Kawasaki Statistics By Revenue Growth And Market Trends (2026)

Updated · May 29, 2026

Table of Contents

- Introduction

- Editor’s Choice

- Kawasaki Heavy Industries FY2025 Financial Growth

- Kawasaki Segmented Financial Statistics

- Kawasaki Profit and Loss Statistics

- Factors Affecting Changes in Kawasaki Business Profit

- Kawasaki Heavy Industries Debt

- Kawasaki Cash Flows

- Kawasaki Market Reaction and Stock Performance

- Conclusion

Introduction

Kawasaki Statistics: Kawasaki Heavy Industries sort of rolled into the 2025–2026 stretch with solid momentum across motorcycles, defense systems, aerospace, rail transportation, and energy infrastructure. It looked like the business caught a tailwind from growing global interest in premium motorcycles, higher defense spending in Japan, and a decent uptick in industrial equipment orders. Sure, there were the usual headwinds— inflationary pressure, currency swings, and some softening in discretionary spending depending on the region—but Kawasaki still managed to hold onto revenue growth and even push profitability higher.

For 2025–2026, Kawasaki seemed to lean hard into electrification, hydrogen-related technology, premium motorcycle expansion, and defense contracts with more value, and that’s meant to set up longer-range growth across industries and mobility markets worldwide.

Editor’s Choice

- Kawasaki’s FY2025 total orders climbed to ¥2,739.1 billion, up ¥108.4 billion year over year.

- Revenue is projected at ¥2,311.2 billion, rising ¥181.9 billion vs FY2024.

- Profit Before Tax is expected to move higher to ¥145.5 billion, an increase of ¥38 billion YoY.

- Net profit attributable to owners is forecast at ¥108.1 billion, up ¥20.1 billion year over year.

- Business profit margin sits at 6.3%, and the net profit margin came in at 4.7%.

- ROIC is projected to improve from 8.0% to 9.0%, which suggests better capital efficiency.

- The assumed average USD/JPY exchange rate increased to 149.08, and that supports export profitability.

- Kawasaki’s total revenue forecast is for 8.5% growth, moving from ¥2,129.3 billion to ¥2,311.2 billion.

- Energy Solution & Marine Engineering revenue is projected at ¥433.5 billion, while profit is expected to rise to ¥55.0 billion.

- Precision Machinery & Robot division profit is expected to go up sort of fast, from ¥7.0 billion to ¥14.3 billion, which is more than 104% actually.

- Powersports & Engine revenue is forecast to jump to ¥682.8 billion, but profit is projected to fall by ¥25.1 billion, to ¥22.7 billion too.

- Foreign exchange performance got way better, moving from a ¥16.0 billion loss to an ¥18.9 billion gain.

- U.S. tariffs did not help profitability; they dragged it down by roughly ¥18.7 billion over FY2025.

- Total debt went down from ¥851.7 billion in FY2025 Q3 to ¥606.1 billion in Q4, so a drop of nearly ¥245 billion.

- Kawasaki’s shares climbed around 7.5%–7.8% after FY2026 earnings, while the trailing 12-month returns hovered near 60%–65%.

Kawasaki Heavy Industries FY2025 Financial Growth

(Source: global.kawasaki.com)

- Kawasaki Heavy Industries delivered a resilient FY2025 showing steady growth in orders, revenue, and profitability across its electronics and industrial systems activities.

- The company’s total orders received land at ¥2,739.1 billion, up by ¥108.4 billion YoY, and also ¥119.1 billion higher than the prior figure. This sort of movement points to strong market demand for infrastructure, automation, and energy-adjacent projects.

- Revenue is expected to come in at ¥2,311.2 billion, which is a rise of ¥181.9 billion year-on-year.

- Still, it sits a bit lower than the earlier view by ¥28.8 billion, implying that even if demand is staying solid, some projects might be running into delayed execution or slower customer deliveries.

- The most attention-grabbing part is the sharp push up in Profit Before Tax, climbing to ¥145.5 billion, which is a strong gain of ¥38 billion YoY.

- Net profit attributable to owners stands at ¥108.1 billion, rising ¥20.1 billion versus the previous year.

- These upgrades suggest tighter cost control and improved performance in higher-value industrial segments.

- Business profit margin is 6.3%, while net profit margin is 4.7%. For a heavy industrial manufacturer, those numbers are decent, but they also hint that higher material costs, currency swings, and supply chain overheads keep squeezing profitability, bit by bit.

- Another key statistical point is the projected ROIC (Return on Invested Capital) moving up from 8.0% to 9.0%, which signals better capital efficiency.

- Meanwhile, the average USD/JPY exchange assumption also climbs to 149.08, suggesting the company may keep gaining traction from a weaker yen across overseas sales.

- Overall, the view for FY2025 indicates Kawasaki is heading in with stronger earnings momentum and improved financial efficiency, even while wider global industrial risks still linger.

Kawasaki Segmented Financial Statistics

(Source: global.kawasaki.com)

- Kawasaki Heavy Industries gave a rather mixed, but still sort of strategically positive, FY2025 segment outlook, and it looks like growth is being pulled more and more by industrial technology, energy solutions, and robotics, not so much by the older engine-type businesses.

- The company’s total revenue is slated to rise from ¥2,129.3 billion in FY2024 to ¥2,311.2 billion in FY2025, and that comes out to an 8.5% increase, which is kind of solid.

- At the same time, business profit is also expected to improve, from ¥143.1 billion to ¥145.1 billion.

- Revenue is set to increase by ¥35.4 billion, and it should land at ¥433.5 billion, while business profit is planned to jump by ¥10.7 billion to ¥55.0 billion.

- In plain terms, this points to continued global appetite for energy infrastructure, hydrogen-related systems, and marine engineering projects. This segment is turning into one of Kawasaki’s steadier profit generators, as governments and industries keep allocating budgets toward cleaner and more efficient energy technologies.

- Another bright spot seems to be the Precision Machinery & Robot division. Revenue is projected to climb by ¥17.6 billion, and profit is basically close to doubling, moving from ¥7.0 billion to ¥14.3 billion. That indicates factory automation demand is picking up, along with industrial robotics, mainly across Asian manufacturing markets.

- The profit uptick of more than 104% YoY also signals strong operating leverage, plus better efficiency over time. (Source: Company Financial Data)

- Even if revenue is to surge by ¥73.4 billion, to ¥682.8 billion, business profit will decline sharply by ¥25.1 billion, landing at ¥22.7 billion. This hints at rising production costs, pricing pressure, or margins that are thinning out despite solid sales volumes.

- In the meantime, the Aerospace Systems segment has softer order intake, with orders dropping by ¥71.9 billion, though profitability still improves, but only a little.

- Taken together, Kawasaki’s FY2025 outlook reads like the firm is shifting toward higher-value industrial and energy operations, where technology-led divisions are increasingly steering future earnings.

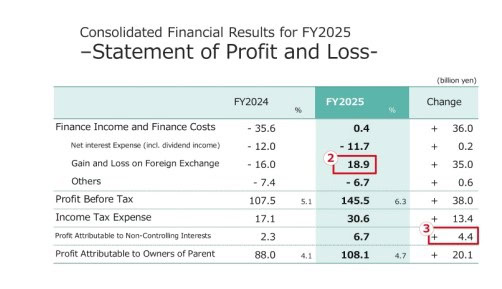

Kawasaki Profit and Loss Statistics

(Source: global.kawasaki.com)

- Kawasaki Heavy Industries came out with a pretty noticeable improvement in its FY2025 profit outlook, sort of powered a lot by foreign exchange wins and tighter, more disciplined financial management.

- The company is guiding for Profit Before Tax to climb from ¥107.5 billion in FY2024 up to ¥145.5 billion in FY2025, which works out to a solid 35.3% year-on-year jump.

- Profit margin is also expected to move higher, from 5.1% to 6.3%, so it looks like operational effectiveness across the business is getting better.

- One of the main things behind this uplift is the dramatic reversal in foreign exchange results. In FY2024, Kawasaki booked a ¥16.0 billion foreign exchange loss.

- Then in FY2025 it swung to an ¥18.9 billion gain — a positive turn of about ¥35.0 billion.

- At the same time, finance income and finance costs improved sharply, going from a ¥35.6 billion loss to a ¥0.4 billion gain, which should help support the bottom line.

- Still, as profitability rose, taxes also went up, with tax expenses increasing from ¥17.1 billion to ¥30.6 billion.

- Net profit attributable to owners of the parent company is expected to land at ¥108.1 billion, up 22.8% YoY. Profit attributable to non-controlling interests also rose by ¥4.4 billion, suggesting that the overall earnings improvement is spreading across subsidiaries.

- Overall, Kawasaki’s FY2025 outlook points toward stronger financial steadiness, where currency benefits and careful cost control help cushion global economic uncertainty, even with all the noise.

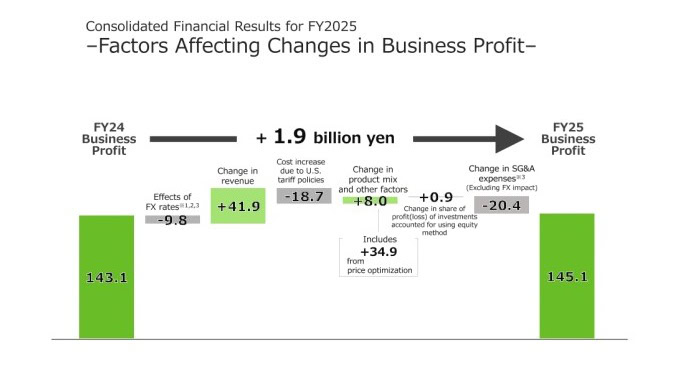

Factors Affecting Changes in Kawasaki Business Profit

(Source: global.kawasaki.com)

- Kawasaki Heavy Industries reported what looks like a modest, yet quite strategically meaningful step up in FY2025 business profit, and you can kind of see how the company managed to keep its footing through inflation, tariffs, plus foreign-exchange swings, even while the overall global picture stayed pretty rough.

- In the company’s FY2025 financial presentation, business profit rose from ¥143.1 billion in FY2024 to ¥145.1 billion in FY2025, so in the end it’s basically a net improvement of ¥1.9 billion.

- Now the main push, the one that stands out most, was stronger revenue momentum, which fed into profit improvement by about +¥41.9 billion.

- Kawasaki leaned on higher sales in its PS&E segment, covering power sports, engines, and adjacent equipment-related activities.

- They also captured benefits from product-mix adjustments and pricing tactics, which added another +¥8.0 billion. Of that total, roughly +¥34.9 billion came specifically from price optimization efforts, so it’s not just growth in volume but also smarter commercial handling.

- Put differently, Kawasaki managed to pass part of its rising cost burden along to customers without, at least in broad terms, crushing demand.

- Still, profitability did not sail smoothly. U.S. tariff policy alone was a big drag, pushing costs higher by ¥18.7 billion.

- Then, unfavourable foreign-exchange movement shaved off ¥9.8 billion from profits.

- Meanwhile, SG&A expenses climbed by ¥20.4 billion, pointing to higher operational and administrative spending throughout the business. Sources: Kawasaki Investor Presentation, Company Earnings Materials.

- Kawasaki still managed to keep overall profit growth moving, despite the pretty intense external pressure, which signals solid operational discipline and pricing power. Those are critical capabilities for a diversified industrial and heavy-electronics manufacturer operating across volatile global markets.

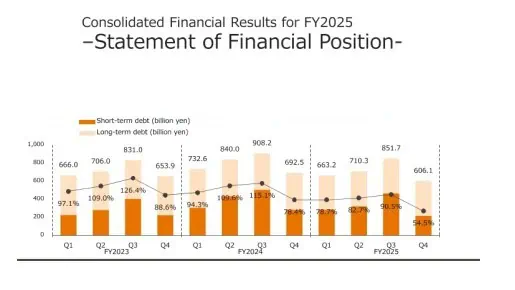

Kawasaki Heavy Industries Debt

(Source: global.kawasaki.com)

- Kawasaki Heavy Industries showed a meaningful improvement in its debt structure across FY2023 to FY2025, and that sort of signals stronger financial discipline, plus a more stable balance-sheet handling, even if the industrial setting stayed pretty volatile.

- Based on the chart included in Kawasaki’s financial materials, the company kept trimming its debt burden toward the end of FY2025, with a particularly strong move in Q4, when the debt ratio slid fast down to 54.5%. That’s a big contrast versus earlier highs that went beyond 126% in some periods.

- The pattern looks like the business is actively moving away from aggressive borrowing toward balance-sheet stabilization.

- During FY2023 and FY2024, total debt still sat on the high side, and the sum of short-term plus long-term debt even reached up to ¥908.2 billion in FY2024 Q3.

- The debt ratios kept climbing over 115%, which hints at a heavy reliance on financing while the backdrop included supply-chain disruptions, rising raw-material costs, and global interest-rate pressure.

- Still, FY2025 is where the shift shows up clearly. Total debt fell from ¥851.7 billion in FY2025 Q3 to ¥606.1 billion in FY2025 Q4, which is roughly a ¥245 billion reduction within just one quarter. This improvement may be tied to steadier cash generation, tighter control over working capital, and a more contained level of capital spending.

- The dropping debt ratio matters a lot for Kawasaki, because the company basically runs capital-intensive kinds of businesses, like aerospace, industrial robotics, heavy machinery, and energy systems.

- With lower leverage, the firm gets more financial manoeuvring space, it also cuts down on interest-cost exposure, and it can channel more resources into what’s next, meaning hydrogen infrastructure, automation, and advanced mobility technologies.

Kawasaki Cash Flows

(Source: global.kawasaki.com)

- Kawasaki Heavy Industries showed a pretty noticeable lift in how much cash it can generate between FY2016 and FY2025, and that points to a sort of enhanced operational efficiency plus a stronger financial staying power across its heavy industrial lineup.

- In the company’s financial chart, operating cash flow got to around ¥140 billion in FY2025, and honestly, that feels like one of the best marks in the last decade.

- The big thing to watch isn’t just the cash number by itself; it’s the calm, steady progress in working capital efficiency.

- Working capital jumped a lot from ¥419.2 billion in FY2016 to ¥1.09 trillion in FY2025, which signals bigger business scale, more inventory, and a broader ramp in industrial activity.

- Still, even with this larger capital base, Kawasaki kept operating cash flow in positive territory, so the firm seems to be turning sales into actual liquidity more effectively than before.

- The chart also hints at phases where spending got more aggressive. Investing cash flow stayed negative in most years, which usually means ongoing capital outlays in areas like aerospace, robotics, energy systems, transportation, and heavy-electronics infrastructure.

- Free cash flow, therefore, swung around too, and it dipped into negative territory whenever investment ramps up, like in FY2019 and FY2022. Sources: Kawasaki Annual Reports, Corporate Cash Flow Analysis.

- Operating cash flow climbed to almost ¥149 billion in FY2024, then it leveled off near ¥140 billion in FY2025. That suggests Kawasaki’s restructuring and portfolio optimisation work is starting to pay off more durably, rather than just a temporary improvement.

- For investors, this matters because strong operating cash flow gives Kawasaki greater flexibility to fund future growth areas like hydrogen energy systems, industrial automation, defense technology, and next-generation mobility without relying excessively on new debt financing.

Kawasaki Market Reaction and Stock Performance

|

Metric / event |

Indicative value (2026 context) | Interpretation of investor sentiment |

| Post‑earnings price reaction (May 12, 2026) | Stock up about 7.5–7.8% on the day after Q4/FY2026 results |

Signals strong approval of earnings quality and outlook. |

|

Q4 FY2026 EPS vs. forecast |

~¥50.6 EPS, beating consensus by ~62% | Margin and restructuring progress exceeded expectations. |

| Trailing 12‑month stock return (early/mid‑2026) | Approximately 60–65% gain; some peaks cited closer to 140% 1‑year return finance. |

Reflects a powerful rerating as restructuring gains credibility. |

|

FY2026 full‑year EPS trend |

EPS ~¥129 vs. ~¥105 prior year, +18–20% | Demonstrates structurally higher earnings power. |

| Analyst stance and target price | Consensus “Buy,” average target ~¥3,700+ vs. ~¥3,050 spot finance. |

Indicates that, even after strong gains, analysts still see upside. |

Conclusion

Kawasaki Heavy Industries kicked off 2025–2026 with profitability that looks a bit better, operational efficiency that’s stronger, and demand that’s also moving up across industrial work, robotics, energy, and defense. Even with tariffs hanging around, inflation pushing costs, and foreign-exchange swings, the firm seems to have held earnings in a firmer place, mostly by disciplined cost management, smarter pricing, and by growing the higher-value industrial side.

Robotics, hydrogen infrastructure, and energy solutions are turning into those longer-term growth engines, while motorcycles and powersports keep playing their part in maintaining the brand strength globally. Cash flows improved, debt is trending down, and ROIC is stronger, so overall financial discipline looks healthier. Analysts also point to Kawasaki’s diversified business structure, plus strategic investment into future technologies, as reasons the company should be well-positioned for sustainable industrial and mobility growth worldwide.

FAQ.

Kawasaki projects FY2025 revenue of around ¥2,311.2 billion.

Profit Before Tax is expected to climb 35.3% year-over-year to ¥145.5 billion.

The Precision Machinery & Robot division nearly doubled its profit from ¥7.0 billion to ¥14.3 billion.

Total debt slid from ¥851.7 billion in Q3 to ¥606.1 billion in Q4 FY2025.

Kawasaki shares jumped roughly 7.5%–7.8% following the FY2026 earnings announcement.

Joseph D'Souza founded ElectroIQ in 2010 as a personal project to share his insights and experiences with tech gadgets. Over time, it has grown into a well-regarded tech blog, known for its in-depth technology trends, smartphone reviews and app-related statistics.