SYM Statistics By Global Growth And Market Impact (2026)

Updated · Jun 04, 2026

Table of Contents

- Introduction

- Editor’s Choice

- SYM Taiwan’s Largest Motorcycle Manufacturer in 2025

- SYM Revenue

- SYM Motors: A Decade of Rising Profits and Consistent Shareholder Returns

- SYM Motors Earnings Per Share Profitability

- SYM vs. Kymco: The 2025–2026 Market Share Battle

- SYM EV Transition and Battery-Swapping Reality

- Conclusion

Introduction

SYM Statistics: SYM, the flagship label of the Taiwan-based Sanyang Motor Co., Ltd., kicked off 2025–2026 as one of the world’s most successful scooter makers. During the last ten years, the company has moved from a regional player to a global two-wheeler leader, and it has also kept tightening its grip across Taiwan, Europe, Latin America, Africa, and Southeast Asia.

Even with tough conditions in Europe and tougher rivalry from Japanese, Chinese, and electric vehicle brands, SYM still managed to hold steady growth in registrations. It also preserved domestic market leadership and brought in more than USD 2 billion in annual revenue. Their premium scooter approach, bigger manufacturing scale, and the constantly widening international presence keep SYM among the more influential names in global urban mobility.

Editor’s Choice

- In 2025, SYM logged 544,790 worldwide vehicle registrations, and that was up 1.4% YoY, even with rougher market conditions around it.

- Over the past decade, global registrations rose from about 250,000 units to well over 544,000, so overall sales volume more than doubled.

- SYM has stayed in Taiwan’s No.1 motorcycle place since 2022, beating Kymco.

- Taiwan registrations in 2025 rose 1.2%, helping SYM keep its top position at home.

- In Europe, registrations slipped only 1.3%, which suggests a bit more staying power than a lot of competitors saw in a weak market period.

- Latin America became SYM’s fastest-growing region, with registrations jumping 60.8% YoY.

- In Africa, registrations grew 27.5% YoY, and that underlines why the continent matters so much as a growth destination.

- Sanyang Motor has built more than 17 million motorcycles, scooters, and ATVs worldwide.

- SYM basically makes over 1 million two-wheelers each year, and it brings in more than USD 1 billion in annual sales too.

- In January–April 2026, the consolidated revenue hit NTUSD 20.26 billion, with a small drop, around 2.84% year over year.

- The net income story is pretty big… it moved from a NTUSD 322 million loss in 2016, to a NTUSD 4.53 billion profit in 2025.

- The dividend per share went from NTUSD 1.03 back in 2016 up to NTUSD 3.00 in 2025, and the payout ratio ended up at 52%, which is not small.

- In Q1 2026, EPS was NTUSD 1.37, down 11% YoY. Meanwhile, pre-tax income dropped 15.3% YoY to NTUSD 1.40 billion.

- SYM held 44.3% of Taiwan’s motorcycle segment in 2025, while Kymco had 25.9%, giving SYM an 18.4 percentage point lead.

- Gogoro then saw 2025 vehicle sales slide 37.6% to 28,000 units, and revenue also fell 9.4% to USUSD 281.5 million.

SYM Taiwan’s Largest Motorcycle Manufacturer in 2025

- SYM reinforced itself as the biggest Taiwanese motorcycle maker in 2025, with 544,790 global vehicle registrations logged that year, which is basically a 1.4% year on year uptick even while conditions felt tough across multiple international markets.

- Over the past ten years, the company has also kept a pretty remarkable growth path, since global registrations moved from roughly 250,000 units to well above 544,000, so yeah, the numbers nearly double, and it really shows how well its worldwide expansion strategy is landing.

- SYM has been leading Taiwan’s motorcycle market since 2022, a kind of milestone moment, after it passed longtime local rival Kymco and then further locked in its dominance at home.

- Taiwan stayed among SYM’s most solid markets in 2025, with registrations up 1.2%, letting the company hold onto leadership without too much stress.

- Europe is still a major pillar in SYM’s global business, and even though the European motorcycle market was pretty soft in 2025, SYM’s registrations only slipped 1.3%, which reads like resilience, plus strong brand loyalty.

- Registrations jumped 60.8% in Latin America, and rose 27.5% in Africa. This quick lift basically mirrors the wider global acceptance of SYM’s lineup, and not just within the usual Asian comfort zone.

- North Africa and the Maghreb area have turned into especially relevant growth engines, helping to spread out income and lessen reliance on more mature markets.

- Started in 1954, in Hsinchu, Taiwan, Sanyang Motor has basically built up a long story, over seven decades, going from a local maker into a real global two-wheeler powerhouse.

- Back in 1962, a big partnership with Honda kicked things off, and it helped enable production of Taiwan’s very first locally assembled motorcycles. That moment basically set up the industrial growth for SYM, and you can still see the momentum in how they operate today.

- Since the beginning, the company has put together more than 17 million motorcycles, scooters, and ATVs, which really shows a notable contribution across the global two-wheeler world.

- At the moment, SYM brings in annual revenues above USD 1 billion, and it turns out more than 1 million two-wheelers every year, so it reflects strong manufacturing scale, plus solid operational efficiency too.

- Sanyang Motor has around 2,400 employees worldwide and keeps production facilities in Taiwan, China, and Vietnam, while supported by subsidiaries in the United States, Italy, Germany, and China.

- SYM’s strategic turn toward hybrid models should help the company catch the rebound in market demand through 2027 and 2028.

SYM Revenue

(Reference: sanyang.com)

- SYM’s 2026 consolidated revenue report gives a sort of mixed but still useful view into how the company did during the first four months of the year.

- In the SYM 2026 Monthly Consolidated Revenue Report, total revenue for January through April 2026 came to NTUSD 20.26 billion, which is a 2.84% drop year-on-year. Even with that overall decline, monthly results feel pretty uneven, and that really points to shifting consumer appetite across Taiwan and export destinations, more than anything.

- January seemed to kick things off the best. Revenue was NTUSD 5.35 billion, up 16.22% YoY, and that signals solid demand along with fairly active dealer movement right at the start. Then the pace didn’t last.

- February fell to NTUSD 4.09 billion, down 10.75% YoY, which likely ties back to softer market conditions and less selling time during the month.

- March bounced back to NTUSD 5.57 billion, actually the top figure across that period, but it still slipped by 5.56% versus the prior year.

- April was NTUSD 5.25 billion, down 8.90% YoY, and it lines up with the broader slowdown you can also see in Taiwan’s motorcycle market.

- If you crunch it a bit, March likely contributed around 27.5% of the overall revenue from those four months, and January made up about 26.4%.

- So overall, SYM kept a relatively even revenue distribution, despite the market doing these twists and turns.

- The modest 2.84% decline looks kind of manageable, especially when you put it next to the sharper contraction that’s been reported across several areas of Taiwan’s motorcycle industry in early 2026.

- Overall, the figures still make it seem like SYM is financially stable and also well-positioned to defend its market leadership.

- Even so, slower domestic demand along with weaker momentum in electric scooter sales is adding pressure, but the company’s diversified product line-up and a strong brand presence keep acting like a sturdy base for a recovery later in 2026.

(Source: sanyang.com.tw)

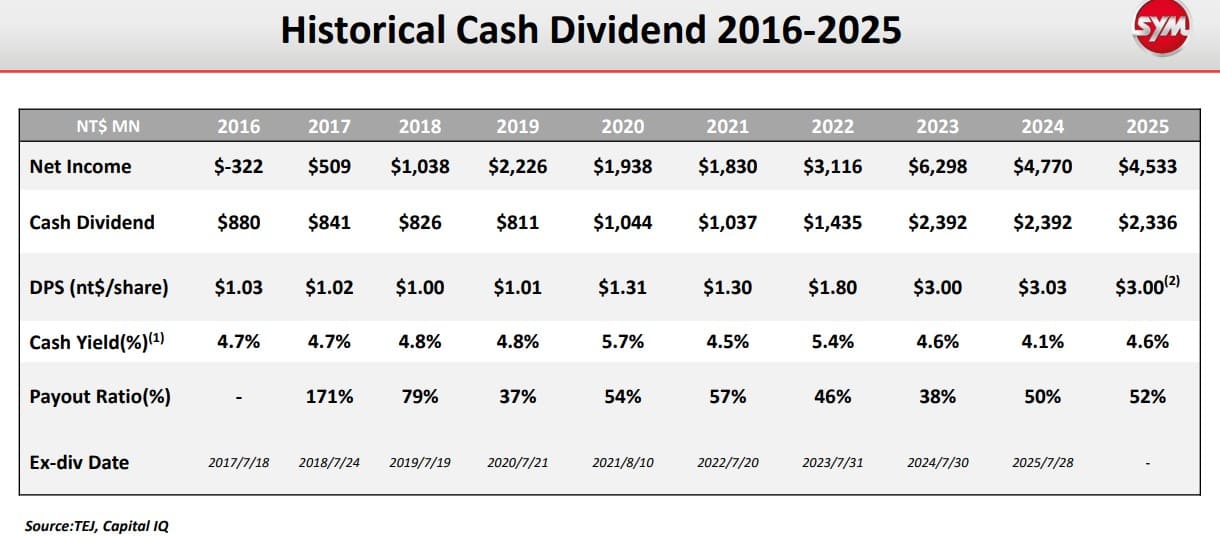

- SYM Motors’ dividend and earnings record from 2016 up to 2025 shows a company that has, kind of, managed to keep profitability, expansion, and shareholder rewards in a workable balance. The numbers feel like a “grown-up” maker that has gradually improved its financial standing while still running a pretty solid cash-return approach.

- The most eye-catching shift is net income. It moved from a loss of NTUSD 322 million in 2016 to a gain of NTUSD 4.53 billion in 2025. That’s a big reversal, and it suggests SYM’s margins have been expanding, its market position has been reinforced, and its day-to-day operations have gotten better.

- The firm hit a peak profit of NTUSD 6.30 billion in 2023, then it softened to NTUSD 4.77 billion in 2024 and NTUSD 4.53 billion in 2025.

- Cash dividends increased from NTUSD 880 million in 2016 to NTUSD 2.34 billion in 2025, while Dividend Per Share (DPS) nearly tripled from NTUSD 1.03 to NTUSD 3.00 during the same stretch. This steady rise in payouts hints that management has real faith in ongoing cash production, not just short-term optics.

- Another signal worth noting is cash yield. It stayed fairly steady across the decade, hovering around 4.1% to 5.7%.

- In 2025, shareholders effectively got a 4.6% cash yield, so SYM looks like an option for income-minded investors who care about consistency more than fireworks.

- Finally, the payout ratio was 52% in 2025. For context, it was 38% in 2023 and 50% in 2024, meaning SYM still sends back about half of earnings to shareholders while keeping enough funding capacity for future growth, and for product development too.

- Overall, the numbers portray SYM as a financially disciplined company with a proven ability to generate profits, reward investors, and maintain long-term stability.

- In a competitive global motorcycle industry, this combination of earnings strength and dividend consistency remains one of SYM’s key investment advantages.

(Source: twse.com.tw)

- SYM Motors’ latest quarterly earnings data basically point to a company that is still profitable, but it seems to be sliding into a more normal phase after several years of truly exceptional growth.

- The results suggest SYM keeps producing decent earnings, though the momentum we saw in 2022–2024 is no longer as sharp, with softer motorcycle demand and a tougher market environment in the background, or something like that.

- As per the Taiwan Stock Exchange (TWSE) Market Observation Post System (MOPS), Q1 2026 earnings per share (EPS) landed at NTUSD 1.37, vs NTUSD 1.54 in Q1 2025. That’s roughly an 11% year-on-year dip.

- Also, income from continuing operations before tax fell from NTUSD 1.65 billion in Q1 2025 to NTUSD 1.40 billion in Q1 2026, down around 15.3%, if you look at it plainly. (Source: SYM Quarterly Financial Statements)

- Annual EPS grew from NTUSD 2.30 in 2021 to a high point of NTUSD 7.95 in 2023, then cooled off to NTUSD 6.02 in 2024 and NTUSD 5.78 in 2025.

- In the same way, pre-tax income rose from NTUSD 2.34 billion in 2021 to NTUSD 8.08 billion in 2023, which kind of underlines the strength of SYM’s core operations during the post-pandemic surge period. (Source: SYM Investor Relations Data)

- The Q1 2026 pre-tax income of NTUSD 1.40 billion remains nearly 84% higher than the NTUSD 761 million shown in Q1 2021, so the earnings foundation has clearly become stronger over these last five years.

- In 2026, it looks more like a transition year than a clear downturn or something like that. Even if earnings are feeling some pressure due to weaker motorcycle demand in Taiwan and slower overall industry growth, SYM seems to keep its footing—solid profitability, decent cash generation, and, in general, market leadership.

- So overall, the company still comes across as financially resilient and kind of well-positioned to benefit once conditions start improving again.

|

Metric |

SYM (Sanyang Motor) | Kymco | Analyst Insight |

| Taiwan Market Share (2025) | 44.30% | 25.90% |

SYM led the Taiwanese scooter market with an 18.4 percentage-point advantage, creating a significant competitive gap over Kymco. |

|

Market Position (2025) |

1st | 2nd | Nearly 1 out of every 2 scooters sold in Taiwan carried a SYM badge, reinforcing its dominant position. |

| Early 2026 Sales Performance | -4.20% | -21.50% |

SYM showed strong resilience during a declining market, while Kymco experienced a much steeper contraction. |

|

Competitive Gap (2025 Share) |

44.30% | 25.90% | SYM’s market share was approximately 1.7 times larger than Kymco’s. |

| Youth-Oriented Scooter Focus | Strong emphasis on 125cc–300cc lifestyle scooters | More premium and technology-focused offerings |

SYM successfully captured younger riders through aggressive pricing and modern features. |

|

Electrification Approach |

Gradual integration of EV models while maintaining ICE leadership | Early EV push through Ionex battery-swapping ecosystem | Kymco pioneered EV technology, but SYM achieved stronger overall market traction. |

| Performance During Market Downturn (2026) | Limited decline despite market contraction | Significant volume loss |

SYM demonstrated stronger inventory management and brand pull during weak demand conditions. |

|

Strategic Strength |

Scale, pricing power, strong domestic base, export growth | Technology leadership in EVs, but weaker market execution |

SYM’s balanced strategy delivered superior market-share gains and financial stability. |

SYM EV Transition and Battery-Swapping Reality

- On the bigger picture, the global electric two-wheeler industry is still one of the fastest-moving mobility pockets.

- TechSci Research puts the market at USD 127.21 billion in 2025, and then forecasts USD 221.82 billion by 2031, which is roughly 9.71% CAGR. That kind of growth also implies that electrification is still a long-term mega trend, even when the short term gets noisy or volatile.

- 2025–2026 basically showed that rapid EV adoption is rarely a straight line, because consumer appetite, charging or infrastructure costs, and government incentive setups can start to tug performance in different directions.

- Gogoro, which many people once treated as the global reference point for battery swapping tech, went through one of the toughest stretches in the space.

- For the full year 2025, its revenue slipped 9.4% to USD 281.5 million, per the company’s own financial disclosures.

- The most obvious hit really came from vehicle demand, where unit sales fell 37.6% down to about 28,000 units in 2025, suggesting the consumer appetite weakened even though the tech story is still strong.

- Then in Taiwan, Gogoro’s situation looked even harsher. MotorcyclesData.com notes domestic sales dropped 44.9% year on year to 29,691 units. It’s one of those cases where leadership can erode pretty quickly once demand cools off, and everyone notices almost immediately.

- Financial pressure seems to have intensified after the company reported a net loss of around USD 122.75 million for the latest fiscal year, which really underlines the challenge of trying to balance infrastructure investments with those declining vehicle volumes.

- Even though Q1 2026 gross margin did improve to 20.4%, Gogoro still posted a USD 7.9 million net loss; profitability is still more like a medium-term objective instead of some immediate outcome.

- A rather noticeable strategic turn showed up during 2025, as Gogoro started aiming less at being only a vehicle maker and more at turning into a battery-swapping infrastructure provider.

- The wider lesson for the global EV industry is that progress after 2027 won’t depend only on better batteries or charging approaches. It will also hinge on durable business models, customer affordability, and infrastructure that scales, and this is exactly where Gogoro’s experience works as both a caution and a kind of roadmap for next-wave EV companies.

(Sources: TechSci Research, MotorcyclesData.com, Gogoro Annual Report & Q1 2026 Financial Results.)

Conclusion

SYM came into 2025–2026 from a position that looked really strong, still leading in Taiwan, while also pushing its presence a bit further internationally across Latin America, Africa, and Europe. Even though motorcycle demand felt softer, and during early 2026, there was a small pullback in revenue and earnings, the company looks financially sturdy, basically because profitability stays solid, dividends keep growing, and the footprint is spread out globally. SYM’s 44.3% share at home, plus its widening advantage over Kymco, suggests the pricing, product mix, and distribution approach is working well.

Looking forward, SYM seems to be leaning into hybrid mobility, continued export expansion, and a more measured shift toward electrification, so it can ride the broader two-wheeler growth wave through 2027 and even after that.

Sources

FAQ.

SYM logged 544,790 global vehicle registrations, up 1.4% year over year.

SYM held 44.3% of Taiwan’s motorcycle market in 2025, so yes, it stays the market leader.

SYM reported NTUSD 4.53 billion in net profit and paid a NTUSD 3.00 dividend per share in 2025.

Latin America (+60.8%) and Africa (+27.5%) were the fastest-growing regions for SYM in 2025.

Gogoro’s 37.6% drop in vehicle sales basically shows that EV progress needs sustainable business models, real infrastructure, and consumer affordability, not only the technology itself.

Barry Elad is a passionate technology and finance journalist who loves diving deep into various technology and finance topics. He gathers important statistics and facts to help others understand the tech and finance world better. With a keen interest in software, Barry writes about its benefits and how it can improve our daily lives. In his spare time, he enjoys experimenting with healthy recipes, practicing yoga, meditating, or taking nature walks with his child. Barry’s goal is to make complex tech and finance information easy and accessible for everyone.