TVS Motor Statistics By Financial And Market Insights (2026)

Updated · Jun 03, 2026

Table of Contents

Introduction

TVS Motor Statistics: TVS Motor Company, one of the fastest-growing global two-wheeler manufacturers, seems to have strengthened its stance across motorcycles, scooters, electric vehicles (EVs), and international markets in a way that feels pretty consistent. It notched up record-breaking financial and operational results, largely backed by sturdy domestic demand, the push on premium motorcycle expansion, quick EV adoption, and exports that keep getting better. Brands like Apache, Jupiter, Raider, Ntorq, and iQube are clearly doing the heavy lifting for sales, and in turn, TVS has diversified its revenue streams while also improving profitability.

Their emphasis on electrification, technology partnerships, connected mobility, and premium product development has helped them stay ahead of multiple industry peers. So, FY2025 and FY2026 turned out to be kind of landmark years, meaning record revenue, strong sales volumes, better EBITDA margins, and shareholder returns that looked notably healthy.

Editor’s Choice

- TVS Motor’s Q4 FY26 revenue from operations rose 34.1% YoY to ₹12,807.63 crore, and this basically reflects strong demand plus some market share gains too.

- Vehicle sales climbed 28.3% YoY to 15.60 lakh units in Q4 FY26, which shows the volumes staying robust.

- In Q4 FY26, EBITDA reached ₹1,634 crore, with the EBITDA margin improving to 13.1% overall.

- Net profit stood at ₹997 crore in Q4 FY26, translating into a net profit margin of about 7.8%, give or take.

- For FY26, revenue grew 30% YoY to ₹47,270 crore, highlighting sustained business expansion.

- FY26 EBITDA increased to ₹6,079 crore, and EBITDA margin moved up from 12.3% to 12.9% while still keeping momentum.

- EV sales jumped 51% YoY in Q4 FY26, making electric mobility one of TVS Motor’s fastest-growing segments. Honestly, it looks that way.

- The iQube electric scooter crossed 8 lakh cumulative domestic wholesales by December 2025, visibly reinforcing TVS’s EV leadership.

- R&D expenditure reached a record ₹1,024.95 crore in FY25, rising 59% YoY and more than doubling in two years.

- TVS exported 14,26,424 units in FY26, up 30.9% YoY, increasing export market share to 27.5%.

TVS Motors Financial Statistics

(Source: bseindia.com)

- TVS Motor delivered this really solid financial performance in FY26, showing they can scale up the operations while still staying profitable.

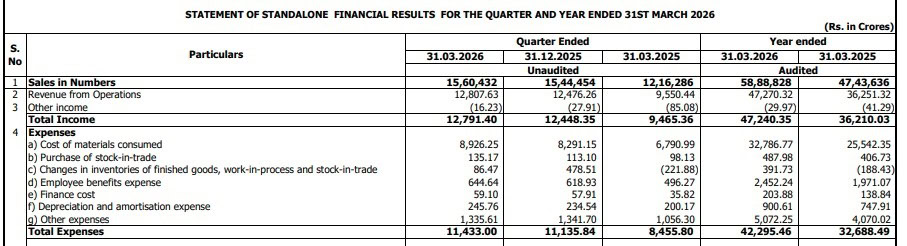

- So, as per TVS Motor Standalone Financial Results FY26, the revenue from operations for the March 2026 quarter came in at ₹12,807.63 crore.

- In March 2025, it was ₹9,550.44 crore, and that works out to a 34.1% year-on-year increase, which basically points to a widening market presence and solid product acceptance.

- Meanwhile, vehicle sales rose to 15.60 lakh units, from 12.16 lakh units a year before. That’s an increase of 28.3% in volume, and it seems the momentum is not slowing down.

- Now on profitability, total income jumped to ₹12,791.40 crore from ₹9,465.36 crore, and total expenses also went up, by 32.4% to ₹11,433 crore.

- In the Company Quarterly Statement, Profit Before Tax, or PBT, was around ₹1,375 crore. This indicates operating leverage is doing its job, and cost control is working more tightly than in earlier quarters.

- When you zoom in on costs, raw material costs made up nearly 70% of total expenses, which underlines why supply-chain management matters so much here.

- Employee benefit expenses moved up to ₹644.64 crore, and depreciation and amortization expenses increased to ₹245.76 crore. That combination also hints at continued investment in manufacturing capacity, technology, and the kinds of initiatives they plan for the next round of growth.

- Lastly, according to FY26 Financial Disclosures, finance costs increased to ₹59.10 crore but still stayed fairly contained compared with the revenue growth trajectory. So in a way, it looks like the expansion path was handled without piling on excessive financial strain, or at least not in any dramatic manner.

- Overall, TVS Motor appears to be riding a strong growth cycle. Rising sales volumes, double-digit revenue growth, and improving profitability demonstrate the company’s ability to convert market demand into sustainable earnings.

- For investors, FY26 reinforces TVS Motor’s position as one of India’s most competitive and financially resilient two-wheeler manufacturers.

(Sources: TVS Motor Standalone Financial Results FY26, Company Quarterly Statement)

TVS Motor’s Profitability

(Source: tvsmotor.com)

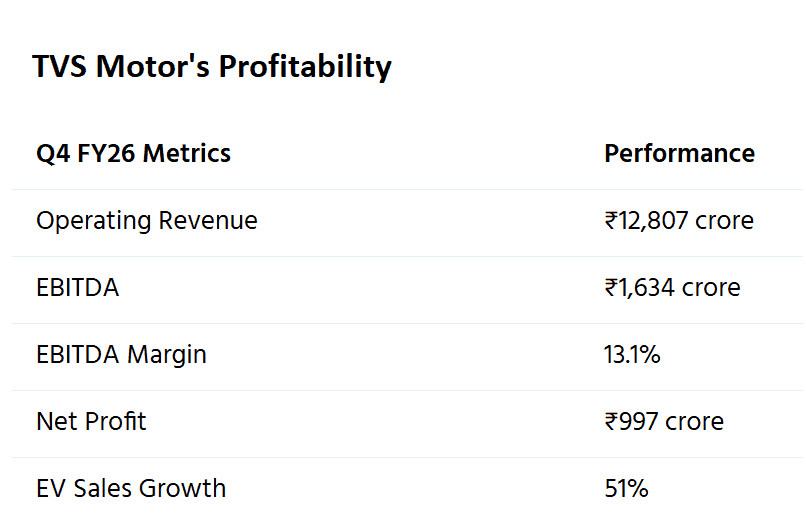

- TVS Motor showed a pretty impressive performance in Q4 FY26, kind of showing that it can grow revenue without really losing the plot on profitability.

- The quarter also feels like the company is getting a lift from strong demand, smoother operations, and better momentum in the electric vehicle (EV) space… You know, that increasing traction everyone keeps talking about.

- The main thing, the biggest highlight, is the company’s Operating Revenue of ₹12,807 crore, which in a way points to how solid its product portfolio is, and how wide its market reach can be.

- In the TVS Motor Q4 FY26 Results, it seems like the growth momentum kept going, even with a competitive auto environment around it. Higher vehicle volumes, plus better sales of premium products, and exports likely helped keep the revenue numbers this strong.

- Profitability was equally steady. EBITDA came in at ₹1,634 crore, and that translated into an EBITDA Margin of 13.1%. As per the Company Financial Disclosures, holding a double-digit margin at this kind of revenue scale suggests disciplined cost control and efficient execution.

- As per the revenue yardstick, for every ₹100 earned in revenue, TVS retained about ₹13.10 as operating profit, which suggests it’s managing growth and profitability together, not pushing one at the expense of the other.

- Net Profit reached ₹997 crore, taking Net Profit Margin to roughly 7.8%. This generally indicates that TVS converted a meaningful share of its sales into earnings for shareholders.

- From the Quarterly Earnings Presentation, the stronger bottom line was likely aided by an improved product mix and operational leverage, not just one factor, but several moving together.

- One of the more exciting metrics is that 51% growth in EV sales. It also shows TVS Motor’s expanding footprint in India’s rapidly accelerating electric mobility space.

- As mentioned in the Management Commentary and Investor Updates, the company keeps pushing money into innovation, and the EV expansion part too, to catch the next wave of opportunities.

- Overall, Q4 FY26 feels like a business running at full throttle. Strong revenue, solid margins, almost ₹1,000 crore in quarterly profit, and fast EV momentum, all of that puts TVS Motor right up there among the most energetic players in the Indian two-wheeler industry.

(Sources: TVS Motor Q4 FY26 Results, Company Financial Disclosures, Quarterly Earnings Presentation, Management Commentary, and Investor Updates.)

TVS Motor’s R&D Investment

(Reference: tvsmotor.com)

- TVS Motor’s research and development, in other words, R&D, spending hit a record ₹1,024.95 crore in FY25. That basically underlines a strong dedication toward innovation, electrification, connected mobility, and the next-generation product push.

- In the TVS Motor Annual Report FY25, R&D expenditure climbed by an impressive 59% year-on-year, going from ₹644.7 crore in FY24 and more than doubling versus ₹494.6 crore in FY23. This steep lift seems less like a short-term expense and more like an intentional investment.

- The company added roughly ₹530 crore to R&D over the past two years, which mirrors management’s attention on reinforcing its competitiveness across motorcycles, scooters, electric vehicles, and global mobility solutions.

TVS Motor’s Workforce

(Source: tvsmotor.com)

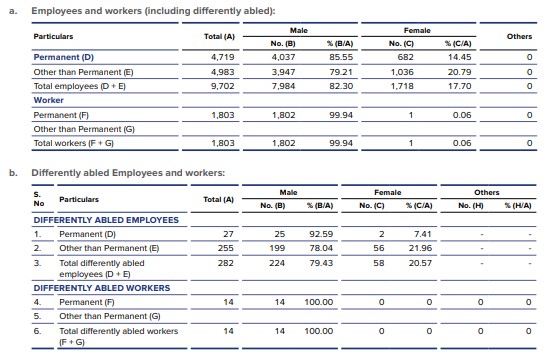

- TVS Motor’s FY25 employee data sort of points to the company’s continued emphasis on building a big, capable, and gradually more diverse workforce, so it can support its expanding global operations in a smoother way.

- As per the TVS Motor Annual Report FY25, the company had 9,702 permanent and non-permanent employees in total, made up of 7,984 men (82.3%) and 1,718 women (17.7%).

- Permanent employees came in at 4,719, with women making up 682 employees (14.45%). Meanwhile, among the 4,983 non-permanent employees, female representation was comparatively higher at 20.79% (1,036 employees).

- In a way, this indicates TVS is widening chances for women not only in operational roles but also in supporting functions, especially as production volumes move up.

- Looking at worker categories, the picture is still mostly male. There are 1,803 workers overall, where 1,802 (99.94%) are men, and just 1 (0.06%) is a woman. This is pretty aligned with broader realities in heavy manufacturing and the automotive sector, where shop-floor or plant-type positions remain predominantly male.

- One part that stands out, and honestly feels encouraging, is the company’s inclusion approach.

- The TVS Motor Annual Report FY25 records 282 differently abled employees, which is roughly about 2.9% of the total headcount. Out of these, 27 are permanent employees, and 255 are non-permanent employees.

- The report also notes employment of 14 differently abled workers separately, which suggests TVS is trying to create participation opportunities across several workforce segments, not just one lane.

- Nearly 10,000 employees make up the workforce that gives TVS the human capital it needs for scaling up, especially across motorcycles, electric vehicles, exports, and technology-led mobility solutions.

- In a sense, it’s not just hiring more people; it’s also about workforce expansion, a larger share of women, and hiring that’s more inclusive, all of which help sharpen TVS Motor’s image as a forward-looking employer and support long-term operational scalability.

(Sources: TVS Motor Annual Report FY25, Corporate Governance Report FY25, TVS Motor Sustainability and ESG Disclosures.)

TVS Motor Electric Vehicle (EV) Strategy, and FY27 projections

- TVS Motor’s electric vehicle strategy is getting there pretty quickly to being a main growth driver, with FY26 revenue climbing 30% YoY to ₹47,270 crore.

- At the same time, EBITDA moved up to ₹6,079 crore, and EBITDA margin also improved from 12.3% to 12.9%—this is often read as evidence of better EV contribution plus operational efficiency.

- In Q4 FY26, EV sales hit 1.15 lakh units, and that translated into a strong 51% year-on-year jump. So yeah, it points to faster consumer uptake of TVS’s electric mobility line.

- The TVS iQube is still the company’s key EV product, and by December 2025, it reportedly crossed 8 lakh cumulative domestic wholesales.

- There were 35,177 units dispatched in a single month, which puts it on a sensible path to getting closer to the 1 million-unit milestone across FY26–FY27.

- EVIndia data also suggests iQube passed 6 lakh cumulative sales earlier in 2025. That means TVS likely added almost 2 lakh more units within a year, a sign of steady market momentum, not exactly slowing down.

- TVS has basically picked a dual-product EV approach, in which the mass-to-premium iQube pulls the volume side while the more premium TVS X, priced close to ₹2.66 lakh, quietly (or not so quietly) boosts brand image, tech leadership, and overall ASPs.

- Total company sales clocked in at 58.9 lakh units in FY26, up about 24% YoY, and EVs are showing up among the quickest-growing pockets in the whole business.

- In just Q3 FY26, TVS moved 1.06 lakh electric two-wheelers, which is a solid 40% bump versus 76,000 units in the same quarter a year earlier, so it looks less like a short-term spike and more like a real structural trend.

- Management is likely eyeing annual EV volumes of 4–5 lakh units in FY27, and if the current pace sticks, it could even climb into the 6–7 lakh band.

- Also, the partnership with Jio-bp is widening the charging footprint, which should help adoption go wider, especially since India’s EV market is projected to expand at a 47.1% CAGR between 2022 and 2027.

- Looking ahead, more product rollouts, like new electric two-wheelers and electric three-wheelers, are expected to widen TVS’s addressable opportunity, and at the same time, keep the competitive stance strong.

- TVS seems to be moving from a more conventional two-wheeler maker into a broader electric mobility player.

- The EVs could contribute roughly 15–20% of domestic sales by FY28. That should, in turn, help the consolidated EBITDA margins drift toward the 14–15% zone, helped by a better product blend and scale efficiency, though you know how that part goes with execs speaking in cautious wording.

TVS Export Market Penetration and Global Reach

- TVS Motor has really, at this point, cemented itself as India’s second-largest two-wheeler exporter. It also keeps reinforcing its global credibility and somehow steadily extending its reach across both newer and more established international markets.

- For FY2026, TVS exported 14,26,424 units worldwide, managing a solid 30.9% year-on-year climb, which sits among the better performances for major Indian two-wheeler makers.

- The company’s export market share moved up to 27.5% in FY2026, adding 1.6 percentage points compared to FY2025. That shift has helped it hold up the clear number-two exporter status from India.

- On a broader level, India’s total two-wheeler exports hit a record 51,80,429 units in FY2026, growing 23.4% YoY. TVS, meanwhile, contributed more than one-fourth of the overall export volumes from the country.

- Even so, Bajaj Auto stayed the export front-runner, with 19,67,810 units and about a 38% market share, but TVS has been closing the gap steadily, through persistent expansion across a set of key overseas regions.

- Looking at where the momentum came from, Africa, Latin America, and APAC basically became the main growth engines for TVS. In particular, export volumes from Africa and Latin America jumped 35% YoY during Q3 FY26.

- Latin America has also turned into a sort of priority arena, with strong pull mentioned in Mexico, Colombia, and Guatemala. That demand seems to be helping diversify TVS’s international revenue base in a more balanced way.

- Africa is still viewed as a longer-term growth pillar, and this recent lift in volumes suggests consumer appetite is improving, even though inflation and currency-related hurdles remain in multiple markets.

- TVS kind of follows a region-specific product strategy, you know, it adapts motorcycles and scooters to local fuel quality, pricing needs, and actual riding conditions, rather than just exporting the domestic models straight as they are.

- The planned European entry for the Apache RTX 300 adventure motorcycle basically shows TVS wanting to move into higher margin mature markets, and go head-to-head with the more established global brands.

- During Q3 FY26, TVS apparently hit record sales of 15.44 lakh vehicles, and revenue of ₹12,476 crore, with the back up coming from solid domestic demand and a 35% jump in exports.

- Looking forward, exports may become around 25–30% of TVS’s overall two-wheeler volumes by FY28, with APAC, Africa, and Latin America still being major pillars, while Europe slowly increases its involvement over time.

Conclusion

TVS Motor delivered this kinda landmark performance in FY2025–FY2026, with a mix of record revenue, better profitability, exports, and electric vehicle growth. Somehow, the company managed to lean on strong demand inside India, pushed premium motorcycle expansion further, and rode the faster EV adoption curve to improve its competitive standing.

There were also big pushes into research and development, connected mobility, and electrification, which feels like it’s building a base for the longer-term growth. On top of that, export momentum across Africa, Latin America, and Asia-Pacific helped diversify where the money comes from, so it’s less tied to the domestic market only. With EBITDA margins climbing, EV volumes going up, and TVS Motor’s international footprint widening, it’s moving toward becoming more like a global mobility player, ready to benefit from upcoming transport shifts and electrification trends.

FAQ.

TVS Motor reported FY26 revenue of ₹47,270 crore, and that’s a 30% year-on-year jump.

TVS Motor’s EV sales grew 51% year-on-year in Q4 FY26, which is pretty much far ahead of overall industry growth, like a lot.

The TVS iQube crossed 8 lakh cumulative domestic wholesales by December 2025.

TVS exported 14,26,424 units worldwide in FY26, recording 30.9% year-on-year growth.

TVS Motor invested ₹1,024.95 crore in R&D during FY25, which was a 59% increase compared with FY24.

Joseph D'Souza founded ElectroIQ in 2010 as a personal project to share his insights and experiences with tech gadgets. Over time, it has grown into a well-regarded tech blog, known for its in-depth technology trends, smartphone reviews and app-related statistics.