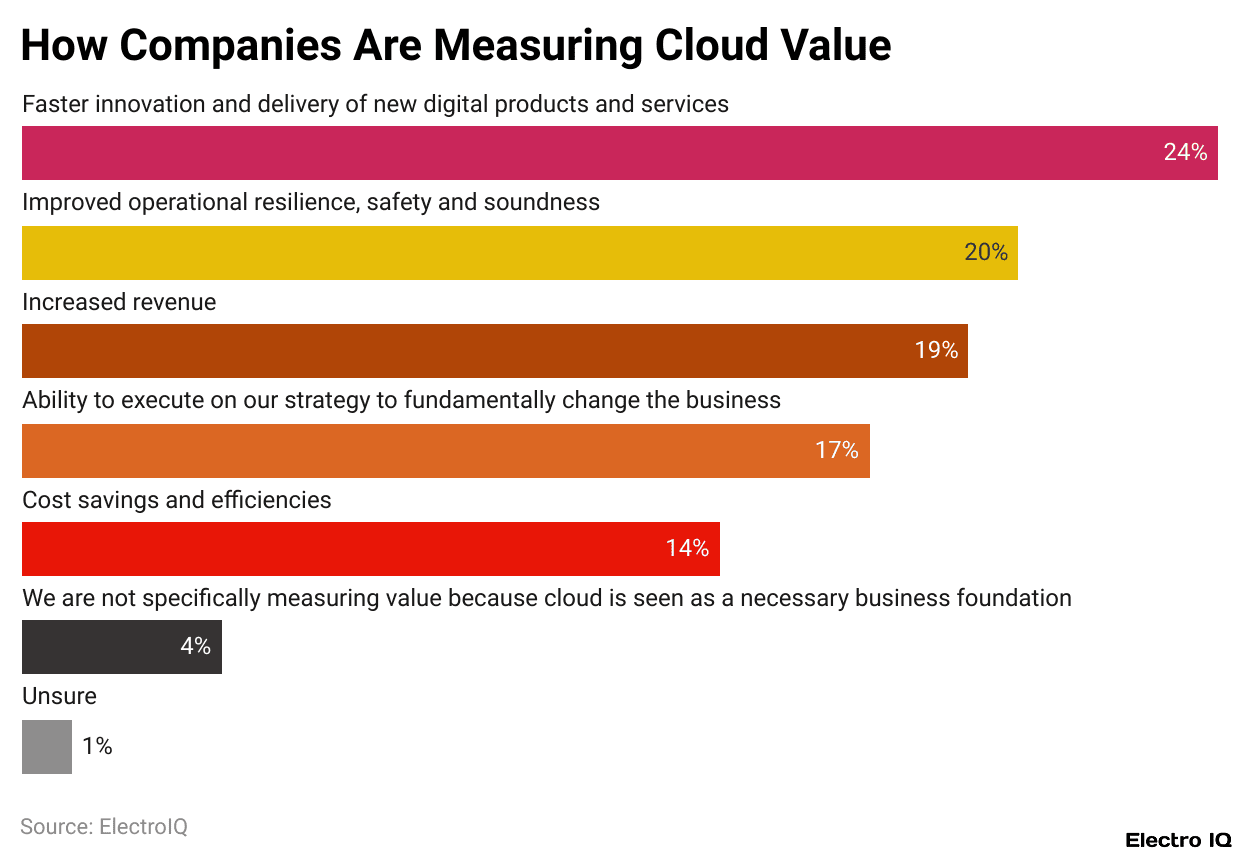

Cloud Computing Value

(Reference: cloudzero.com)

- In a PwC survey on cloud computing statistics that included 524 technology leaders from Fortune 1000 companies.

- 126 respondents (or 24%) indicated that the primary advantage of cloud computing was its ability to foster innovation faster and speed up the launch of new products and services.

- This was the leading value driver of cloud computing, with enhanced operational resilience ranked second.

Global Cloud Computing Data By Region

Europe

- The IT and business services sector in the EMEA region generated about US$350 billion in 2022, rising to around US$360 billion in 2023.

- Within this, the European cloud computing market alone was valued at US$63 billion in 2021.

- A survey showed that 58% of European organisations reported “heavy” cloud usage, which is slightly below the global average of 63%.

- Interestingly, 65% of companies said their cloud use was higher than they initially planned, partly due to the pandemic accelerating adoption.

- European organisations experience several challenges with cloud adoption.

- The most significant challenge is the evaluation of technical feasibility at 51%, followed by a 49% understanding of application dependencies, and 44% for comparing cloud and on-premises costs.

- Workload migration (69%), coupled with improving current cloud usage (68%) and the adoption of the cloud-first strategy (47%), continues to be the main cloud priorities.

North America

- In the United States, the market for cloud computing was valued at US$92.4 billion in 2019, with US$56.6 billion or 61.3% of that revenue coming from SaaS solutions.

- With 37% of organisations having experienced an audit failure or data breach that was cloud-related in the previous year, security still remains an issue.

- The rate of cloud adoption is accelerating in the healthcare sector.

- The U.S. is expected to lead this expansion, which is projected to grow by US$25.54 billion between 2020 and 2025.

- Cloud computing in U.S. healthcare alone is forecasted to increase by 40% in the same timeframe.

South America

- Cloud computing in South America witnessed a CAGR of 22.4% between 2019 and 2023, with PaaS exhibiting even greater expansion of 30.1%.

- In 2021, Argentina’s IT market was estimated to be worth US$10.18 billion, and SaaS being the biggest segment, it is predicted to reach US$15.03 billion by 2026 at a CAGR of 8.1%.

- The demand for cloud storage is increasing all over the world, including Latin America, where the cloud storage services were worth US$2.3 billion in 2021 and are predicted to further increase to US$145 billion by 2026.

- This is mainly attributed to the increasing data requirements and the cost benefits of cloud storage compared to traditional storage.

Africa

- Cloud computing is still in its early stages on the continent, but it is steadily growing.

- In 2021, Nigerian government agencies hosted over 70% of their data overseas in countries such as the UK, the USA, and Ukraine.

- On the continent, there is a tech hub count of 643, with the business hubs in Nigeria (90), South Africa (78), and Egypt (56) taking the lead.

- The movement toward cloud and serverless computing is projected to yield revenue of about US$2 billion in 2024.

- While the public cloud spending for Africa is less than 1% on the global scale (as per 2018), the promise is great with enterprise and wholesale markets valued at over US$10 billion.

- From the US$100 million that IBM invested in the African Development Centre in 2019.

- Azure data centres in South Africa, with the opening of their first African data centre in Cape Town in 2020.

- AWS has shown that it is committed to the continent. Public cloud services from Huawei also marked the entrance of the company into the African market.

Asia-Pacific Region

- The Asia-Pacific region is notable for its rapid cloud market growth.

- As of the third quarter of 2022, China’s cloud infrastructure investment topped US$7.8 billion, which is 12% of the total global expenditure for the quarter.

- The market is led by regional players: Alibaba Cloud (36%), Huawei Cloud (19%), Tencent Cloud (16%), and Baidu AI Cloud (9%), whose combined market share is 80%.

- In Australia, 87% of infrastructure decision-makers subscribe to at least one cloud service, 70% subscribe to hybrid clouds, and 59% to multiple public clouds.

- These figures look even better in India, where the number is at 91%.

- Across the board, Asia-Pacific public cloud revenue is expected to increase from US$51.2 billion in 2021 to US$165.2 billion in 2026 at a CAGR of 26.4%.

- The forecast for Asia’s cloud revenue by 2027 stands at US$225.55 billion.

- The region possesses 37% of the world’s cloud data centres, with expansions currently in progress in Vietnam, Thailand, and Malaysia.

- In 2022, Google also declared new data centres in Thailand, Malaysia, and New Zealand.

United Kingdom

- 46% of the population uses cloud storage.

- The UK cloud market was worth £41bn (US$48.5bn) in 2022, with an expected swell to £59bn (US$69.9bn) by 2024.

- Public cloud revenue was US$15.57bn, expected to increase to US$20.03bn in 2023.

- The SaaS segment leads, expected to hit US$12.66 billion in 2023.

- During 2023, a company was on average expected to pay US$565.50 in cloud services for every employee.

- Even with the remarkable adoption, 36% of organisations have had either a failed audit or a cloud-related data breach in the last year.

Cloud Storage And Usage

- Storage in the Cloud has become central in data management businesses, with companies of all sizes depending on it.

- Today, 94% of businesses use cloud computing, indicating that it is now ubiquitous. AWS and Microsoft Azure are the leading public cloud providers.

- Nearly 74% of companies use public cloud services as a data warehouse, and 60% use managed service providers to assist in managing these systems.

- Businesses integrating generative AI as a public cloud service in 2025 marked a new milestone in AI trends in the cloud ecosystem.

- Data from cloud storage is most often recovered for backup and recovery, with most businesses doing so at least once a month.

- Usage of cloud services is still not universal, with only 44% of classic small-scale enterprises making use of cloud infrastructure or hosting services.

- On the personal front, users are accessing an average of 36 cloud-based services daily, including applications and storage services.

- The U.S. and Western Europe dominate the cloud computing software market, whereas nearly 39% of firms in Central and Eastern Europe, as well as Sub-Saharan Africa, remain in the cloud adoption assessment or planning phase.

Cloud Computing Cost

- Cloud computing offers strong returns, but its cost is steep and often unpredictable.

- Depending on the business’s requirements, the services could cost from US$50 to above US$500 per month, and worldwide expenditures on public, private, and hybrid cloud services are estimated to be US$1.3 trillion by 2025.

- Though the costs might be steep, the returns tend to be worth it. More often than not, enterprises stand to triple the value of their migration, with US$3.86 being the average return on every dollar invested.

- Storage goes on to account for the largest single chunk of expenses, making up 49% of the total cloud fees.

- The most problematic issue greatly affects businesses—it is the continued management of cloud spending.

- More than half of the public cloud storage spending is reported over budget, doing so is 62%, and the overall increase in cloud costs of the companies stands at 59%, both in the past year.

- Such dissatisfaction with pricing is typical, as there is anger towards the steep fees and non-existent transparency that cloud providers exhibit.

- For controlling such issues, 82% of enterprise teams believe that automated methods are a must in order to optimise cloud costs and maintain ROI.

Cloud Computing’s Role In Business

- Almost all businesses have adopted cloud computing, with 98% of them having SaaS products or fully cloud-native environments.

- A dramatic rise has been noted in spending on cloud infrastructure, which is estimated to have gone up by 23% in 2023.

- Usage intensity has also shifted; in 2022, 63% of professionals reported “heavy” use of cloud services, as opposed to 59% in 2021 and 53% in 2020.

- As cloud adoption becomes increasingly complicated, companies are starting to use tools to oversee and secure their services.

- Larger companies, especially those with over 10,000 employees, are spearheading this trend.

- For example, 41% of them use multi-cloud security tools versus the 32% average, and 37% use multi-cloud cost management tools versus 31% overall.

- The impact is huge in terms of finances. Spending by end users for public cloud services is an estimate of nearly US$600 billion for 2023.

- SaaS accounting for the largest share of US$208 billion, followed by IaaS at US$156.2 billion and PaaS at US$136.4 billion.

- More than half of the businesses feel that their cloud spending is inefficient, with 52% of the professionals stating that the cloud cost optimisation received more attention in 2022 than in prior years.

- It is surprising to note that less than half (46%) of people think their cloud costs are well-optimised, and this decreases further to 32% in businesses where engineering teams are not responsible for cloud spending.

- This is yet another indication of the misalignment between cloud adoption and cost optimisation, at the very time when businesses are increasing their dependence on cloud technology.

Cloud Adoption Statistics

- Unlike running an exclusive cloud provider, most organisations engage in multi-cloud strategies.

- In 2022, 753 organisations were surveyed, out of which 89% disclosed the use of more than one cloud for storage and workloads.

- 9% used a single public cloud (up from 8% in 2021), and only 2% was on a private cloud.

- Among multiplatform users, 80% preferred a hybrid with a combination of public and private clouds. Lesser proportions were on multiple public (7%) or private (2%) cloud only.

- Looking further, 48% use a combination of multiple private and multiple public clouds, 31% use multiple public and one private.

- 12% use one public and multiple private, and 9% use a single public and single private clouds.

- The relevance of cloud technology adoption became even more apparent with the COVID-19 pandemic.

- By 2024, it is anticipated that an average of 80% of IT budgets will be spent on cloud technologies.

- While there is a small percentage (9%) of companies that lower their annual cloud budgets after the pandemic, their numbers are eclipsed by the 65% that raise their spending.

- This shows, to an even greater extent, that over 50% of companies are moving more applications to the cloud, which indicates the immense value it offers for recovery and expansion.

Conclusion

Cloud Computing Statistics: Innovation, along with business growth and digital transformation, cloud computing is still leading the charge. The industry, which has managed to generate over US$500 billion in revenue, is set on reaching US$1.6 trillion by 2030, with no signs of stopping. The industry is still dominated by AWS, Azure, and Google. Companies are increasingly adopting multi-cloud and hybrid cloud strategies.

The AI-driven, and more specifically, generative AI, demand has sped up infrastructure innovation and spending. All the while, ROI and agility improvements remain strong, even with the elevated costs and budget constraints. As companies across the globe allocate more funds from their IT budgets to the cloud, it continues to be a pivot for technology and business strategy.

FAQ.

Looking at the cloud computing market on a global scale, in 2023 it was valued close to US$500 billion, with expectations to exceed US$1 trillion by 2028 and reach US$1.6 trillion by 2030. The cloud computing market is witnessing an increasing CAGR of more than 17%, which is now associated with generative AI, the need for cost-effective scalability, and efficiency on a cross-industry basis.

By the second quarter of 2025, Amazon Web Services (AWS) took about 30% of the global cloud infrastructure market, followed by Microsoft Azure at 20% and Google Cloud at 13%. Combining their shares, those three tech companies had more than 60% of the market, while other companies such as Alibaba and IBM had noticeably smaller portions.

One of the significant factors that contributes to the adoption of the cloud platform is AI. In the second quarter of 2025, AI-focused cloud services offered a 140 to 180% growth, which is well above the general market growth. The generative AI models, such as OpenAI’s GPT series, required computing power turned to infrastructure and service offered to major providers, namely AWS, Azure and Google Cloud, which greatly increased in demand.

Cloud services have been used by 98% of organisations, so nearly every organisation has adopted them. 89% of organisations implement multi-cloud strategies, which mix both public and private providers to enhance flexibility and resilience. On the other hand, traditional small businesses seem to be lagging behind, as only 44% of them use cloud infrastructure.

Cost management emerges as the primary concern. Despite an average ROI of US$3.86 for every US$1 invested in cloud technology, 62% of businesses report exceeding their budget on cloud storage, and 59% report an increase in total costs in the last year. In addition, a great number of enterprises continue to have issues with pricing transparency and effective cloud expenditure, which makes cost optimisation tools, along with automation, a necessity.

I hold an MBA in Finance and Marketing, bringing a unique blend of business acumen and creative communication skills. With experience as a content in crafting statistical and research-backed content across multiple domains, including education, technology, product reviews, and company website analytics, I specialize in producing engaging, informative, and SEO-optimized content tailored to diverse audiences. My work bridges technical accuracy with compelling storytelling, helping brands educate, inform, and connect with their target markets.